MAC - Unibail-Rodamco-Westfield Is A Bargain Trading At A ~7x P/E Ratio

Summary

- Unibail-Rodamco-Westfield delivered solid results for its fiscal year 2022, marking an almost complete recovery from the impact of Covid.

- Earnings and EBITDA grew considerably compared to 2021, occupancy continues to improve, and leasing remains healthy with positive spreads.

- Shares are extremely undervalued with a p/e ratio of ~7x and trading at roughly 40% of book value.

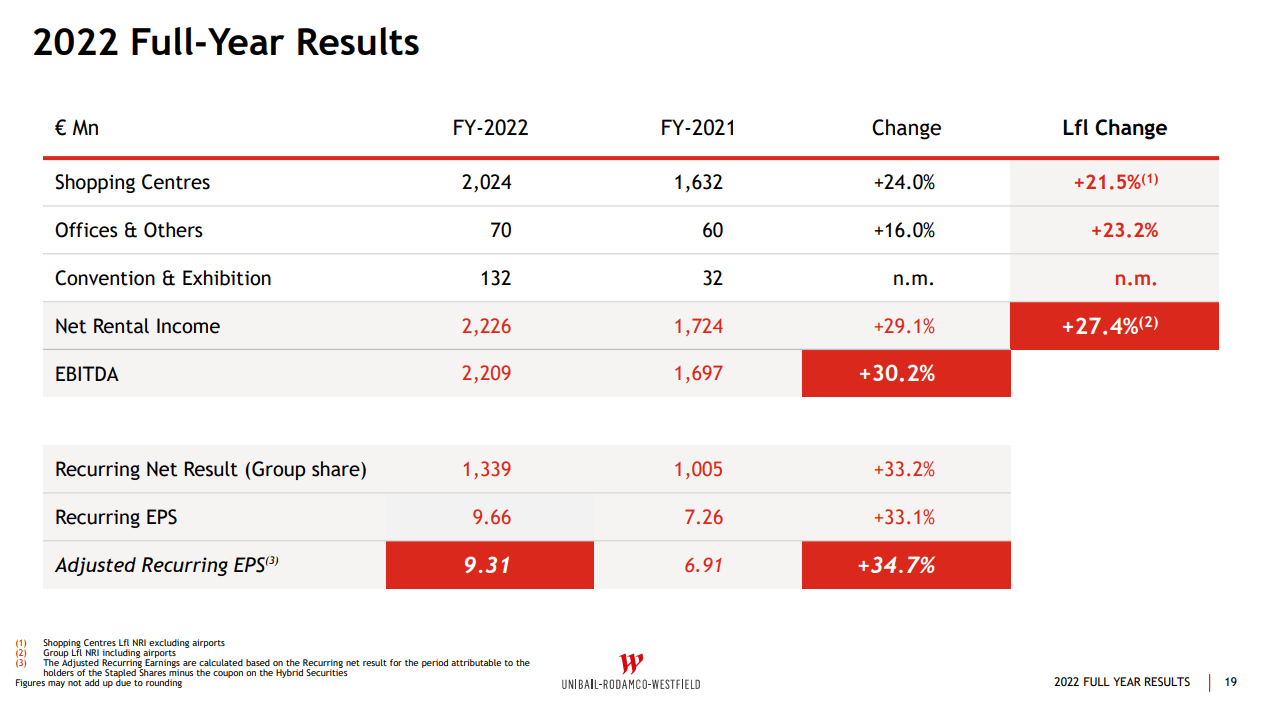

Unibail-Rodamco-Westfield ( UNBLF ) just published their fiscal year 2022 results and it appears the company has almost completely recovered from the Covid impact. Its EBITDA increased ~30.2% to ~€2.2 billion compared to FY 2021, its adjusted recurring earnings per share went up ~34.7% to €9.31, and it managed to bring its net debt to EBITDA leverage ratio to ~9.6x from ~13.7x in FY2021.

