KLPEF - Unibail-Rodamco-Westfield: I Am Bullish On The REIT That Does Not Pay Dividends

2023-05-15 10:41:25 ET

Summary

- Unibail-Rodamco-Westfield is the only class-A mall owner whose shares never took off in the post-pandemic stock market rally.

- Concerns over strategy and leverage have held the stock back, but new management has worked hard to point the company in the right direction.

- A dividend reinstatement and interest rates pivot could act as catalysts within 12 months. Barring a complete economic disaster ahead, I see an upward re-rating as inevitable.

After publishing its Q1 trading update last month and holding its AGM last week, I have taken a fresh look at Unibail-Rodamco-Westfield ( OTCPK:UNBLF ). The shopping center owner and developer, known by its acronym URW, posted solid results but continues to trade at rock-bottom valuation. The overall economic outlook calls for caution, but markets are forward-looking, and REITs shareholders have already taken quite a hit. With URW trading lower than the March 2020 pandemic levels, I see a lot of negatives priced in its shares and believe the company is arguably the best recovery play in the space.

The company and its woes

Like its closest peers Simon Property Group ( SPG ) in the US and Klepierre ( OTCPK:KLPEF ) in Europe, Unibail-Rodamco-Westfield is a large shopping mall REIT, currently operating 78 properties across 12 countries. While I understand that naming URW's field of operations can be enough for some perspective investors to say "pass," I also think there are two sides to every coin. E-commerce competition, high(er) interest rates, and low CRE transaction volumes are all known problems affecting URW. Still, the negative narrative has already been pushed beyond its logical boundaries, resulting in the over compression of profit and cash flow multiples.

