UAA - Under Armour: Weak Sales And High Inventory Merits Caution

2023-10-17 02:15:15 ET

Summary

- Under Armour continues to struggle with declining sales, particularly in its key North American market.

- The challenging retail environment in the US, with increased promotional strategies and high inventory levels, has contributed to the decline.

- The company's direct-to-consumer business shows promise, but the lack of focus and clear message about the brand remains a challenge.

Under Armour, Inc. (UAA) has long suffered from declining sales. A trend that has continued in its most recent quarter. These sales declines are likely to persist in the upcoming quarters and will be exacerbated by continued weakness in the broader US retail market. Under Armour witnessed a notable 9.1% dip in sales in its key North American market.

A significant portion of this decline is attributed to the challenging retail environment in the United States, where apparel vendors have increasingly turned to promotional strategies to clear their inventory. This surplus of stock at retail outlets housing Under Armour products has translated to fewer orders being placed, as these retailers strive to sell their existing inventories first. At the same time, Under Armour itself has seen a surge in inventory levels increasing the risk of income volatility and margin pressure in quarters ahead.

While Under Armour has an attractive valuation, I currently rate the stock a hold. The primary motivator for the hold rating is the continued decline in sales and the associated volatility in the share price that could come with this decline in sales.

Sales and Earnings Outlook

Under Armour reported a 9.1% decline in sales in North America, the most important market for the company. Despite the decline in sales, net income was up slightly amidst a decline in costs. These lower costs were primarily driven by lower transport costs in the first quarter of 2024.

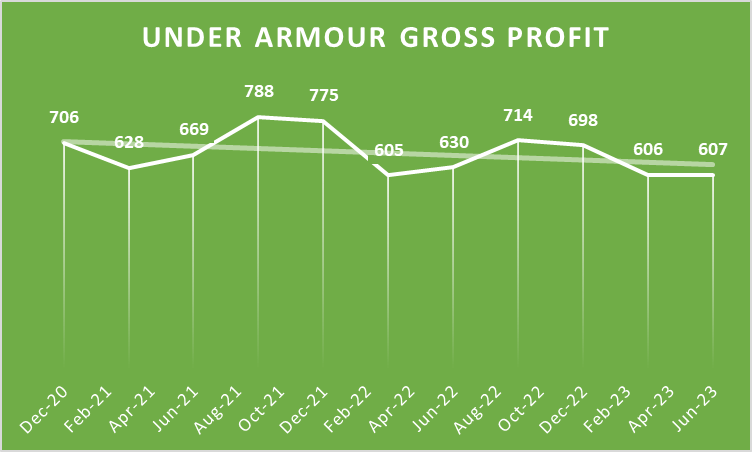

When viewing Under Armour's gross profit over the course of the past few years, as depicted in the chart below, it is clear that there has been fairly significant earnings volatility. This is not entirely unexpected given the cyclical nature of its business. However, in my view, there has been a clear downward trend despite occasional upticks in recent quarters.

{kind=link}

Nevertheless, management expects earnings to remain flat for the year as a result of the challenging sales environment. In my view, any further decline in sales is likely to filter through to lower earnings unless further cost reductions can be achieved. The company has attributed a substantial portion of the decline in sales to the challenging retail environment in the United States where apparel retailers have increasingly resorted to promotions in an attempt to clear inventory. These elevated inventory levels at retail stores stocking Under Armour’s products has resulted in fewer orders being placed as these retailers seek to clear their stock first.

Interestingly, Under Armour’s products in the athleisure segment should be less impacted by the weak retail environment than it is. The athleisure segment of the market in general has witnessed strong sales growth in 2023 despite weaknesses in other retail segments. It is Under Armour’s reliance on hard-hit retailers such as Kohl’s which has likely contributed the most to its declining sales. GlobalData noted that the customer base at these retailers is somewhat more affected by inflation, causing them to cut back on spending more significantly.

As I previously observed , the drop in sales to middle-income consumers has been observed across various retailers, as these customers are increasingly reducing spending on non-essential items and adopting a more cautious approach to expenses. This shift in consumer behaviour is a response to consistently elevated levels of inflation and doesn't appear likely to revert back in the foreseeable future. While Under Armour’s primary target market has not been as affected by inflation, the wholesalers it depends on are very dependent on those consumers and have seen a decline in sales which has a knock-on effect on Under Armour.

Neil Saunders, an analyst at GlobalData, opined that while Under Armour does have some strong wholesale partners like DICK'S Sporting Goods ( DKS ), they don't fully compensate for weaknesses in other areas. They also don't address the fundamental issue of not having more of their own brand stores, which Saunders notes has been a crucial factor in driving brand strength and revenue growth for companies like Lululemon and Fabletics. Saunders is of the view that this lack of direct distribution has consistently been a challenge for Under Armour.

While the reliance on other retailers has certainly been a challenge for Under Armour, I am not quite sure if I would support a strong push for company owned stores. The direct-to-consumer segment of Under Armour’s business has certainly been an outlier in terms of performance with growing sales. However, the company’s direct-to-consumer revenues increase of 4% in the first quarter of 2024 was driven primarily by a 6% increase in ecommerce sales.

