UFI - Unifi: Changing Trade Trends Could Push Prices Up

2023-06-26 06:15:37 ET

Summary

- Unifi shares have fallen 14% YTD, but there are signs of demand recovery and profitability improvement in Q3 2023.

- Factors such as normalization of inflation, revenue growth in the US and Asian segments, and cost control measures could boost the company's share price.

- UFI stock is currently undervalued compared to historical data and industry averages, presenting a potential opportunity for long positions.

Introduction

Shares of Unifi ( UFI ) have fallen 14% YTD. Despite the fact that the company's operating and financial results are still under pressure relative to last year's results, I believe that the most difficult period is behind us.

Investment thesis

In my personal opinion, now we have the opportunity to open a long position at the very beginning of the trend. Firstly, in Q3 2023 (fiscal), we saw the first signs of a normalization in demand and a recovery in profitability compared to the previous quarter, especially in the US market, which is the most important, as it accounts for 65% of revenue. Second, I expect inflation to normalize in the second half of 2023 (calendar), which will support consumer clothing spending. Thirdly, revenue growth in the US segment will contribute both to the growth of economies of scale, which is positive for profitability, and the growth of revenue from the Asian segment, because some Asian customers manufacture products for sale in the US market. I believe that in the coming quarters we may see a recovery in both business volumes and operating margins, which could help boost the company's share price, while at the moment we have a relatively low buying opportunity in line with multiples.

Company overview

Unifi is a manufacturer of synthetic fibers for clothing. The main and most recognizable brand of the company is REPREVE. The main markets are USA, Brazil and Asia. The company was founded in 1969. The headquarters is located in the USA.

3Q 2023 (fiscal) Earnings Review

According to the results of the 3rd quarter of 2023 (fiscal), the company's revenue decreased by 21.9% YoY and reached $156.7 million. In terms of geography, the Asian segment was the biggest contributor to the decline in revenue, with revenue down 47% YoY, while the US and Brazilian markets were down 15% YoY and 8% YoY, respectively. You can see the details in the chart below. The decrease in revenue in the American and Asian markets is associated with a decrease in sales volumes, while in the Brazilian market the decrease is caused by a decrease in the average price of products.

Revenue by geography (Company's information)

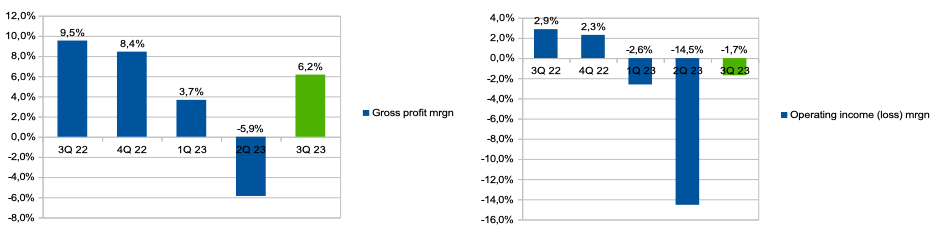

Gross margin decreased from 9.5% in Q3 2022 (fiscal) to 6.2% in Q3 2023 (fiscal). The operating margin decreased from 2.9% in Q3 2022 (fiscal) to -1.7% in Q3 2023 (fiscal). You can see the details in the chart below.

Margin trends (Company's information)

{kind=link}

In terms of yoy financial results analysis, the company continues to be under pressure from weak consumer demand, declining economies of scale and profitability trends.

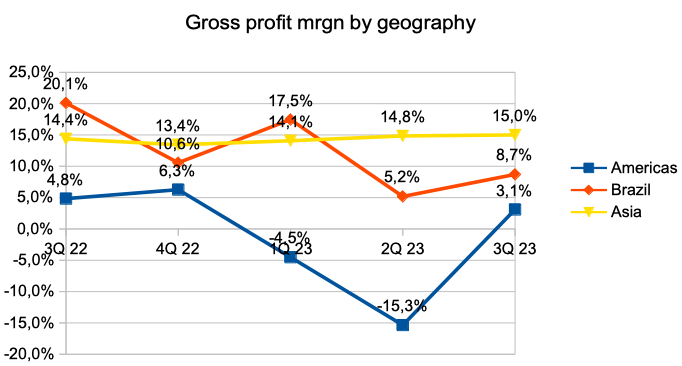

However, looking at QoQ financial results, we can see signs of demand recovering, trade trends normalizing (revenue recovery) and profitability recovering. Thus, revenue in all geography showed growth compared to the previous quarter, and the gross margin level recovered significantly. For example, the gross margin in the US market recovered from -15.3% in Q2 2023 (fiscal) to 3.1% in Q3 2023 (fiscal), in my opinion, this is a fairly significant recovery. You can see the details in the chart below.

