UNBLF - Unibail-Rodamco-Westfield: A 10% Dividend Yield In 2024 Is Likely

Summary

- Unibail is making progress with its asset disposals. Assets are sold at smaller than expected discounts (and in some cases even a premium).

- Despite a higher average interest rate, I expect Unibail to report earnings north of 6 EUR per share in 2024.

- Perhaps even higher as Unibail will still be able to take advantage of a fully-hedged debt book and the higher interest rates come into play after 2026-2027.

- By this time next year, I anticipate Unibail to be a 10% dividend payer while its balance sheet will have a LTV ratio of less than 30%.

Introduction

Unibail-Rodamco-Westfield ( OTCPK:UNBLF ) ( OTC:URMCY ) is one of the largest commercial real estate REITs in the world. While the REIT seemed to have bitten off more than it could chew with the pre-COVID acquisition of Westfield, an Australia-based commercial real estate REIT, it spent the past few years on getting itself sorted out. The management took the courageous but wise decision to cancel the dividend for a few years. This enables Unibail to retain hundreds of millions in cash to protect its balance sheet while it is also selling assets. It looks like the market has given up on Unibail due to the lack of a dividend, but I think the REIT could be in a stronger position than ever before by the end of this year.

{kind=link}

Unibail has its primary listing on Euronext Amsterdam where it's trading with URW as its ticker symbol . The average daily volume in Amsterdam is just under 700,000 shares, representing a monetary value of 35M EUR (and close to $40M). As Amsterdam offers the best liquidity to trade in Unibail’s shares, I would strongly recommend to use that exchange to trade in the company’s securities. I will use the Euro as base currency throughout this article.

Selling the US portfolio is slower than I had expected – but the prices are better

When I discussed Unibail in 2022, the REIT had just organized a capital markets date with an encouraging update and outlook for 2024. The REIT mentioned it planned to entirely exit the US market and focus on quality.

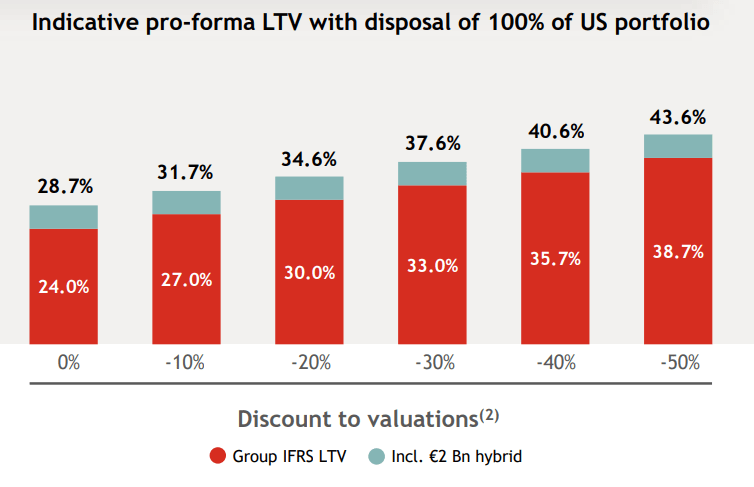

One of the most important slides presented during the capital markets day was this sensitivity analysis. Unibail provided investors with how the sale of the US portfolio would impact the LTV ratios of the REIT on post-deal basis. I was perhaps a bit surprised the REIT even provided the outcome of a scenario where the US assets would be sold at a 50% discount (!) to their respective book values but even in this scenario the LTV ratio would stay below 39% and even if one would include the hybrid bond (deeply subordinated debt which is actually added to the equity portion of the balance sheet due to its status), the LTV ratio would be a very manageable 43.6%.