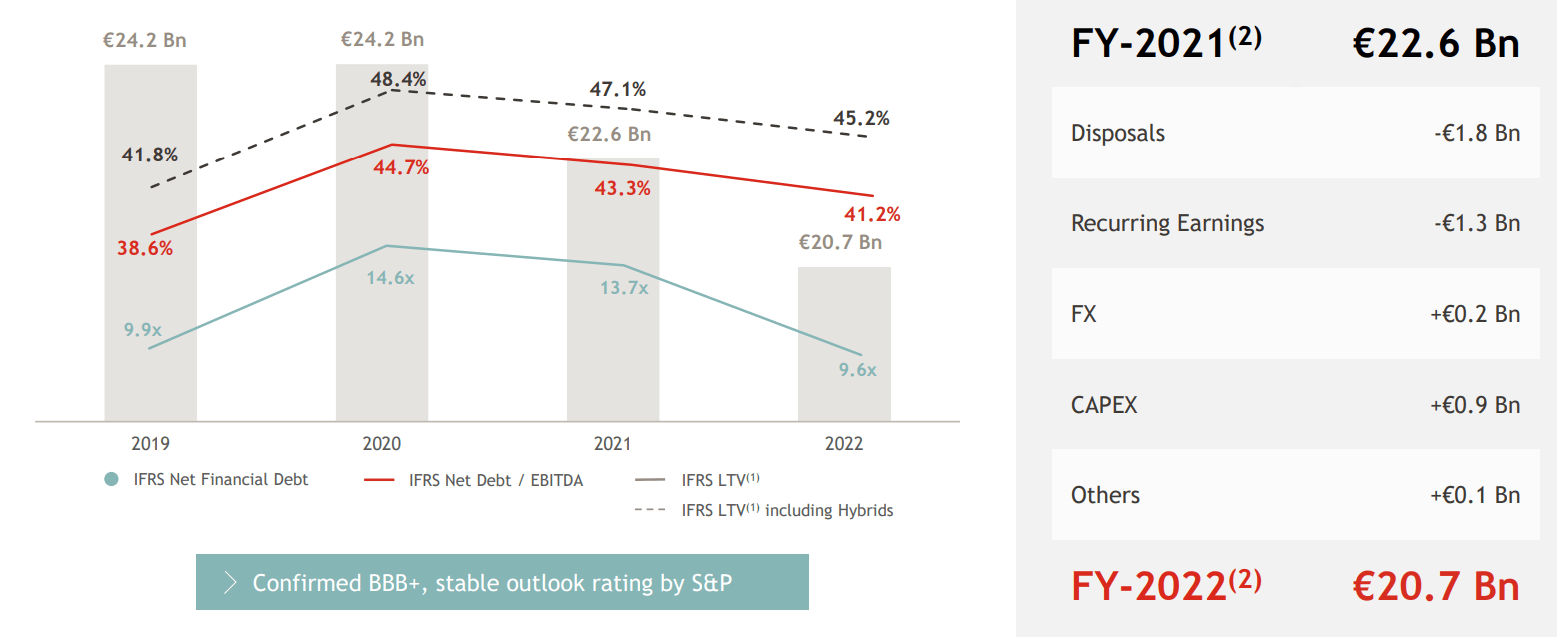

While this is true for all the companies mentioned above, URW's higher leverage has also resulted in some relative undervaluation vs. its closest peers. Despite lower loan-to-value (LTV) coming down from the pandemic highs, the company's financial position is still weaker than SPG or Klepierre. URW's net-debt to EBITDA ratio remains elevated at 9.6x (FY22) vs. Klepierre's 8.1x and SPG's 6.3x. Still, repayments and a +30.2% rebound in EBITDA brought the figure down five turns from the awful 14.6x at the end of FY2020, and the company continues to earn an investment grade rating from both S&P (BBB+) and Moody's (Baa2), stable outlook.

{kind=link}

URW also suffered one more problem that its peers didn't: poor management. Here's what a Morningstar note had to say about the company's past capital allocation:

The decision to take on substantial debt to acquire Westfield in 2018 has in hindsight been very poor for securityholders. While it was nearly impossible to predict COVID-19 or its impact, the Westfield deal resulted in an uncomfortable debt load that would have taken years to pay down even without a recession.

Executives engaged in empire-building are a typical red flag, but in URW's case, the proverbial last straw came with the attempt to go through with a massive capital raise (and dilution) at the heights of the pandemic. Fortunately, investors woke up just in time to oust the CEO and push for a radical change in the company's strategy.

The few strategic pillars that URW's new management has been called to deliver on are: dispose of US properties, use proceeds to deleverage and focus on Europe. Although achieving multiple dispositions of US assets is no easy feat in the current environment, the company is in no rush to complete the capital recycling plan. Looming debt maturities are manageable, and the company has retained all cash flow for three years to pay down debt. A severe recession in H2 2023 could further delay the company plans and share price recovery. Still, unless people stop shopping in physical stores altogether (a farfetched outcome), I see some upward re-rating from here as inevitable.

