UL - Unilever: A Consumer Giant In Need Of A Turnaround

2023-06-19 23:56:00 ET

Summary

- Unilever has been underperforming in the past few years, as the management team continues to disappoint in execution.

- The company's growth remains very underwhelming while the amount of debt and leverage continues to increase.

- The rapidly declining inflation should put pressure on pricing, which will likely further weigh on growth in the near term.

- The current valuation is cheap, as multiples are meaningfully lower than other leading consumer staples companies.

Investment Thesis

Unilever ( UL ), in my opinion, is a great example of a great company with a bad management team. The company has huge opportunities with its leading brands but the potential was never realised. Its fundamentals have been deteriorating in the past few years and so did the share price. As shown in the chart below, shares have declined around 4% in the past 5 years, substantially underperforming the S&P 500 ( SPY ) and peers like Nestle ( OTCPK:NSRGY ).

The company is trying to reaccelerate growth, but it will likely take some time before we see any meaningful progress. With inflation now easing quickly, it should also face increasing pressure on pricing, which will likely further impact growth. The company's valuation is discounted but the weak growth will likely weigh on its upside potential in the near term.

Underwhelming Execution

Unilever is one of the world's leading consumer goods companies, operating over 400 brands in 5 major categories: Beauty & Wellbeing, Personal Care, Home Care, Nutrition, and Ice Cream. The London-based company owns some of the most iconic brands such as Dove, Lipton, Ben & Jerry's, and Vaseline.

While the company has a strong and diverse portfolio of brands, the management team's execution has been very underwhelming in the past few years. Due to multiple acquisitions, the company racked up over €17 billion in debt in the past 6 years alone. It divested a few brands during the process but it still has over $30 billion of debt outstanding at the moment. This resulted in the leverage (net debt/EBITDA) ratio reaching 2.2x, the highest since 2017 and also above the company's target of 2x. Most acquisitions did not pay off either, as revenue growth remained soft (as shown in the chart below) while the ROIC (return on invested capital) continued to drop.

Shifting To Beauty & Wellbeing

Unilever is now hoping to reaccelerate growth by shifting its focus to the Beauty & Wellbeing segment, which has the most potential. According to the company , the TAM (total addressable market) of the segment is €350 billion growing at a CAGR (compounded annual growth rate) of 4% to 6%. The growth is largely driven by increasing awareness of self-care and the rising influence of social media, especially TikTok and Instagram.

The company is aiming to "premiumize" its products by leveraging its strong branding, especially within the beauty segment. As of last year, premium products only account for around 30% of total turnover, which leaves ample room for expansion. A successful shift towards the higher-end market should be highly accretive, as premium products generally have higher margins and better pricing power. It is also aiming to put more resources into emerging markets, predominantly India and China which have enormous populations.