Gross margin by geography (Company's information)

{kind=link}

My expectations

In my personal opinion, we may see an improvement in trading trends and operating margins in the coming quarters. First, based on macro data, reports from other companies in the consumer sector and my own expectations, I expect the inflation rate to decrease in the second half of 2023, which should support real consumer incomes in the US market and, therefore, contribute to the recovery of clothing and growth in the company's revenue.

Secondly, I expect that the recovery in demand in the US market will support not only revenue growth in the US segment, but also in the Asian segment of the business, since, in accordance with the comments of management, a part of the company's Asian clients produce clothes for sale to brands in the US market .

It also explains for us why our Asian business has not opened up bigger because most of our Asian sales, as most of you may know, are shipped into U.S. retailers and U.S. Brands.

Third, a recovery in sales volumes could help restore operating margins through economies of scale. In addition, I would like to note the confident statements of the company's management regarding financial results in the following quarters.

We expect a gradual improvement going into the next few quarters.

Drivers

Macro (general driver): support for the real disposable income of the population in view of lower inflation rates in the second half of 2023 may contribute to the growth of consumer spending on clothing, which is positive for the company's revenue in the US market.

Cost control: the company continues to implement solutions to effectively control operating costs. So, now the company uses a flexible workforce in the US market, which should reduce fixed costs. In addition, the company purchased new EvoCooler machines for production, which are more productive and consume less energy.

Margin: stable commodity prices and a recovery in sales volumes could support operating margins as economies of scale increase.

Risks

Macro (general risk): a decrease in consumer confidence and real incomes of consumers may lead to lower spending in the discretionary segment, which may lead to a decrease in demand for the company's products.

Margin: ?hina's extreme recovery in apparel production could push up raw material prices, which could put pressure on business margins.

Valuation

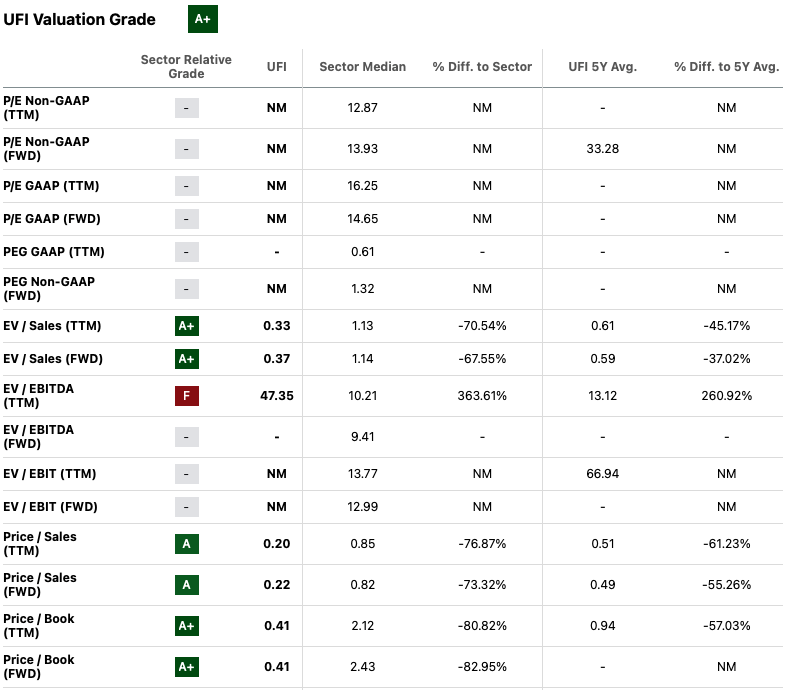

At the moment, the company's shares are relatively cheap compared to historical data and sector averages. I believe that at the moment the market does not fully take into account the potential for recovery in both revenue and profitability of the company. If we look at the multiples, only the EV/EBITDA ((TTM)) multiple looks anomalous due to the extreme pressure on the company's profitability due to weak demand over the past 12 months. Based on EV/Sales and Price/Sales multiples, the company's stock looks very attractive.

{kind=link}

Conclusion

In my personal opinion, now we have a great opportunity to open long positions. First, the current trading trends, in my opinion, indicate a recovery in clothing demand, which could support both the company's top line and profitability in the coming quarters. Secondly, in accordance with the multiples, the stock is not expensive compared to historical data and average values ??in the industry, which potentially limits the downside, since, in accordance with the dynamics of financial results in recent years, the worst quarters are behind us. I believe that the publication of financial results in the coming quarters may be a catalyst for the growth of the company's share price.

For further details see:

Unifi: Changing Trade Trends Could Push Prices Up