{kind=link}

This actually was one of the main reasons why I started keeping close tabs on Unibail again. While the scenario of selling the US assets at a 50% discount sounded ridiculous, I would have been perfectly fine with the "minus 30% scenario" as in that scenario the LTV ratio would also be a very manageable 33%. So whatever happens to the US portfolio, Unibail will emerge as a stronger REIT. Sure there will be earnings implications but for a REIT whose existence was threatened during the COVID pandemic, strengthening the balance sheet is priority number one.

Subsequent to the capital markets day, Unibail announced the sale of two European assets. I admittedly scratched my head as I was expecting the US asset sales to be prioritized, but this doesn’t mean this was a bad move by Unibail. The 116M EUR sale of a German property was completed at a premium to book value while the sale of a Dutch mall was completed at book value. These two transactions already helped to rapidly reduce the gross debt and net debt on the balance sheet. And at the end of the third quarter, Unibail sold a French mall which allowed it to reach a total disposal value of 3.2B EUR of the 4B EUR it was eyeing to sell. The average sales price of those assets was a premium of approximately 5% to the book value.

I thought that was great, but the market didn’t care and in the weeks subsequent to the completion of the sale of the French mall, Unibail’s shares traded at a level we hadn’t seen since Q4 2020.

I did understand the impatience of the market, as everyone was waiting for the sale of the US portfolio but investors had to wait for about five months after the capital markets day before seeing the first substantial US asset sale. The Westfield Santa Ana asset was sold for $537.5M which represented a discount of less than 11% on the book value.

A second noteworthy sale in the USA was completed right before the end of the financial year as Unibail sold the San Fernando Valley asset for $325M, again at a discount of less than 11% to the book value .

While selling assets at a discount to their book value never is a good thing to do, the in excess of $1B in US asset sales confirm one thing: The discount to the book value is lower than I had anticipated. Even my conservative scenario of conceding a 30% discount to the book value now appears to be too conservative. Which means that Unibail now has a very good chance to reach an LTV ratio of less than 30% upon the completion of the sale of the US assets. That would make the balance sheet one of the best and most robust in the European commercial real estate segment of the market.

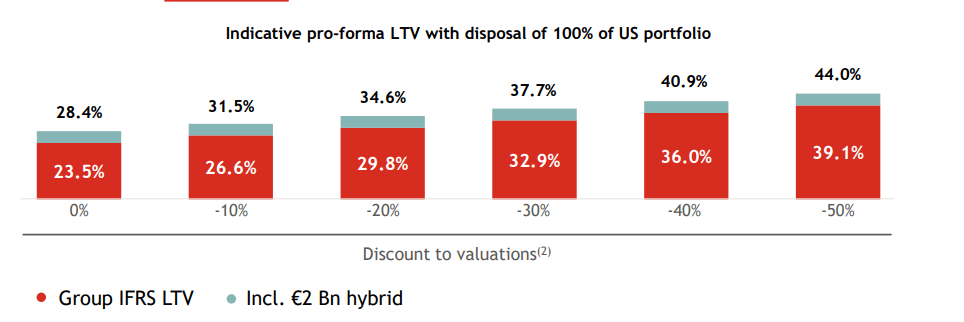

Subsequent to the capital markets day, Unibail did provide a new sensitivity analysis taking the asset sales up until the end of Q3 but excluding the Westfield Santa Ana sale into account.

{kind=link}

So even if the remainder of the US portfolio would be sold at a 20% discount, the LTV ratio would be less than 30%.

The recent asset disposals will help to protect the book value, while the earnings will remain strong

The downside of selling assets is quite obviously that a REIT is no longer able to collect the rent. This means the net rental income and cash flows will suffer. That being said, it will also allow Unibail to repay some of its most expensive debt which means the actual net impact on the FFO should remain limited.

Unibail reports its FFO as AREPS, Annual Recurring EPS. It basically is the net income but excluding the property valuations which can have an impact on the bottom line. Although REPS is not a European standard (that would be EPRA earnings) and although Unibail does not report the US-equivalent FFO, we should consider the REPS to be the FFO-equivalent.

