CI - Uncovering The Hidden Value In Cigna: A Thorough DCF Valuation

Summary

- Despite delivering strong results, Cigna's stock has been underperforming the S&P, leading investors to question whether the company is undervalued.

- Cigna's strategic partnerships, geographic expansion, and strong financial position make it well-positioned for future growth.

- Despite taking a conservative approach in our DCF analysis, we consistently found that Cigna is undervalued by the market.

Cigna Group (CI) is a leading global health service company that offers insurance and health services to a diverse range of clients, including individuals, families, and businesses. Despite the company delivering impressive results, its stock has been underperforming the S&P since the beginning of 2023. As a result, investors may be wondering if Cigna is undervalued, and if now is the right time to invest in the company.

Investment Thesis

The purpose of this article is to provide a comprehensive valuation of Cigna using a discounted cash flow approach. By analyzing Cigna's financial statements and projecting future cash flows, we have determined that the company's estimated worth is currently undervalued. Our model assumptions, which were intentionally conservative, suggest that Cigna has significant upside potential, making it an attractive investment opportunity for long-term investors. In fact, based on our analysis, we believe that the current market price is underestimating the true value of the company. However, we also acknowledge that there are risks associated with the company's business and prospects that must be considered to have a comprehensive understanding of its overall investment potential.

Overview of last quarter's report & earnings call

In my analysis of Cigna, I drew upon insights from the company's latest earnings call, which reaffirmed a positive outlook for its growth and future prospects. Here are some key takeaways:

- Cigna's Q4 2022 earnings beat analysts' estimates, with strong growth in the health services segment and higher revenue from commercial and government customers;

- The company expects further growth in 2023, with a projection of 33.6 million to 34.1 million total medical customers;

- Cigna plans to expand its services and product offerings, particularly in the areas of behavioral health and pharmacy benefit management, as well as increasing the use of digital capabilities and technology to improve customer experience and outcomes;

- The company is well-positioned for the current trends in the healthcare industry, particularly the move towards value-based care and precision medicine, and the increasing demand for coordination and integration of services;

- Cigna has a positive outlook for its growth and future prospects, with a focus on innovation, customer-centricity, and adaptability to changing industry trends;

- However, Cigna expects some softening in the labor market and a further uptick in disenrollment in 2023, which they have factored into their projections.

Cigna Discounted Cash Flow

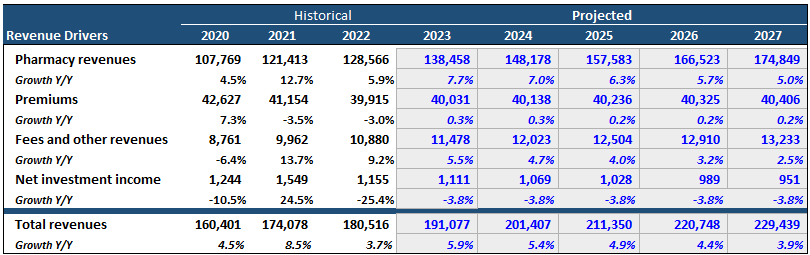

Revenue Growth Assumptions

Based on the company's positive outlook, they project adjusted earnings of at least $24.60 per share in 2023 and adjusted EPS of at least $28 in 2024, representing a growth of 5.72% and 13.82% respectively. Additionally, the ongoing partnership with VillageMD is expected to contribute to shared savings with Evernorth, although it is not expected to be a significant revenue or earnings driver in 2023. To support these assumptions, I used a conservative approach, projecting a 7.7% growth rate for Pharmacy revenues in 2023, declining to 5.0% by 2027. I also applied conservative growth assumptions for revenue from premiums, Fees and other revenues, and net investment income, resulting in a projected revenue increase of 5.9% in 2023, declining to 3.9% by 2027.

{kind=link}

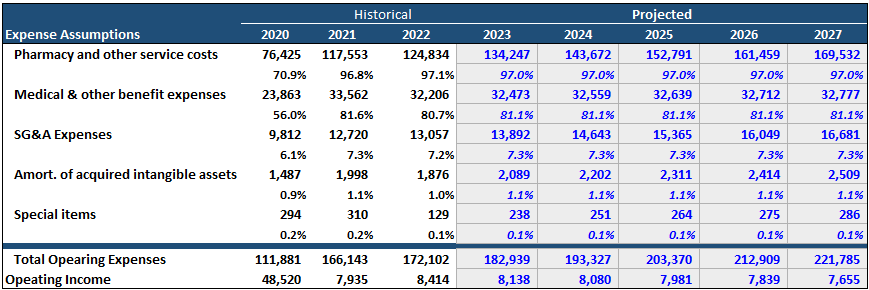

Projecting Expenses and Operating Income

To estimate Cigna's operating income for the projected period, I made assumptions about several expenses as a percentage of different revenue sources:

