VNQ - UMH Properties: Improving The Renter's Lot In Appalachia

Summary

- Due to the ongoing housing shortage, I expected Manufactured Housing REITs to outperform the REIT average this year.

- Instead, they have underperformed, and the sell-off has created some interesting value propositions, such as UMH Properties.

- Thanks in part to a recapitalization of its Series C preferred stock, and secular tailwinds increased demand and limited housing supply, there are signs of a turn-around in UMH's fortunes.

- This article examines growth, balance sheet, dividend, and valuation metrics for lower mid-cap REIT UMH Properties.

Due to the ongoing housing shortage, I expected Manufactured Housing REITs to outperform the REIT average this year. Instead, that sector has underperformed, returning (-38.53)% YTD, compared to the still-awful (-32.87)% REIT average.

Hoya Capital Income Builder

The sell-off has created some interesting value propositions. Today we will take a closer look at one of those companies, UMH Properties, which has returned (-39.35)% YTD.

Meet the company

UMH Properties, Inc.

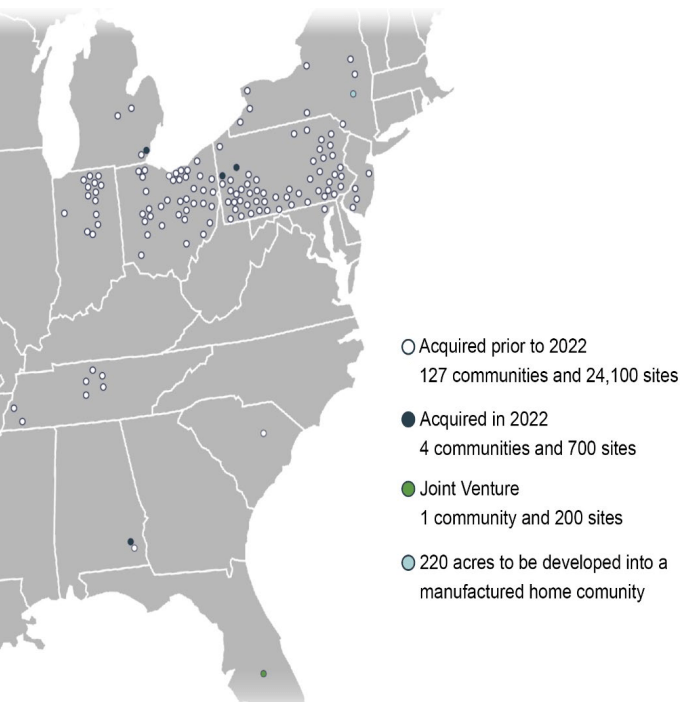

Headquartered in New Jersey, UMH Properties ( UMH ) has been in operation since 1968. The company first converted to a publicly-traded REIT in 1985, and became a component of the Russell 2000 in 2009. By far the smallest of the Manufactured Housing REITS, this company owns and operates 131 manufactured home communities, consisting of 24,800 developed home sites across 10 U.S. states, all east of the Mississippi. Total portfolio site occupancy is just 85.1%, with same-property occupancy of 86.7%, and average site rent running at $494 a month.

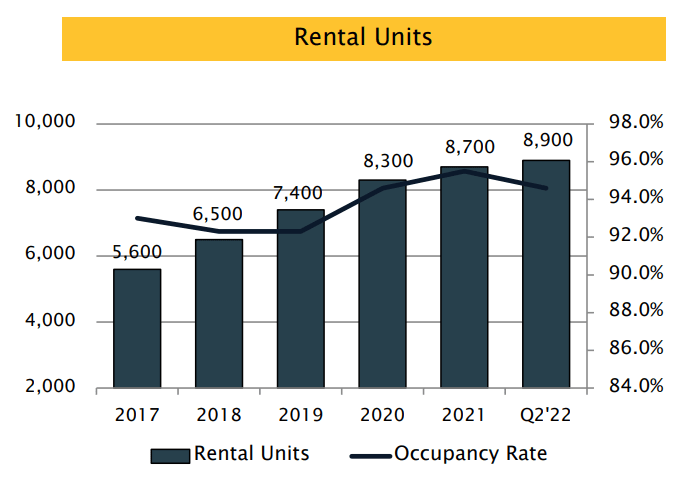

Of the total portfolio, 8900 of the developed sites (35.8% of the portfolio) are occupied by homes owned by the company, and that segment of the portfolio is 94.1% occupied. Average rent for these homes is $844 a month, which includes site rent. UMH also owns 1900 acres of undeveloped land.