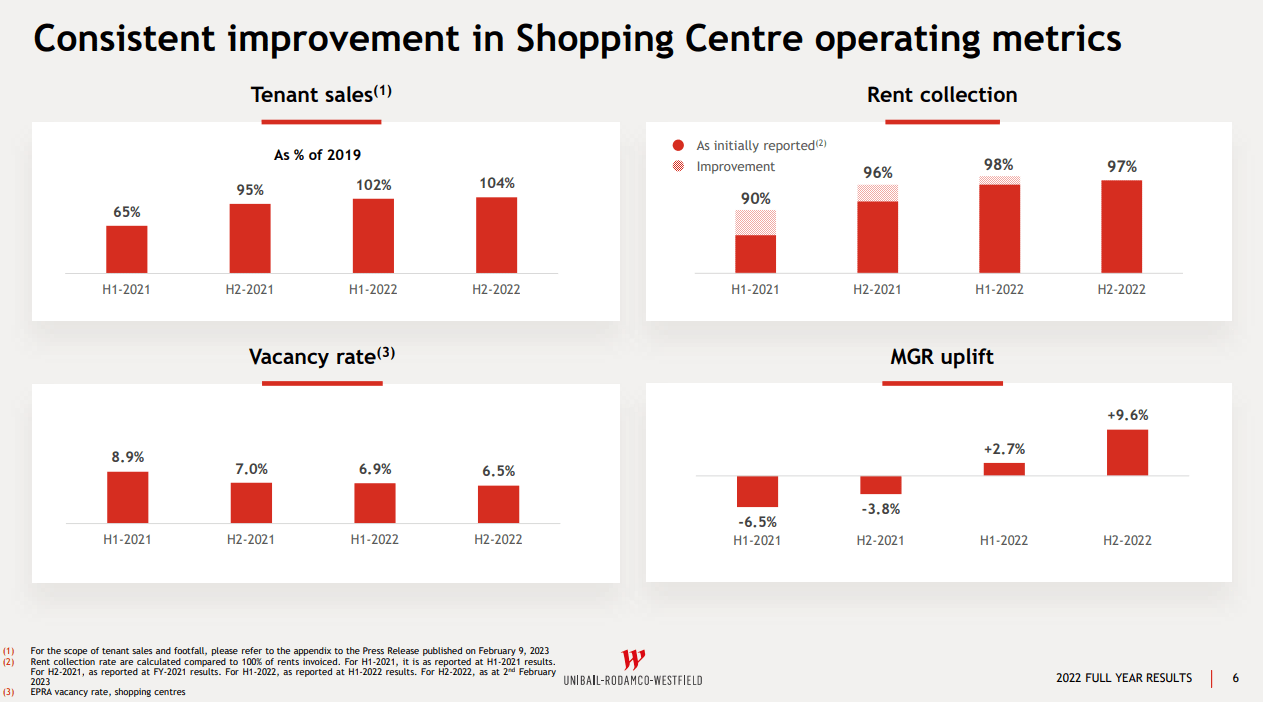

Its tenant sales are above 2019 levels and, importantly, the minimum guaranteed rent uplift is now solidly positive, meaning the company is executing leases with nice rent increases. The vacancy rate remains higher than pre-Covid by ~1.1%, but occupancy is getting very close to being fully restored.

Unibail Rodamco Westfield Investor Presentation

{kind=link}

We believe high quality shopping mall companies like Macerich ( MAC ) and Simon Property Group ( SPG ) remain undervalued, but that their European counterparts like Klépierre ( KLPEF ) and Unibail-Rodamco-Westfield are even cheaper. Based on recent prices of the native Unibail shares, which are trading at ~€61, the price/earnings ratio is only 6.55x. This is despite the fact that the company focuses mainly on very high quality Class A shopping malls, and that its balance sheet is in much better shape now after two years of deleveraging. The company is guiding to a small increase in earnings for 2023 at the mid-point, with adjusted recurring earnings per share expected to be in the range of €9.30 to €9.50. In other words, not only is the p/e multiple extremely low, but earnings are expected to increase slightly this year. As the company continues to improve occupancy, and to sign leases with higher leasing spreads, we believe it can continue to post earnings growth going forward.

Financials

Adjusted recurring earnings per share amounted to €9.31, up +34.7% compared to 2021, mainly driven by strong shopping center operational performance (including the end of Covid rent relief, lower doubtful debtors, and higher variable income), the recovery of the Convention & Exhibition division, and the delivery of projects, partly offset by disposals, increases in financial expenses and taxes. These results are getting very close to pre-Covid levels, reflecting the enormous progress in the recovery the company has made.

