XYLD - Understanding Covered Call Risk With XYLD

2023-08-04 11:38:15 ET

Summary

- Covered call ETFs like XYLD offer attractive yields for income-seeking investors, but have underperformed the broader market over the past ten years.

- The strategy of selling covered calls comes with a capped upside and unlimited downside.

- Investors in XYLD should closely monitor the moneyness figure to assess the performance of the options sold over time.

An Interesting Concept

An enamoration with covered calls is something that most investors will go through at some point in their investing lives. The concept is certainly enticing--sell for a premium the right but not the obligation to purchase shares owned by the investor for a price above the price today. If the shares price goes nowhere, then the investor wins in the sense that they get to keep the premium collected from the option. If the shares go down, the investor has a cushion or sorts in the sense that the premium collected against the position is still technically a return on investment. If the shares go up and through the agreed price (the strike price), however, the investor loses the additional gains on the shares.

Given the attractiveness of this concept overall, it's not surprising that covered call ETFs have remained quite popular over the years. A concept on paper, however, does not always translate to an attractive investment in real life.

Today, we will consider the Global X Funds S&P 500 Covered Call ETF ( XYLD ), and see if the lure of covered calls against an index present a compelling case for investors.

Let's dive in.

Who Is The Buyer?

As stated above, covered calls have an implied cap on gains. That is, if the agreed upon strike price is 5% above the current price, the most a seller of covered calls can expect to gain on their underlying equity position is the 5% of upside. Thus, this is likely not exactly a strategy befitting hyper-aggressive investors who want to capture every bit of upward momentum. Generally speaking (very generally), XYLD and other ETFs like it are geared towards investors who are primarily seeking income through the collected options premiums.

