LULU - Under Armour: Finding Joy In The Darkest Of Times

2023-04-18 16:59:08 ET

Summary

- The sportswear industry is known for being resistant to recession.

- High-interest rates caused a significant rise in inventory costs.

- Under Armour, Inc. maintains a high inventory turnover ratio by carrying less seasonal inventory, making it responsive to the macro environment.

- The current time is deemed a good entry point, despite uncertain timing for a full recovery.

Investment Thesis

When the night is darkest, the stars shine brightest. Investors can overcome the near-term recession fear only by focusing on long-term strategy execution.

Under Armour, Inc. (UA) (UAA), a global performance apparel company, demonstrates resilience in the face of economic challenges, with a focus on product innovation, strategic refinements, and a nimble inventory approach. The company has strong brand and product lines that help consumers stay healthy and confident during a depressed economy.

The art of contrarian investing: No rush! Investors have plenty of time to profit from market inefficiencies. By gradually adding positions, investors can take advantage of these opportunities without exposing themselves to undue risk.

Company Profile

Under Armour, Inc. was founded in 1996. Its principal business activities are developing, marketing, and distributing branded performance apparel, footwear, and accessories for men, women, and youth. Its performance products are engineered in many designs and styles for use in nearly every climate and are worn worldwide by athletes at all levels, from youth to professional, on various playing fields around the globe, and by consumers with active lifestyles.

Company Fundamentals

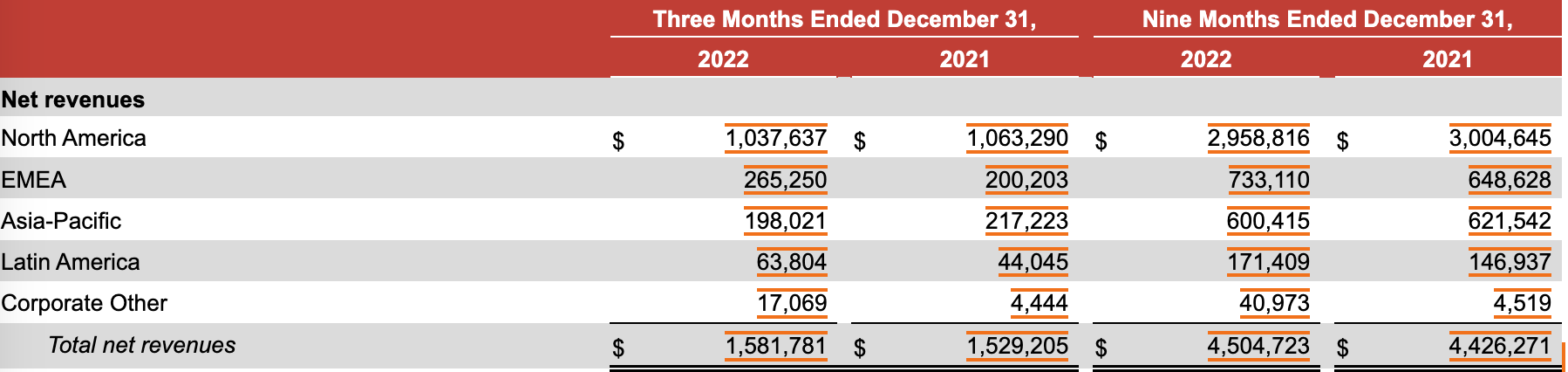

Revenues breakdown by geography (Under Armour)

{kind=link}

For the nine months ended by Dec 2022, the company generated $4.5 billion in sales, 65% in North America, 16% in EMEA, 13% in Asia-Pacific, and 4% in Latin America.