Unfortunately Unibail only provides detailed financial statements every six months, but the Q3 Trading Update did contain some interesting information. The net debt decreased by 800M EUR during the third quarter to 23.3B EUR, and Unibail’s sale of the San Fernando Valley asset in combination with retained earnings, will for sure result in a net debt level of less than 23B EUR as of the end of 2022. Unibail also had 3B EUR in cash on hand and had access to 10B EUR in credit lines so liquidity for sure is not an issue at this time. The REIT estimates that its existing cash and credit lines could take care of all of its financing needs for the next three years (including dividend payments and the repayment of a hybrid bond).

The REIT also hiked its AREPS guidance from 8.90 EUR to 9.10 EUR . This indeed means the REIT is currently trading at just six times its AREPS which by itself is cheap. Too cheap.

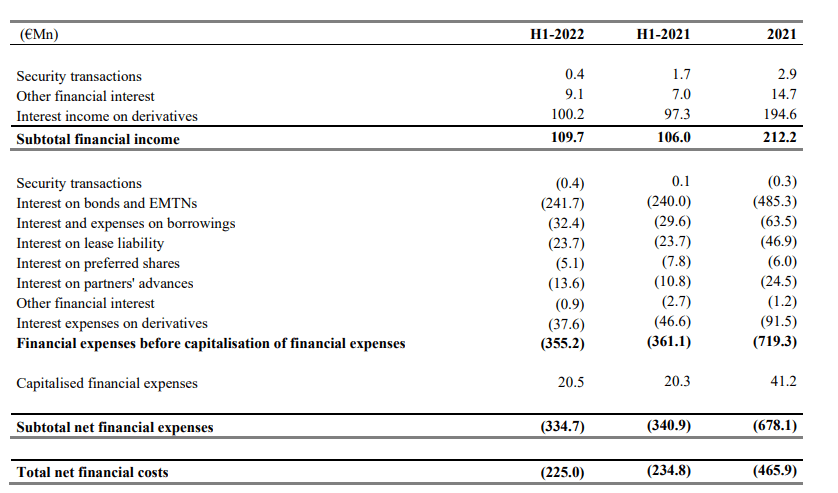

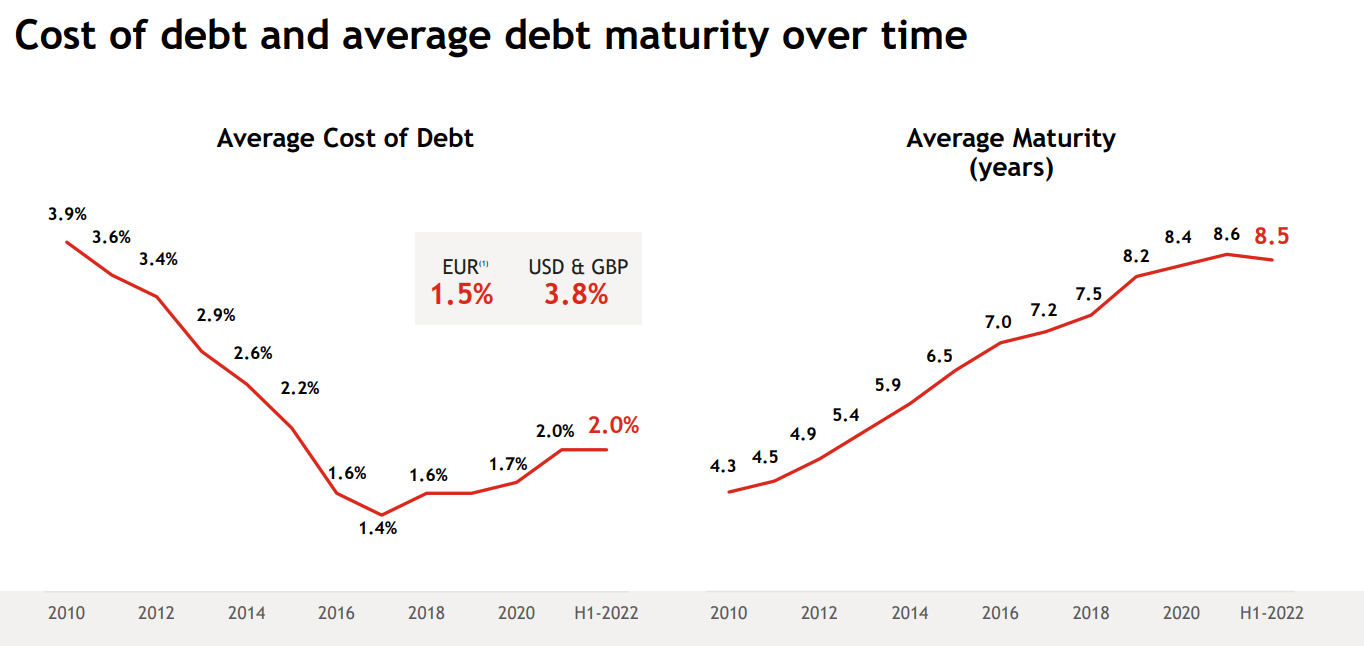

Sure, the AREPS will decrease as Unibail completes its asset disposal program, but Unibail will also be able to rapidly reduce its interest expenses so I expect the net impact to be relatively limited. Unibail paid 225M EUR in net finance expenses in the first half of this year (335M EUR in interest expenses partially offset by roughly 110M EUR in interest income on derivatives).

{kind=link}

The higher interest rates on the market does mean I will have to fine-tune my expectations for 2024. Unibail originally expected to generate a Net Rental Income of 1.57B EUR. I will use 1.65B EUR as updated basis given the current strong performance.

