UNF - UniFirst: Persistent Cost Pressures Vs. Growth Prospects

2023-06-29 12:29:24 ET

Summary

- UniFirst's Q3 2023 earnings report shows a bullish outlook with substantial revenue growth and strategic acquisitions, despite financial and operational challenges.

- High P/E ratios and a low dividend yield could indicate overvaluation and disappoint income-focused investors.

- Despite challenges, UniFirst's resilient business model, promising growth prospects, and strong balance sheet suggest a potential upside.

Thesis

Despite certain financial and operational challenges, UniFirst's (UNF) recent Q3 2023 earnings report reveals a bullish outlook, marked by substantial revenue growth and strategic acquisitions. However, potential pitfalls lurk in the form of persistent cost pressures, risks tied to substantial capital investments, and concerning valuation metrics. Despite these challenges, the company's resilient business model, coupled with promising growth prospects and strong balance sheet, suggest a potential upside. This analysis ultimately concludes with a cautious affirmation to hold UniFirst stock.

Company Overview

UniFirst's business model is multifaceted; they design, manufacture, personalize, rent, clean, deliver, and sell a broad spectrum of uniforms and protective wear. From everyday shirts, pants, and jackets to specialized wear such as high-visibility and flame-resistant clothing, the company covers a wide array of industries.

In addition to clothing, UniFirst broadens its revenue streams by selling and renting industrial products such as wiping items, floor mats, and both dry and wet mops. The company also engages in supplying facility services, catering to the needs of businesses in need of restroom and cleaning supplies. From sanitizers and hand soaps to gloves and masks, they're in the business of ensuring cleanliness.

UniFirst's Bullish Q3 2023 Earnings Takeaways

UniFirst's Q3 2023 latest financial report present an uplifting narrative, with consolidated revenues experiencing a robust 12.7% uplift year-on-year to clock in at a healthy $576.7 million. The twin engines of this remarkable growth, a testament to the efficacy of the firm's pricing strategies within an inflation-challenged landscape and their formidable sales performance, should not be underestimated.

The company's Core Laundry operations formed the backbone of this growth, demonstrating an organic expansion of 7.8%. Coupled with this, we see the Specialty Garments segment making a dramatic leap of 19.9%. This surge, attributable to robust cleanroom operations and an uptick in project work within North American nuclear operations, is a solid indication of the segment's potential as a powerhouse of growth in the future.

The analysis becomes more nuanced when we shift focus to the operational profitability. Although there is a slight contraction in consolidated operating income, a silver lining emerges in the form of the EBITDA metric. A healthy upswing of 6.3% in this metric, reaching $64 million from the previous year's $60.3 million, points towards an enhanced operational efficiency.

Despite shouldering some costs associated with strategic initiatives such as CRM, ERP, and branding, along with the financial burden of the Clean Uniform acquisition, UniFirst's financial fortitude holds strong. Its balance sheet stands resilient, boasting zero long-term debt and maintaining an enviable cash position of $69.3 million. There's a particular noteworthy point in the form of operating cash flows - they've surged to $142.8 million from last year's $88.8 million, an indication of the business's reduced need for working capital, reflecting improved efficiency and liquidity management.

The acquisition of Clean Uniform, while being a financial load in the short term, carries the promise of lucrative returns in the future. This strategic move is already bearing fruit, contributing roughly $20 million to the Core Laundry Operations' revenue in this quarter alone, offering a glimpse of the potential value it might add moving forward.

UniFirst's robust revenue growth in the Specialty Garments segment, alongside the burgeoning First Aid segment (which posted a strong 25.8% increase), underscores their potential as significant growth catalysts for the future.

Looking at the bigger picture, UniFirst projects its consolidated revenues for the full year to land somewhere between $2.22 billion and $2.23 billion. Although the company anticipates a squeeze in the Core Laundry Operations' operating and EBITDA margins due to persistent cost pressures, it is tactfully offsetting this by making strategic investments to prime itself for future growth.

Valuation

Their D+ Valuation Grade (see table below) and particularly the high P/E ratios raise eyebrows for me. Their Non-GAAP P/E ( TTM ) of 23.33 is quite ahead of the sector median of 16.89, a 38.12% difference. And looking forward, the discrepancy persists with a 37.73% difference. To further dampen enthusiasm, these numbers mark a drop from their 5-year average, indicating a possible trend of overvaluation.

