UNF - UniFirst Corporation: Avoid It For Now

2023-04-18 17:06:03 ET

Summary

- UNF recently announced its Q2 FY23 results.

- They recently acquired Clean Uniform intending to boost their revenues.

- I believe the current valuation is high, and the technical chart of UNF is showing weakness.

- I assign a hold rating on UNF.

UniFirst Corporation ( UNF ) offers protective workwear clothing and workplace uniforms globally. UNF designs, manufactures, rents, delivers, and sells uniform and protective clothing like pants, lab coats, and aprons. They also rent and sell floor mats, paper products, masks, and hand soaps. UNF recently announced its Q2 FY23 results. I assign a hold rating on UNF, and the reasons behind it I will discuss in this report. In addition, I will discuss its valuation and growth potential and analyze its financial performance in this report.

Financial Analysis

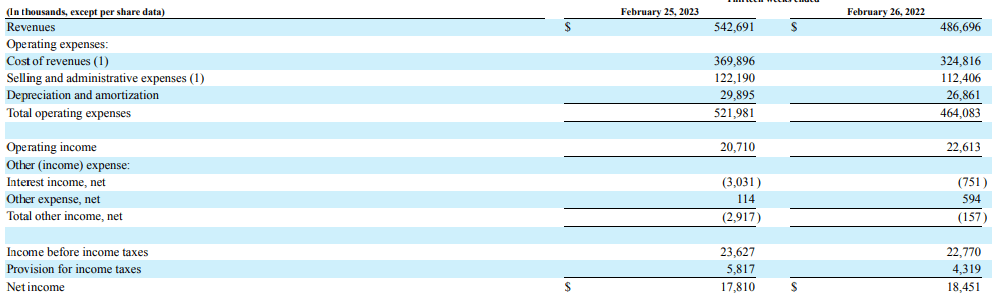

UNF recently posted its Q2 FY23 results . The revenues for Q2 FY23 were $542.6 million, a rise of 11.5% compared to Q2 FY22. I believe the main reason behind the rise was a strong performance in the specialty garments and core laundry segments. They provide cleanroom and nuclear decontamination products and services in the specialty garment segment. The revenues from specialty garments grew by 18.5% in Q2 FY23 compared to Q2 FY22. I believe the main reason behind the rise was increased project work in North American nuclear operations and solid growth in their cleanroom operations. The revenues from the core laundry operations segment grew by 10.2% in Q2 FY23 compared to Q2 FY22. I believe revenue from core laundry operations increased due to a higher pricing strategy.

{kind=link}

The net income for Q2 FY23 was $17.8 million, a decline of 3.4% compared to Q2 FY22. The $1 million loss incurred by the company in the first aid segment and the $2 million costs related to the clean uniform acquisition they incurred were the main reasons behind the decline in the net income. In my opinion, the financial performance of UNF in Q2 FY23 was decent. The revenues increased despite the challenging environment, and the decline in the net income doesn’t bother me much because I think the drop was mainly due to costs related to the acquisition; if the acquisition goes right for the company, then I believe we might see an increase in the net income in the coming quarters.