Roughly half (49%) of UMH's 7,268 acres of property sits in the Marcellus and Utica Shale Regions, which are large natural gas fields stretching from upstate New York, across Pennsylvania, Ohio, and West Virginia. This region has the potential to be among the largest sources of natural gas in the world, and development of the fields is expected to accelerate over the next few years, bringing increased employment and higher property values. Demand for rental homes in this region "has increased substantially over the past year", according to the company.

{kind=link}

Due to its geographic positioning, UMH's portfolio is not subject to extensive damage from hurricanes, as most of the other Manufactured Housing REITs are. Fully 60% of UMH's properties are located in Pennsylvania and Ohio, with another 16% in Indiana. Also, unlike other Manufactured Housing REITs, which have branched out into RV parks and marinas, UMH deals only in manufactured housing.

Company investor presentation

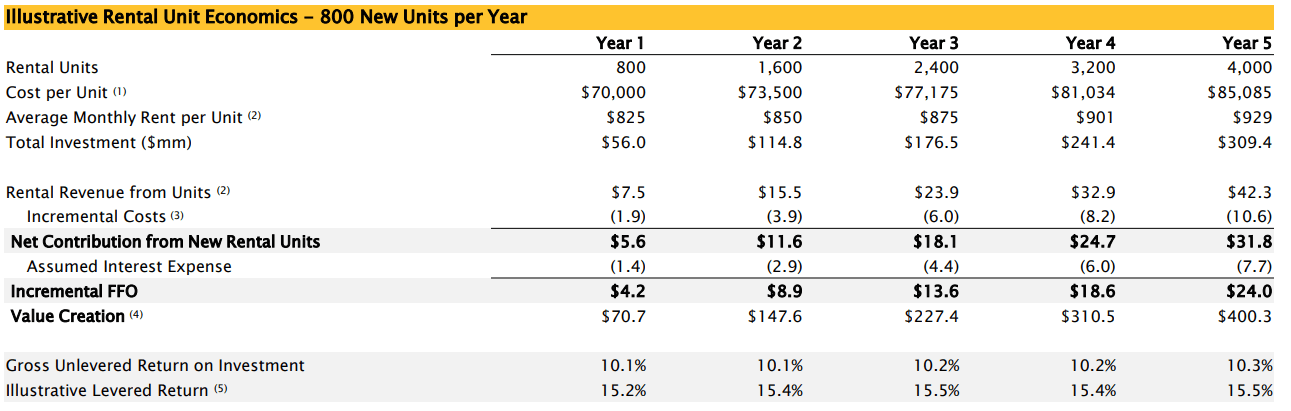

Because the company can buy and rent new manufactured homes at an unlevered 10% rate of return, the company is expanding its footprint in these types of homes.

{kind=link}

From 2017 through 2020, UMH was buying and installing 900 new rental homes per year. The rate of increase fell to just 400 homes in 2021, and 200 more through the first half of this year.

{kind=link}

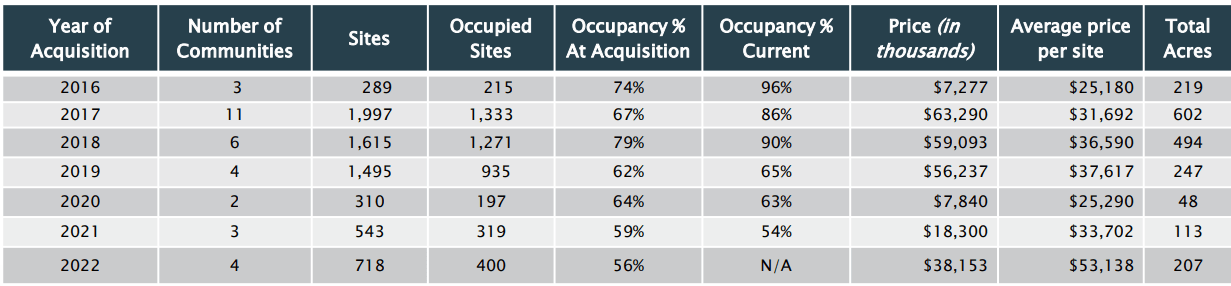

UMH typically acquires communities that are 50% - 75% occupied, and fixes them up, to drive higher occupancy, higher rent, and improved property values over the course of 3 - 5 years, as the table below shows.

