UNIRF - Unibail: I'm No Longer Expecting A Meaningful Dividend In 2024

2023-09-06 08:30:00 ET

Summary

- Unibail's focus on repairing its balance sheet and exiting the North American market has delayed the re-establishment of dividends.

- The REIT's rental income and Adjusted Recurring EPS are improving on the back of a higher net rental income.

- Unibail's net rental income and Adjusted Recurring Earnings per Share have increased, but its high LTV ratio and potential impact of higher interest rates on asset valuations are concerns.

Introduction

For a long time, I have not been too impressed with Unibail ( UNBLF ) ( UNIRF ) as its acquisition of Westfield in combination with a subsequent COVID pandemic have put pressure on the balance sheet. The commercial REIT hasn’t paid a dividend for years as the sole focus is on repairing the balance sheet while exiting the North American market. That exit is going slower than planned (obviously caused by the changing market circumstances), and although Unibail was originally guiding for the dividend to be re-established in 2024, the company has not provided any additional guidance on this.

{kind=link}

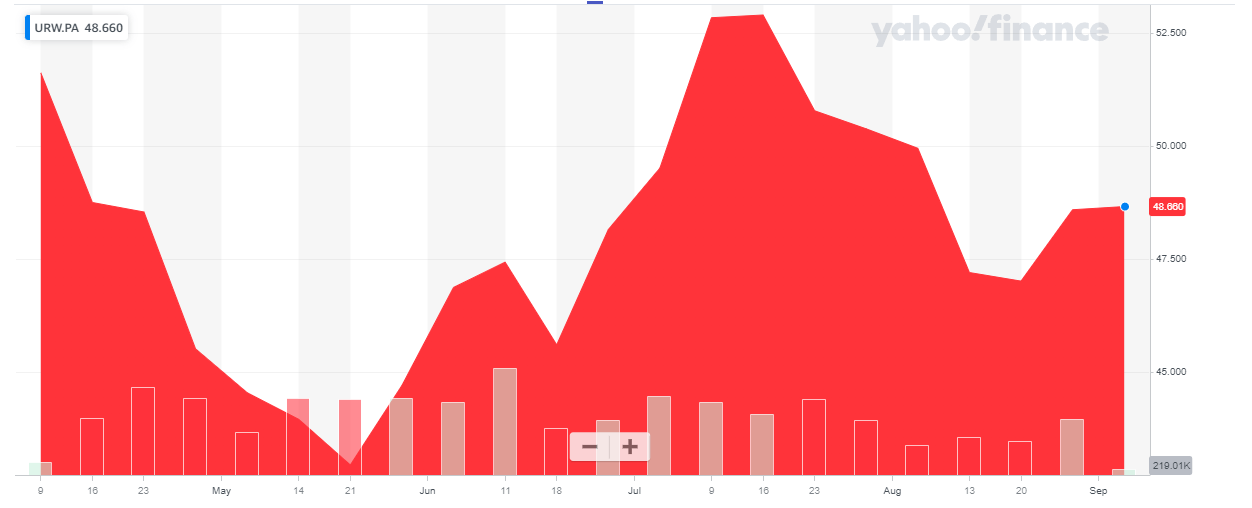

Unibail has its primary listing on Euronext Paris (it moved to Paris from Amsterdam) and the average daily volume in Pars is just over 420,000 shares, representing a monetary value of 20M EUR. As Paris offers the best liquidity to trade in Unibail’s shares, I would strongly recommend to use that exchange to trade in the company’s securities. I will use the Euro as base currency throughout this article as that’s the currency Unibail is trading in and reports its financial results in.

The earnings remain strong, and the liquidity on the balance sheet continues to improve

As the balance sheet is the REIT’s primary concern, this automatically means we need to keep an eye on the rental income and the AREPS (the Adjusted Recurring EPS). As the REIT does not pay a dividend, it is able to retain the adjusted recurring income on its balance sheet.

Unibail Investor Relations

The first semester of 2023 was characterized by the continuous increase of the footfall and tenant sales compared to the first half of 2022, as you can see above. That’s good news for Unibail as it means its tenants are definitely seeing the consumers returning to their stores. And while I acknowledge the revenue of a tenant does not say anything about its profitability, it is a good sign.

