UL - Unilever: At The Crossroads Of Years Of Underperformance

2023-08-23 12:19:13 ET

Summary

- Unilever's Revenue and Operating Margin have gone virtually nowhere in the past decade due to a lack of focus and underwhelming investment in growth areas.

- With the appointment of a new CEO and change in strategy, the H1 2023 report shows initial signs of growth resurgence, anticipated to extend into H2 and beyond.

- Offering a robust 3.61% dividend, considerably surpassing the industry average, the company maintains a secure payout ratio of 52%, setting the stage for growth in the upcoming years.

- Based on my Fair Value assessment, considering a projected CAGR growth of 3.1% over the next decade, Unilever is trading today with a 20% discount.

Investment Thesis

Unilever (UL) stands as a multinational consumer goods enterprise celebrated for its extensive array of offerings encompassing personal care, food, and household products. Boasting a storied legacy that spans numerous decades, Unilever has firmly positioned itself as a prominent figure within the worldwide market, emphasizing innovation, sustainability, and ethical commitment.

Unilever Portfolio Map (Unilever Website)

{kind=link}

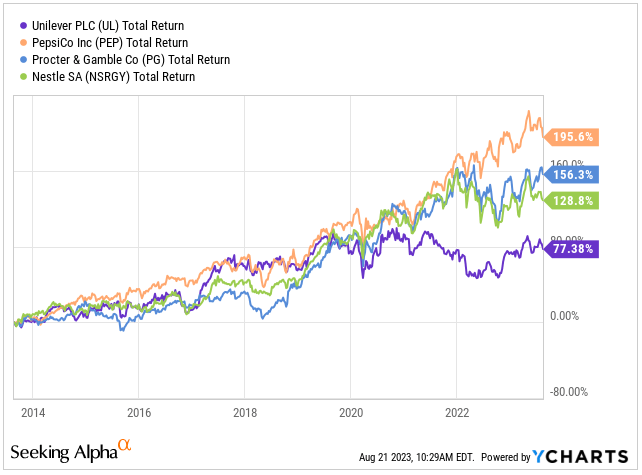

In spite of its business magnitude, Unilever has faced difficulties in achieving substantial revenue and profit margin growth over the last decade, leading to a performance lag compared to its industry counterparts. Throughout the period from 2013 to 2023, the company's revenue and operating income have virtually gone nowhere, occasionally edging higher or lower. Despite this historical plateau in growth and profitability enhancement, Unilever boasts a formidable portfolio that, with a well-devised strategy, holds the potential to pleasantly surprise investors in the coming years. I firmly believe, the recent appointment of Hein Schumacher as CEO, coupled with the strategic approach of streamlining products and focusing on core brands with growth potential, while simplifying organization which fosters brand innovation, stands as a pivotal lever capable of unlocking shareholder value moving forward.

Total Return vs. Peers (Seeking Alpha / YCHARTS)