Unibail Rodamco Westfield Investor Presentation

{kind=link}

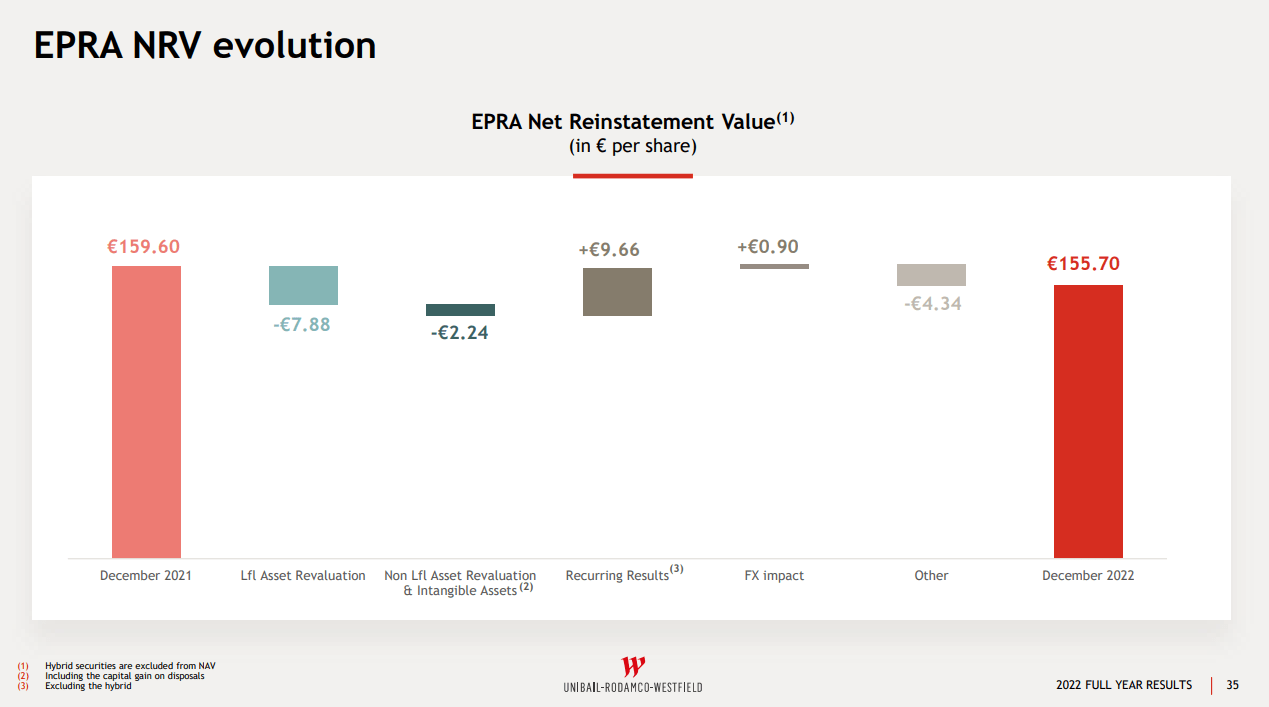

The EPRA Net Reinstatement Value per share, a version of book value per share, ended the year at €155.70, down -€3.90 (-2.4%) compared to the end of 2021, mainly driven by the revaluation of investment properties, partly offset by the retained recurring results. The rise in interest rates is having a negative impact on the valuation of its properties. This means that shares are currently trading at ~40% of book value, an enormous discount.

Unibail Rodamco Westfield Investor Presentation

{kind=link}

Leasing Spreads

We like the company's leasing strategy, where they are being more aggressive on rent increases for long-term deals, while being more flexible with short-term leases aimed at just improving occupancy quickly. The company reported that the percentage of long-term leases, those with a duration of 36 months or longer, increased to ~68% of leases in 2022. This is a good sign that occupancy gains will be more permanent. These leases are also the ones reporting a higher minimum guaranteed rent uplift, while the company is giving better deals to tenants on short duration leases. In any case, it is very reassuring that in 2022 leasing spreads were on average positive, which was not the case in 2021. As the company shifts its focus from improving occupancy to negotiating better leases, we believe there is potential for leasing spreads to improve even more in the future.

