UA - Under Armour: Favorable Risk/Reward

2023-08-08 19:06:28 ET

Summary

- Under Armour, Inc. reported mixed fiscal Q1 results with the sector facing ongoing inventory issues and gross margins still under pressure.

- The company's focus on improving margins and resolving inventory issues is expected to boost profitability in the long term.

- Despite the challenges, Under Armour remains a deep value stock with potential for multiple expansion and profitable growth.

Despite an apparently successful turnaround during Covid, Under Armour, Inc. ( UA , UAA ) is now plagued with never-ending inventory issues. The athletic apparel company is working on boosting gross margins, but the inventory headwinds won't resolve until the end of this FY. My investment thesis remains ultra Bullish on the stock with an ongoing protracted turnaround and the re-start of student debt repayments clouding the upside potential at Under Armour.

{kind=link}

Inventory Plague

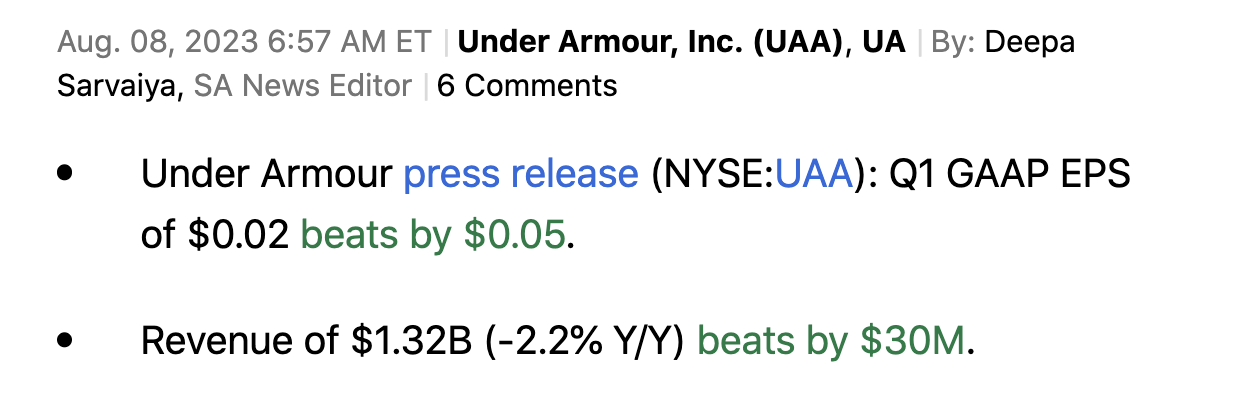

Under Armour reported mixed fiscal Q1 '24 results with the following numbers:

{kind=link}

As expected, numbers were generally weak due to a heavily promotional market in the North American retail segment. Under Armour reported a small profit in the quarter with gross margins still under pressure.

The athletic apparel company had spent the prior years building gross margins back to the 50% level to separate from peer Nike ( NKE ). After the Covid hit, Under Armour had gross margins right around the magical 50% level, but the industry inventory pressures have pushed the margins back down to 46.1% for the June quarter. Lululemon Athletica ( LULU ) has margins approaching 60%.

The company guided to improving margins for FY24, but the number will tail the 50.3% levels of FY21. The corporate goal is only for gross margins to rally 25 to 75 basis points from the 44.9% level of FY23, or nearly 500 basis points below the recent peak.

The biggest issue remains the high inventory levels in the sector. Under Armour ended the quarter with inventory at $1.3 billion, up 38% from prior year levels, though in line with expectations due to leaner inventories in 2022.

The athletic apparel company had done a great job avoiding the inventory issues back in 2022, but Nike sunk the whole sector with elevated inventory. Nike spent the last year cutting inventory leaving Under Armour now with too much product, especially in the North America segment.

The previous top executives had already made some progress on this front, but new CEO Stephanie Linnartz plans to double down on the margin front once the North America inventory issues are resolved. She repeated this concept multiple times on the FQ1'24 earnings call as follows:

Both heat gear and Meridian will be priced to attack better and best level products, helping to advance one of our broader goals which is to drive higher ASPs to leverage gross margin and P&L productivity better.

Outside of the retail issue in North America where sales are forecast to dip 3% to 4% this FY, Under Amour is seeing a booming business. The EMEA and APAC regions both expect double digit sales growth rates for FY24.

{kind=link}

Unfortunately, the Under Armour business remains 63% focused on North America. The company started the year with sales in this segment down an incredible 9% and will end the year reporting flat to up quarterly sales in North America.

As the new CEO gets the inventory levels under control in the 2H of the year and turns around the North America market, the stock should become far more appealing. The company continues innovating with new products and it's a matter of time before these products start driving overall growth.

Deep Value

Under Armour remains a deep value stock, but the inventory issues of the last couple of years have clouded the stock. Nike isn't forecast to generate much in the way of sales growth in the next year either, but the stock continues to trade at a massive P/S multiple in comparison to Under Armour.

Lululemon trading at a higher multiple makes sense, with the premium growth rates and higher gross margins. As discussed above, Under Armour is focusing on more premium market sales with higher margins and profitability placing the business back into the mid-point between Nike and Lululemon.

The ultimate goal for an investor is the company returning to profitable growth and obtaining a considerable amount of multiple expansion. A stock trading at the mid-point of the P/S multiples of these peer stocks would trade at 3.5x forward sales targets while Under Armour currently trades at only 0.55x sales.

The athletic apparel company has ~$700 million in cash and solid cash flows to drive the business forward during this final tough period following the Covid volatility.

Takeaway

The key investor takeaway is that Under Armour offers a lot of potential rewards to shareholders once the company resolves some lingering inventory issues pressuring gross margins. The new management team definitely isn't guaranteed to solve these problems, but the risk/reward favors investors with the stock at only $7.

For further details see:

Under Armour: Favorable Risk/Reward