{kind=link}

Business Update

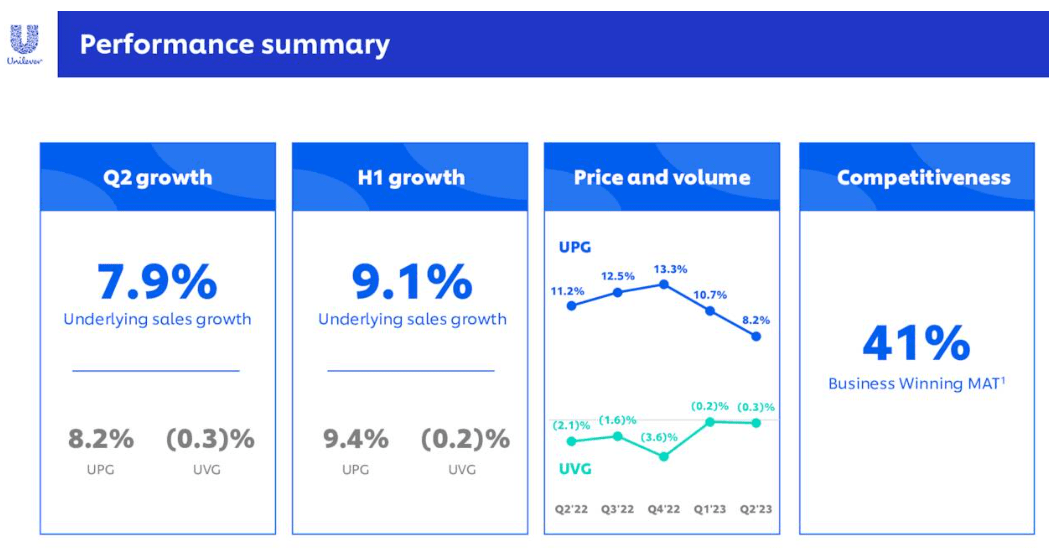

Unilever's performance in the first half of the year has brought a positive surprise, which can be attributed to the strategic consolidation of businesses initiated over a year ago. This move has led to a simplified organizational structure with a greater focus on high-growth segments. During the first half of 2023, the company has achieved an underlying sales growth of 9.1%, driven by a 9.4% increase in prices, accompanied by a slight 0.2% reduction in volumes. As price growth gradually moderates over the course of the year, different business units are navigating the diverse phases of the inflationary cycle. These results highlight effective inflation management achieved through responsible pricing, a positive trajectory in volume, and the emerging recovery of gross margin.

The Business Winning measure dropped to 41% over the past quarter, which, from my perspective, is a bit disappointing. Unilever is now focusing on improving this measure . The decline was influenced by a mix of strategic decisions, shifts in consumer behavior, and competitive vulnerabilities.

- First, business groups intentionally streamlined portfolios, leading to SKU rationalization programs for improved structural health. While necessary, this temporarily impacted market share.

- Second, ongoing cost inflation in Nutrition and Ice Cream led to needed pricing adjustments, resulting in short-term turnover losses.

- Third, consumers shifted toward segments less covered by Unilever, reflecting a value-driven trend seen in the growth of unbranded tea in India and budget-friendly laundry brands in Brazil.

Performance Summary (Unilever IR)

