UMH - UMH Properties: Rising Demand And Appealing Yield

2024-01-02 08:30:00 ET

Summary

- UMH Properties is a growing manufactured housing REIT that has underperformed the market but offers strong potential for value and income investors.

- UMH has a concentrated portfolio in natural gas producing regions, allowing for operating efficiencies and scalability.

- The company has demonstrated steady growth in its communities and positive demand trends, with increasing occupancy and rental revenue.

Manufactured housing is one of the most durable asset classes to own for uncertain times, and yet some names remain undervalued and haven’t seen the type of run-up that the rest of the market has experienced over the past year.

This brings me to UMH Properties ( UMH ), which I last covered here in March of 2023 with a ‘Buy’ rating, noting strong demand trends and its relative undervaluation. The stock has given a respectable 4% share price appreciation and 8.5% total return including dividends since then, but that’s still underperformed the 24% rise in the S&P 500 ( SPY ) over the same timeframe.

In this article, I provide an update on the stock and discuss why UMH remains an appealing ‘Buy’ at present for value and income, so let’s get started!

Why UMH?

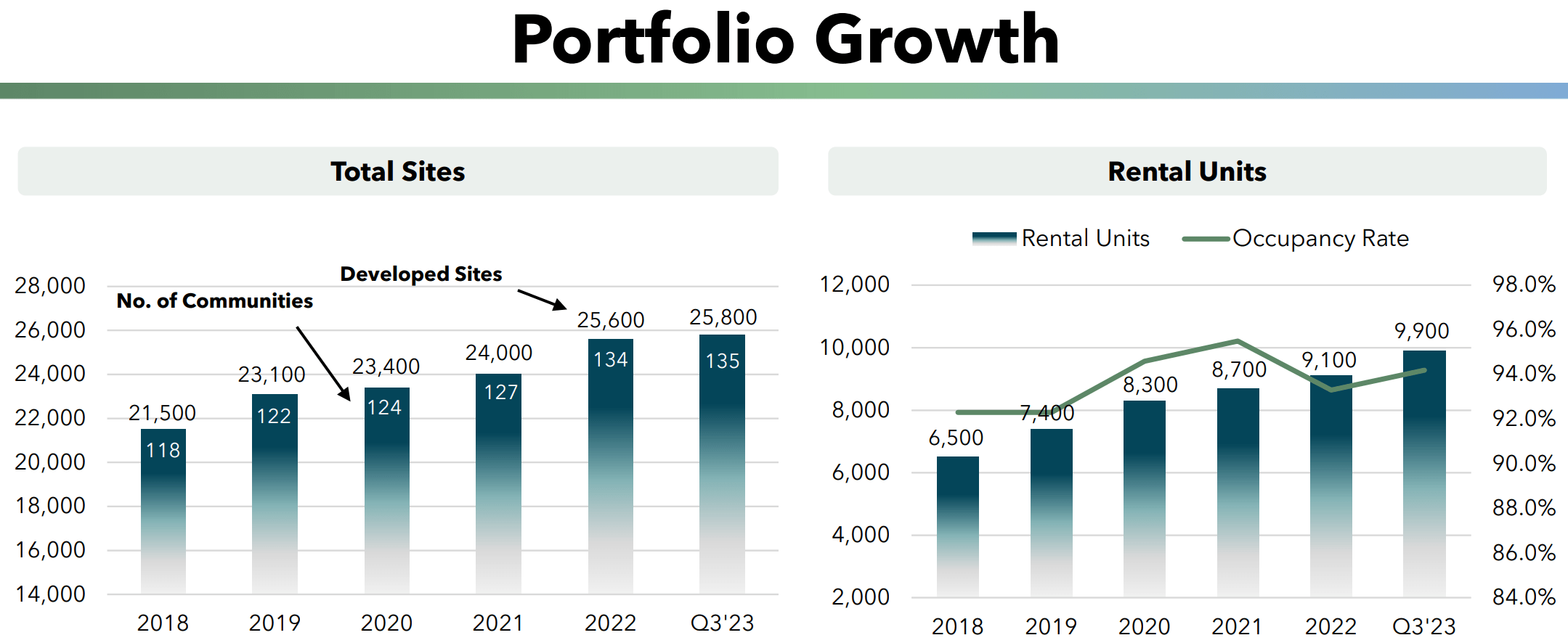

UMH is an internally-managed REIT that is an owner and operator of manufactured housing communities, leasing manufactured homesites to private residential homeowners. At present, it has a portfolio of 135 MH communities containing 25,800 developed homesites, and increase of 3% (or 700 homesites) over the prior year.