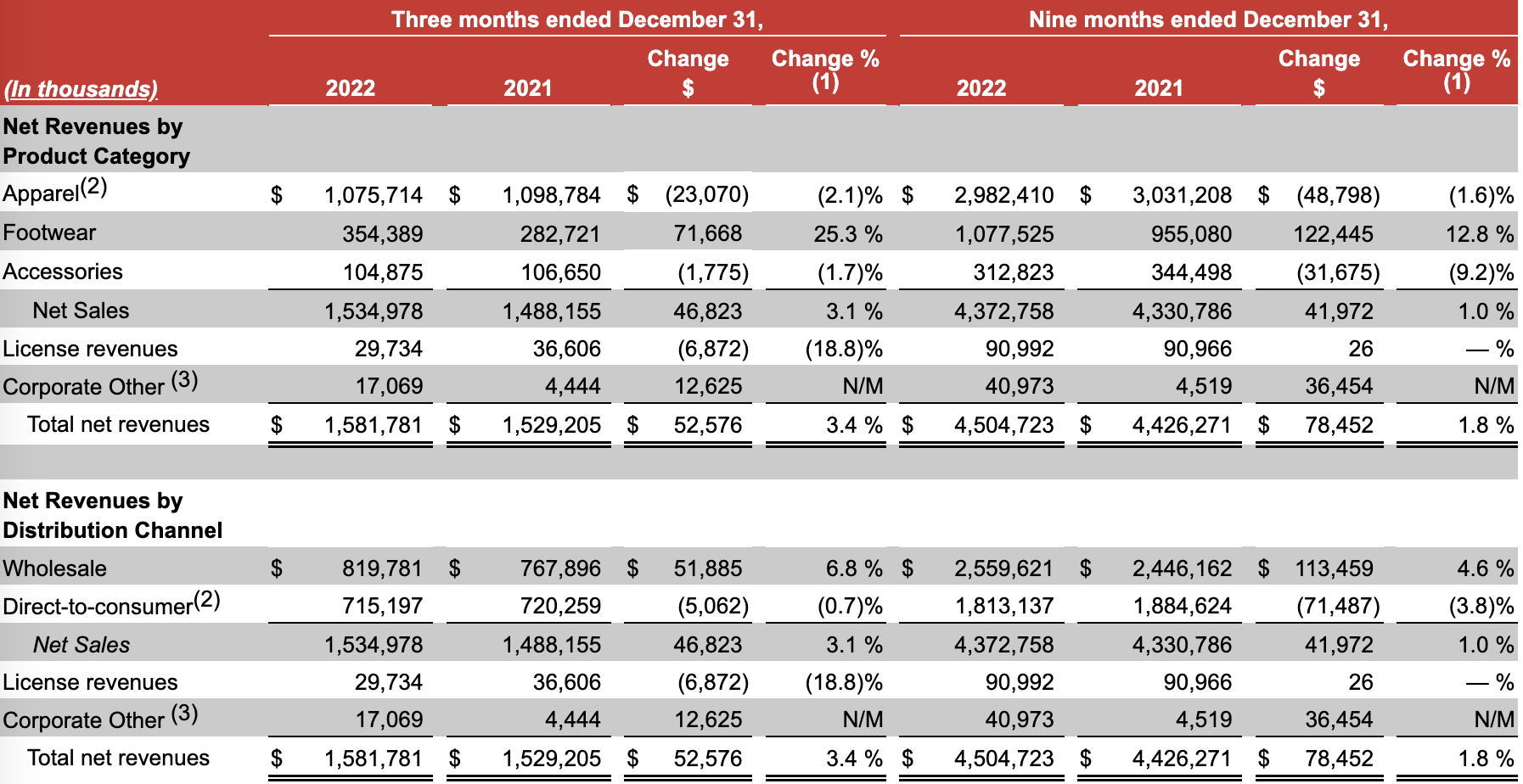

Revenues breakdown by products and channels (Under Armour)

{kind=link}

For the nine months ended by Dec 2022, the company generated 66% of its revenues in apparel, 24% in footwear, and 7% in accessories.

The company generated 57% of its revenues from the wholesale channel and 42% from the direct-to-consumer channel.

Growth Drivers

- Consumers prioritize health and fitness in an inflationary environment.