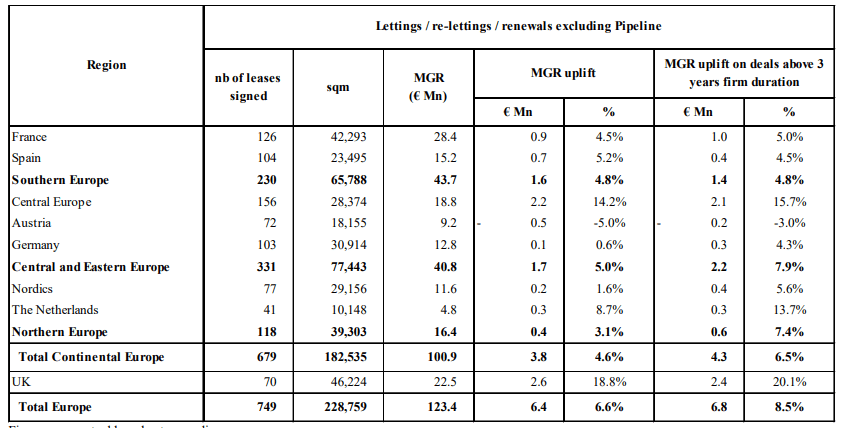

A second important element is the lease renewals. As you can see below, the REIT confirmed a leasing spread of 4.6% (on top of the indexed passing rents). And surprisingly, the longer-term deals (defined as having a duration of in excess of 3 years) had an even higher spread of 6.5%.

{kind=link}

The main takeaway here is that the commercial space owned by Unibail is still highly sought after. Occupancy on a GLA basis exceeded 92% in June, while 96% of the H1 rent was collected.

The strong performance and inflation-linked rent increases were very clearly noticeable in the net rental income result. As you can see below, the NRI increased by 5.3% in Europe to 782.5M EUR. That’s 1.57B EUR on an annual basis. The total net rental income increased by just 1.1% to 1.15B EUR. That’s a pretty low percentage compared to the European NRI growth, but the disposals in the USA obviously had a negative impact on the NRI result. On a like-for-like basis, the Net Rental Income increased by 8.2%.

