UAA - Under Armour: Still In Troubled Waters

2023-03-06 12:50:22 ET

Summary

- Q3 results beat expectations, but there are some serious weaknesses.

- The increase in inventory levels could lead to a snowball effect.

- The company needs to improve its positioning in the premium market.

- Despite the undervaluation, the company is still not a great pick in my view.

Under Armour ( UA ) ( UAA ) has been facing several challenges in recent years, including low revenue growth, intense competition, and issues related to its brand perception. In this article, I will examine Under Armour's recent financial performance, its strengths and weaknesses, its position in the sportswear industry, and why, despite the current undervaluation and the good quarterly results, the company is still not a great pick.

Under Armour's Q3 2023 results beat expectations, but there are serious weaknesses

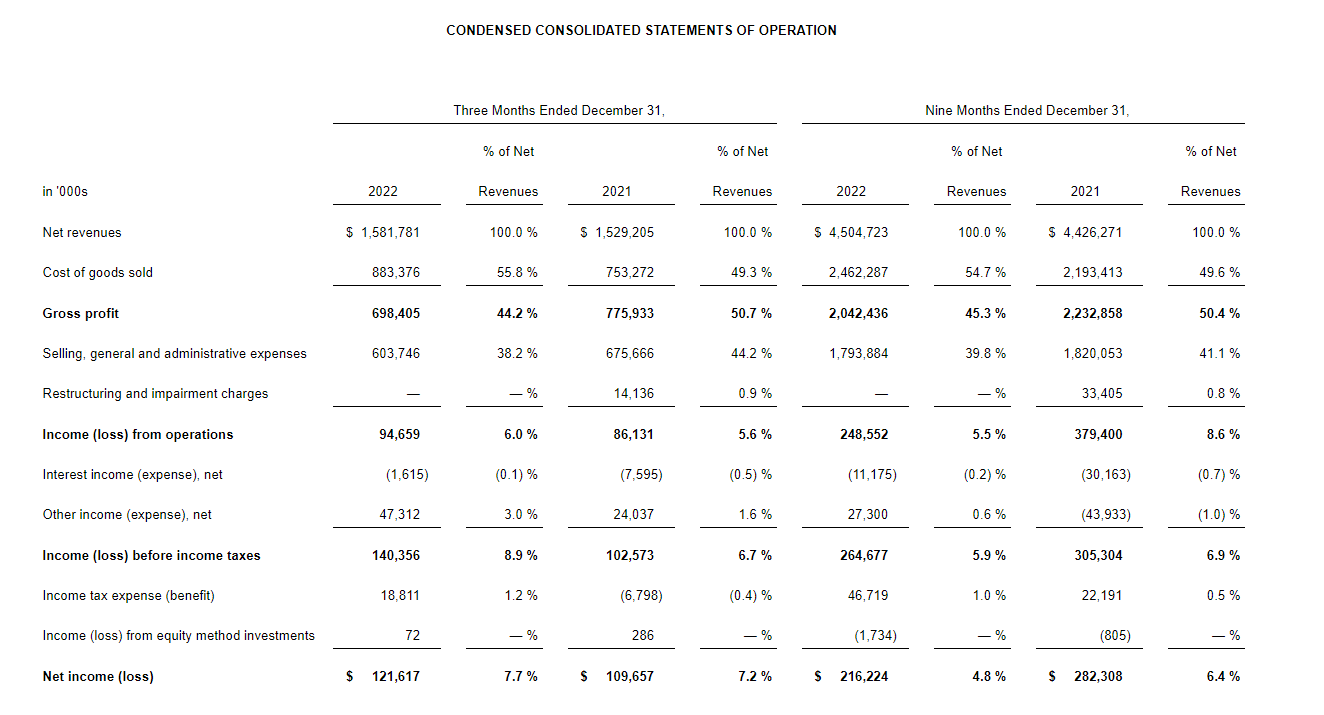

In the last quarterly results , Under Armour beat expectations, but in my opinion, there are some key points that show Under Armour is still facing headwinds. Here is a summary of the latest earnings call:

- Under Armour reported a diluted earnings-per-share profit of $0.16 for fiscal Q3 2023, beating analyst estimates by $0.07.

- Revenues grew YoY by 4.6% to $1.60 billion, beating analyst estimates of $1.55 billion.

- Wholesale revenues grew by 7%, while direct-to-consumer DTC revenues fell by 1% to $715 million.

- Gross margins declined YoY by 650 bps to 44.2%, due to higher promotions and FX, while inventory increased by 50% to $1.2 billion.

- Under Armour raised its fiscal full-year 2023 EPS guidance to $0.52 to $0.56, from its previously lowered guidance of $0.44 to $0.48 in the prior quarter's report.

- The company expects revenue to grow in constant currency at a low single-digit percentage range, with gross margins expected to fall between 375 bps to 425 bps.

- Under Armour's North American revenues fell by 2% YoY, while international revenues rose by 14% to $527 million.

- The company closed the quarter with $850 million in cash and cash equivalents.

Third Quarter Fiscal 2023 Results (UAA IR)

{kind=link}

What concerns me the most, is that Under Armour's inventory levels increased by 50% YoY to $1.2 billion, which could be due to weak sales or overproduction. Moreover, the company's gross margins declined YoY by 650 bps to 44.2%, due to the shift towards e-commerce sales and higher promotions. This activity may be necessary to drive sales, but it is not sustainable in the long run!

These elements, combined with intense competition in the sportswear industry, are putting pressure on Under Armour's growth prospects. Indeed, while the company's revenue growth has improved from the previous quarter, it is still below the industry average, making it the last pick among the main players in the industry.

