UNBLF - Unibail: Resumption Of Dividend May Be A Positive Catalyst For A Re-Rating Of The Stock

2023-11-28 15:51:03 ET

Summary

- Unibail-Rodamco-Westfield is close to completing its asset disposal program, allowing it to shift focus to providing attractive capital returns.

- The company's operating performance has been recovering, with improved net rental income and tenant sales.

- Unibail's liquidity is strong, and it may resume dividend payments in the near future, making it an undervalued play in the real estate sector.

Unibail-Rodamco-Westfield ( NBLF ) continues to maintain an improving operating momentum and is now almost complete in its asset disposal program, putting it in a good position to change its strategy from balance sheet management to providing attractive capital returns again.

As I covered in a previous article , Unibail's operating performance has been recovering over the past few quarters following a more negative period due to the pandemic, but its valuation was still quite low, making Unibail an interesting value play.

Article performance (Seeking Alpha)

As shown in the previous graph, Unibail's share price has recovered somewhat in recent months and has outperformed the market since my previous analysis. In this article, I update Unibail's most recent financial performance and investment case, to see if it remains an interesting value play within the European real estate sector or not.

Earnings Analysis

Unibail is one of the largest European real estate companies measured by total assets, being the leading company focused on shopping centres. Its business is spread across Continental Europe, the U.K., and the U.S., and at the end of last June, its property portfolio was valued at about €51 billion, a decline of 2.3% compared to the end of 2022. Investors should note that Unibail, like some other French companies, only reports earnings twice per year, thus the most updated financial figures are related to June.

This portfolio devaluation is the result of asset disposals and lower property valuations due to higher interest rates. During the first half of the year , Unibail continued to execute its asset disposal program to protect its balance sheet and investment grade credit rating, having reached €3.3 billion of accumulated sale proceeds since 2021.

Given that its goal is to perform asset disposals of some €4 billion, this means Unibail is now close to completing its asset disposal program and may in the near future switch its business focus from deleveraging to returning capital to shareholders once again.

These most recent disposals have enabled Unibail to reduce its net debt by some €500 million in H1 2023, plus it already announced further deals since the end of the first semester, expecting to reach its remaining €700 million of asset disposals by the end of this year.

This is key for the company to maintain debt at acceptable levels, which has been one of the company's main concerns over the past couple of years.

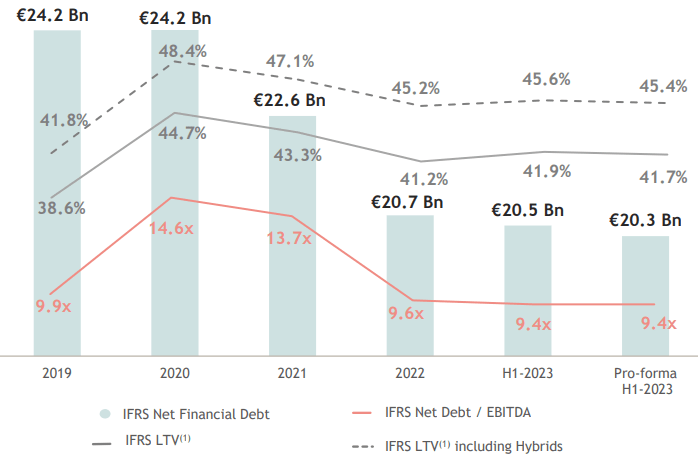

Its net debt at the end of June was €20.3 billion, representing a loan-to-value (LTV) ratio, a key measure of leverage in the European real estate sector, of 45.4%. Note that this ratio includes hybrid debt to be more conservative, while without hybrid debt its LTV ratio was 41.7%. As shown in the next graph, Unibail's net debt has been reduced by close to €4 billion since 2020, which was a decisive factor for the company to be able to maintain sound credit ratios during this difficult period.

{kind=link}

While its operational performance in 2020 and 2021 was quite affected by the pandemic and subsequent lockdowns, which had a negative impact on physical retail sales, its business has been on a recovery trend since mid-2021.

However, the recovery was stronger in Continental Europe in 2022, while the U.S. and U.K. lagged somewhat due to a higher penetration of e-commerce sales and some structural headwinds for shopping centres in these geographies.

Nevertheless, showing that Unibail's strategy to focus on large shopping centres that are well located, its operating performance has improved during the first half of 2023, which is quite encouraging for a sustained recovery ahead.

Its shopping centre net rental income was up by 8.5% YoY, on a like-for-like basis, of which some 4.5% came from the inflation indexation impact. This means that Unibail has been able to pass a large part of inflation on to its tenants, showing that it has pricing power over customers, which is quite good for its business fundamentals over the long term.

This is also positive because tenant sales have been recovering, up by 9% YoY, due to higher footfall (+7% YoY) and strong consumer purchasing power, despite inflationary pressures and the cost of living crisis. This backdrop has also been supportive of relatively high collection rates, which was 96% in H1 2023, a slight drop from 98% during the same period of 2022.