- Pharmacy and other service costs as a percentage of Pharmacy revenues are expected to remain at 97.0% (average of the % during 2021 and 2022);

- Medical costs and other benefit expenses as a percentage of premiums revenues are also expected to remain stable at 81.1% (average of the % during 2021 and 2022);

- Selling, general and administrative expenses, Amortization of acquired intangible assets, and Special items are projected as a percentage of total revenue based on the average during 2021 and 2022.

Based on these assumptions, Cigna's operating income is expected to decrease during the projection period. It's worth noting that these assumptions are very conservative.

{kind=link}

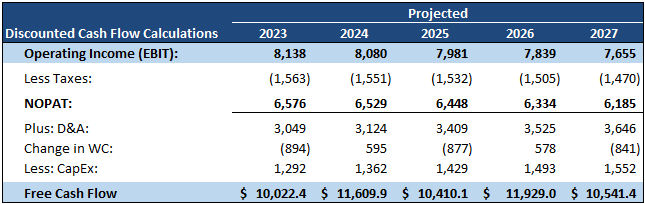

Cigna Free Cash Flow by year

Moving to the free cash flow calculation, based on my projections, in 2023 Cigna is expected to generate $10,022.4 million which is expected to fluctuate slightly over the years, reaching approximately $10,541.4 million in 2027. For instance, Cigna plans to allocate around $1.4 billion to capital expenditures in 2023 while based on my assumptions and projections, the estimated amount for capital expenditures is approximately $1.3 billion.

{kind=link}

Cigna Terminal Value

When valuing a company like Cigna, we need to consider various factors such as the estimated terminal free cash flow ((FCF)) growth rate and the weighted average cost of capital ((WACC)). Based on our analysis, we estimate a terminal FCF growth rate of 2.0% and a current WACC for Cigna of 6.18%. However, since there is a possibility of further rate hikes in the near future, we are adding an additional 1% to the WACC, resulting in a total of 7.18%. Using this adjusted WACC, we have arrived at a terminal value of $207,573 million USD.

Fair value per share DCF

After adjusting for cash, debt, and minority interests, we estimate an equity fair value of $165,981. Based on the current number of shares outstanding (305.413 million), we estimate a fair value per share of $543.46, according to the assumptions of this DCF model.

While the estimated fair value for Cigna might seem high, it is important to conduct a sensitivity analysis to understand the impact of changing key assumptions on the final value per share. In this case, we analyzed the impact of varying terminal growth and WACC assumptions on the estimated value. Even with more conservative assumptions, the final value per share remains above $400, indicating that Cigna is still an attractive investment opportunity.

Cigna Sensitivity Analysis (Author calculations)

Investment Risks

Cigna's positive outlook is tempered by several risks that could affect its financial performance in the future. These risks include:

- Regulatory changes in the healthcare industry, including changes to laws, regulations, and government programs such as Medicare and Medicaid, which could reduce demand for Cigna's services and negatively impact its financial results.

- Increasing competition in the healthcare industry from traditional insurers and newer, technology-driven companies, which could disrupt the industry and challenge Cigna's market position.

- Business concentration in the United States, exposing it to regional economic and political risks.

- Prolonged periods of high interest rates , which could increase the cost of borrowing, reduce demand for new insurance policies, and impact Cigna's ability to finance future growth or acquisitions.

- Risks associated with Cigna's partners, VillageMD and Evernorth , including financial instability, reputational damage, and integration.

Conclusion

In conclusion, the DCF model used to value Cigna suggests that the company is well-positioned for long-term growth and presents an attractive investment opportunity for investors. The model projects steady revenue and earnings growth for the company driven by strategic partnerships, geographic expansion, and its strong financial position. Although the healthcare industry poses certain risks and uncertainties, Cigna has taken steps to mitigate these risks and is well-equipped to adapt to changes in the regulatory environment. Our analysis emphasizes the importance of evaluating a company's financial performance and growth prospects when making investment decisions.

Moreover, based on our findings, we believe that Cigna represents a promising investment opportunity for investors seeking exposure to the healthcare industry, with a long-term fair value estimate of over $500. Yet, this price target should be closely monitored upon the company's financial performance over the next few quarters.

For further details see:

Uncovering The Hidden Value In Cigna: A Thorough DCF Valuation