Unlike its more diversified peers Equity LifeStyle ( ELS ) and Sun Communities ( SUI ), UMH’s property is more concentrated in the natural gas producing regions of the Marcellus and Utica shale basis. As such, most of its properties are centered around Pennsylvania and eastern Ohio.

Advantages from having a higher portfolio concentration in its target region comes from the ability to scale and leverage operating efficiencies, since UMH can more easily manage a greater number of properties that are in close proximity to one another. UMH has experienced a steady track record of growing its communities over the past 5 years in its target region, with 52% growth in the number of rental units from 6,500 in 2018 to 9,900, as shown below.

{kind=link}

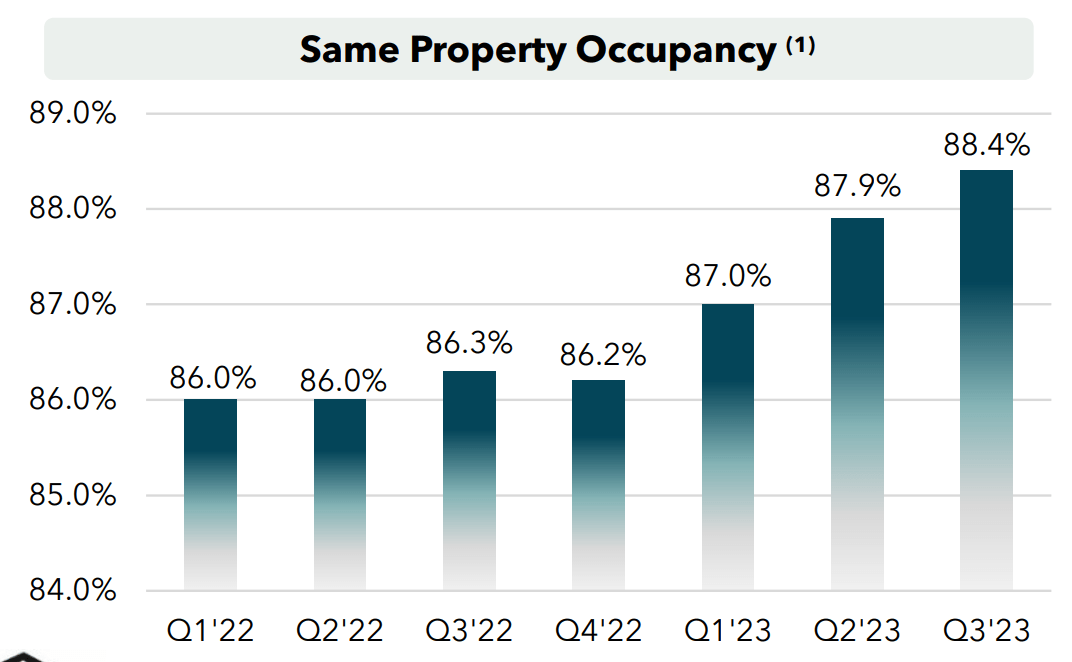

Meanwhile, UMH has demonstrated encouraging growth recently, with same property NOI growing by 13% YoY during the third quarter. Importantly, expenses have been kept in check amidst an inflationary environment, with same property operating expense-to-revenue ratio declining by 150 basis points to 40.6% over the same timeframe. This improvement was driven by higher rental revenue and occupancy, which rose by 210 basis points to 88.4%. As shown below, positive demand trends for UMH’s properties have led to steadily increasing occupancy since the start of 2022.

