UL - Unilever: A Slowing Eurozone And Currency Risks Should Concern Investors

2023-11-02 09:56:47 ET

Summary

- Unilever's stock has not performed well in the past five years, offering investors only 5.29% total returns compared to the S&P 500's 68.71%.

- The company's growth outlook has deteriorated due to economic challenges in the Eurozone and Asia, and it lacks a plan for substantive organic sales volume growth.

- Unilever's revenue growth has been weak, relying on unsustainable price increases, and its recent earnings show struggles in growing organic sales volume.

Companies with strong brands are not always appealing investments. While iconic labels often have more inelastic demand, growing saturated brands is often a challenge. The market will also frequently charge a significant premium to invest in these companies.

The Unilever ( UL ) corporation owns some of the most well-known brands in the world. This British company owns Ben and Jerry's, AXE, comfort, Dove, and many other established brands across different industries.

Still, this well-known retailer's stock has gone nowhere in the last five years. Unilever has offered investors total returns of just 5.29% over the last five years, while the S&P 500 ( SPY ) has offered investors total returns of 68.71% during the same time period.

I last wrote about Unilever in March of this year. I rated the stock a sell because of my view that the company was relying on unsustainable price increases to drive growth, and the company also faced a number of macro headwinds as well. The stock is down 5.4% since that time measured by total returns, while the S&P 500 is up 6.52% during this same time frame. Today I am downgrading the company to strong sell. The economic growth outlook has deteriorated significantly in the last couple of months in the Eurozone and Asia, Unilever still has no plan to drive substantive organic sales volume growth with the company's saturated core brands, and the company will also likely face increasing forex headwinds as well.

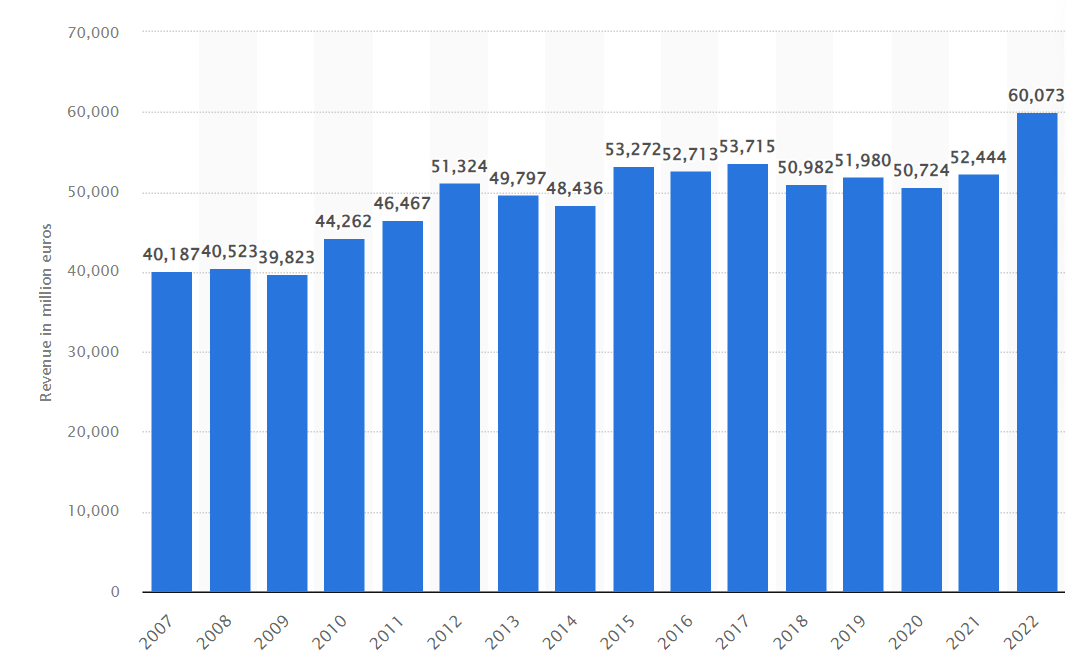

A chart of Unilever's revenues (Statista)

{kind=link}

Unilever's revenue growth was anemic from 2012 to 2021, and management was only able to drive earnings growth in 2022 because of what are likely unsustainabale pricing power. The company's recent earnings report shows that management is also continuing to struggle to grow organic sales volume as well.

