UNCRY - UniCredit: High Returns Despite Windfall Tax Woes

2023-09-19 08:21:19 ET

Summary

- UniCredit reported strong Q2 results, with revenue and net profit beating expectations and an improvement in the capital position.

- The impact of the Italian windfall tax is expected to have minimal downside on earnings and capital requirements.

- UniCredit remains undervalued and offers significant capital returns: 1/3rd of the market cap will be distributed to shareholders in 2023-4.

We have previously presented a note on UniCredit (UNCRY) with a Buy rating, highlighting attractive valuation multiples, discount to sector P/TBV and PE ratios, as well as hefty shareholders distributions: at the time of the note a quarter of the market capitalization was to be distributed over the current and next fiscal year. In August the Italian government came forward with a windfall tax which we believe does not materially affect the investment case. In this note, we will analyze the impact of the tax, review Q2 results, as well as update our forecast and valuation. We highly recommend readers to check our previous note on UniCredit.

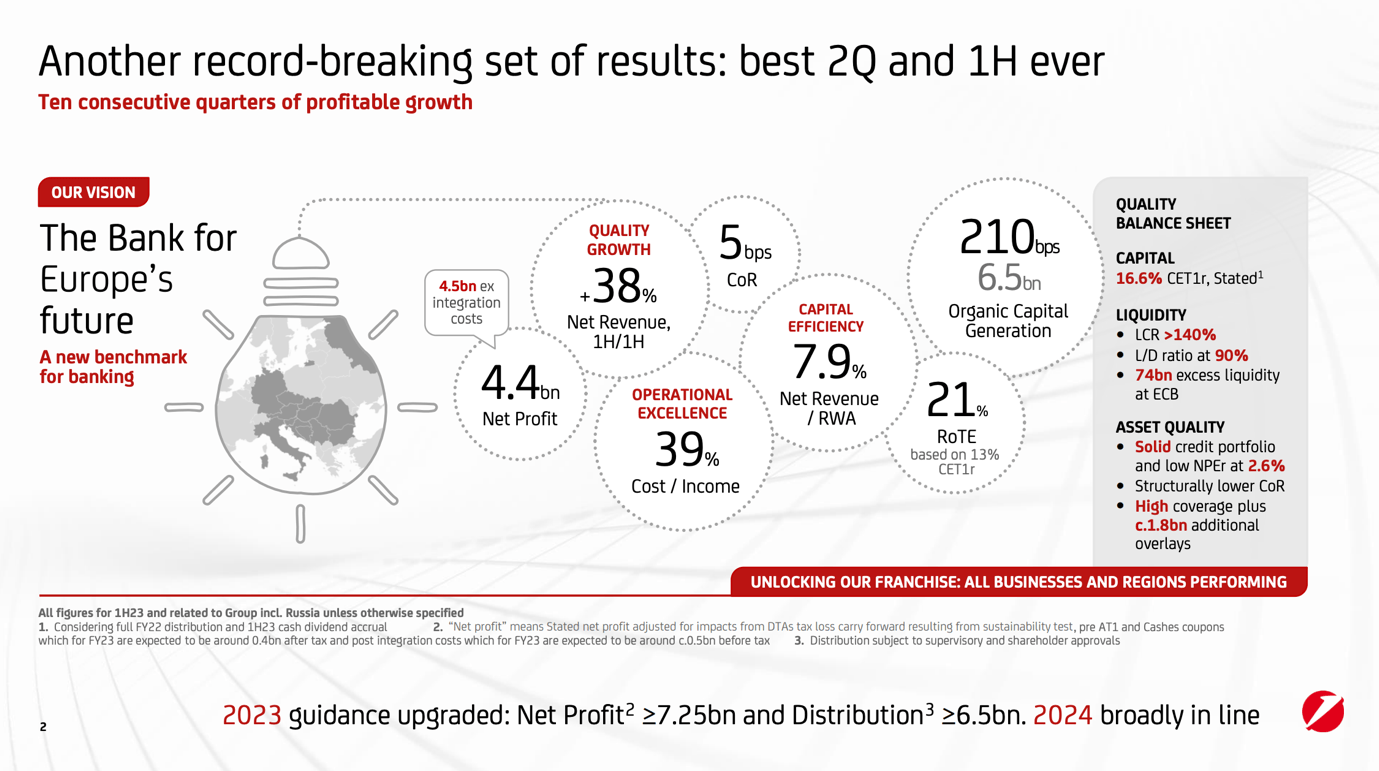

A strong set of Q2 results

UniCredit reported a strong set of Q2 results with revenue and net profit beating sell-side consensus expectations. The revenue beat was driven by higher Net Interest Income, with the outperformance coming from Italy, Germany, and Central Europe. NII Guidance was upgraded by €600 million to more than €13.2 billion, going further than consensus expectations for the full year. Deposit beta remains satisfactory at 24% for H1, with Q2 at a slight increase vs Q1. In addition, cost management was strong as costs came 2% below consensus, further driving the net profit beat. Asset quality remains encouraging with Loan Loss Provisions coming in significantly below consensus at €21 million, or around €300 million lower than expected. Given the trend Cost of Risk guidance has been lowered to <25 basis points with potential for upside (i.e., lower CoR) vs. the previous guidance of 30-35 bps.

Net profit came in around €450 million above consensus at €2.3 billion, and there was an improvement in the capital position of the bank with organic capital formation of 101 bps and a CET1 ratio of 16.6% or 30 basis points above consensus. Moreover, net profit and capital returns guidance was upgraded with FY2023 net profit standing at €7.25 billion i.e., 12% higher than the previous guidance, and FY2023 total shareholder distributions (buybacks + dividends) standing at €6.5 billion vs. the previous €5.75 billion, or 17% of UniCredit’s current market capitalization. UniCredit expects the same strong trends to persist in the next fiscal year.

{kind=link}

Impact of Italian windfall tax

In early August, the Italian government unexpectedly announced the implementation of a windfall tax for Italian banks. “Extra profits” will be taxed to fund tax cuts and support mortgages for first-time buyers, collectively bringing in more than €2 billion. Initially, the share price reaction was significantly negative given the surprising nature of this announcement. The government later clarified that the tax would be limited to 0.1% of firms’ assets. Although the scope is not clear, we believe this creates at most mid-single digit downside to our FY2024 earnings estimates and does not significantly affect capital requirement, shareholder distributions, etc. to change our long thesis. However, we are discouraged by the abrupt decision, especially coming from a government with a pro-business / low-tax agenda.