{kind=link}

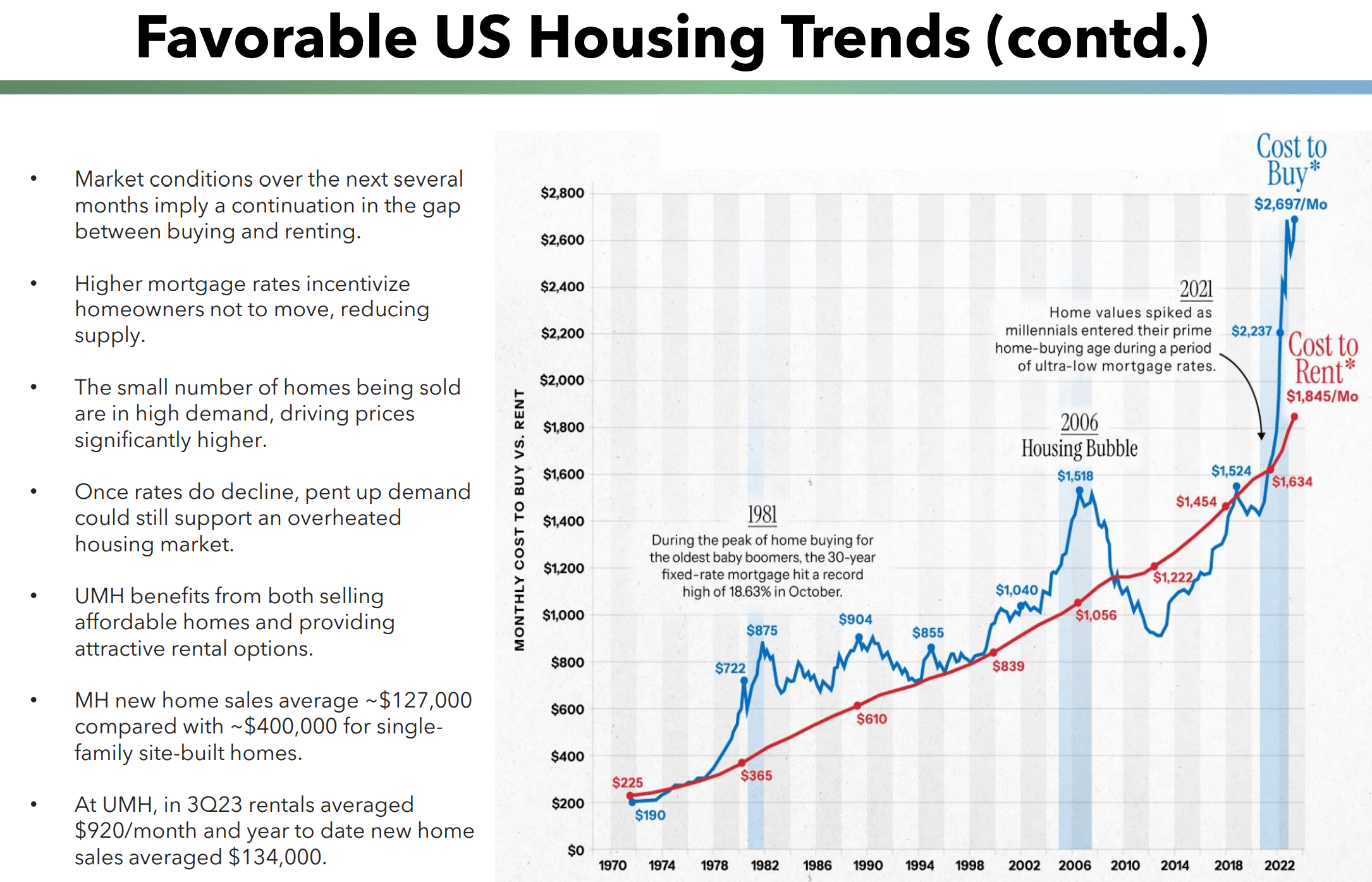

Looking ahead, I see continued positive demand trends for UMH considering the value proposition that affordable manufactured housing makes for homeowners amidst a still-high interest rate environment. High interest rates could also be a strong contributing factor to homeowners sticking to their current homes for their lack of desire to trade for a new home at a higher mortgage rate, and this provides further support to UMH’s occupancy. As shown below, the cost-to-buy vs cost-to-rent ratio currently sits at one of the highest levels over the past 5 decades.