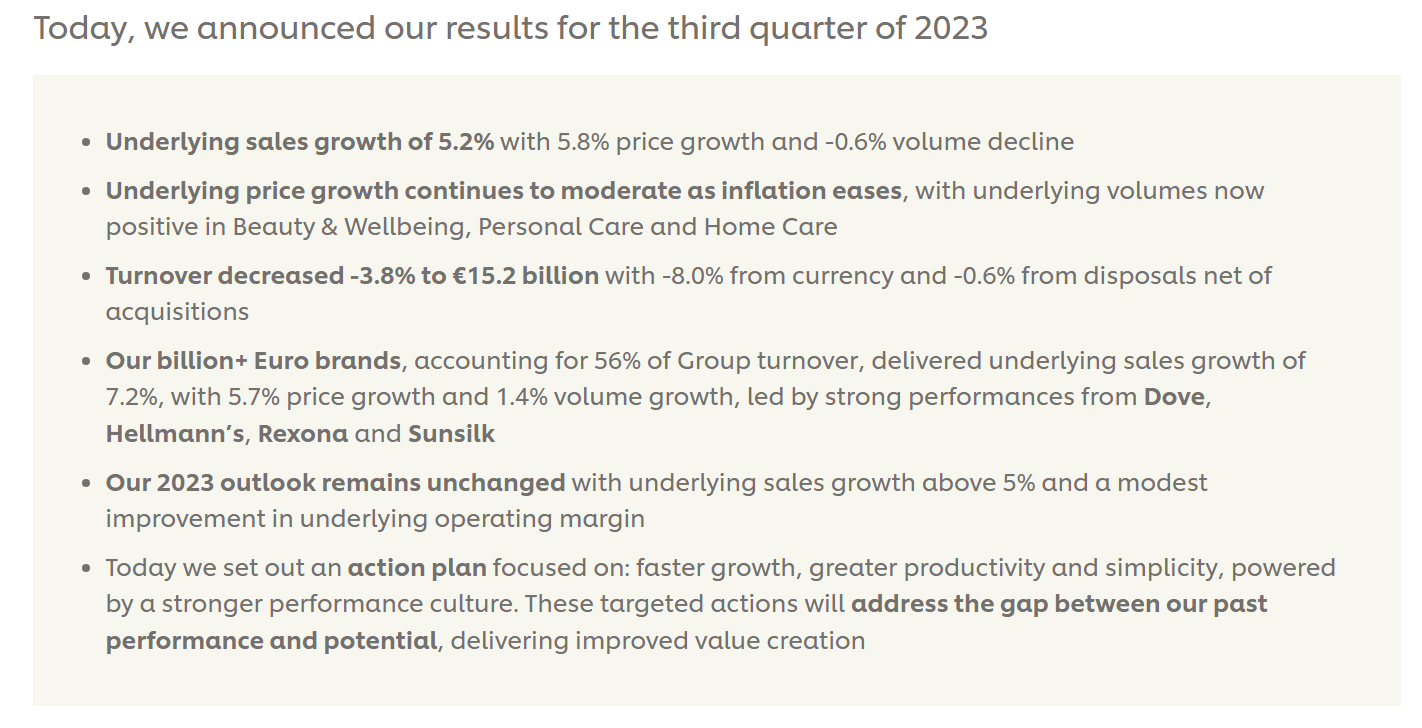

An excerpt from Unilever's earnings report (Unilever)

{kind=link}

Unilever saw sales grow 5.2% in the third quarter because of 5.2% price growth overall volumes declined across the company's division by .6%. The company's earnings growth was solely the result of price increases, and management also did not raise guidance for the full year either.

The Eurozone economy looked to be stabilizing after the EU resolved the recent energy crisis over the past year, but the economic outlook in this region has worsened significantly over the last several months. The European Commission recently downgraded growth estimates in the Eurozone from 1% to .8% this year, and growth estimates were downgraded for next year from 1.7% to 1.4%. The commission is also forecasting inflation this year in the Eurozone to be 5.6% this year, and 2.9% next year, while above the European Central Bank's target of 2%.