Investment case and valuation

In our previous note, we highlighted UniCredit’s robust capital position, increasing profit and shareholder returns, and attractive portfolio exposures. We are encouraged by the latest results confirming our view and remain constructive on UniCredit given the persistent discount vs. European banking peers (UniCredit trades at lower P/E and P/TBV) despite solid fundamentals and continued outperformance. However, we have made some adjustments to our estimates to reflect the pressure from the Italian windfall tax.

We reiterate our expectation of total revenue of €22.0 billion and lower our net profit estimate to €6.7 billion in 2024, lowered to reflect the impact of the newly introduced windfall tax in Italy.

We update our forecasts on shareholder remunerations, a key element for our long thesis. €6.5 billion will be distributed in 2023, with €1 billion of share buybacks remaining to be executed by year-end; and at least an additional €5.75 billion at least will be distributed in 2024. Roughly 32% of the current market capitalization will be distributed to shareholders over the next two fiscal years – an industry leading ratio.

We value UniCredit using a blended P/TBV and P/E multiples analysis. We value UniCredit at 8x forward earnings, and we obtain an equity value of €54 billion for the group, or a share price of €30 or $32, implying a 38% upside. The current multiple corresponds to a trough valuation and is at a discount to historical values as well as to the wider peer group.

From a P/TBV perspective, the current P/TBV multiple implies a cost of equity higher than 18% which we view as excessively large. We forecast a tangible book value of €34.4 and 11.7% ROTBV in FY24, implying 0.63x forward P/TBV which we believe should eventually rerate to more than 0.8x P/TBV’24e, implying at least a 25% upside, or a share price of €27.5.

Risks

With the risk of windfall / excess profit tax already materialized, downside risks include but are not limited to weaker macroeconomic conditions, interest rate declines leading to lower NIM, higher cost of funding leading to lower NIM, additional pressure from Russian operations, unexpected changes in regulation e.g., increasing capital requirements, a decline in asset quality and a deterioration of the capital position, higher competition from traditional banks as well as fintech firms and neobanks, and lower-than-expected capital returns.

Conclusion

We believe UniCredit remains significantly undervalued and offers a high teens-low twenties IRR at the current share price, as one third of the market cap is distributed over 2023-4 and there is additional scope for the stock to rerate. We are encouraged by the latest results, see little reason to worry over the impact of the Italian windfall tax, and remain optimistic about the following quarters.

For further details see:

UniCredit: High Returns Despite Windfall Tax Woes