Technical Analysis

{kind=link}

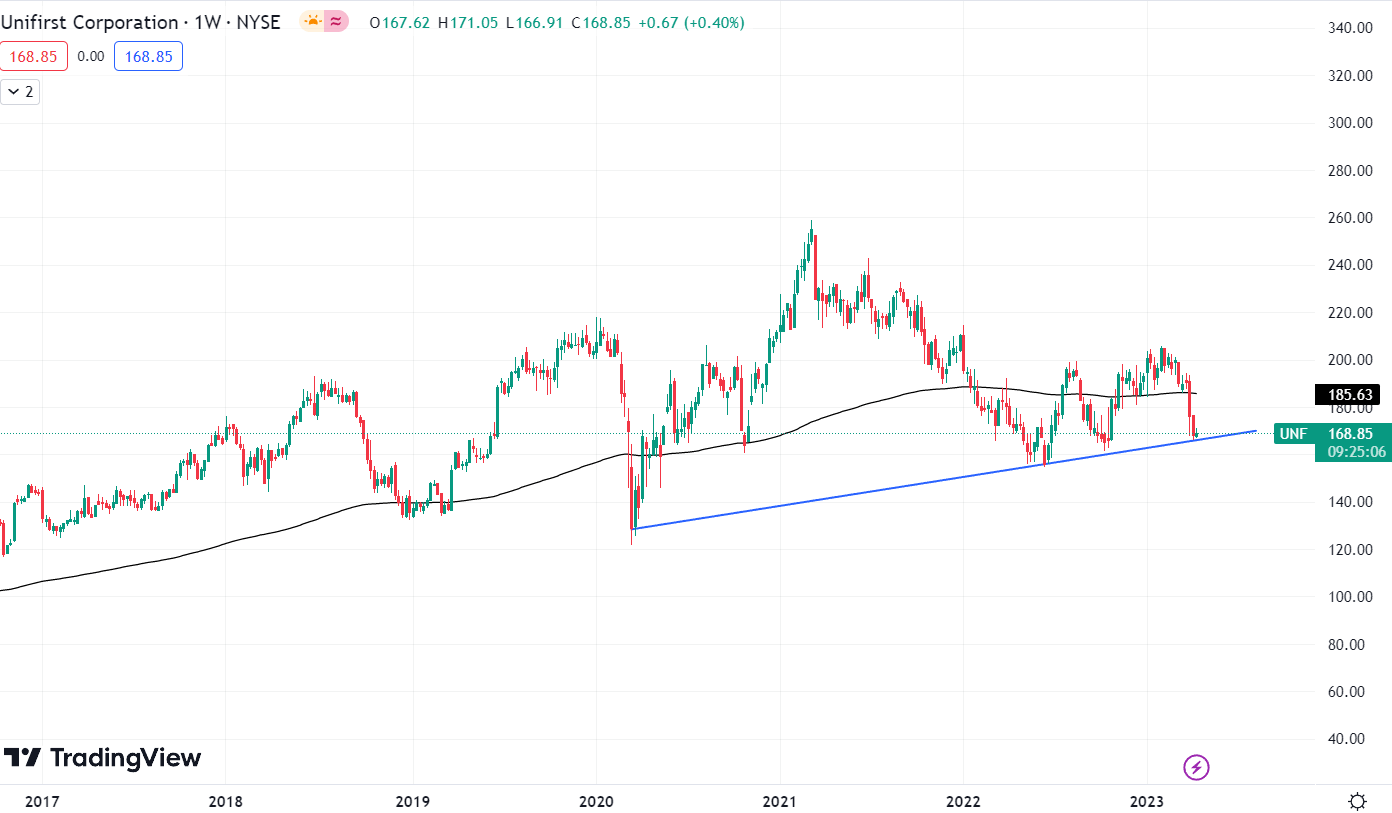

UNF is trading at the level of $169. The stock has been taking support from the trendline since March 2020. It has touched the trendline four times in the last three years, which shows that the price is following the trendline. However, in my opinion, the stock is showing bearish signs like recently it broke down its 200 ema, and the stock has formed two big red candles, which shows weakness. Currently, the stock is at a crucial level; it is taking support from the trendline; if it breaks the trendline,, the stock can fall to $130. So I believe one should not take any fresh positions in the stock as there are various uncertainties and the stock is showing weakness.

Should One Invest In UNF?