Growth estimates in Asia have also recently been revised down as well, with the Asian Development Bank revising their economic growth outlook for the region down from 4.8% to 4.7%. The EU is also China's biggest trade partner, so the deteriorating growth outlook in the Eurozone will obviously lead to further downward revisions in Asia's economic outlook as well.

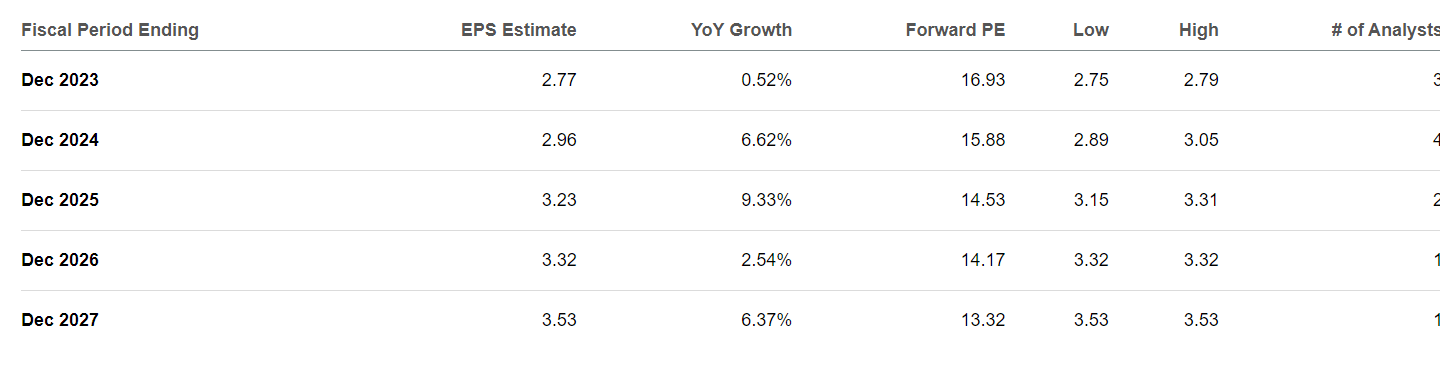

This is why Unilever looks significantly overvalued at the current share price of 16.93x likely forward earnings. The company is only expected to grow revenues by 3-4% over the next several years, and the retailer's earnings are also supposed to increase by only 4-5% over the next 2 years.

A table of Unilever's revenue projections (Seeking Alpha) A table of Unilever's revenue projections (Seeking Alpha)

{kind=link}

{kind=link}

Even though most of the core brands of Unilever are fairly recession-resistant, the growth premium for a company with saturated brands that have not been growing for years is unrealistic. Unilever's brands have very high market share right now, and the company hasn't able to grow them for some time. Hellman's currently has nearly 30% of the mayonnaise market in U.S., while Dove's market share in the U.S. is 40%.

Since Unilever's growth rate remains anemic, the company is also vulnerable to even slight forex moves, and the current inflation rate of 3.7% in the US is also while above the Fed's 2% target for the rate of price increases as well. The Fed is unlikely to reverse the current rate cycle, and the US economy remains stronger than the economies in the Eurozone. The dollar is likely to continue to rise against the Euro and other major currencies in the current economic environment, which would also put additional pressure on Unilever's minimal earnings growth.

While there is a possibility Unilever could outperform, this scenario is unlikely. If inflation were to come down, and the ECB and Fed were to pause the current rate cycle, the EU and US economies would likely recover much faster. A reversal of the current rate cycle would also impact forex moves as well, likely causing the dollar to weaken against foreign currencies. Unilever still has a possibility of seeing organic sales volume growth in markets where the company's brands have lower market share, such as in Asia and in some emerging markets as well. These events remain unlikely.

Companies with well-known brands often trade at a premium, and this leading European retailer looks significantly overvalued at the current price. Unilever's management team has not shown any ability to consistently grow the company's saturated brands. While the company's iconic brands aren't likely to lose significant market share any time soon, investors should be able to find better value elsewhere.

For further details see:

Unilever: A Slowing Eurozone And Currency Risks Should Concern Investors