{kind=link}

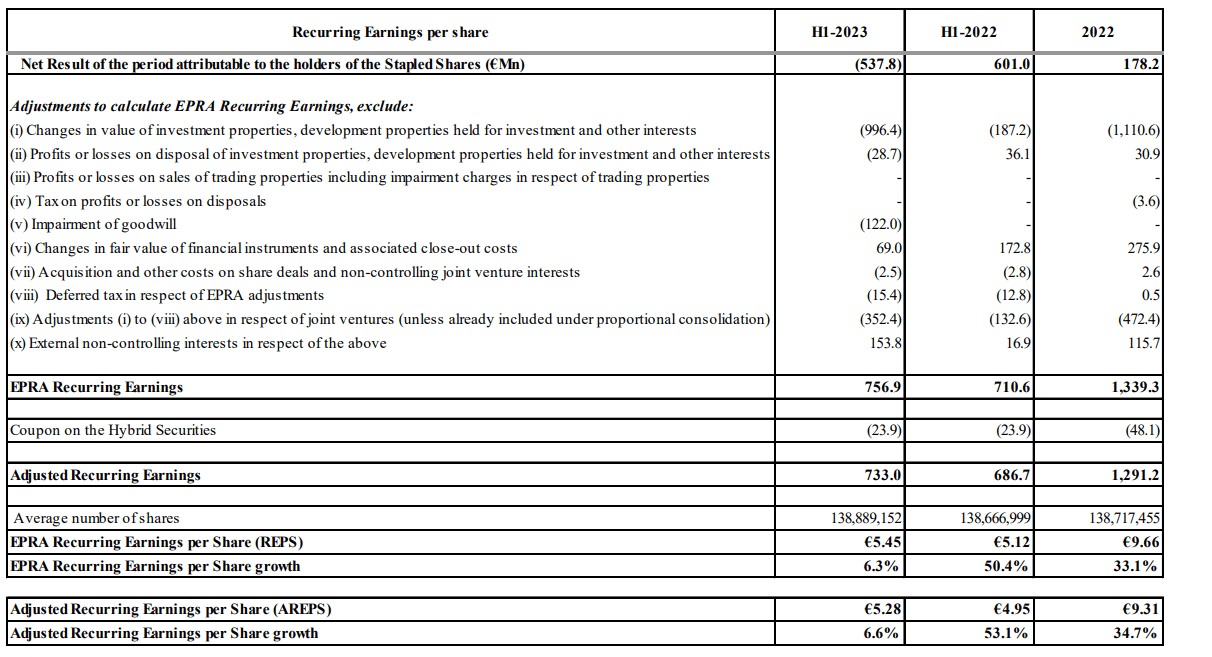

The total Adjusted Recurring Earnings per Share (comparable to the FFO) came in at 5.28 EUR in the first half of this year. And that includes the 24M EUR impact from the coupon payments on the hybrid instruments.

{kind=link}

Right before the end of the second quarter, Unibail proposed a swap to its hybrid bondholders whereby they would be allowed to convert their equity-like deeply subordinated bonds for a perpetual bond with a 7.25% coupon. That’s more than 500 bp higher than the initial cost of the hybrid bond, but the high acceptance rate of the proposed swap is encouraging. You can read about that deal here.

It will increase the interest expenses, but that was inevitable anyway as the interest rate on the hybrid securities would have reset this year anyway.

I’m not too concerned about the balance sheet

I was a bit surprised when I learned some of the analysts are a bit uneasy when it comes to Unibail’s balance sheet and LTV ratio. For some reason, the market is only now waking up to the risk the higher interest rates are posing on the level of asset valuations. Everyone seemed overly concerned about the impact of higher interest rates on the FFO and AFFO (and that’s definitely something to keep an eye on), but not a lot of investors seem to have questioned the impact of a higher risk-free interest rate on the capitalization rates used for the valuation of the properties.

While there is not necessarily a 1:1 correlation, a 300 bp increase in the risk-free interest rate for sure has an impact on the capitalization rates, and thus the valuation of assets.

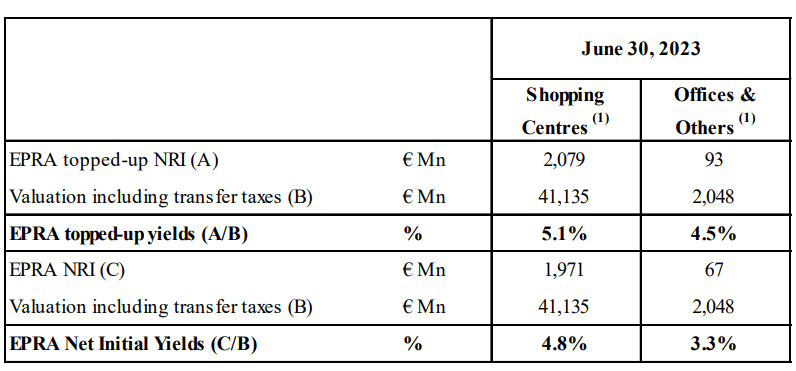

As of the end of H1, Unibail’s assets were valued at a 5.1% topped up yield based on the NRI (the European equivalent of the NOI).