{kind=link}

UMH is also on track to grow its rental revenues from ground leases, management believe it’s on track in 2023 to break its previous sales record of $28.1 million with its sales goal of $30 million for the year. It’s also finding opportunities across its “land bank” as management expects to develop 400 sites and receive approvals to develop an additional 800 sites in 2024. UMH is also seeing the net value of its sites increase, as the replacement value of its sites developed 12 years ago has risen from $40,000 to $70,000.

Risks to UMH include potential for an economic recession, which could negatively impact its rental base. In addition, while UMH’s geographic concentration carries advantages of scale, it also poses as a risk should the area suffer from region-specific negative economic consequences such as a decline in natural gas exploration. Other risks include potential for higher interest rates should inflation be difficult to tame in 2024.

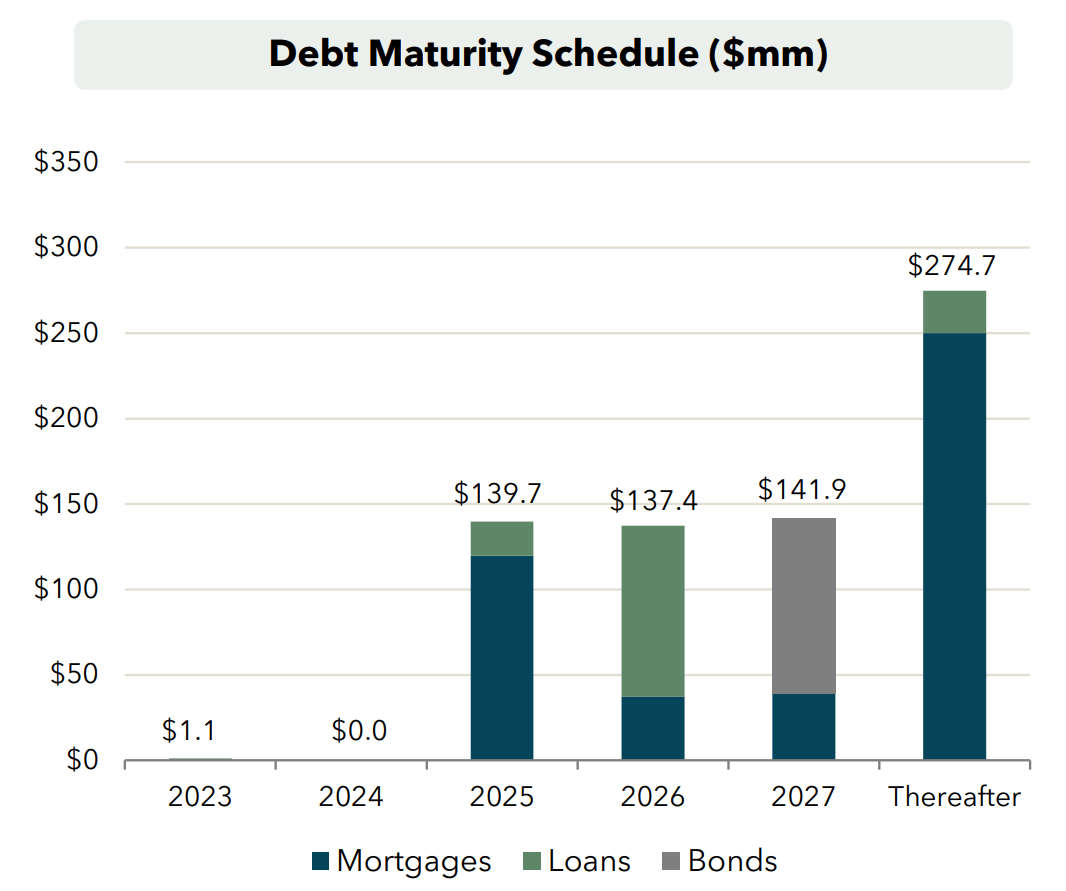

Nonetheless, UMH is reasonably levered with a net debt (including securities portfolio) to EBITDA ratio of 6.2x, sitting slightly higher than the 6.0x level generally considered to be safe for REITs. As shown below, UMH has no debt maturities next year, and its maturities are well-laddered thereafter. With the Federal Reserve indicating the potential for three rate cuts next year, UMH could be well-positioned from a balance sheet standpoint should occupancy and rental rates continue to grow.

