UAA - Under Armour: Q2 Beats But Guidance Quietly Reduced Again

Summary

- Under Armour recently reported Q2 earnings that beat low expectations.

- Revenue edged up 2%, while adjusted operating income hit $129MM, positively surprising investors.

- However, Under Armour announced that revenues will rise below its previously forecasted 5%-7% range, while the forecasted profit range fell ~10%.

- I reiterate my previous "Hold" recommendation for Under Armour from August, and forecast an $11 USD price target with an 18-month view.

Introduction & Purpose

Under Armour, Inc. ( UA , UAA ) just reported fiscal Q2 earnings (through 30 September) that beat analysts' low expectations, but didn't comfort me. The company's wholesale and shoe wear businesses generated some growth, while the high-margin direct-to-consumer business saw a decline. My Q1 update on UAA showcased a bear view, and this quarter reinforced my initial opinion. With the holiday shopping environment likely to remain challenged as rates rise and supply chain woes drag on, UAA isn't positioned well to overcome macroeconomic obstacles. Coupled with yet another guidance downgrade, and still no CEO, I reiterate a "Hold" rating with an $11 USD price target over an 18-month timeline.

Q2 Review

UAA announced Q2 earnings on Nov. 3, 2022 that shocked the market, as evidenced by the stock soaring 12% that day. Revenue edged forward 2% to $1.6Bn. The company's adjusted operating profit totaled $87MM, a decent bounce back after a sluggish Q1 . Two segments saw revenue jumps; the lowest margin business, wholesale, and e-commerce, which both increased 4%. E-commerce accounted for 36% of the revenue mix, which showcased a disappointing decline from Q1's 39%. Contrasting this increase was a significant dip in store revenue by 4%.

The company highlighted strong growth in the Asian and European markets, with both seeing close to double-digit gains. However, this was more than offset by a decline in North America by 2%, which is still the company's largest geographic footprint. Gross margins and SG&A both fell, as expected, while footwear revenue rose 14%; at face value, the quarter was relatively decent. However, beneath the surface, the same issues that have plagued UAA, unfortunately, remain entrenched. The largest segments of the business (apparel) and geographic reach (North America) continue to see slides.

UAA Q2 Earnings Release

The company didn't announce same-store sales figures, but given the in-store revenue dipping 4%, I doubt it would have been positive. CFO David Bergman provided financial updates in the investor call , highlighting that inventory was up 29%, which isn't too bad compared to other peers, some of whom have seen jumps over 70%. SG&A dipped 1% as the company rightsized their marketing spend. Executives also answered questions in the Q&A period about the health of the brand. They remained steadfast that operational and public perception improvements continue to make headway, and feel that they are gaining traction in the athlete space with minor league teams. Management also reiterated that the margins shouldn't drop too much more and that footwear and wholesale would primarily drive growth.

On the positive side, the company announced that a new CEO would be announced before the year-end. They also highlighted ambassador strength, headlined by Bryce Harper, Steph Curry, and WNBA champion Kelsey Plum, reaffirming management's confidence in collaborating with successful athletes without the budget of competitors.

The company also made negative adjustments to their guidance outlook. UAA now anticipates year-end operating profit of $270MM-$290MM, below the previous forecast of $300MM-$325MM. The company also downgraded revenue projections, now forecasting low-single-digit growth compared with the prior expectation of 5%-7% growth. Diluted earnings per share were also reduced and now expected to be $0.56 to $0.60 versus the previous expectation of $0.61 to $0.67.

With margins still expected to remain sluggish versus 2021 figures, I wouldn't buy this stock even with momentum after the share price jump. The troublesome part of margin deterioration remains operational, driven primarily by higher promotions, elevated freight expenses related to supply chain impacts, unfavorable channel mix, and the negative impact of changes in foreign currency. This means that discounted product will continue to hit the shelves heading into Black Friday and Christmas. UAA reaffirmed their expectation to spend $225MM in CAPEX, in line with prior communication.

The company repurchased $25MM of shares during the quarter, cancelling 3.2MM shares. They still have approximately $150MM remaining under authorization to buy back shares. With profit headwinds, I still doubt they complete the buyback program in full.