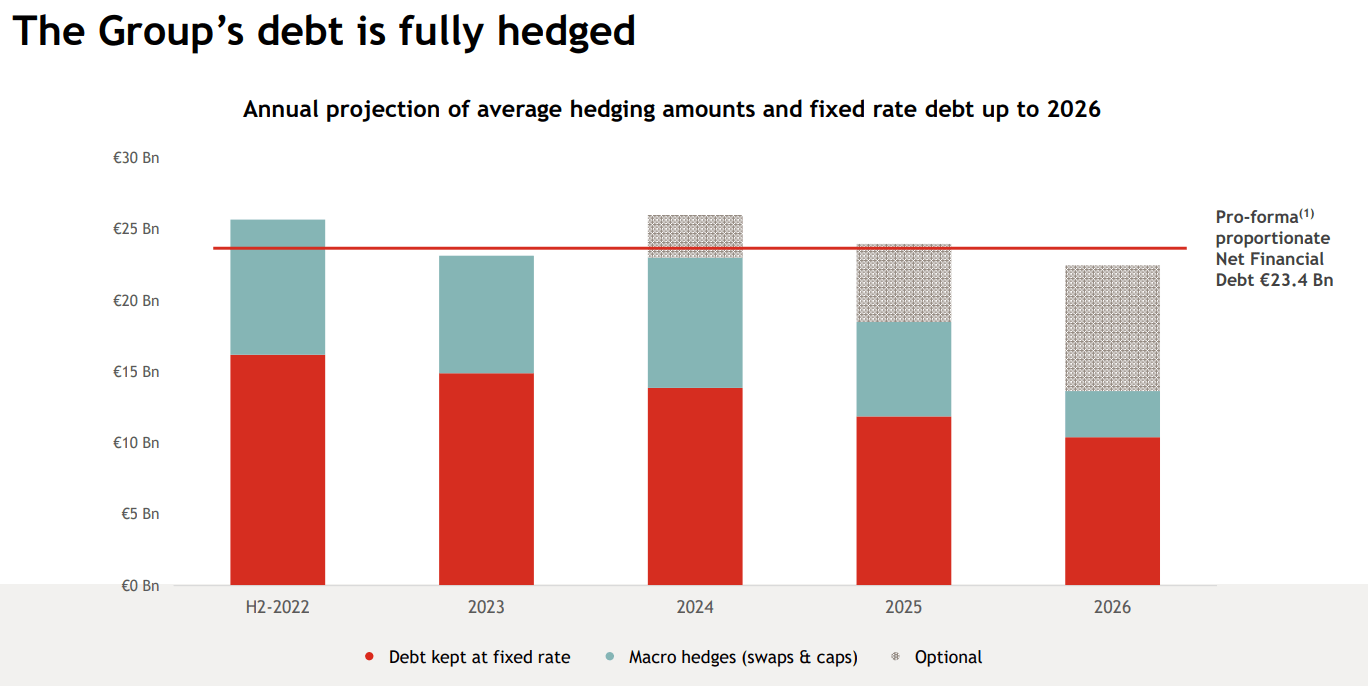

I'm slightly lowering my G&A expenses to 170M EUR (a 20% decrease from FY 2021 with inflation partially offsetting the cost savings related to exiting the US market) but I’m afraid I will have to strongly increase my anticipated interest expenses. Assuming the gross debt will decrease to 12B EUR while the average interest rate increases to 4% (the full effect will only be felt from 2026 on as Unibail has hedged its entire interest rate exposure), the new interest expense will increase to 480M EUR. This would indicate Unibail’s ARE would come in at 1B EUR. We would still have to deduct the 50M EUR in payments on the deeply subordinated debt and about 75M EUR in annual earnings attributable to non-controlling interests.

{kind=link}

This would indicate the shareholders of Unibail can look forward to 875M EUR in Annual Recurring Earnings and divided over 139M shares, the AREPS would be 6.3 EUR per share. Applying a multiple of 12 which really isn’t unreasonable considering the LTV ratio will likely be less than 30% would result in a fair value of 75 EUR per share.

More importantly, applying a payout ratio of 75% would indicate a dividend of 4.8 UR per share. And should Unibail decide to repay it hybrid debt securities, the 75% payout ratio would imply a dividend of 5.1 EUR per share. I think it is increasingly likely Unibail will call the hybrid securities as the interest rate will reset this year and based on the current five-year Euro-midswap, Unibail would have to start paying 4.5-5% on these securities.

{kind=link}

Investment thesis