Seeking Alpha

The picture isn't much rosier with their GAAP P/E. While they're running significantly hotter than the sector at a whopping 59.96% and 65.42% difference for TTM and FWD respectively, it's the upswing from their 5-year average that bothers me. An 18.5% and 15.58% increase from their average indicates a steadily inflating valuation that I find concerning.

Without a coverage of the PEG ratio, it's challenging to decipher the growth prospects priced into these elevated multiples. Nonetheless, it's clear the market is paying a premium for future growth, but whether that's justified remains to be seen.

On the brighter side, the EV/Sales metrics paint a friendlier picture. With ratios under the sector median and a 5-year average, they suggest relative undervaluation. I do admire the attractive EV/EBITDA, with both TTM and FWD under the sector median and only a minor departure from their 5-year averages.

However, the company's EV/EBIT ratio strikes me as a bit too high, which could be an indicator of low operating profitability or an overpriced stock, or a mix of both. Similarly, the price to cash flow ratios - especially the 22.00 TTM, well above the sector's 14.79 - gives me pause. It seems to suggest that the market may be too optimistic about the company's ability to generate future cash flow.

Also, their low dividend yield of 0.74% compares poorly with the sector median of 1.47% and should disappoint income-focused investors. Although there has been some improvement from their five-year average dividend yield figure, much more work needs to be done in improving it further.

{kind=link}

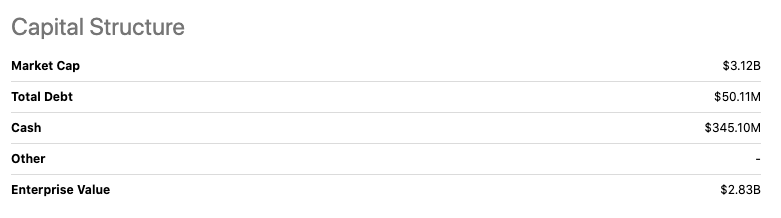

And finally, UniFirst's capital structure presents a comforting sight. Their market cap of $3.12B seems reasonable, and the relatively low total debt of $50.11M juxtaposed against a substantial cash position of $345.10M does provide a sense of stability.

Risks & Headwinds

UniFirst's Core Laundry segment has been a primary victim of substantial cost pressures, which have contributed to a noteworthy contraction in both operating margin and EBITDA margin .

The cause of this predicament?

An unforgiving trifecta of high healthcare claims expenses, unresolved legal affairs, and an upswing in operating costs driven by the prevailing inflationary environment. The cumulative impact of these factors is manifesting in a distressing trend-a palpable decrease in operating income, EBITDA, and Earnings per Share ( EPS ).

On a more granular level, the First Aid segment paints a concerning picture. Despite posting a healthy 25.8% year-on-year revenue boost, the segment slipped into the territory of operating loss. This insinuates potential obstacles in scaling operations effectively and maintaining the profitability of this business sector.

UniFirst's stock repurchase program raises eyebrows, as its apparent hesitation to purchase additional common stock during this quarter is perplexing. Meanwhile, the company has made aggressive moves with regard to capital investments, investing a massive $124.1 million into capital expenditures and another significant sum ($306.2 million) into acquisitions. While this might appear as an optimistic strategy at first glance, such investments could become riskier should their expected returns fail to materialize, further complicating its financial outlook.

Finally, UniFirst's projection of diminished operating and EBITDA margins for its Core Laundry Operations sector, projected at the midpoint of the range of 4.7% and 10.5% respectively, is not particularly encouraging. This gloomy forecast seems to stem from modest revenue expectations coupled with the persisting cost pressures, signaling a tough path ahead for the company.

Final Takeaway

The resilience of UniFirst's business model, the robust revenue growth, and a strong balance sheet make a compelling case to hold the stock. Despite the cost pressures and potential overvaluation, strategic acquisitions and investments hint towards future growth potential. While risks remain, these are offset by operational efficiency improvements and diverse revenue streams, leading me to affirm the analytical call to hold UniFirst stock.

For further details see:

UniFirst: Persistent Cost Pressures Vs. Growth Prospects