UAA - Under Armour: Partnership With Ripken Baseball May Accelerate The Growth

2023-10-20 02:17:11 ET

Summary

- Under Armour has announced a partnership with Ripken Baseball, which I believe can help UA to counter inflation's effects by acquiring a large customer base and improving its brand image.

- The company maintained net income growth in FY2022 with the help of supply chain benefits such as decreased ocean & air freight which were offset by persistent promotional activities.

- After comparing the forward P/E ratio of 12.89x and 13.94x with the sector median of 14.33x, we can say that the company is slightly undervalued.

Investment Thesis

Under Armour ( UA ) ( UAA ) develops, markets, and distributes apparel, accessories, and footwear. I will be analyzing the company's financial history and impact of inflation & macroeconomic factors on its financials. The company has announced a partnership with Ripken Baseball, which I believe can help UA to counter inflation's effects by acquiring a large customer base and improving its brand image.

About UA

UA mainly develops, markets, and distributes branded performance apparel, accessories, and footwear. The company mainly generates its revenue through the sale of its products globally to regional, national, independent, and specialty wholesalers & distributors. It sells through its direct-to-consumer sales including e-commerce websites and its owned brand & factory house stores. The firm operates in four different regions: North America (including the USA & Canada), EMEA, Asia Pacific, and Latin America, representing 64.72%, 16.81%, 13.98% , and 3.61% of net revenues. The company earns the remaining 0.88% of its net revenue from the 'Corporate Other' segment which earns its revenue from MapMyFitness digital platform and other digital opportunities. Its product portfolio consists of Apparel, Footwear, and Accessories. The Apparel products generate 66% of the company's total net revenue. The Footwear products represent 25% of UA's net revenue. Accessories products generate 7% of the company's total revenue. UA earns the remaining 3% of revenue from Licensing arrangements and digital platforms.

Financials

{kind=link}

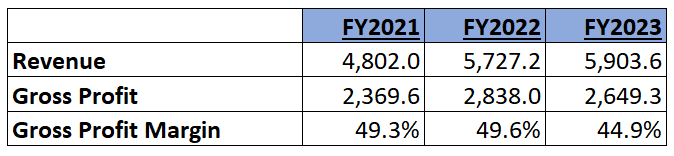

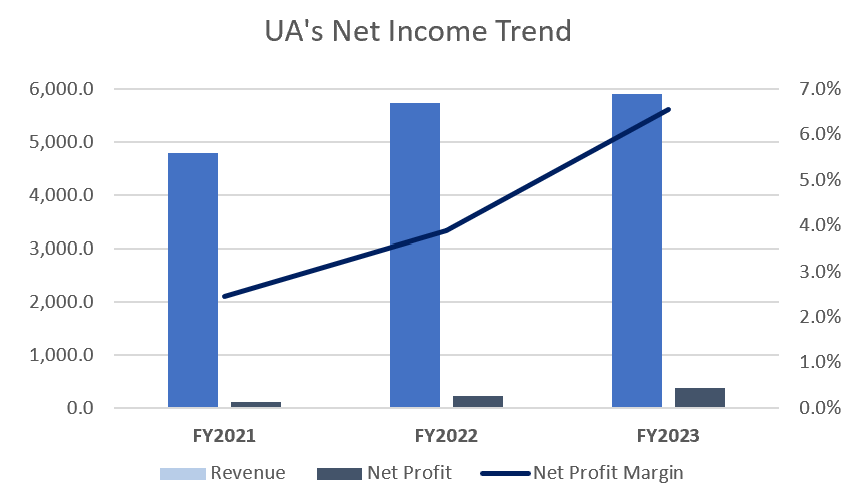

UA has shown an ability to generate stable and consistent revenue growth in the last 3 years. The company has reported a revenue of $5.73 billion in FY2022 which is a growth of 19.26% compared to $4.8 billion in FY2021. This growth was mainly driven by the growth in wholesale and direct-to-consumer business revenue. Despite rising inflation, UA managed to maintain a revenue growth trend in FY2023 as well. It reported revenue of $5.90 billion in FY2023 which is 2.97% growth compared to revenue of FY2022. This growth was mainly driven by a 23% growth in revenue from the EMEA Region. The company has managed to achieve a 3-year CAGR of 7.12% in the period of FY2021 to FY2023.