{kind=link}

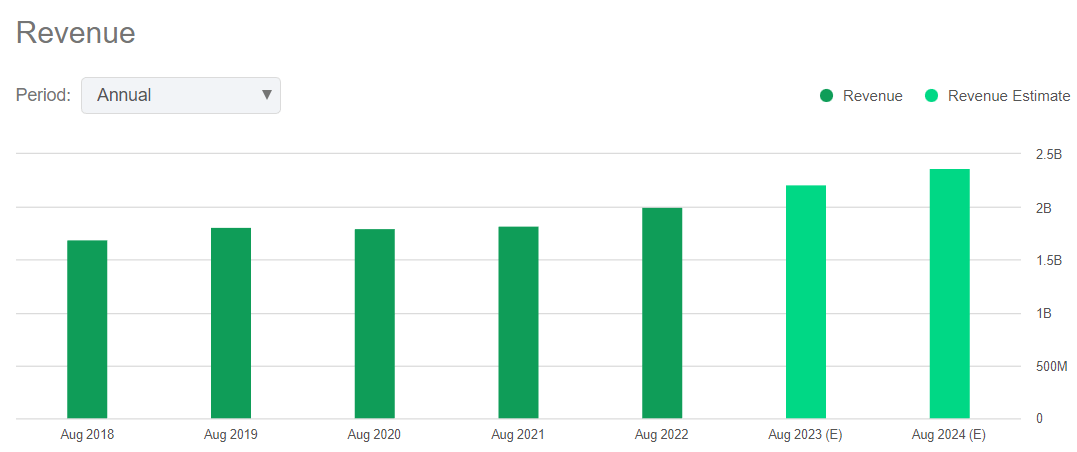

The financial performance of UNF in Q2 FY23 was impressive. Despite the challenging market environment, they were able to grow their revenues. The management has provided a revenue estimate for FY23, which is around $2.2 billion, which is 11% higher than FY22 revenue. In March 2023, they acquired Clean Uniform, an independent Uniform workwear and one of the largest facility service program providers. If the company successfully integrates its acquisition into its business, it could boost its revenues in the coming quarters. I am saying this because Clean Uniforms has a strong customer base and a high reputation among its customers due to the quality of service they provide. The management expects the acquisition to increase the core laundry operations segment’s revenue by $42 million in FY23. So if the acquisition goes right for the company, then I believe they might achieve the revenue targets.

Now talking about the valuation. I will use P/E and EV / EBIT ratios to judge its valuation. The Price/Earnings ratio is calculated by dividing a firm’s share price by EPS. The EV / EBIT ratio can be calculated by dividing the enterprise value ((EV)) by the EBIT. UNF has a P/E ((FWD)) ratio of 23.67x compared to the sector ratio of 16.42x. UNF has an EV / EBIT ((FWD)) ratio of 16.65x compared to the sector ratio of 14.62x. After looking at both ratios, I believe UNF is overvalued, and after looking at the technical chart, I believe there is a high chance that we might see a correction in the stock price. Hence I would advise not to invest in UNF due to poor technicals and high valuation.

Risks

- Generally speaking, over the past several years, the cost of healthcare that they offer to its employees has increased at a rate that has outpaced its revenue growth, which has had an adverse impact on its operating results. Additionally, US healthcare prices are commonly believed to rise in the upcoming years. Additionally, suppose many of its employees become ill or injured, including due to public work. In that case, they may have to pay a hefty amount for healthcare medical crises like the COVID-19 epidemic. Because of these aspects and depending on the impact of any changes they have made or may make in the future to our employee healthcare plans and enrollment levels in those plans, such as because of the Affordable Care Act or any upcoming legislation or regulation affecting the healthcare industry, I anticipate that their future operating results may continue to be negatively impacted by rising healthcare costs.

- With many plants, they operate a considerable percentage of their company in Canada and the United States energy-producing regions. Compared to its rivals, they are typically more dependent on business in these areas. Suppose there was to be a sharp drop in oil prices. In that case, it might affect its clients in the oil sector and force them to scale back their operations, which might have a similar impact on clients in businesses that supply or service the oil sector as well as clients in unrelated industries. As a result, greater workforce reductions in their wearer base and higher lost accounts could adversely affect organic growth in the years after a sharp decline in oil prices. Energy price volatility has occasionally greatly impacted wearer levels at current customers in the North American energy-reliant markets and could have another in the future.

Bottom Line

They reported decent quarterly results, and management has provided optimistic revenue guidance. But I think their current valuation is high, and the technical chart looks weak. So I would advise against taking any fresh positions in the company. Hence I assign a hold rating on UNF.

For further details see:

UniFirst Corporation: Avoid It For Now