{kind=link}

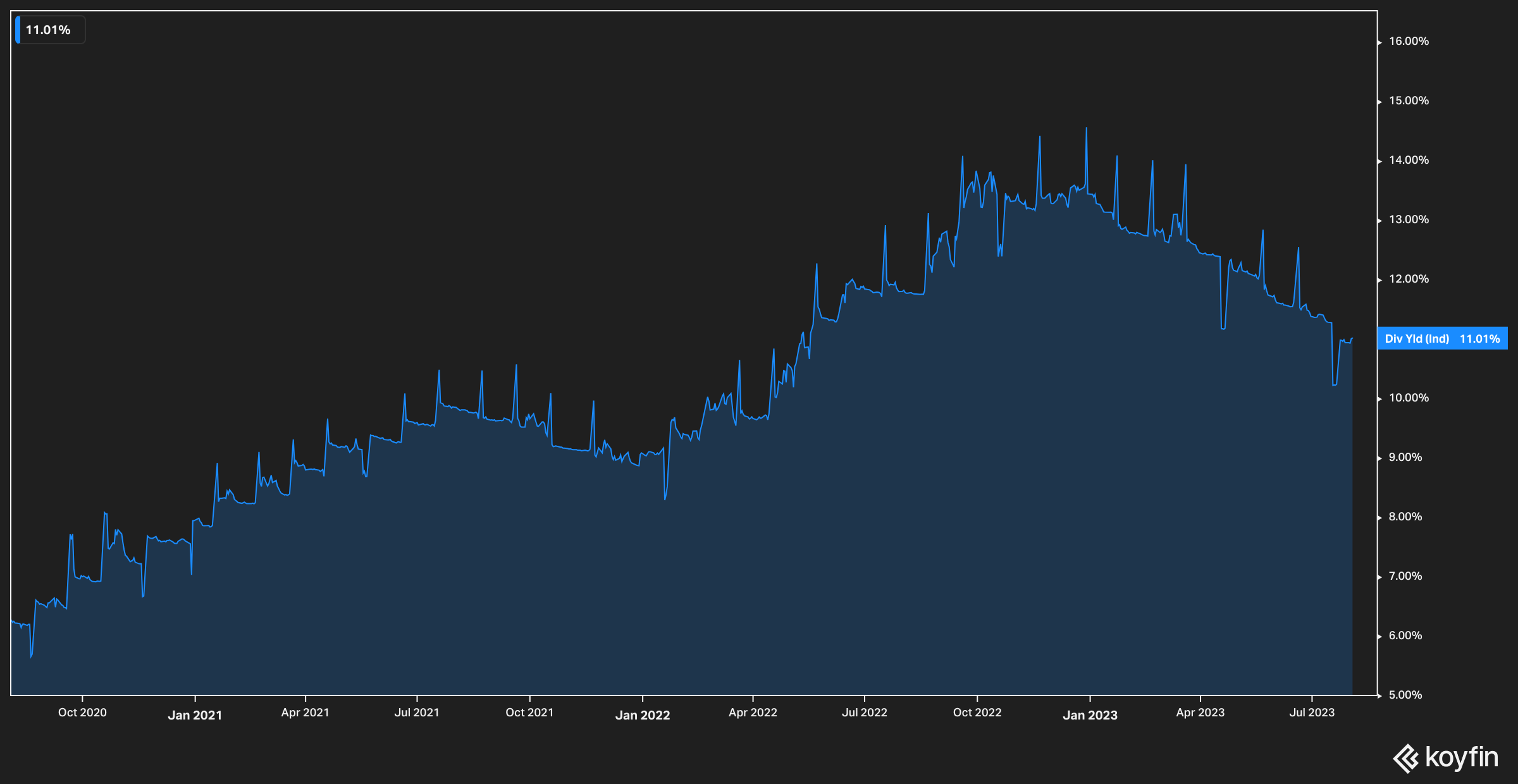

To this end, as of this writing XYLD has a current yield of 11%, which is no doubt attractive to income-seeking investors. There is, however, a trade off that comes with collecting said yield.