I initiated a small long position in October and am looking to expand this position during 2023. My preferred way to gain additional exposure is by writing put options with various strike prices and expiry dates. The market is pricing the options as if it doesn’t believe Unibail will execute on its transformation plan. I think the REIT will be able to sell its US assets at a decent price and even if it takes longer than anticipated, so be it. I also wouldn’t mind if the very first distribution after the reinstatement would be a small one if that would allow Unibail to hoard a few hundred million euro of additional cash.

As mentioned, the option premiums to write put options are surprisingly high. You can write a P50 or P45 for March for an option premium of respectively 3.25 EUR and 1.80 EUR. Meanwhile, a P45 for September can be written for 4.65 EUR while a P35 for September would still get you an option premium of in excess of 2 EUR. I personally don’t think the share price will drop to those levels but I think I’d be happy to pick up tock at those levels. And for those who would want to go a little bit more aggressive: the P60 for December of this year has an option premium of 13.00 EUR. Which means that you either pocket the 13 EUR premium if the option isn’t exercised, or you’d establish a position at 60-13 = 47 EUR per share.

The market isn’t giving Unibail enough credit for what it has already done and I think the market is wrong. The immediate and acute balance sheet danger no longer exists and I’m fine with Unibail selling down its US portfolio asset by asset. I expect the REIT to generate north of 6 EUR per share in FFO after completing the asset sales while the dividend yield could easily approach 10%.

For further details see:

Unibail-Rodamco-Westfield: A 10% Dividend Yield In 2024 Is Likely