Therefore, Under Armour must quickly address inventory levels and focus on improving gross margins to remain competitive in the industry before it is too late, as this situation could lead to an oversupply and further margin reductions.

Brand Perception

Another issue Under Armour is facing regards its brand perception. I am not saying that Under Armour's brand is not strong enough, the opposite, but if I had to choose between UA, adidas (ADDYY), and Nike (NKE), I would probably choose the latter ones.

Let me explain. First of all, Nike and adidas have a larger loyal-customer base thanks to their reliability and the market segment they are targeting. Indeed, adidas and Nike have established themselves as premium brands, associated with high-quality products, innovation, and cutting-edge design. Therefore, this "premium" status allows them to appear slightly better than Under Armour and to increase prices without losing customers.

On the other hand, in the last few years Under Armour has positioned itself as a brand for athletes, emphasizing performance and functionality. The company has invested heavily in research and development, particularly in areas like material science and wearable technology, and it has launched new marketing campaigns featuring famous athletes (Stephen Curry, Tom Brady, and The Rock). Additionally, Under Armour has been investing in its direct-to-consumer channels, such as its e-commerce platform and its physical retail stores, to create a more personalized and engaging shopping experience for customers.

However, despite all efforts, adidas and Nike seem to be doing better for now. In fact, Under Armour needs to expand its appeal beyond the athletic market, similar to Nike's foray into mainstream fashion. Without this, the brand will not be able to charge premium prices for its products.

Moreover, its competitors, particularly Nike, are trying to find new ways of advertising in order to gain new markets. For example, in 2021, Nike created NIKELAND, a virtual world built in Roblox (RBLX) that offers mini-games: this would probably allow the company to sell virtual sneakers or reduce development costs by making virtual samples before launching new products on the market. Under Armour is far away from this!

Therefore, Under Armour is trying hard to bridge the gap with adidas and Nike, but still not enough to make the definitive qualitative leap and reach its two main competitors in my opinion.

What about the valuation?

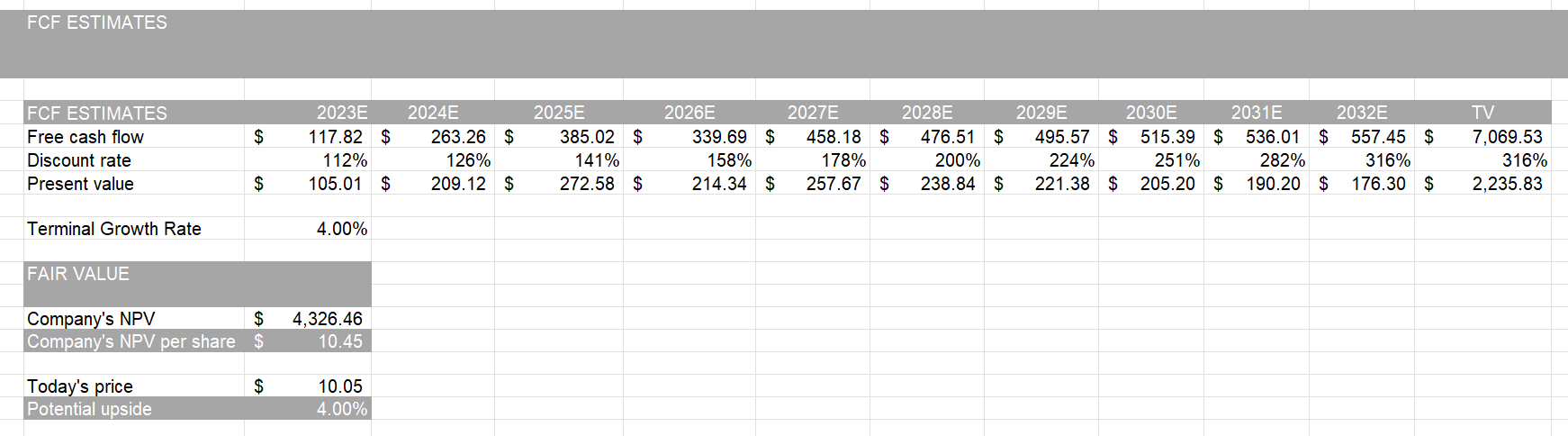

To calculate the intrinsic value of Under Armour, I used a DCF model. Below you find the final table and the results. In particular, I made some assumptions to reach the most realistic value possible and thus model the data based on what I expect from the company in the next few years.

DCF Final Table (Personal Excel Model)

{kind=link}

According to analysts, the global sportswear market is expected to grow at a compound annual growth rate of 6.7% from 2022 to 2028. Therefore, I modeled revenue to reflect this trend and set a terminal growth rate from the end of 2028 at 4.00%, as I expect a slight decrease in growth if the problems I explained above will continue to persist.

The company appears to be slightly undervalued, with a fair value of $10.45 and therefore a potential upside of 4.00%.

Furthermore, Under Armour appears to be undervalued even compared to its industry peers. The company's P/S (price sales) reached x0.82, while the same ratio for Nike is x3.84, for adidas is x1.18 and for Lululemon Athletica (LULU) is x5.32.

Final thoughts

The company, as can be seen from the DCF model, is slightly undervalued, also compared to its market peers. However, a 4.00% safety margin seems too little for the company to be considered a value deal. Moreover, this undervaluation has its reasons!

There are some structural problems that need to be resolved as soon as possible, and the recent setbacks certainly don't help the situation. Finally, in order for the company to be able to compete again with its peers and acquire a real competitive advantage, it needs to review its brand and try to position itself in the premium segment of the market. The new management will most likely bring positive surprises, but until sales results are seen, the company remains a "sell".

For further details see:

Under Armour: Still In Troubled Waters