During a recession, people tend to cut back on discretionary spending, but they often prioritize their health and fitness. This means that sports companies can continue to see demand for their products, particularly for essential athletic gear such as running shoes and workout clothes.

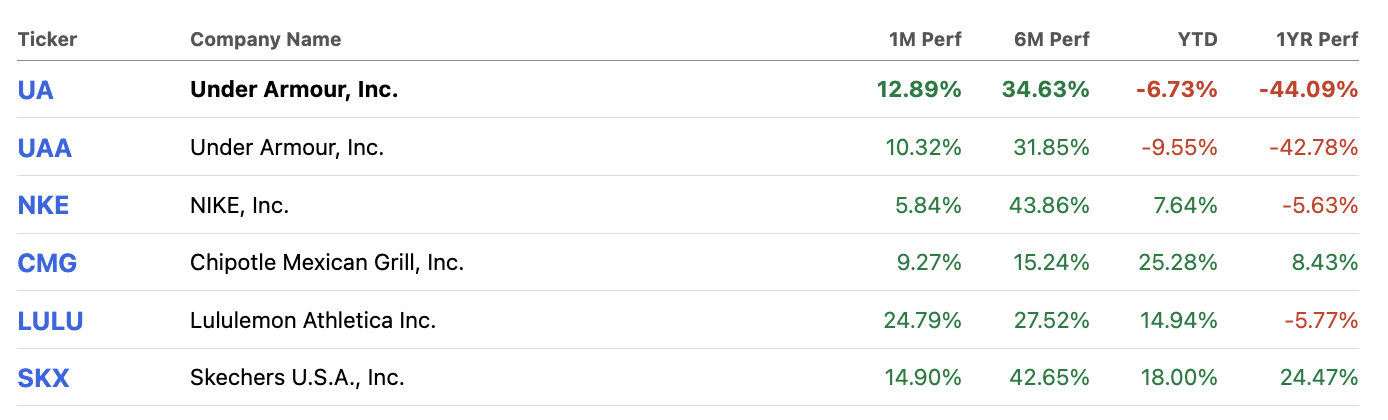

Sportswear stocks had rebound nicely YTD. Nike, Inc. ( NKE ), Lululemon Athletica Inc. ( LULU ), and Skechers U.S.A., Inc. ( SKX ), led the rally. Under Armour seemed to be a laggard of the group.

Stock performance (Seeking Alpha)

{kind=link}

- Sportswear is less seasonal and the company has a high inventory turnover rate.

Many sportswear items such as t-shirts, leggings, and running shoes can be worn year-round and are considered seasonless. This is because they are designed with materials that can be worn comfortably in different weather conditions.

During the earnings call, the company stated that it has identified some seasonless products that it can hold over to next year instead of liquidating them at low prices. The company's inventory was in a healthy place, with not much aged inventory, and the company was packing and holding seasonless products for next year to sell at full price. In addition, the company expects to manage its third-party liquidation in a reasonable spot and stay within the 3% to 5% range.

In addition, in an inflationary environment, the central bank needs to raise the interest rate to combat the strong consumer demand. High-interest rates make holding the inventories very costly as the opportunity costs rise.

Under Armour carries less seasonal inventory so that it doesn't need to replenish the stock very often. Moreover, it maintains a high inventory turnover compared to its peer. This makes the company nimble and responsive to the changes in the macro environment.

Inventory turnover ratios (Companies' filing, LEL Investment)

- Product innovation in the pipeline.

Under Armour was making progress on strategic refinements, focusing on amplifying opportunities for its core business and serving athletes beyond the gym and field.

The company focused on driving premium products at every price point and enhancing storytelling for athletes. The brand's athletes had achieved significant wins across different sports.

They were focusing on creating a broader sports style offering, with the SlipSpeed training footwear and a pop-up store in Manhattan. Under Armour was also evolving its marketing and omni-channel strategies to better connect with the 16-to-20-year-old varsity athlete demographic.

- Sponsorship opportunities in a recession environment.

