UNF - UniFirst Corporation: Looking Way Better Now

2024-01-07 08:28:57 ET

Summary

- UNF's Q1 FY24 revenues rose by 9.5% compared to Q1 FY23, driven by growth in core laundry and first aid segments.

- The successful integration of the Clean Uniform acquisition has boosted sales and improved margins for UNF.

- UNF's stock is currently in a consolidation phase, but buying at the $155 level could provide a great risk-to-reward opportunity.

The last time I wrote on ( UNF ) was in April 2023. I told investors to avoid it due to the high valuation and weak price chart, and it proved to be right. The market is near its all-time, and the majority of the stocks are in an uptrend, whereas UNF’s stock price has corrected 2.7% since my last article. I am writing a follow-up on UNF because I think it is looking way better now than when I last covered it, and it might be rewarding in the coming times.

Financial Analysis

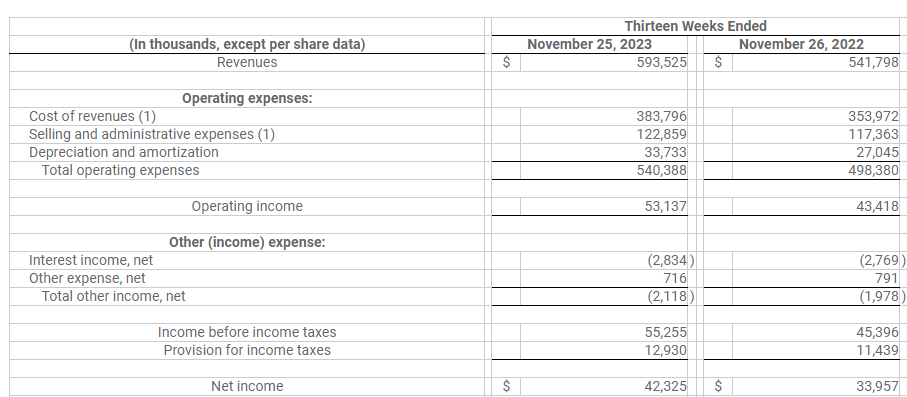

It recently posted its Q1 FY24 results . The revenues for Q1 FY24 were $593.5 million, a rise of 9.5% compared to Q1 FY23. The major reason behind the growth was a rise in revenue in its core laundry and first aid segments. In the core laundry segment, the revenue grew by 9.8% in Q1 FY24 compared to Q1 FY23. The core laundry segment benefitted from higher pricing. The revenue from the first aid segment grew by 22.6% in Q1 FY24 compared to Q1 FY23. Its operating income margin for Q1 FY24 was 8.9%, which was 8% in Q1 FY23. The improvement in operating margin was mainly due to lower energy costs and lower spending on rebranding.

{kind=link}

The net income for Q1 FY24 was $42.3 million, a rise of 24.6% compared to Q1 FY23. Apart from improved margins, an interest income of $2.1 million increased its profitability. In the last report, I emphasized that if the company successfully integrates its Clean Uniform acquisition, then it might boost its revenue growth due to Clean Uniform's strong customer base. The integration has been smooth, and the acquisition has boosted sales in the core laundry segment. So, the successful integration is a positive sign for them. In addition, the other major positive that I see is the margin improvement. In FY23, it struggled with profitability due to pressure on margins, but the improved margins in this quarter were impressive. In the past couple of years, the management has spent heavily on technology transformation and rebranding initiatives, which was one of the major reasons behind the low margins, but the management has stated that the rebranding initiatives are mostly over. So, I believe we might see higher margins with time.

