UNLYF - Unilever: Appetizing With A FCF Yield Of 6.3% Hedged To Inflation

2023-07-18 14:19:16 ET

Summary

- Unilever is a leading consumer staples company that should perform well in a slowing economy and the latest Q1 results showed price increases covering inflation.

- The company's stock seems reasonably priced at 15.6x TTM P/E, providing a good investment opportunity in today's expensive market.

- Investors may be able 6.3% free cash flow yield from Unilever, which should adjust for inflation in the long term due to the strong premium brands of the company.

Unilever ( UL ) is an attractive consumer staples company that I believe should fare well in a slowing economy with high inflation. With a share price of $52.43, Unilever offers investors a good 6.3% free cash flow yield that should adjust long-term for inflation through the pricing power of the company's premium brands. As a consumer staple company, revenues should be less cyclical in an economic recession than other more discretionary businesses. The company has underperformed the market in recent years, but the current low valuation makes Unilever look like a conservative investment opportunity in an expensive market.

Q1 Results Show a Good Inflation Hedge

Unilever's latest Q1 2023 results released April 27th showed what a strong hedge to inflation a consumer staple company like Unilever can offer shareholders. The company saw revenues increase YoY by 10.5% driven by 10.7% price increases partially offset with a small 0.2% decrease in volumes.

These Q1 results shows that even in a flat sales volume environment, Unilever is able to maintain pricing power with consumers as cost pressures mount in their supply chains. Business profits in general can be a good long-term hedge to inflation and great companies like Unilever are able to shorten the pace with which they are able to pass along cost increases to the consumer, all without harming volume.

Unilever also continues share repurchases as part of its dividend program which will be discussed more later. The company's third €750 million share buyback tranche, announced in March, will complete in July 2023 and is likely to be renewed as part of the company's regular capital return program to shareholders.

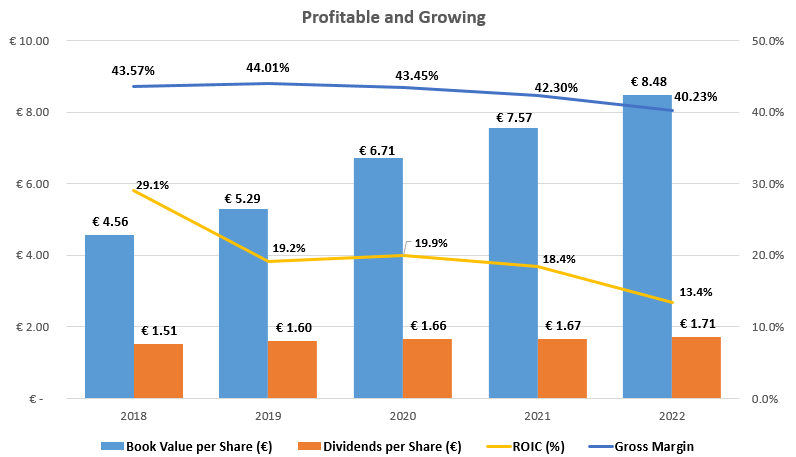

Profitable and Growing

Unilever's strong brand portfolio and scale have allowed it to achieve an average return on equity and return on invested capital of 41.6% and 18.9%, respectively, over the past five years. This level of profitability is well above my rule of thumb of 15% ROE and 9% ROIC, allowing me to be confident that, in my opinion, the company is able to maintain and continue to increase its intrinsic value over a business cycle.

Profitability and Growth at Unilever (compiled by author from company financials)

{kind=link}

Over this time period, dividend growth has been on par with my expectations for a mature consumer staples company. From 2018 to 2022, the dividend has grown from €1.51/share to €1.71 for an average compound growth rate around 3.2%. The dividend looks well supported by earnings given the 57% dividend payout ratio in the fiscal 2022 year. This low payout ratio leaves room for future dividend growth to continue. Let's analyze the potential for increased dividends more through looking at the cash flows.

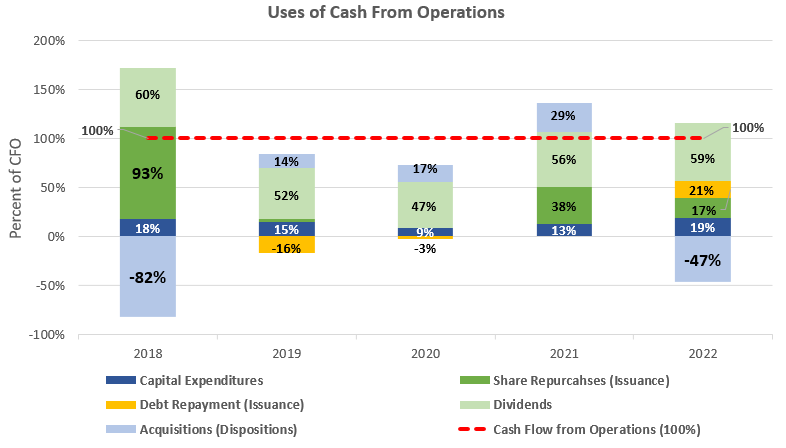

Cash Flow Analysis

Unilever does a great job of generating cash and returns it to the shareholder through both dividends and share repurchases. To get an idea of the sustainability of dividends and share repurchases, we can take a look at what percent of cash flow from operations is available to be returned to shareholders after making the necessary capital expenditures.