{kind=link}

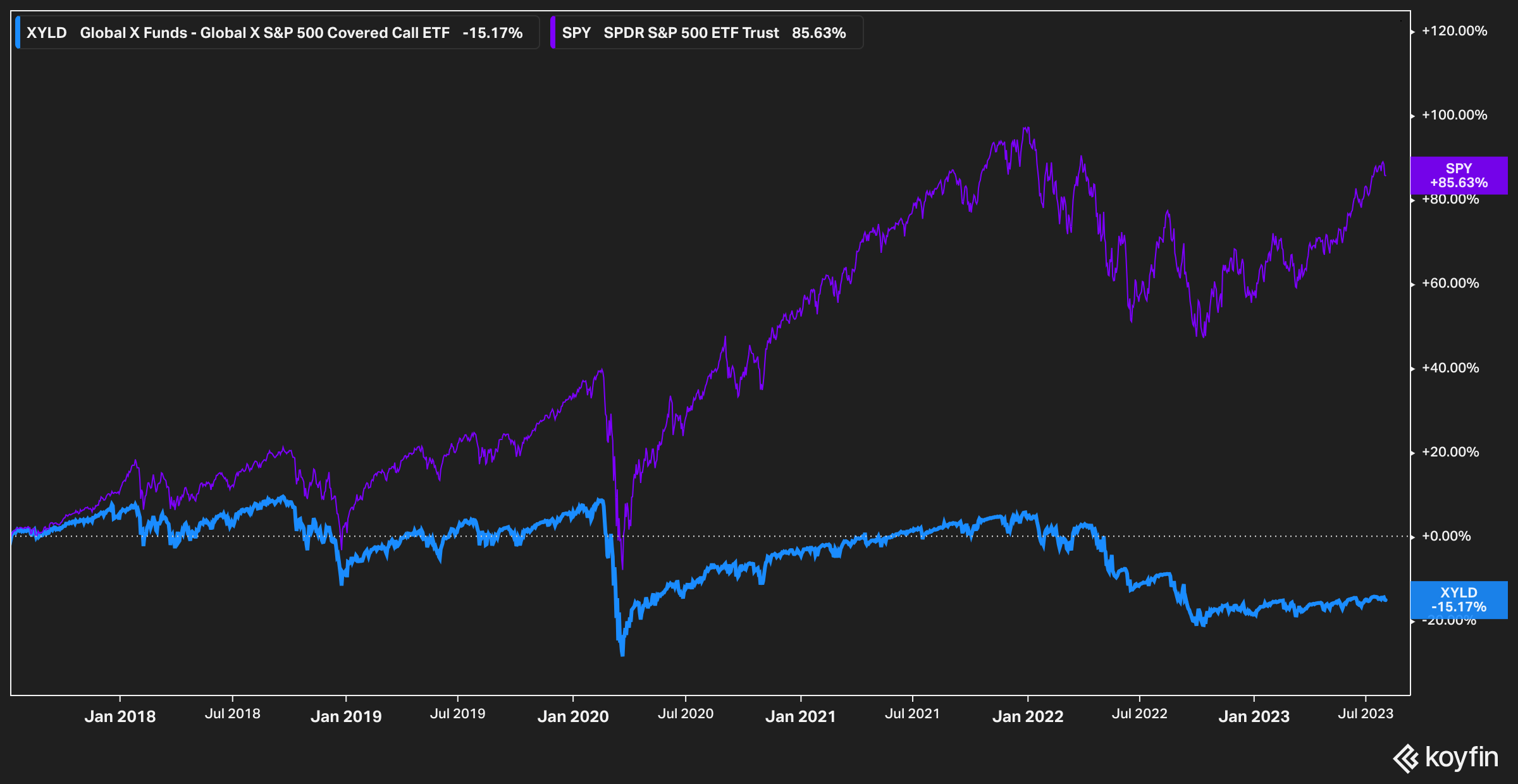

The above chart illustrates the point. Over ten years the share price of XYLD has declined by 15%, versus the broader S&P 500's ( SPY ) return of 85%.

This 15% decline, of course, does not depict the dividends paid nor show the return an investor would achieve if the dividends were reinvested (it likewise does not account for the ETF annual fees).