Currently, the US economy is facing a challenging time due to rising inflation. The apparel & footwear industry is also experiencing a slowdown due to rising inflation.

According to Corey Tarlowe , an analyst at Jefferies, "We believe US consumers are likely to curtail spending ahead, with apparel & footwear being the most likely areas of pullback. With the resumption of student loan repayments, we believe this could be a catalyst that weighs further on already soft sales at some of our specialty apparel coverage."

UA is also currently struggling to maintain growth due to rising inflation. The adverse effects of rising inflation are also reflected in the company's latest quarterly report. It reported a net revenue of $1.317 billion in Q1FY2024, down 2.37% compared to $1.349 billion in Q1FY23. It dropped by 1% when foreign exchange losses caused by a strengthening US dollar were eliminated. The decrease in revenue was fueled by a 9% decrease in revenue from North America. The company is also spending enormous funds on promotional activities which has resulted in a 0.6% drop in gross margin. The company has been experiencing a decreasing gross margin for the last year.

{kind=link}

UA's decreasing gross margin indicates that the company has failed to pass on the rising cost of production to its consumers. The company has managed to decrease the long-term debt significantly which has decreased UA's interest expense dramatically. UA has managed to reduce its long-term debt to $594.1 million which is 41.1% lower compared to $1.01 billion of Mar-2021. The decreased interest expense has resulted in a net interest expense of $1.6 million in Q1FY24 which is 70% lower compared to $6 million in Q1FY23. This drastic decline in interest expense has improved the net income margin of the company. Net income surged by 11.28% YoY from $7.68 million to $8.54 million. The increased net income has translated into a net income margin of 0.65% which is almost the same compared to the net income margin of the same period of last year. The company's net income in FY2022 was $222.7 million (NI margin of 3.9%) which is 88% growth compared to $118.4 million (NI margin of 2%) in FY2021. The company managed to improve net income significantly in FY2022 as well with the help of supply chain benefits such as decreased ocean & air freight which were offset by persistent promotional activities. It reported net income of $386.8 million (NI margin of 6.6%) in FY2023. The increase in promotional and discounting activities is result of a significant rise in inventory. According to the latest quarterly report, the company's inventory has grown by 38% and now stands at $1.3 billion. This rise in inventory signals that we might see huge discounts on UA's products which can adversely affect profits and margins of the company in the coming times. If UA experiences bloating inventory in the coming time due to slowdown demand, then it can increase the cash conversion time as it can increase credit period of retail shops. The increased cash conversion time can stretch the overall working capital cycle. UA is usually considered as the company of middle class as it usually offers heavy discounts on its products. As we know inflation puts heavy pressure on the daily expenses of people and reduces their purchasing power which can reduce spending on apparel and footwear products.

{kind=link}

According to David Payne, Staff Economist, The Kiplinger Letter, "Headline numbers are calculated as the percentage change from a year ago, and December year-ago prices declined or rose only modestly. This will create a temporary spike in the headline CPI figure, with reported inflation likely to come in at about 4.3%. The headline number will drop in January and February, however."

After considering this I think inflation might remain at the same level for a longer time which can soften the revenue of the company in the coming quarters and remain flat for the whole year compared to last year. According to Seeking Alpha, the company's revenue might be $5.94 billion which is 0.62% YoY growth compared to revenue of FY2023. I believe estimates of Seeking Alpha perfectly capture the impact of rising inflation and the partnership with Ripken Baseball. Therefore, I am estimating UA's revenue to be $5.94 billion in FY2024. The company's average net income margin is 4%. I think the company can maintain a net income of 4% in the coming time with the help of supply chain benefits. The revenue estimate of $5.94 billion and net income margin of 4% gives an EPS estimate of $0.54.