{kind=link}

Meanwhile, UMH currently pays a 5.4% dividend yield that’s covered by a 96% payout ratio. It’s also demonstrated 3 years of consecutive dividend growth and while the growth rate has been just about 2.5% annually, I see potential for more meaningful growth down the line as UMH remains committed to capital investments to grow its portfolio in the near term.

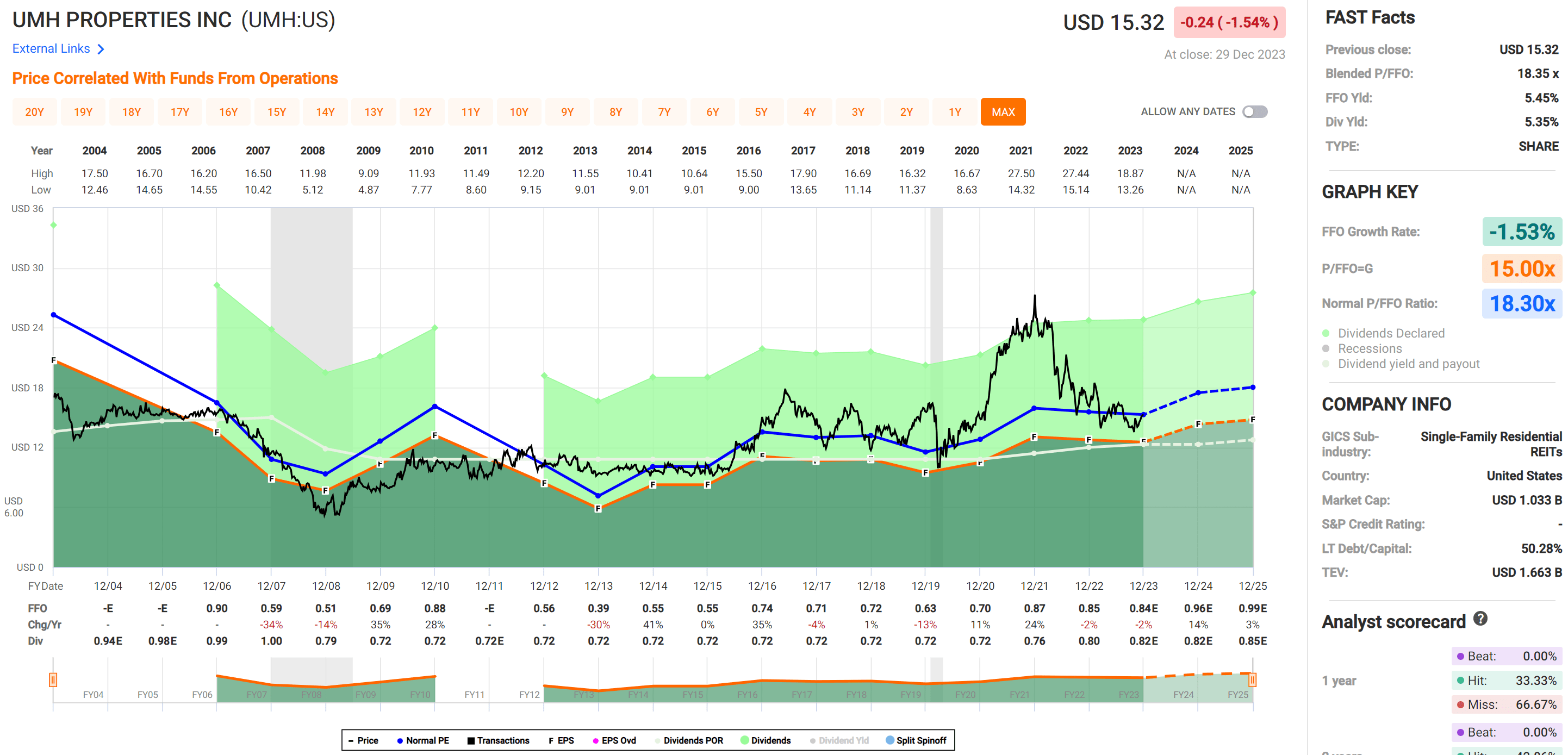

Turning to valuation, I continue to find the shares appealing at the current price of $15.32 with a forward P/FFO of 18.0. While this sits just shy of UMH’s normal P/FFO of 18.3, I believe the appeal is justified considering the strong operating fundamentals and analyst expectations for 13.6% FFO/share growth in 2024, and 6.1% annual growth thereafter.

{kind=link}