{kind=link}

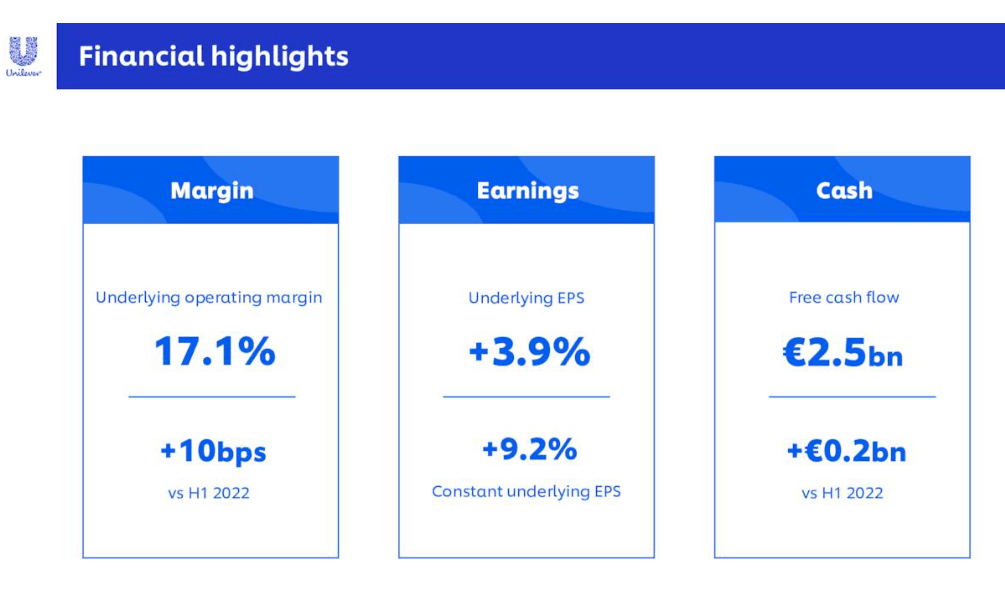

Let's shift our focus to financial highlights. The underlying operating margin stood at 17.1%, marking a 10 basis point rise from the same period last year and increase from the stable 16.7% average in the last decade. The improvement was driven by a healthy increase in gross margin , alongside elevated brand investment and a decrease in overheads as a percentage of turnover. Underlying earnings per share saw a 3.9% rise from last year, and free cash flow remained robust at €2.5 billion, a €0.2 billion increase compared to the corresponding period last year.

Financial Highlights (Unilever IR)

{kind=link}

Turning to Unilever's key markets , the U.S. achieved 7.4% growth, as increased volumes in Prestige, Beauty, and Health & Wellbeing areas compensated for slower price growth. Meanwhile, India achieved a commendable 9.1% growth, effectively balancing price and volume amidst dynamic competition, notably excelling in Home Care. In China, growth surged to 7.9% in H1, fueled by volume, particularly in Food Solutions and out-of-home Ice Cream.

Across emerging markets, which constitute nearly 60% of total turnover, growth reached 10.6%, driven by both price increases and positive volume trends. The transformative impact of Digital Commerce persisted, making up 16% of turnover with a 16% growth in H1. Adapting to evolving channels, including short videos and group buying, which remains a top priority for the company.

Although H1 2023 has marked a much-needed positive phase for the company, I anticipate a similar performance in H2. The easing of commodity pressures should allow for a sufficient gap between input costs and pricing, thereby enabling margin expansion. However, the company still has a considerable journey ahead to realize its new strategy and achieve robust growth to catch up with its competitors.

Return to Shareholders

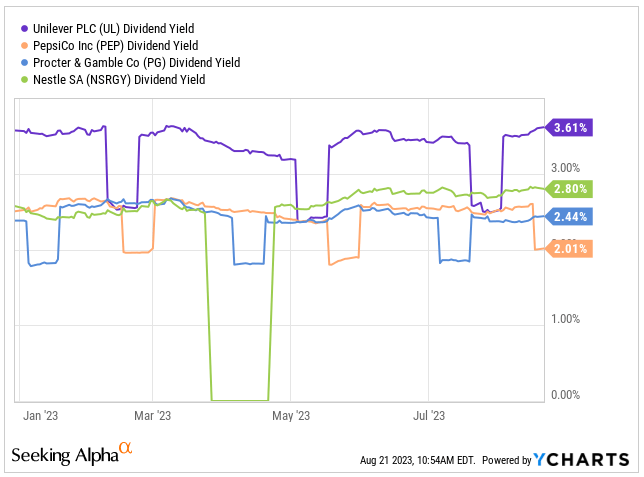

Even though the company hasn't seen much growth in its value due to stagnant revenue and margin expansion in the past decade, it's been treating its shareholders well by consistently providing them with a reliable dividend. This dividend streak has been going strong since 1999. Right now, the dividend rate is at 3.61%, with company's payout ratio of no more than 52%. This stands out quite favorably when compared to the lower dividends of PepsiCo ( PEP ) at 2.80%, Procter & Gamble (PG) at 2.44%, and Nestlé (NSRGY) at 2.01%.