{kind=link}

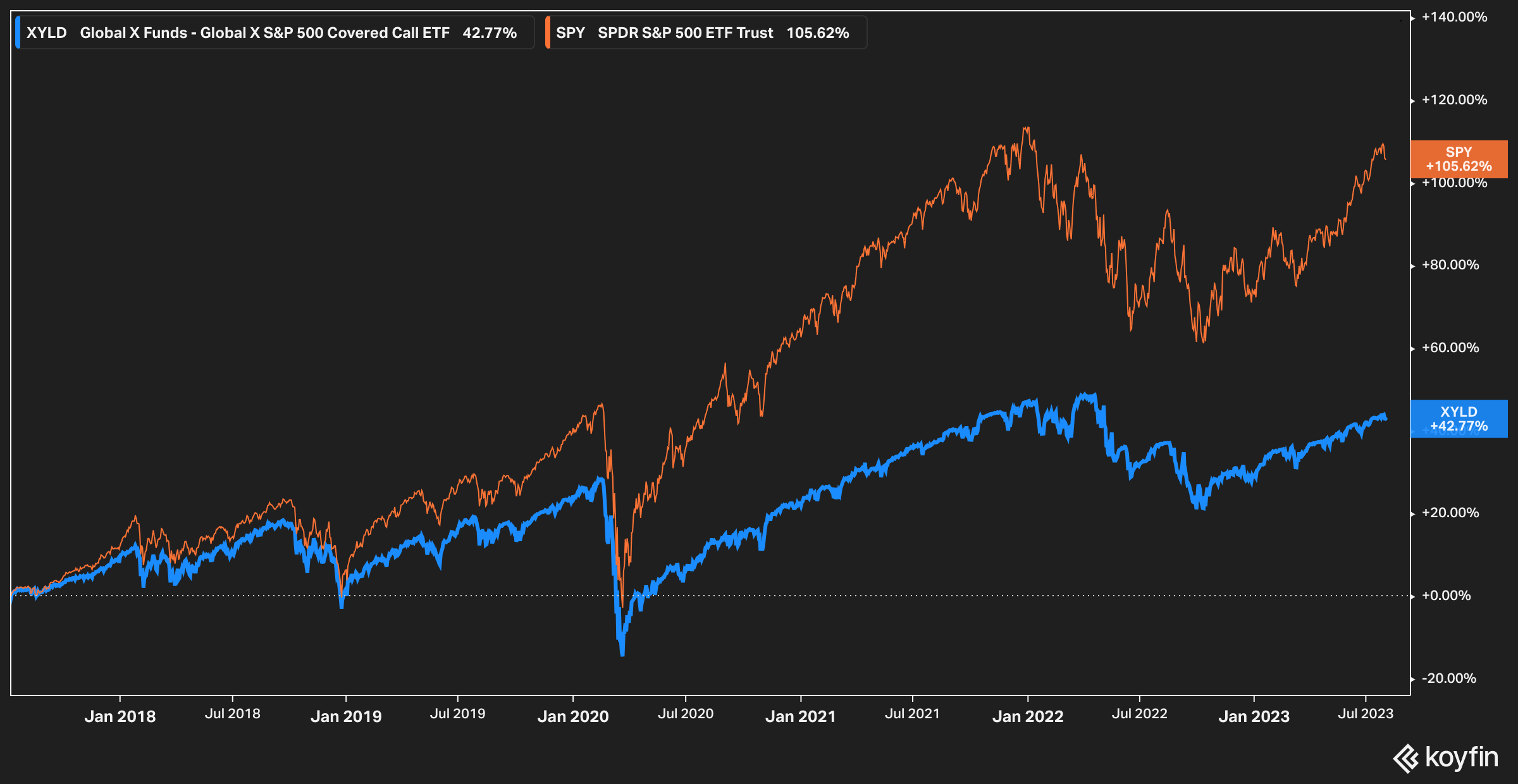

Total return (pictured above) does depict those returns (minus the fee deductions). Holders of XYLD that reinvested dividends over the past ten years would still not outperform the broader market, but would have seen a return of 42.7% as of this writing.

In this regard we must say that the ETF has not performed terribly--investors who have been in the ETF in at least the time frame depicted above have generated a return for themselves, even with the share price depreciation.

Understanding The Risk

For some investors, the underperformance of covered call ETFs like XYLD are a feature, not a bug. They are content to collect the premium divvied out each month without worrying about the underlying price. Other investors, however, have a misguided notion that covered calls are something like an insurance policy.

The bald truth, however, about covered calls is that the seller of the calls retains a capped upside, while retaining unlimited downside. The strategy is also inexorably linked with the risk of the options market.

In an ideal world, covered calls would be sold against stocks that are expected to essentially tread water. In this scenario, the covered call seller is the winner (they gain a premium and incur no loss) and the option buyer is the loser.

Options markets, however, price in a particular stock's expectation of volatility, known as implied volatility , or IV. Options market participants and options market makers thus do not place sizable bids on equities that are not expected to move in the selected time frame (in XYLD's case, options are purchased monthly).

Thus, a stock that is moving sideways may have a thick options market (a lot of buyers and sellers), but the premium associated with each strike price further away from the current equity price will be drastically lower than for a stock that is, say, about to report earnings or which has a significant amount of hype around it.

In other words, the juice (the premium collected) may not be worth the squeeze (putting your underlying equity position at risk of being called if the stock moves up).

Or, in other-other words, covered calls are not the easy money they can be made out to be. Unless one has made peace with the fact that not all upside will be captured while all downside moves will be fully felt, the strategy may not be for them.

In Practice

The investment strategy of XYLD as stated in its summary prospectus is to invest at least 80% of assets into the securities of the CBOE S&P 500 BuyWrite Index, the holdings of which essentially mirror the S&P 500.

Once the funds are invested monthly call options are sold against the position. The premiums collected from these monthly options are distributed to shareholders in the form of dividends.