The Q1 update

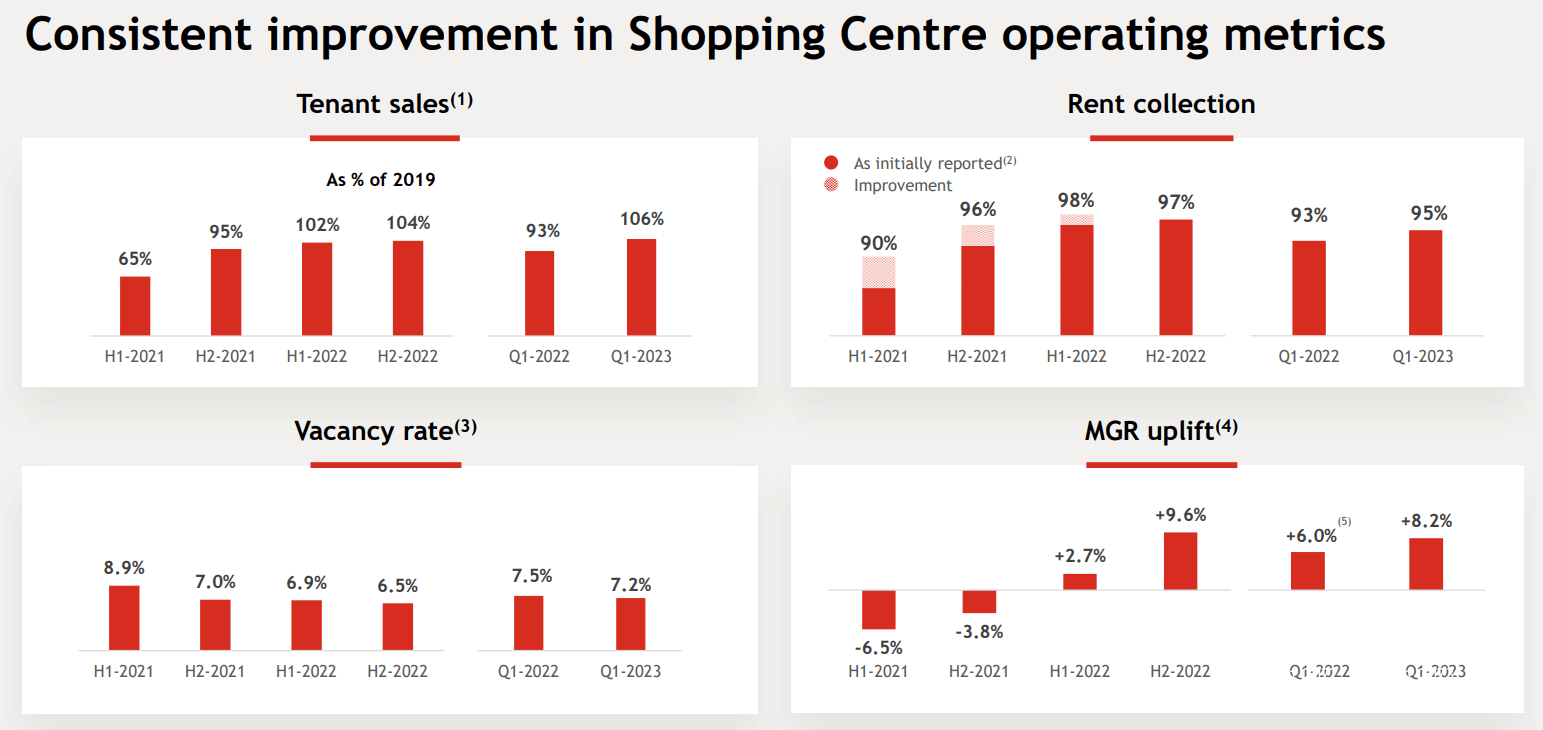

Although the market reaction was muted, the news contained in URW's report was mostly positive. Revenues were up +1.4% vs. the previous year, but considering dispositions, the results were quite impressive. URW's like-for-like growth in the Group's Gross Rental Income ((GRI)) was up +7.8%, and tenant sales were up +12% vs. the year-ago period. While naysayers could disregard the improvements in sales as "inflation driven," the data provided by management also shows a +12% for footfall in Continental Europe and the UK and a +5% for footfall in the US. Paraphrasing Mark Twain, "The news of malls' death has been greatly exaggerated."

Rent uplift in 1Q23 was +8.2% on top of indexed passing rents and accelerating from last year's +6.2%, and vacancies also eased up 30 bps vs. the year-ago period. EPRA occupancy stood at 92.8% in the quarter, and management expects FY23 levels to be above FY22. Vacancy figures were markedly stronger in Continental Europe, with just 3.8% vacant vs. 11.7% in the US.

{kind=link}

Liquidity levels remain strong, with €13.7 billion cash on hand and available credit lines, including €4.2 billion cash.

Finally, management reconfirmed its guidance of 2023 Adjusted Recurring Earnings per Share (AREPS) of €9.30 to €9.50. The low end of the range is flat YoY, but the result includes the potential impact of dispositions. However, the portfolio should continue to perform well, offsetting the shrinking of the asset base.