{kind=link}

Their pace of acquisition slowed considerably during pandemic-blighted 2020 and 2021, but has resumed its pre-COVID pace this year. The company is on pace to add over 400 acres of communities, at an investment of $76 million.

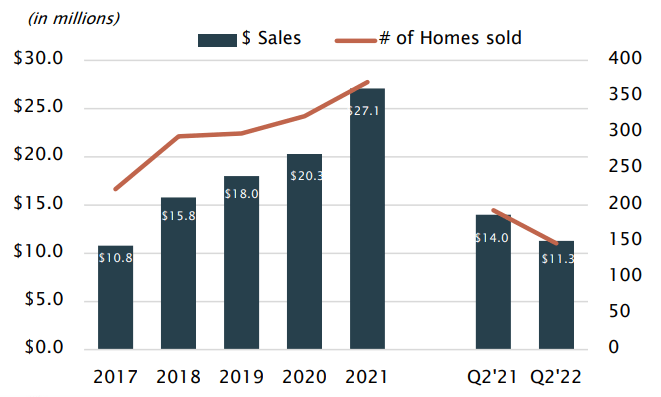

UMH also sells manufactured homes, and finances those sales, typically with 10% down and 15-25 year mortgages, averaging a hefty 6.7% interest rate. Annual revenues from home sales have been increasing steadily over the past 5 years, and though sales levels fell off a bit in Q2 of this year, the company is still on pace for an increase of about 10% in sales revenues in 2022.

UMH Home Sales Revenue (Company investor presentation)

{kind=link}

Meanwhile, the total value of the loan portfolio continues to climb, and the interest rate continues to gradually decline.

UMH Home Financing (Company investor presentation)

CEO Samuel Landy sums it up this way:

We . . . [acquire] value-add communities in strong geographic locations and [make] the required improvements to provide the high-quality affordable housing that our residents desire and deserve. Our improvements result in increased occupancy, revenue, and ultimately, property value. As the community operating results improve and the property values increase, we are able to refinance at lower rates, effectively reducing our cost of capital.

Annual total revenues have continued to climb every year, even through the pandemic.

Company investor presentation

Growth metrics

Here are the 3-year growth figures for FFO (funds from operations), TCFO (total cash from operations), and market cap.

| Metric |

| 2018 |

| 2019 |

| 2020 |

| 2020 |

| 3-year CAGR |

| FFO (millions) |

| $27.0 |

| $24.6 |

| $26.3 |

| $39.1 |

| -- |

| FFO Growth % |

| -- |

| (-8.9) |

| 6.9 |

| 48.7 |

| 13.23% |

| FFO per share |

| $0.74 |

| $0.74 |

| $0.63 |

| $0.70 |

| -- |

| FFO per share growth % |

| -- |

| 0.0 |

| (-14.9) |

| 11.1 |

| (-1.85)% |

| TCFO (millions) |

| $40.2 |

| $38.5 |

| $66.8 |

| $65.2 |

| -- |

| TCFO Growth % |

| -- |

| (-4.2) |

| 73.5 |

| (-2.4) |

| 17.62% |

Source: TD Ameritrade, CompaniesMarketCap.com, and author calculations

Revenue and cash flow growth for UMH have been very spotty. Before the pandemic, the company was struggling with shrinkage in both. In 2020, FFO grew, but FFO/share plummeted, perhaps reflecting excessive share issuance, while cash flow growth exploded by over 70%. Then in 2020, FFO grew by a whopping 48.7%, but FFO per share trailed along at 11.1%, and cash flow slid back (-2.4)%.

UMH is in the process of recapitalization their Series C preferred stock. This will likely have the effect of increasing FFO by $0.12 per share in the coming year, which would be a 17% increase from that factor alone.

Meanwhile, here is how the stock price has done over the past 3 twelve-month periods, compared to the REIT average as represented by the Vanguard Real Estate ETF ( VNQ ).

| Metric |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| 3-yr CAGR |

| UMH |

| 1.58 |

| 23% |

| 11.0 |

| -- |

Source: Hoya Capital Income Builder, TD Ameritrade, and author calculations

UMH is spotty in this area also. The Liquidity Ratio of 1.58 is typical of Manufactured Housing REITs, but well below the REIT average, and the total Debt/unadjusted EBITDA of 11.0 is cautionary.