{kind=link}

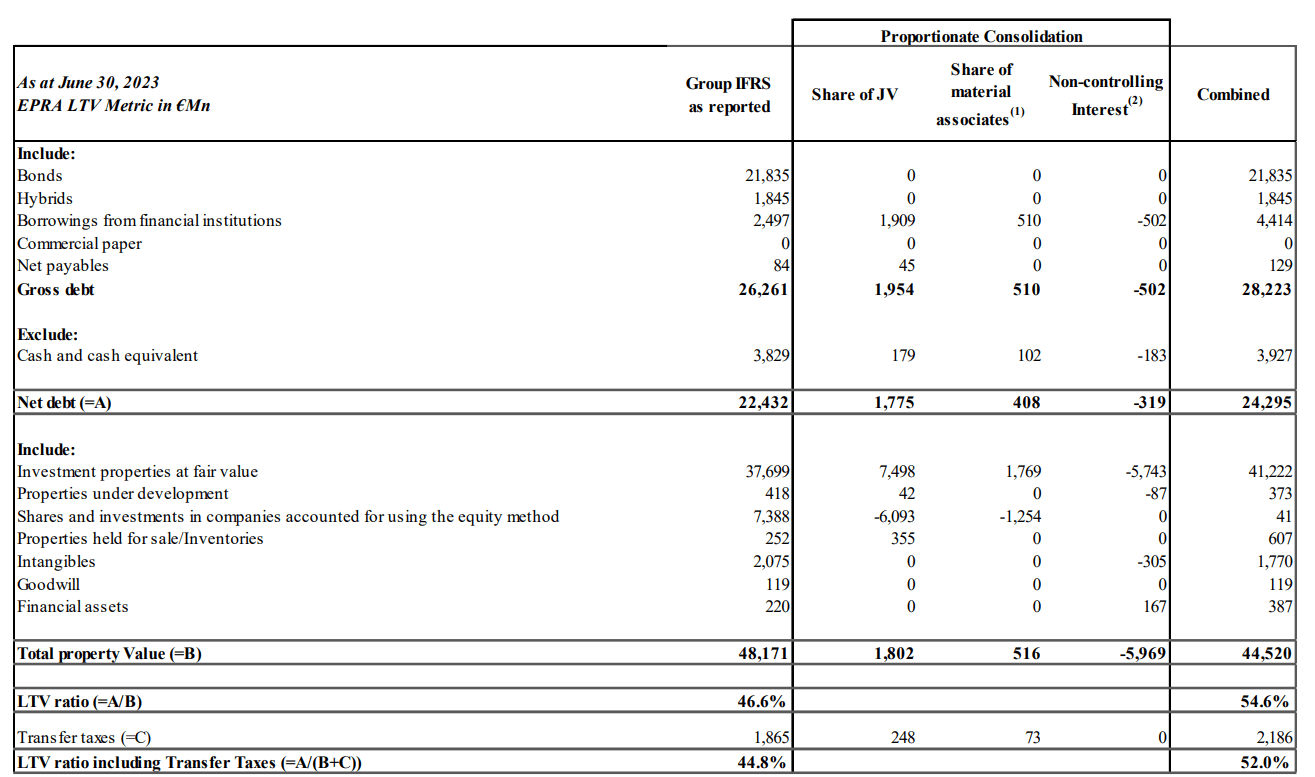

This caused the debt levels to increase. As of the end of June, the LTV ratio was 44.8% on an IFRS basis and about 52% on a combined basis (including the value of transfer taxes). Excluding the transfer tax, the LTV ratio would be 54.6% which is uncomfortably high.

{kind=link}

Which means I totally understand why analysts are starting to question the LTV ratio, I’m just surprised by the timing. This is not a new element and capitalization rates will likely continue to increase.

Assuming a FY 2024 NRI of 2.15B EUR and a 6% capitalization rate, the REIT would lose an additional 5.3B EUR in value which would push the LTV ratio on a combined basis to a very uncomfortable 62%. However, there are two elements that will mitigate the impact of this bearish scenario.

First of all, we have already established the AREPS remains strong and Unibail now expects to reach the upper end of its guidance this year. This means the REIT will generate about 2-2.1B EUR in additional earnings between now and the end of 2024. And that by itself should already be sufficient to reduce the LTV ratio (excluding transfer taxes) to 57%.

Secondly, Unibail continues to sell assets. Not as fast as hoped, but it continues to shed assets. It recently signed an agreement to sell a California-based mall for a very small discount to its book value but more importantly, that asset had an LTV ratio of 98% based on the sales price. The asset was valued at $106M but about $100M in debt will be erased on the other side of the equation. An LTV reduction of 11 bp. Sounds negligible, but every dollar is very helpful at this point.

The San Francisco Centre is in a similar situation. The book value of the stake in that mall is $301M but the proportionate amount of debt is $340M. The debt is non-recourse, so Unibail could just give the keys back to the bank at any time. And just for argument’s sake, if it would do so, that transaction would have an impact of an additional 22 bp to the LTV ratio.