Multi-Year Partnership with Ripken Baseball

The sporting goods industry was impacted by the global COVID-19 pandemic and later it experienced a downturn due to supply chain issues. However, it bounced back at a faster rate with the help of decreased freight costs. This growth is expected to be sustained due to increasing consumer health awareness and increasing interest in outdoor activities, and athleisure apparel. This upside has also intensified competition in the industry to capture a large market share in various segments of sporting goods. Identifying these scenarios, the company has recently entered into a multi-year partnership with Ripken Baseball which is a sports association. As per this deal, Under Armour will be serving as an apparel company for Ripken's six properties, multisport events, and hundreds of tournaments. The company will be offering official uniforms for about 9,000 12U players. This partnership also confirms that the company will be an official retail brand partner. As per my analysis, although quantitative effects of this deal are not clear yet, this might help the company improve its brand exposure by reaching a wider group of customers which can further fuel its brand recognition. Brand image and recognition play very important role inflationary market as people with low purchasing power would get attracted to products of the company that have positive brand image in market. In addition, the collaboration can also provide the company with an excellent platform to acquire customers in the future as Ripken has expanded its facilities in Ohio, New York, and Kentucky in 2023 which combined to host 250,000 participants, 12,000 teams, and 900,000 visitors. This can potentially help the company reach a wide group of people which might contribute to its topline growth.

What is the Main Risk Faced by UA?

The company uses technically advanced products as raw materials which are developed by third parties. These materials are available from limited sources and produced by unaffiliated manufacturers. In 2023, about 65% of its accessories and apparel products were made available by ten manufacturers. Six of these parties produced about all of its footwear products. The company does not have any long-term contracts with its manufacturing sources. If the supply of such materials gets disrupted, it can negatively affect the company's production capabilities and can further contract its profit margins.

Valuation

The industry is struggling to grow due to rising inflation. UA's increased promotional & discounting activities and rising inflation in the market can be responsible for its flat revenue growth in FY2024. Therefore, I am estimating the company can generate revenue of $5.94 billion in FY2024. Seeking Alpha estimates that UA's revenue will be $5.94 billion, a 0.62% YoY increase from the revenue of FY2023. I think Seeking Alpha's projections accurately reflect the effects of growing inflation and the partnership with Ripken Baseball. As a result, I predict that UA can generate $5.94 billion revenue in FY2024. The company might benefit from decreased freight costs which can help it sustain net income margin of 4%. The company has also recently entered into a partnership with Ripken Baseball which I believe can accelerate its growth by increasing its customer base. After considering all the above factors and with an estimated $5.94 billion in sales and a net income margin of 4%, I am predicting EPS of $0.54 for FY2024. After dividing a share price of UA ($6.96) and UAA ($7.53) with EPS of 0.54, we get the forward P/E ratio of UA and UAA as 12.89x and 13.94x, respectively. After comparing the forward P/E ratio of 12.89x and 13.94x with the sector median of 14.33x, we can say that the company is slightly undervalued. I believe UA and UAA might gain momentum in coming time due to benefits of supply chain and its increasing customer base which can help it to trade at its sector median. I estimate the company might trade at a P/E ratio of 14.33x in FY2024, giving the target price of $7.74, which is an 11% potential upside for UA and 2.79% potential upside for UAA compared to the respective current share prices.

Conclusion

The industry is currently fighting adverse impacts of macroeconomic pressures. The rising inventory of the company has increased its promotional and discounting costs. The heavy discounts to counter increasing inventory can hamper UA's brand image. Identifying these scenarios, UA has recently entered into a partnership with Ripken Baseball which can increase its profitability by increasing its customer base & brand recognition. People with low purchasing power might get attracted to products of the company with a good brand image in marketplace, which plays a significant role in the inflationary market. However, UA is exposed to the risk of supply chain disruptions which can reduce its profitability. The stock is currently undervalued but potential upside returns are not attractive. Therefore, after considering all the above factors, I assign a hold rating to UA and UAA.

For further details see:

Under Armour: Partnership With Ripken Baseball May Accelerate The Growth