Therefore, while I agree that Under Armour needs to strengthen its direct-to-consumer business, I don’t think that necessarily means brick-and-mortar stores. Interestingly management indicated that “Under Armour products featured in post on Instagram and TikTok and working towards direct purchase and checkout on their platforms; another step in enhancing our omnichannel capabilities.” I will be closely monitoring this to see if it can be successfully implemented and what this would ultimately mean for strengthening Under Armour’s direct-to-consumer business.

Furthermore, one of the longest standing critiques against Under Armour has been a lack of focus and the absence of a clear message that makes it clear to consumers what exactly makes the Under Armour brand unique. The new PTH 3 strategy seems to acknowledge this with the second-pillar of the strategy focused on product design and specialisation in particular categories. While this doesn’t fully answer the question on what makes Under Armour unique, it is certainly a step in the right direction to a more focused company in my view.

Balance Sheet and Inventory

Under Armour’s balance sheet appears to be quite strong with generally manageable debt levels. The company’s net debt to earnings before interest, taxation, depreciation and amortization (EBIDTA) ratio is around 1.92 which is broadly in line with that of its peers included in the peer comp chart below. While the cash and marketable securities on the company’s balance sheet has declined in recent quarters, it still has more than $700 million available.

Author created based on data from EquityRT

{kind=link}

While the balance sheet as a whole does not raise concern, high inventory levels merits closer attention. The company reported a 38% increase in inventory levels in the first quarter of 2024. This increase was partially expected given that inventory levels were much lower in the previous quarter, but the substantial increase remains a concern.

The concern arises particularly as the company has noted that high inventory levels has necessitated resort to promotional sales to attempt to clear inventory. Management has also indicated that it will appoint a Chief Supply Chain officer to better-manage inventory levels going forward. Investors in the company would need to monitor any further inventory increases in the quarters ahead closely.

Valuation

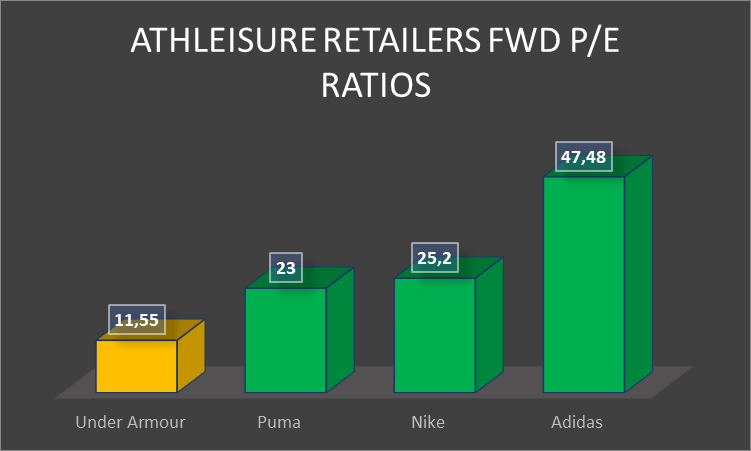

Under Armour is trading at a forward P/E ratio of around 11.5 which is the lowest of the athleisure brands included in the peer comp charts below. It is also well-below the company’s 5-year average forward P/E ratio of around 14.78. This discount is largely driven by concerns over the declining sales.

Author created based on data from EquityRT

{kind=link}

The substantial discount to its historic average P/E ratio certainly suggests that the market has priced in much of the risk of declining sales. However, the share price may nevertheless experience greater volatility as the sales picture remains uncertain in upcoming quarters. It is this uncertainty that makes me hesitant to rate the stock as a buy even if the price seems quite good and fairly close to fair value.

In rating the stock as trading near fair value, I am cognizant of the historic average P/E ratio and the need to discount somewhat for the current volatility. The decline in operating margins further justifies a discount to its historic average valuation levels, in my view.

Conclusion

Under Armour, Inc. continues to grapple with declining sales, a trend that persisted into the latest quarter. In my view, this downturn will also persist in the coming quarters, compounded by ongoing challenges in the broader US retail market. Nevertheless, the growth in the company’s direct-to-consumer business is promising and could contribute to a turnaround in the sales slump in the longer term.

Under Armour's new PTH 3 strategy also aims to bring a sharper focus on product design and specialization in specific categories. While this doesn't entirely clarify what sets Under Armour apart, it represents a step towards a more focused company. This could also contribute to an improvement in its sales outlook in the longer term and is, in my view, a positive development.

In terms of valuation, Under Armour's forward P/E ratio is notably lower than its historical average, reflecting concerns over declining sales. This discount suggests that much of the risk has been factored into the stock price. However, the uncertainty surrounding future sales performance warrants caution in rating the stock as a buy, despite the seemingly attractive price

For further details see:

Under Armour: Weak Sales And High Inventory Merits Caution