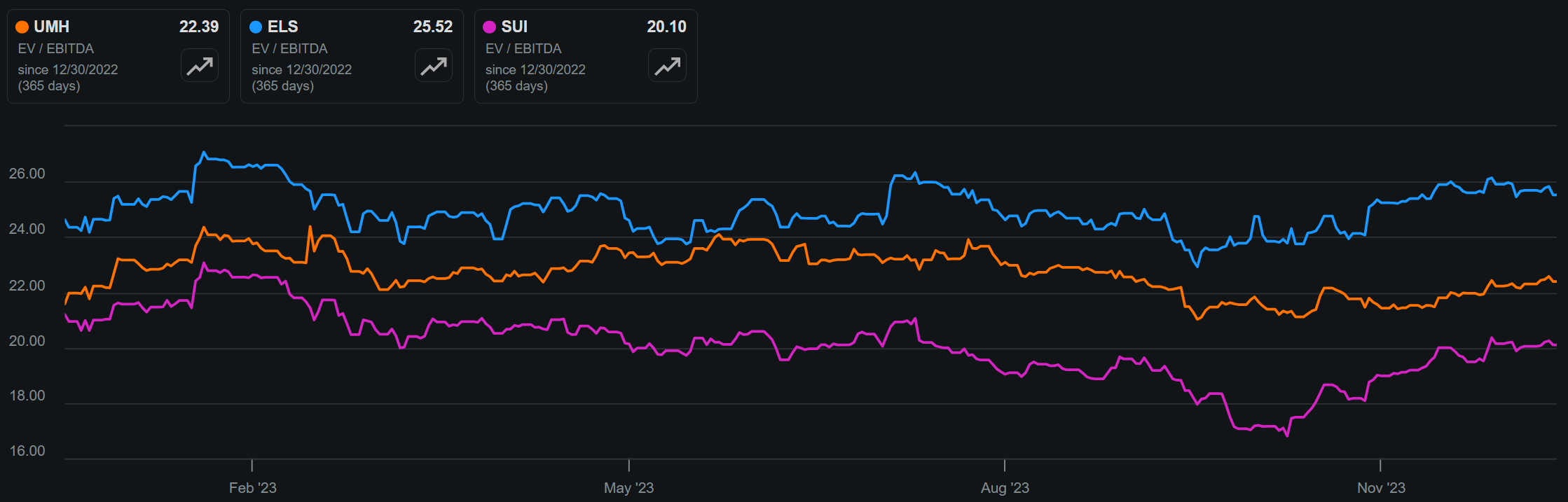

As shown below, UMH also doesn’t appear to be pricey compared to peers. With an EV/EBITDA of 22.4, it sits right in between the 25.5 of ELS and 20.1 of SUI, as shown below.

UMH vs. Peers EV/EBITDA (Seeking Alpha)

{kind=link}

Investor Takeaway

UMH remains an attractive value proposition for investors seeking a REIT with strong operating fundamentals in a growth industry that holds up well in recessions. With a focus on growing its portfolio in its target region, well-managed leverage levels and debt maturities, and potential for further dividend growth down the line, UMH stock remains an appealing ‘Buy’ at present for both value and income-seeking investors.

For further details see:

UMH Properties: Rising Demand And Appealing Yield