As can be seen below, capital expenditures only used up on average only 15% of cash flow from operations over the past decade. This leaves approximately 85% to be returned to investors in the form of dividends and share repurchases. With an average cash flow from operations of €8.1 billion over the past three-year period, this 85% would imply free cash flow to shareholders of €6.6 billion for around a 6.32% free cash flow yield at the current €120.2 billion market capitalization.

Cash Flow Analysis of Unilever (compiled by author from company financials)

{kind=link}

As readers of my articles will know, I normally like to include spending on acquisitions in this FCF calculation as well, but Unilever has actually sold off more worth of businesses than they have acquired in the last 5 years! Given those positive divestitures net of acquisitions, this further cash inflow would only to go to increase the FCF yield, so I have conservatively focused on the figure excluding divestitures.

If we do include the net acquisitions/divestitures over the past five years, the FCF yield rises to 6.77%. It would seem Unilever has great brands to sell off without harming sales! If growing brands and then selling them off is a regular part of Unilever's business and one's investment thesis, this could be the more relevant FCF yield investors might want to focus on.

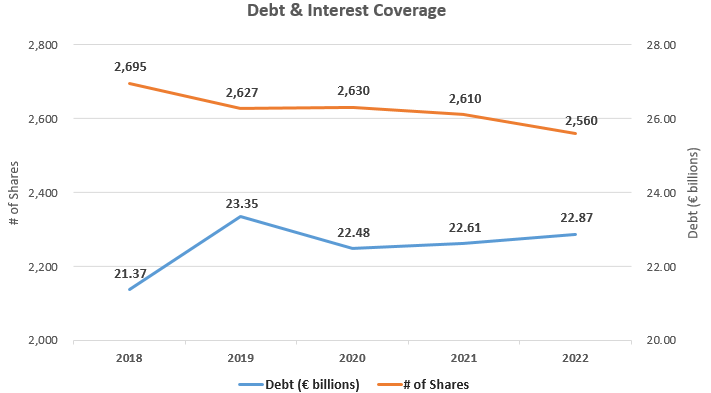

How About the Debt?

Financial leverage at Unilever remains healthy and conservative. The company has been responsible to not get carried away with cheap debt issuances in the past few years as some other companies aggressively have. Share repurchases have been made sustainably using cash flow from operations as discussed earlier and have averaged 1.27% annually over the period. The financial leverage still remains fairly conservative for a consumer staple company as evidenced by an interest coverage ratio of 12.3x in the 2022 fiscal year.

Share Repurchases and Debt at Unilever (compiled by author from company financials)

{kind=link}

Price Ratios and Potential Returns

Unilever's 15.6x TTM P/E ratio can also be expressed as a 6.4% earnings yield, but I also always like to examine the relationship between average ROE and price-to-book value in what I call the Investors' Adjusted ROE. It examines the average ROE over a business cycle and adjusts that ROE for the price investors are currently paying for the company's book value or equity per share. With Unilever earning an average ROE of 41.6% since 2018 and shares currently trading at a price-to-book value of 5.52x when the price is $52.43 (€46.78), this would yield an investors' Adjusted ROE of 7.5% for an investors' equity at that purchase price, if history repeats itself. This is slightly below the 9% that I like to see, but adding a 3% growth rate to represent this mature company growing alongside global GDP, could increase this potential total return up to 10.5%.

Potential Shareholder Yields from Unilever (compiled by author from market data and company financials)

Risks from Competition

While Unilever might have a powerful brand portfolio with many leading names, they do operate in a fragmented market that faces competition from other brand name players as well as the in-house private brands of large retailers. In times of economic weakness, consumers can substitute for these cheaper in-house brands which have, in my tasteful opinion, continued to improve in their product quality over the years. This competition could see Unilever sales suffer disproportionately compared to the total category in a recession and grow at a slower pace than GDP growth.

In such a fragmented and competitive market it takes a lot of marketing spend to keep brands top-of-mind and relevant. Unilever does a good job of tweaking brands and the product portfolio to stay relevant (i.e., environmentally friendly, vegetarian/vegan, etc.) but there is always the risk of major brands and categories losing favor with consumers. This would of course harm revenues and require more brand acquisitions to keep the portfolio fresh, which would hurt free cash flows available to investors.

Takeaway for Investors

Unilever is a great consumer staple company that is still trading at a reasonable valuation and should be less exposed to an economic slowdown than other more cyclical businesses. From the latest Q1 results, it looks like the company is doing a good job of passing on cost increases to consumers and giving investors a hedge against inflation. With a free cash flow yield around 6.3% and similar TTM earnings yield of 6.4%, Unilever still looks like a good investment to hold onto in a high inflation environment, even with GIC rates offering attractive relative 5% yields to equities.

For further details see:

Unilever: Appetizing With A FCF Yield Of 6.3% Hedged To Inflation