Inflation can lead to sponsorship opportunities for sports companies because it can drive up the cost of traditional advertising and marketing. As the cost of advertising rises, companies may look for alternative ways to promote their brand and products, such as through sponsorship agreements with sports teams, athletes, or events.

Sports sponsorship can be an effective way for Under Armour to reach a large and engaged audience without incurring the high costs of traditional advertising. For example, a sports company may sponsor a popular athlete or team and have its logo prominently displayed on the athlete's or team's uniform, equipment, or promotional materials.

Industry

- Citigroup Inc. ( C ) saw consumer spending softened .

Citi expected a mild recession later this year, driven by credit contraction. There was an early sign of weakness in consumer spending in Q1 2023.

We did see a notable softening in consumer spending growth over the course of the quarter. Travel and entertainment continued to grow in March, but essentials were flat, and almost all other spending categories were down. Savings rates are below historic averages.

- Consumer spending may increase following the traveling cycle.

One possible reason for the sluggish consumer spending in the consumer discretionary sector could be attributed to the recent surge in travel trends. Once travel demand slows, it's likely that spending will return to the consumer discretionary sector.

During its Q1 2023 earnings call, Delta Air Lines expects a strong June quarter with capacity and revenue growth and is investing in its global network and technology to support future growth and margin expansion.

Moving forward, we are sunsetting the comparisons to 2019 and returning to year-over-year metrics. Domestically, we are growing our seats mid-single digits over last year with our core hub rebuild beginning to take hold in June and accelerating through the fall. On international, we are excited with the momentum we’re seeing and expect record revenues and profitability for the summer travel season. To meet increasing demand, we are growing our international seats by more than 20% in the June quarter compared to prior year, and we already have about 75% of our bookings on hand.