Dividend Yield vs. Peers (Seeking Alpha / YCHARTS)

{kind=link}

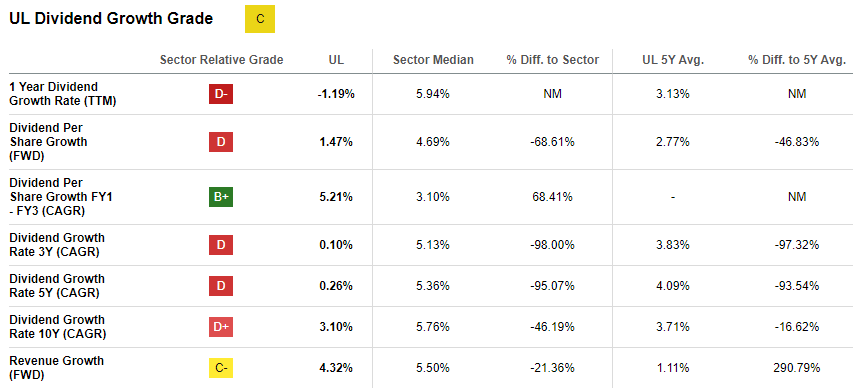

Nevertheless, even though the yield appears attractive when compared to the industry median of 2.43%, the issue becomes apparent when examining the dividend growth rate, which has been hampered by the absence of overall growth. Over the past decade, the company has displayed modest dividend growth with a mere CAGR of 3.10%, a notable difference from the industry median of 5.76%. Similarly, in the last 5 years, its dividend growth was just 0.26% as opposed to the industry's 5.36%.

As we move ahead, I personally think that the potential for future dividend growth will rely on how well they carry out their new growth and margin expansion strategy. If this strategy doesn't pan out, we could find ourselves stuck with the current dividend status quo.

Dividend Growth Score Card (Seeking Alpha)

{kind=link}

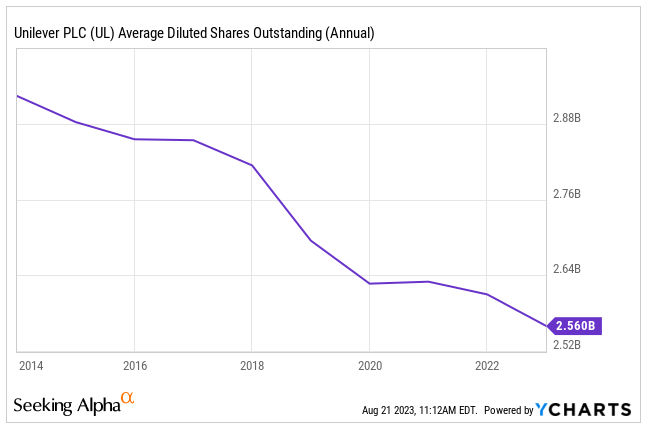

A notable aspect of the company's return to its shareholders has been its share buyback program, which has seen Unilever repurchasing 11.4% of its shares since 2013. While this might be perceived positively by investors, indicating healthy balance sheet to fund such initiatives, my perspective leans toward the opposite. I believe the company should have directed those funds towards fostering growth or enhancing operational efficiency to bolster its bottom line. This choice seems to me as indicative of a lack of clear focus and strategic direction.

Shares Outstanding (Seeking Alpha / YCHARTS)

{kind=link}

Valuation

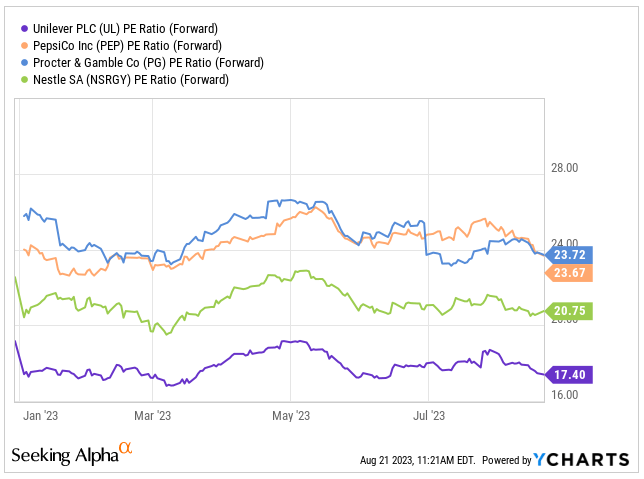

Now, the one area where Unilever truly stands out is the valuation.