The company has been doing a nice job of bringing down its Net Debt/Market Cap and Net Debt/Adjusted EBITDA over the past 4 years, as the two charts below illustrate.

Company investor presentation

Company investor presentation

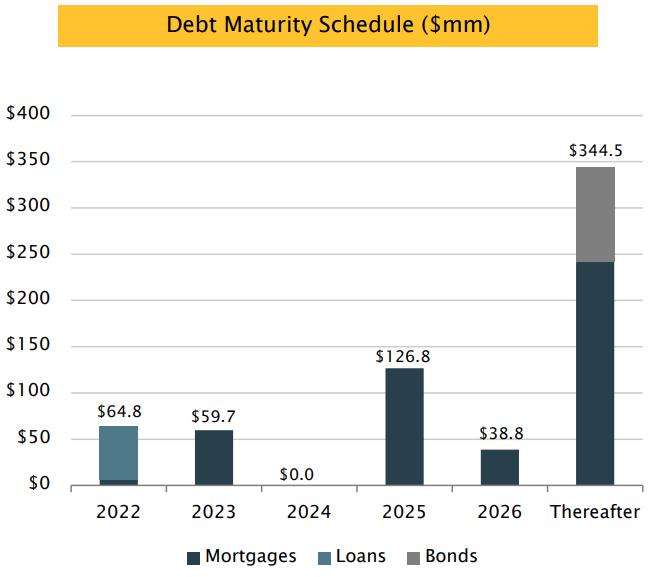

As of June 30, UMH was carrying $626 million in debt, at a weighted average interest rate of 3.92%, and holding $276 million in cash and equivalents, enough to cover the next 4 years of debt payments.

More than half the debt comes due in 2027 or thereafter. Of the remaining amount, debts coming due in 2022 total $64.8 million, with $59.7 million due next year, and no maturities at all in 2024, before a leap to $126.8 million in 2025 and a drop back to $38.8 million in 2026.

{kind=link}

Dividend metrics

UMH has never cut its dividend since 2009, and has begun modestly increasing the payout over the past two years, though not fast enough to keep pace with the Manufactured Housing sector, nor the REIT average. Its current Yield and Dividend Score are well above average. However, the payout ratio of 110% is dangerously high.

| Company |

| Div. Yield |

| 3-yr Div. Growth |

| Div. Score |

| Payout |

| Div. Safety |

| UMH |

| 5.45 |

| 22.0 |

| (-31.9)% |

Source: Hoya Capital Income Builder, TD Ameritrade, and author calculations

Which way is the wind blowing?

Hoya Capital's recent report on Manufactured Housing REITs says that going forward, UMH should benefit from:

- the redemption of its relatively high-cost preferreds and

- fundamental secular tailwinds of limited affordable housing supply and robust demographic-driven demand