Model & Conclusion

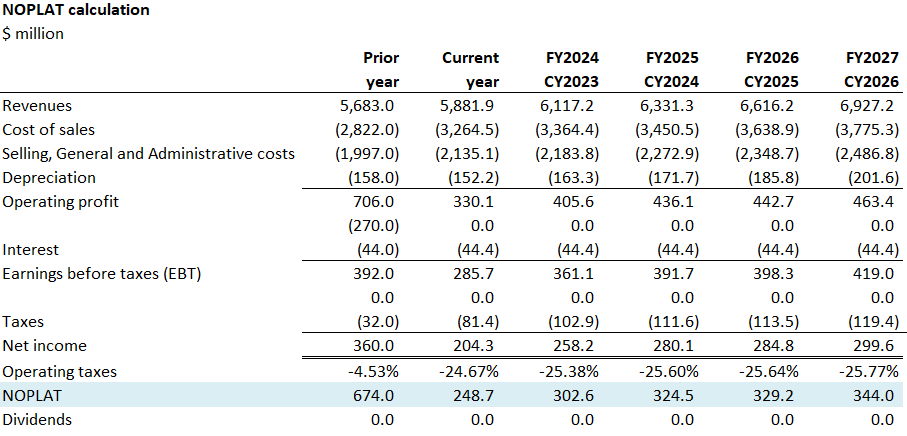

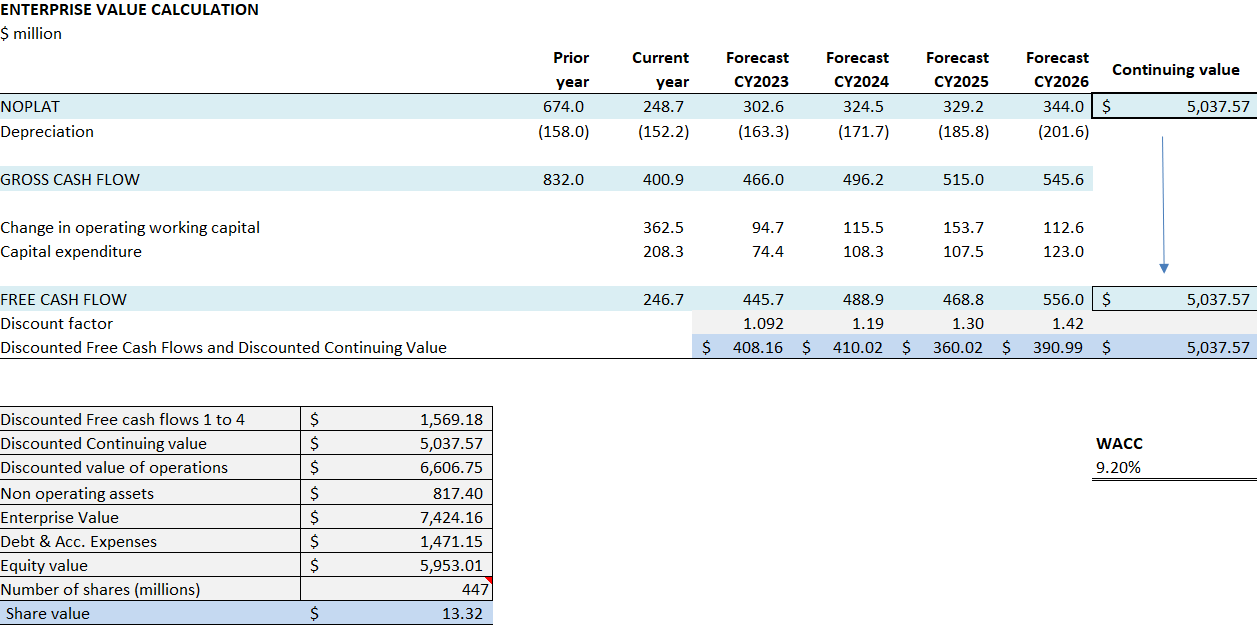

While I don't foresee a sustained share price comeback, the model still shows that if the company can deliver on forecasted growth, there's some runway for the stock to rise. The company's cash position is starting to stabilize, and I doubt that guidance will be reduced yet another time. The model forecasts a WACC of ~9.2%, a little higher than my previous outlook, with minor updates to the market premium and the 10-year paper.

Author WACC

I forecast the continuing value above $5B, given a 3.5% revenue increase this year and blended revenue growth of ~4% for the three years after. I hold other cost ratios mostly equal as a percentage of revenue from the previous forecast, with only minor updates per guidance from management. As discounted merchandise sales start negatively affecting the bottom line, I believe CAPEX spend will slow, to $208MM vs. the expected $225MM.

A $13 share price (see below) can be supported with fundamentals. However, I think that new leadership will have some growing pains and that the share price will not support the CY2023 EV/EBITDA model forecast of 13. Slashing the share price prediction to $11 based on negative company intangibles and historical lack of support from Wall St. showcases an EV/EBITDA of 10.3 and a calendar year CY2023 EPS of $0.58, within the updated range. In today's price target, I estimate 447MM shares outstanding given the share buyback has continued, albeit at a slower pace.

{kind=link}

{kind=link}

While UAA had a decent quarter, the company remains an underperformer versus peers. UAA is now well into a transition plan that has yet to significantly pan out, though at least the next CEO will soon be announced. The company guided margins and profit down again, and with retail sales slowing and elevated inflation, I still project an $11 price target for Under Armour with a "Hold" rating.

For further details see:

Under Armour: Q2 Beats, But Guidance Quietly Reduced Again