I find the company's valuation to be quite attractive. At present, it carries a Forward PE ratio of 17.40x. In comparison, peers like PepsiCo trade at 23.67x, Procter & Gamble at 23.72x, and Nestle at 20.75x. This equates to an approximate undervaluation of Unilever by about 23.3%.

In my view, Unilever shouldn't necessarily be trading at such a discount compared to its peers. Despite its limited growth over the past decade, the company consistently generates substantial FCF and maintains a track record of steady performance. As long as it continues delivering consistent results and potentially drives growth and margin expansion through its new initiatives, I anticipate its valuation will gradually align closer that of its peers, offering upside from its current level.

Forward PE Ratio vs. Peers (Seeking Alpha / YCHARTS)

{kind=link}

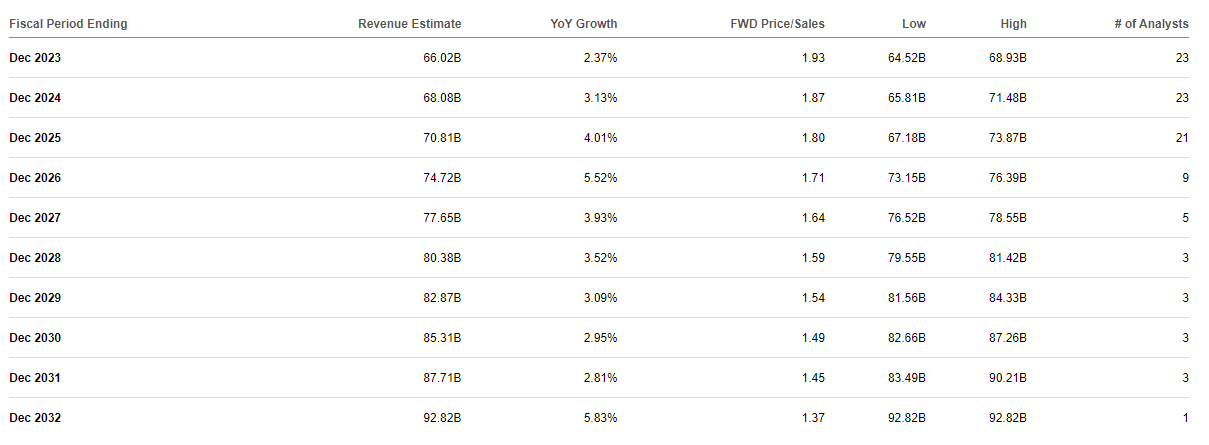

Looking ahead to the next decade, analysts anticipate Unilever to achieve a Revenue growth of CAGR of 3.1%. I agree with this forecast, provided that the company's operations run smoothly without significant hindrances arising from a decelerating economy or further inflation-related pressures that could prompt increased monetary tightening. This growth trajectory is expected to be primarily propelled by the expansion of its core brands and a greater market share in untapped markets. If this prediction materializes, we should expect Unilever to achieve revenue nearing $93 billion by 2032. Assuming that the operating margin remains consistent with the decade's average of 16.7%, we could anticipate an Operating Income of approximately $15.5 billion, leading to an approximate 50% expansion from current year.

Financial Estimates (Seeking Alpha)