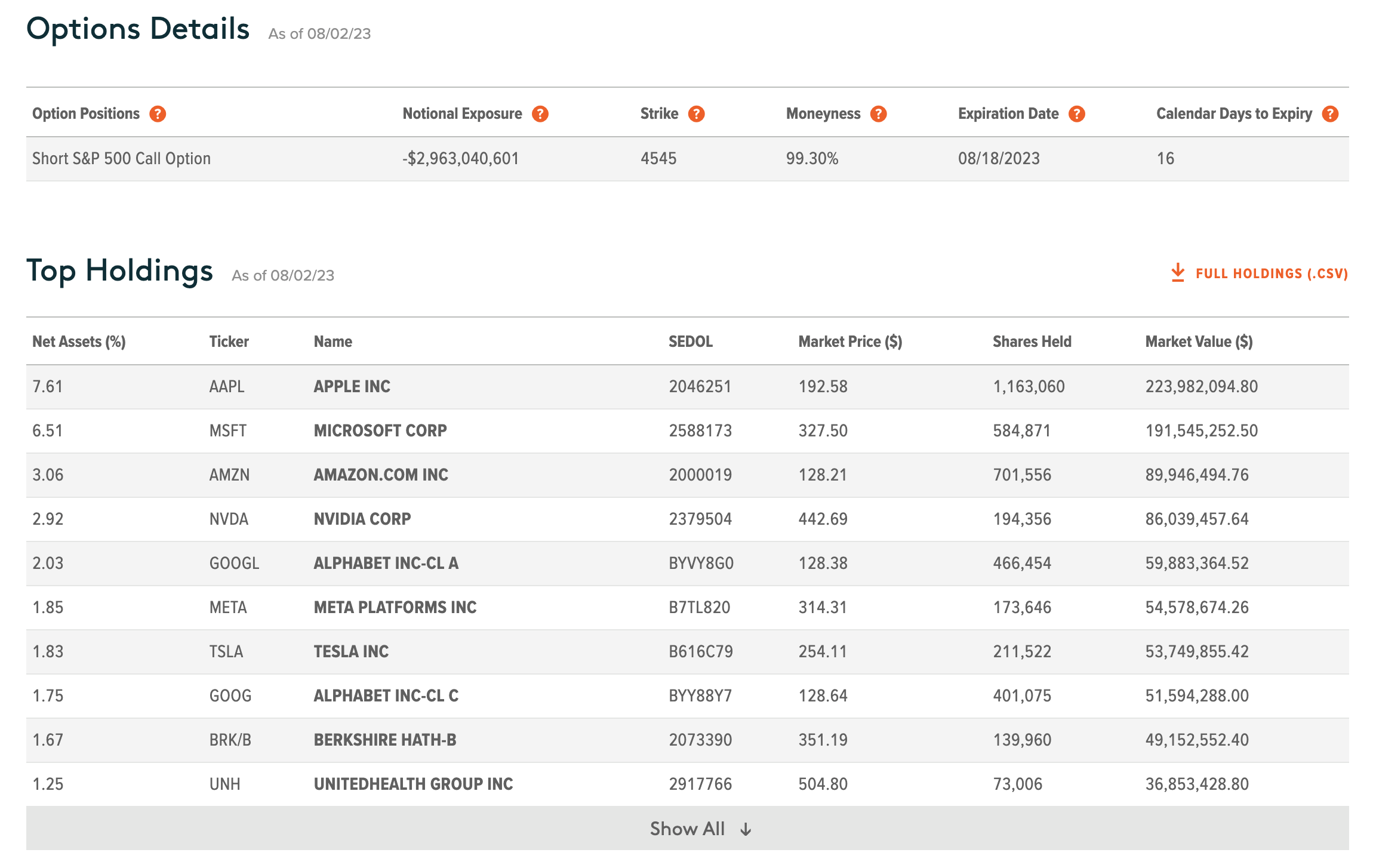

An important metric to note for investors in XYLD is the current state of the funds options, and how close to the money they are. The fund updates this regularly on its website , and by viewing it investors can view current holdings and some pertinent information about the current options position.

{kind=link}

In our opinion, one of the most important things to note here is the 'Moneyness' figure in the screenshot above. Moneyness is essentially how close an option position is to the strike price. The closer to 100 the number, the closer to the strike price. Moving past 100 means that the option is in the money, and thus very likely to be called.

A current moneyness of 99.3% is an indicator that the index price is very close to the strike price (the strike indicated in the screenshot is 4545 for the S&P 500). It's our opinion that investors in XYLD would do well to keep a close eye on this figure over time to assess how well the options sold are performing over time.

The Bottom Line

XYLD is an S&P 500 Covered Call ETF. While the fund has delivered negative returns for shareholders on a long term basis in terms of price appreciation, it has been positive overall for those who have reinvested dividends. Given the capped upside and unlimited downside of the covered call strategy, we think that only certain investors are likely suited for the strategy in the long run, and it is likely not compelling for investors seeking unlimited upside gains. Given this, we remain on the fence when it comes to XYLD.

For further details see:

Understanding Covered Call Risk With XYLD