The report reads, in part,

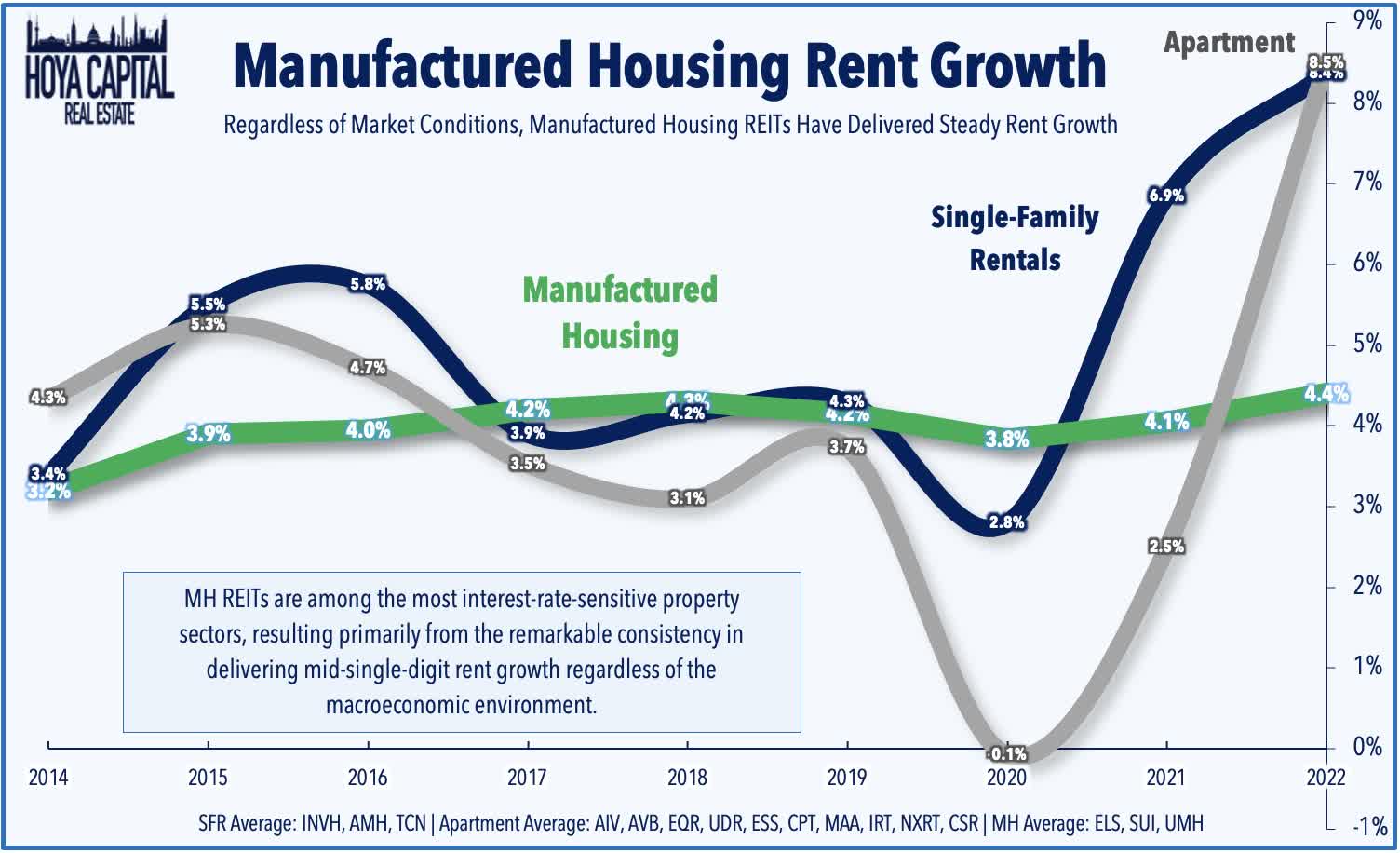

MH REITs are more "bond-like" in their investment characteristics than most would otherwise assume, due in part to their remarkably consistent pattern in delivering 3-4% annual rent growth year-in-and-year-out. That said, we believe that MH REITs' inflation-hedging potential is underappreciated by the market as MH rents are more closely linked with the CPI Index than any other residential sector . . . MH REITs are still among the most interest-rate-sensitive property sectors, resulting primarily from the remarkable consistency in delivering mid-single-digit rent growth regardless of the macroeconomic environment.

{kind=link}

The war in Ukraine has greatly disrupted energy supply, especially oil and gas. With winter coming on, the need for home heating in Western Europe will likely spur natural gas production. This would be a significant economic tailwind for UMH, driving a demand for housing and an increase in per capita income, since nearly has half UMH's assets are in the Marcellus and Utica Shale Regions.

What could go wrong?

UMH is running a significant risk of a dividend cut, which would directly threaten share prices.

Natural gas production can be environmentally problematic, and over time could significantly inhibit the growth of property values.

Since more than half of UMH's portfolio is concentrated in just two states (Pennsylvania and Ohio), unexpected economic downturns in that region could negatively impact UMH's performance.

Investor's bottom line

Despite the many factors working in this company's favor, UMH's spotty performance on the baseline metrics and its risky payout ratio and high Debt/EBITDA prevent me from pulling the trigger on a Buy rating. I see the company as a Hold. There are better bargains in higher-quality and higher-yielding companies lying around right now, all across REITdom. If you want to beef up your exposure to Manufactured Housing REITs, Sun Communities ( SUI ) is a much better buy at the moment in my opinion, for a variety of reasons.

Analyst opinions of UMH vary sharply. The Seeking Alpha Quant ratings say Sell, while Zacks, The Street, TipRanks, and Ford Equity Research all say Hold. At the same time, 6 of the 7 Wall Street analysts covering the firm rate UMH a Buy or Strong Buy, with a price target of $24.00, implying 47% upside.

Seeking Alpha Premium

In the last analysis, the opinion that matters most is yours.

For further details see:

UMH Properties: Improving The Renter's Lot In Appalachia