{kind=link}

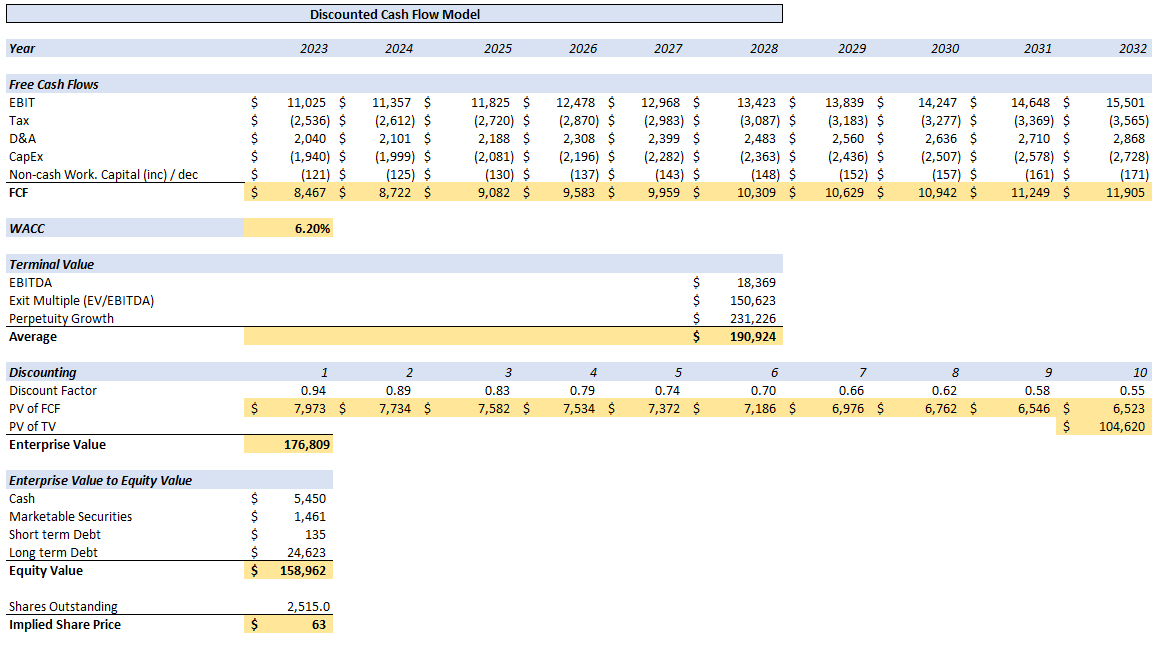

To gauge Unilever's Fair Value, I am using DCF Model. Building upon the mentioned growth projections, I've adopted a WACC of 6.20%, coupled with a Tax Rate of 23%, and a Terminal Growth Rate of 1.5%- slightly below the long-term GDP growth rate of developed nations. Drawing from historical data, I've approximated Depreciation & Amortization and CAPEX to likely fall within the respective range of around 18.5% and 17.6% relative to EBIT. The Average Terminal Value is computed by multiplying EBITDA with an EV/EBITDA ratio of 8.2, adjusted by the Perpetuity Growth Value and WACC.

Once these values are discounted over the ensuing 10 years, the PV of FCF amounts to roughly $72.2 billion, while the PV of TV reaches nearly USD 105 billion. Consequently, the overall Enterprise Value is approximated at nearly $177 billion. After accommodating Cash, Marketable Securities, Short & Long-term debt adjustments, the resultant Equity Value stands at approximately $159 billion.

DCF Model, Fair Value (Author's Table)

{kind=link}

Utilizing the growth projections integrated into the model, my estimation for Unilever's Fair Value stands at approximately $63.00 USD. This reflects a discount of around 20% in comparison to the current price of $50.50 USD. With that, I rate the stock as a BUY at a current price.

Conclusion

Even though Unilever boasts a diverse range of products and a rich history, it has struggled to achieve revenue and profit growth over the last decade. Nevertheless, I'm optimistic about the company's future due to the recent change in strategy and the appointment of a new CEO. I believe their strategic shift towards focusing on core brands with promising growth profiles, simplified organizational structure, and brand innovation will play a crucial role in enhancing shareholder value.

Interestingly, Unilever pleasantly surprised us in H1 2023, indicating the initial positive outcomes of their strategy change. The company showcased accelerated growth and improved margins during this period. Taking into account that the stock is currently undervalued compared to its fair value, I rate is as a BUY.

For further details see:

Unilever: At The Crossroads Of Years Of Underperformance