Unibail Rodamco Westfield Investor Presentation

Balance Sheet

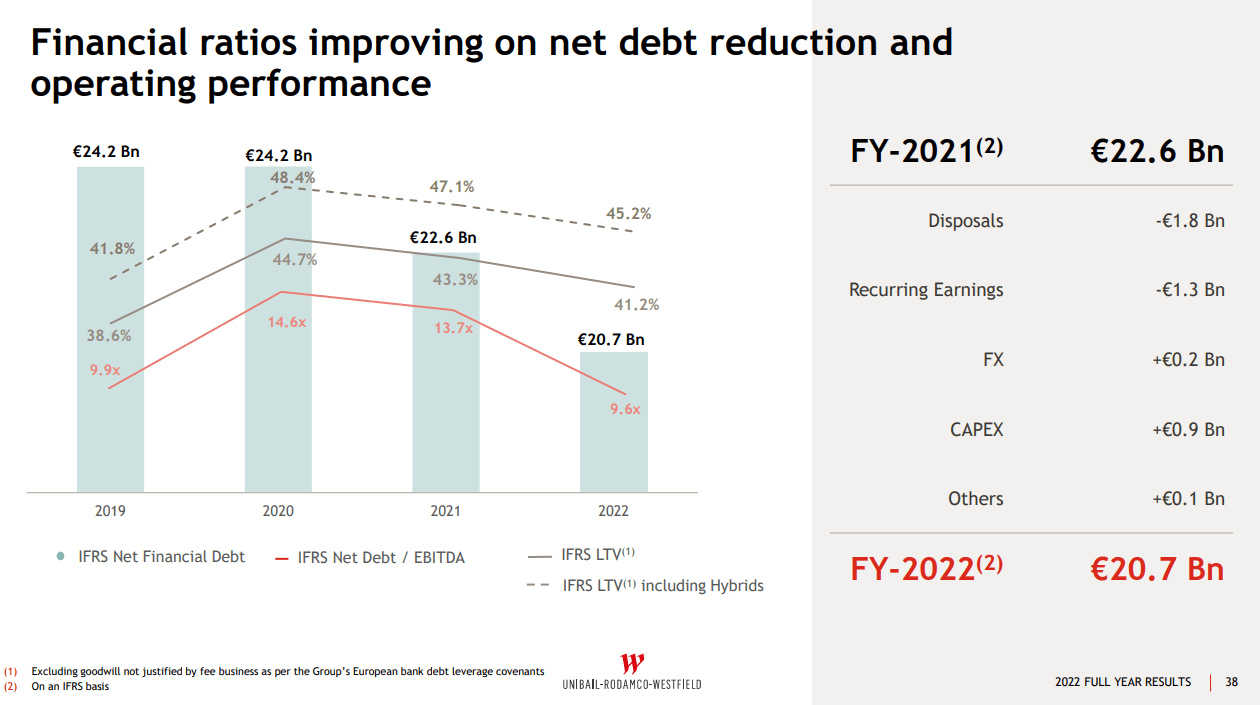

The combination of stopping the dividend to retain earnings, strategic asset disposals, and improved operating results has significantly improved the company's credit ratings. Its net debt/EBITDA is now below 2019 levels, and loan to value is getting closer to the company's target of ~40%. The company has a healthy debt maturity schedule with 8.3 years average debt maturity, it has €3.5 billion cash on hand and €9.7 billion in undrawn credit facilities. Liquidity is therefore not an issue, and the company is well positioned to deal with maturing debt for the next few years.

Unibail Rodamco Westfield Investor Presentation

{kind=link}

Valuation

We understand that malls are not the most popular investment sector, but the company has demonstrated resiliency, and the valuation is extremely low. We believe a potential catalyst for the valuation to re-rate higher is once the company restarts the dividend. That could potentially happen next year. As can be seen in the graph below, shares are trading at a fraction of their book value, and based on adjusted recurring earnings per share, the p/e multiple is only ~7x. As the company continues improving its balance sheet, occupancy levels, and potentially restarts the dividend, we believe there is ample room for the valuation to re-rate higher.

Risks

Unibail-Rodamco-Westfield is finally getting close to pre-Covid operating levels, showing just how big an impact the Covid crisis had on the company. Should another adverse event occur, such as a deep recession, this could put the recovery in jeopardy and could potentially even reverse some of the gains the company has made in the last couple of years. E-commerce also remains a headwind, although class A mall have proven more resilient compared to lower quality shopping centers.

Conclusion

The business is almost back to 2019 levels, with retailers expanding and the company delivering solid leasing performance even in a challenging environment. The balance sheet is much healthier, and credit ratios have markedly improved. The valuation, however, remains extremely low, with shares trading with a p/e of only ~7x. We believe further operational improvements, and the potential return of the dividend next year, can serve as catalysts to re-rate the valuation of the shares higher. Overall we were pleased with the progress the company reported for 2022, and as such we are maintaining our 'Strong Buy' rating.

For further details see:

Unibail-Rodamco-Westfield Is A Bargain Trading At A ~7x P/E Ratio