Technical Analysis

{kind=link}

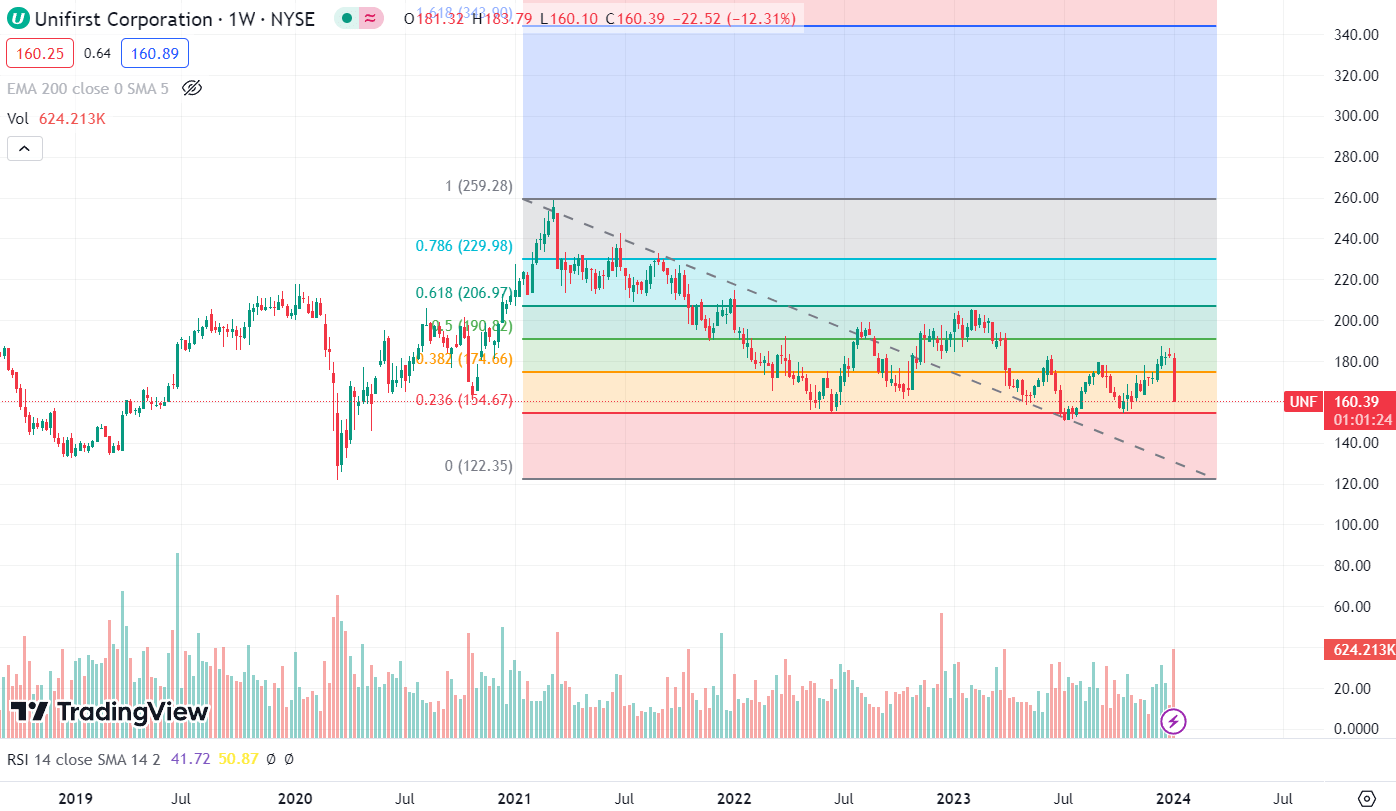

It is trading at $161.3. The stock is in a consolidation phase. It has been consolidating between $155-$181 since June 2023. In my opinion, I don’t see any buying opportunity in UNF for now. However, I believe it can provide a great opportunity in the coming times. If the stock reaches the $155 level, then it can be a great buy because it will be a great risk-to-reward opportunity. The downside risk from the $155 level is minimal because this level has been strong support for the stock since 2020. In addition, the Fibonacci retracement shows that the 0.2 level is at $155, and the chances of the stock reversing from that level are quite high. Hence, I would advise investors to add this stock to their watchlist because buying at the right level might be rewarding.

Should One Invest In UNF?

UNF has been consistently growing its revenues over the years, and it is off to a strong start in FY24. Its FY24 revenue guidance is around $2.42 billion, which is 8.5% higher than FY23 revenues. So, the expected positive revenue growth is a positive sign; there are positive revenue growth expectations, and I expect healthy margins in the coming quarters. Last time, I told you to avoid it despite it performing well because of the weak technical chart and overvaluation. However, UNF has started to look attractive in terms of valuation. It is trading at a P/E [FWD] ratio of 21.95x, which is lower than its five-year average of 25.33x, and it has an EV / EBITDA [FWD] ratio of 9.51x compared to the sector median of 11.30x. In my opinion, UNF is now looking way better than I last covered in terms of financials, valuations, and margins. However, despite all these positives, I think waiting for the right price levels might be the right choice here. The stock price is approaching the support level of $155, and buying the stock at that price level will be safer and more rewarding. Hence, I assign a hold rating on it.

Risk

Their operating margins have suffered as a result of rising inflation rates. Even though recent inflation rates have somewhat decreased, high inflation or future inflation increases could lead to a decline in the market for their goods and services, higher operating costs—including labor costs—lower liquidity, and difficulties obtaining credit or raising other forms of debt and equity capital. In addition, the US Federal Reserve has increased interest rates and may do so in the future due to worries about inflation. Continued high interest rates or rate hikes may aggravate these risks and raise economic uncertainty, which could lead to an economic recession, particularly if combined with decreased government spending and financial market volatility. They might not be able to raise the price of their goods and services at or above the rate at which their costs rise in an inflationary climate, which could lower their operating margins and materially harm their financial performance. In addition, if there is a decline in consumer spending or a negative response to their price, they can see lower-than-anticipated sales and possibly detrimental effects on their competitive position. A decline in their revenue could have a negative effect on their future growth as well as their profitability and financial situation.

Bottom Line

UNF is looking way better now than when I last covered it. Its financial results were strong, and it is off to a strong start in FY24. Its valuation also looks cheap, and it can be rewarding. However, I think waiting for the right price level will maximize the gains, and looking at the price chart, I think there is a high chance of it reaching the level of $155. Hence, for now, I will assign a hold rating to it.

For further details see:

UniFirst Corporation: Looking Way Better Now