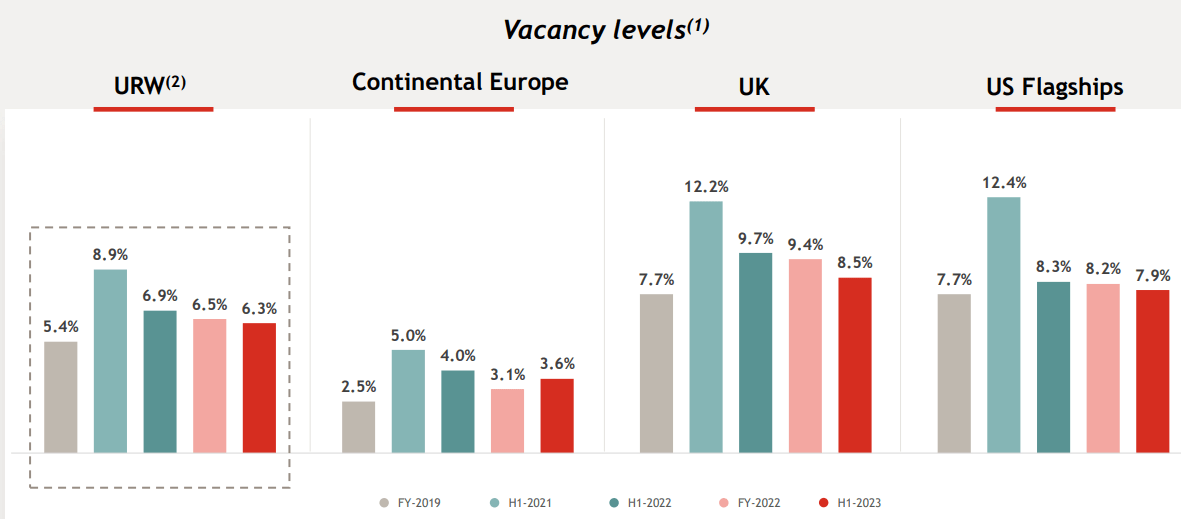

On the other hand, the end of Covid-related support measures in Europe led to higher store bankruptcies, leading to a higher vacancy rate in Continental Europe. As shown in the next graph, Unibail's overall vacancy rate was 6.3% at the end of June, supported by lower vacancy in the U.K. and the U.S., while Continental Europe struggled due to store closures increasing to 'normalized' levels following a record low in 2022, due to Covid-relief programs.

{kind=link}

In addition to lower vacancy across its portfolio, its rental income is expected to maintain a solid growth path in the near term, as the company reported a record semester regarding new leasings. These new deals were signed with Minimum Guaranteed Rent ((MGR)) amounting to €219 million of additional rent, an increase of 12.5% YoY, boding well for rental growth in the second semester of the year.

Regarding other segments, namely office and exhibition, it also reported positive trends with higher net rental income, leading to an overall net rental income of €1.15 billion in H1 2023, up by 8.2% YoY, on a like-for-like basis. Its net result in the period was €757 million, up by 5.7% YoY, and its adjusted recurring EPS was €5.28, up by 6.6% YoY. Its net asset value per share was €150.7 at the end of June, a decline of 3.2% compared to the end of 2022, due to lower property valuations and asset disposals.

Related to Q3 2023 , Unibail only provided a trading update, reporting like-for-like rental income growth of 11.5% YoY in 9M 2023, and positive trends regarding new leases and MGR uplifts (+8.4% YoY). Its vacancy rate was 6.1%, stable compared to June, and performed further disposals having now reached some 90% of its €4 billion asset disposal program. Its guidance for adjusted recurring EPS was updated to at least €9.50 for the full year (vs. a range of €9.30-€9.50 previously), which represents a small increase compared to the previous year.

Regarding its liquidity, it had more than €5 billion of cash at the end of last September, plus some €8.1 billion of undrawn credit facilities, which covers some three years of upcoming debt and loan maturities.

This means that Unibail is not expected to have any liquidity issues in the short to medium term, and may potentially decide to resume its dividend payment in the coming months, given that its asset disposal program is almost complete and Unibail can now shift its business focus from balance sheet management to capital returns. The street seems to agree with this view given that, according to analysts' estimates , Unibail is expected to distribute a dividend per share of about €3, related to 2023 earnings.

This would represent a dividend payout ratio of about 32%, which is quite conservative, thus Unibail can easily resume its dividend payments in the short term and deliver a growing dividend in the coming years, supported both by a higher payout ratio and earnings growth.

Conclusion

Unibail's operating recovery continues to progress quite well, and its efforts to sell assets and protect its balance sheet are almost complete. This means Unibail is now in a good position to resume its dividend payment, which has been suspended since 2020, being potentially an important catalyst for a higher share price in the coming months.

At its current share price, Unibail trades at a forward dividend yield of some 5.5% despite its relatively low dividend expected, showing that its shares are undervalued right now. Indeed, based on 2023 expected EPS, Unibail is trading at a P/E of less than 6x, which is quite low and makes Unibail a compelling value play within the European real estate sector.

For further details see:

Unibail: Resumption Of Dividend May Be A Positive Catalyst For A Re-Rating Of The Stock