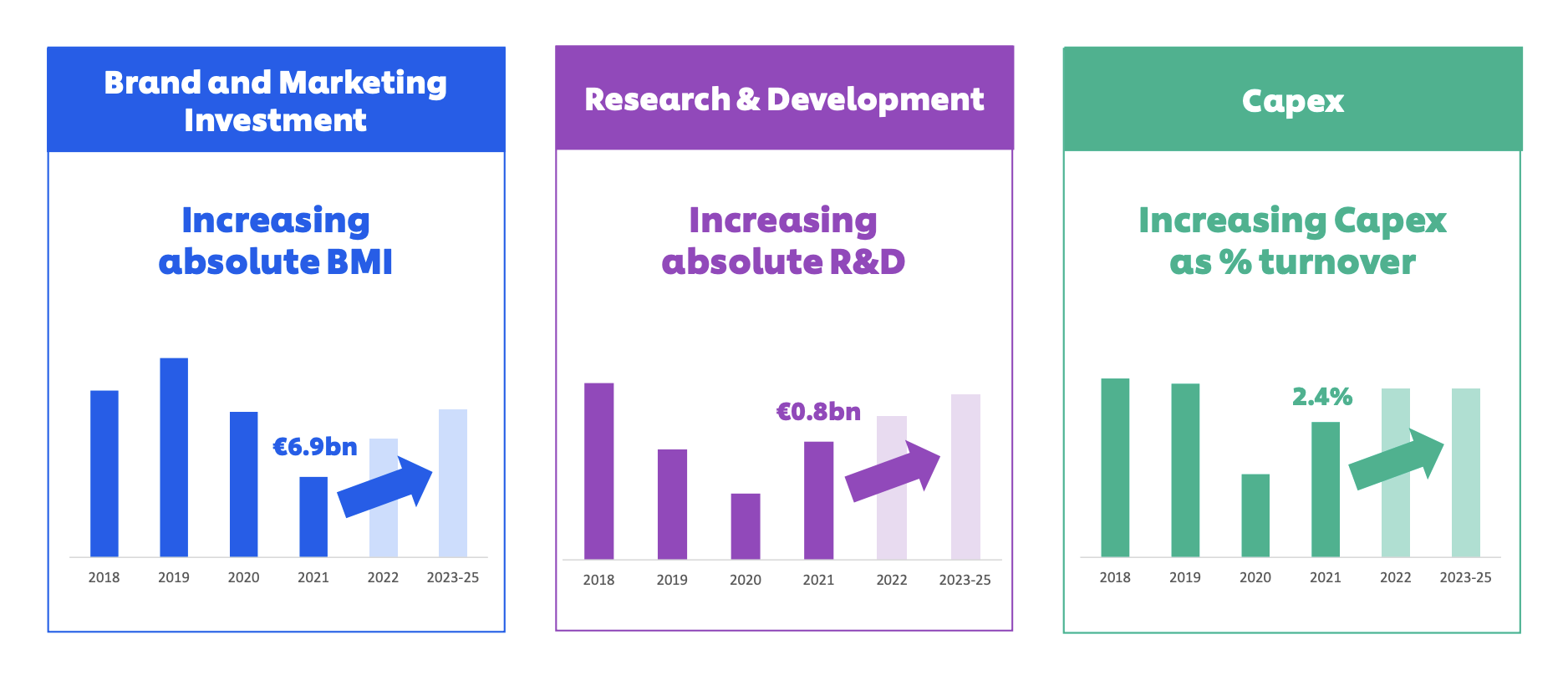

In order to support these growth initiatives, the company is turning on the tap again by reaccelerating its investments. After a few years of slow spending, marketing expenses, R&D (research and development) expenses, and CAPEX are all set to increase in the next few years, as shown in the charts below.