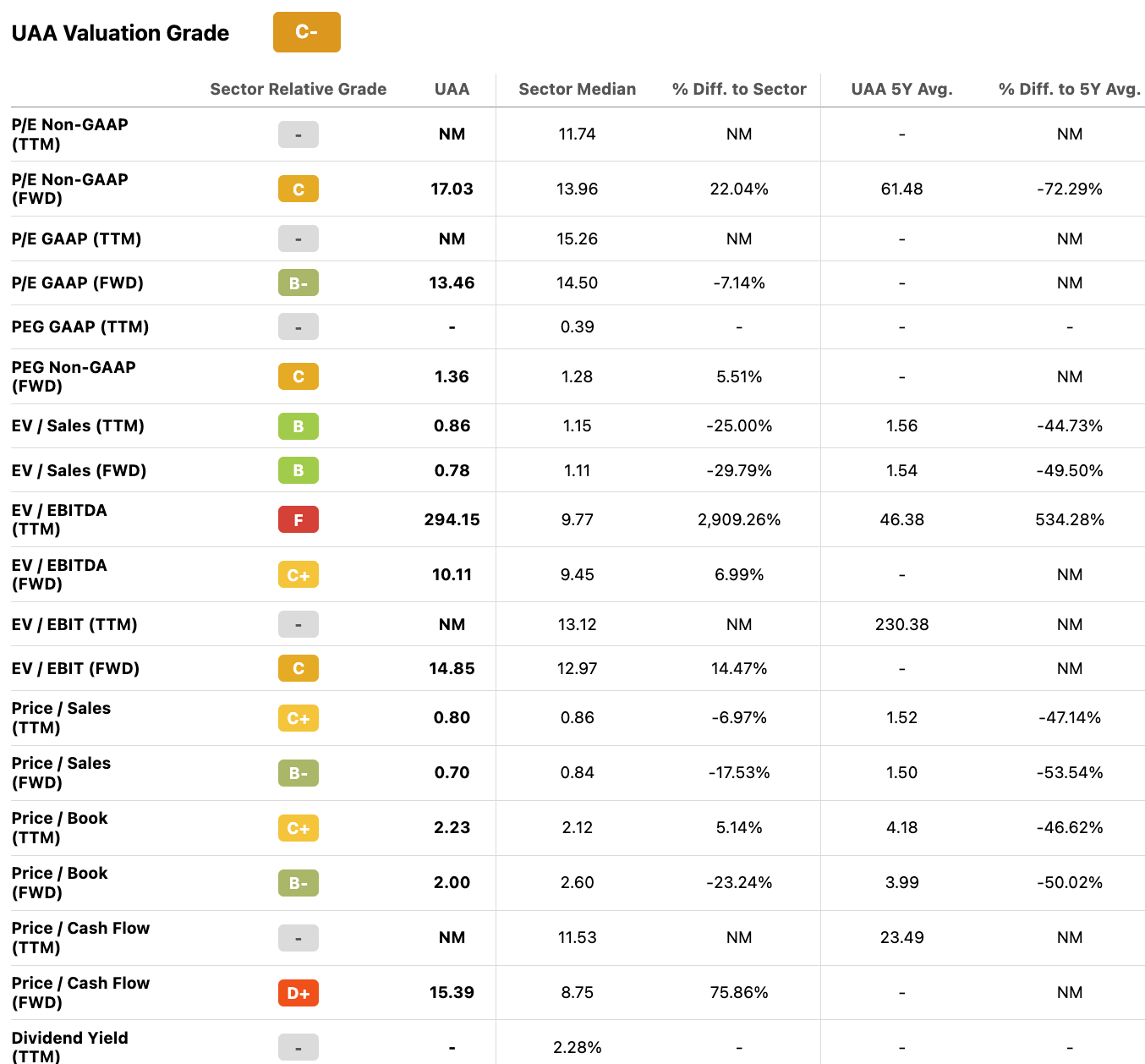

Valuation

{kind=link}

The company expected its revenue to be up at a low single-digit rate on a reported basis and a mid-single-digit rate on a currency-neutral basis, with a full-year gross margin decline to be at the high end of the previously provided 375 to 425 basis point range and full-year SG&A down at a low single-digit rate.

Its valuation multiples are trading below its 5-year average, and its forward P/E ratio is below 20x. Given the potential for sportswear to outperform the consumer discretionary category and the company's excellent brand and offerings, we believe the valuation to be reasonable.

Catalysts

The company is anticipated to adopt a defensive stance in FY2024, while significant revenue growth is expected in FY2025 and beyond. The travel demand is likely to persist into the summer. Hence, investors should expect its fundamentals to rebound in the second half or later.

Risks

- U.S. macro environment worse than expected.

Under Armour's promotional environment is expected to continue for a while due to heavy inventory in the industry, while consumer conversion is challenged due to cautious spending. There is a possibility that credit contraction brought on by the banking crisis will result in higher-than-expected unemployment. As a result, the promotional environment can be lasting longer than expected.

We believe that Under Armour's presence across a wide range of geographies can help to reduce the risk. Under Armour was performing well in Europe despite a difficult macroeconomic environment in Q3 2023. The third quarter was challenging in China due to lockdowns, but the company was optimistic as stores begin to open up.

Under Armour's inventory was up 50% to $1.2 billion. However, the company does not see this as a developing consumer weakness. We believe that because sportswear inventory is less seasonal, there is less risk for the company to hold onto its inventories as the timing of the economic recovery is uncertain.

Summary

The sportswear is a recession-resistant industry. The cost of keeping inventory rose dramatically as a result of the high-interest rate environment. Under Armour, Inc. carries less seasonal inventory and has maintained a high inventory turnover ratio. This makes it nimble and responsive to the macro environment. Its valuation multiple is not expensive compared to its historical average. Although the timing of full recovery is uncertain, we think now is a good entry for Under Armour, Inc. Our investment approach is more contrarian driven, and we prefer to add to our Under Armour, Inc. position as it goes lower rather than try to guess the bottom.

Editor's Note : This article was submitted as part of Seeking Alpha’s Best Investment Idea For A Potential Recession competition, which runs through April 28. This competition is open to all users and contributors; click here to find out more and submit your article today!

For further details see:

Under Armour: Finding Joy In The Darkest Of Times