What about the dividend

URW used to pay up to 90% of its AREPS in good years. However, the dividend came to an abrupt halt with the pandemic. The company needed to retain all available cash flow to deleverage and fund both CAPEX and the remaining new developments internally. From a regulatory perspective, SIIC status (European-equivalent of REIT) can be maintained, and URW has no obligation to proceed with dividends as the company carries statutory cumulated negative retained earnings (currently -€2.3 billion), which are below its carry forward SIIC distribution obligations (€1.7 billion).

That said, URW has guided for a three-year pause in dividend payments from 2021 to 2023 (no dividends related to FY20, FY21, and FY22 results). Like European peers, URW declares annual dividends based on the AGM's approval of the prior year's results. I see little reason to believe management will opt for a continued suspension beyond the original timeline if URW achieves AREPS guidance and net debt to EBITDA falls below the 9x mark at the end of 2023. So, even if it is true that URW does not pay dividends at the moment, perspective investors could be rewarded as dividends are potentially reinstated within 12 months from this writing.

I do not expect URW to return to paying 90% of FY23 AREPS, as the company will need to continue to work down the debt load and self-fund its growth. Still, URW shares trade at depressed levels, and based on the current €45 share price, a 50% AREPS payout ratio would translate into a dividend of approximately €4.7 per share or a 10.5% dividend yield.

Valuation

With e-commerce sales rising, retail REITs have gone through a substantial downward valuation re-rating in recent years. Even if I reject the idea that malls, especially in Europe, are going the way of the dinosaurs, it is important to acknowledge that the competitive landscape has changed and be realistic about these REITs' future. Higher levels of maintenance CAPEX, lower profitability, and low growth are the main reasons prospective investors should consider stepping up their buying only when valuations are well below the 14x - 17x FFO multiple that used to be considered "fair" for companies like URW or Simon Property Group.

Ideally, base-case fair multiples can now theoretically settle in the 10x - 14x range, with potential discount/premium relative to peers, depending on leverage level and asset quality. Morningstar analysts seem to agree with the above statement, and their current fair value assessment comes at 10x fwd FFO for URW, 12.5x fwd FFO for SPG, 15x fwd P/FFO for Macerich ( MAC ). While I see the reasoning for the premium granted to SPG vs. URW (lower leverage), I think Macerich won't re-rate just as much. Despite their high-quality portfolio, the debt level is too high, and their credit rating is below investment grade. I see MAC's medium-term upside somewhat capped to 10x FFO, although arguably, URW could trade at a higher, rather than lower, multiple.

URW and MAC currently trade at 4.8x, 5.2x forward FFO, SPG, and Klepierre at 8.9x forward FFO, suggesting a broad upside in the space but highlighting that URW could be the best risk-adjusted opportunity available today.

{kind=link}

Even after considering that URW can probably re-rate at a lower P/FFO level compared to Klepierre or SPG, the annualized five-year rate of return could be above 25% (*assumes URW will start to pay dividends again next year, and the payment is considered constant throughout the holding period). Even if all these names could be good buys, URW seems the only one deserving a "strong buy" rating.

Investors takeaway

Despite the challenges of a potential upcoming recession, Unibail-Rodamco-Westfield trades at less than 5x forward Earnings and one-third of their EPRA replacement (book) value.

Even if e-commerce likely continues to eat away growth from physical stores, the class-A shopping centers in key locations that URW owns will continue to produce solid earnings over the next economic cycle: the negatives seem priced in already, and the market valuation assigned to this kind of company by the market is just too low.

I expect investments in URW to fare well over the next few years, producing 20% - 30% IRR returns, depending on the severity of the upcoming economic recession, interest rate pivot, and URW's timeline of dividend reinstatement and deleverage momentum.

For further details see:

Unibail-Rodamco-Westfield: I Am Bullish On The REIT That Does Not Pay Dividends