{kind=link}

Inflation Headwind

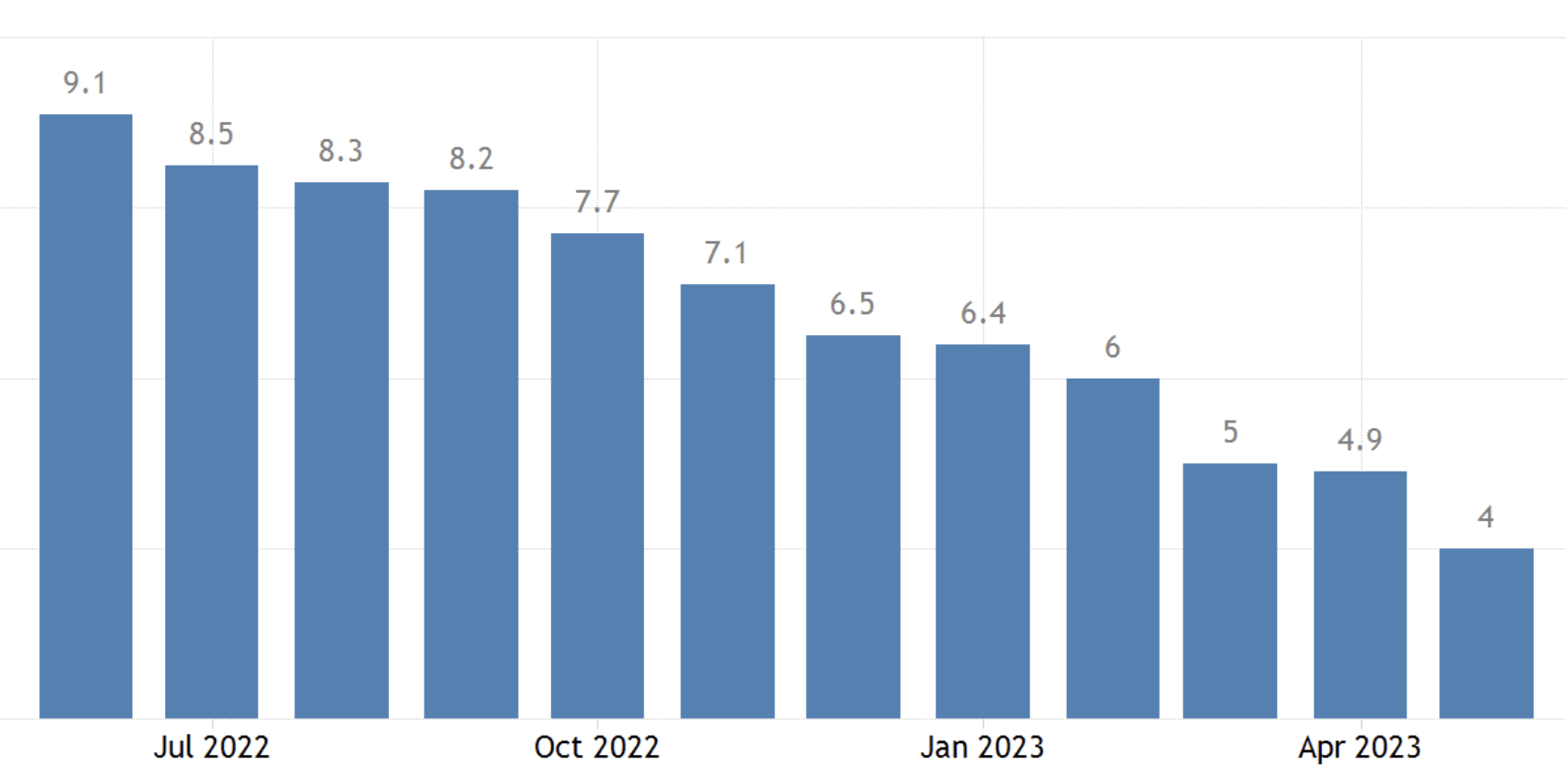

The rapidly declining inflation should also be a major headwind for Unilever moving forward. The US CPI ( consumer price index ) for May came in at just 4%, down from 4.9% in the prior month and 9.3% in the prior year. While the core CPI remains elevated, most of the stickiness came from services and housing segments. The slowing inflation will likely put heavy pressure on the company's pricing, as it is becoming much harder to justify further price increases to customers without significantly hurting demand.

This will impact growth substantially as the company has been relying heavily on price increases to drive revenue. It has also been able to raise prices at an even higher percentage due to its strong branding. For instance, pricing grew 10.7% YoY (year over year) in the latest quarter, while volume actually dropped 0.2% YoY. As price increases become increasingly unsustainable, the company's growth rate should also start to decline meaningfully.

{kind=link}

Cheap Valuation

Unilever has one of the more compelling valuations in this expensive market. The company is currently trading at a PE ratio of 16.7x, which is pretty discounted among the consumer staples sector. As shown in the first chart below, the current multiple is meaningfully lower than notable peers such as Procter & Gamble ( PG ), Mondelez International ( MDLZ ), and Kimberly-Clark ( KMB ). They used to trade at similar levels but the trend has diverged in the past few years. Unilever is now trading at a 33.5% discount compared to the peer group's average PE ratio of 25.1x. While the company's valuation is cheap, its growth rate of 1.3% is also the weakest among the peer group, as shown in the second chart below. I believe the soft growth will likely weigh on the company's upside potential in the near term.

Investors' Takeaway

I remain highly skeptical of Unilever's outlook despite it having such a strong and diverse portfolio of brands. The company is hoping to reaccelerate growth through the Beauty & Wellbeing segment but whether it will succeed remains highly uncertain, especially when considering the management team's poor track record. Not to mention the headwind from inflation should further drag on growth in the near term. Unilever is cheap but there should not be much upside potential until the company can show meaningful progress on a turnaround. On a more positive note, I think the discounted valuation and its well-diversified business should still provide solid downside protection. Therefore I rate Unilever as a hold.

For further details see:

Unilever: A Consumer Giant In Need Of A Turnaround