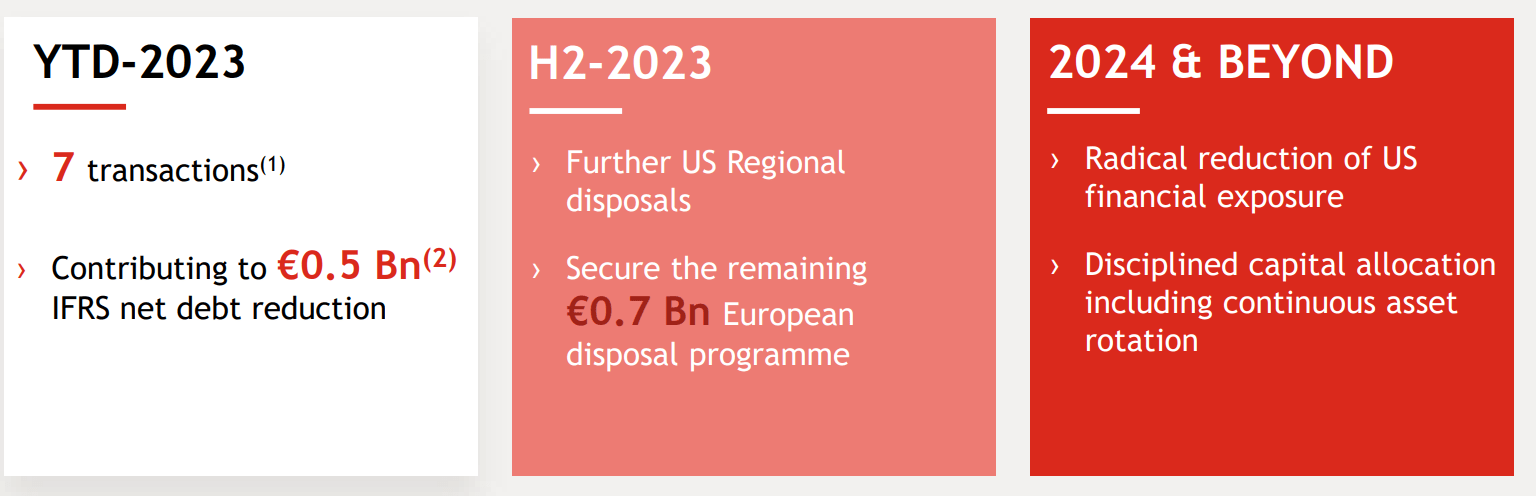

While Unibail initially wanted to complete its exit from the USA in 2023, changing market circumstances now may have deferred this to a more moving target. The Q2 presentation includes a slide which shows the exit from the US markets with an anticipated completion of ‘2024 and beyond’.

{kind=link}

This now likely also means I should not count on a dividend in 2024, although a symbolic dividend would definitely still be possible. While the market may appear to be a bit nervous about the balance sheet situation, let’s not forget an AREPS of 9.5 EUR Per share represents 1.32B EUR based on the current share count of 139M shares and even if a relatively small dividend of 2.50 EUR per share would be proposed, the REIT would still retain about a billion Euros per year to fortify its balance sheet.

Investment thesis

While a meaningful dividend in 2024 based on the FY 2023 results is now uncertain as the balance sheet management remains the REIT’s absolute priority, I am increasingly confident in Unibail’s ability to get through this existential crisis. The REIT understood early on that asset sales are the only real way out of the situation it created for itself, and I will continue to applaud any asset sales at small single digit discounts to their respective book values.

So I will just continue the strategy I have been deploying since January : I write out of the money put options to take advantage of the relatively high option premiums while I slowly build a position. I realize most investors won’t be very interested in a REIT without any dividend, but I have a long-term view on Unibail, and that's why I still assigned a 'buy' rating to the stock. The sale of the US assets will immediately repair the balance sheet (and mitigate the impact of higher interest expenses) while the remaining European assets should be sufficient to retain an attractive investment profile with an AREPS of 5-6 EUR per share.

I don’t expect it to be more than that, as the complete sale of the US assets would reduce the Net Rental Income by 25% while only reducing the net debt by about 20%. Meanwhile, the increasing cost of debt on the remaining debt will also weigh on the performance from the ‘residual’ assets.

For further details see:

Unibail: I'm No Longer Expecting A Meaningful Dividend In 2024