UNLYF - Unilever: Bears Are Getting It Wrong Again

2023-09-27 09:00:10 ET

Summary

- Unilever outperformed the broader consumer staples sector since I made the stock a high conviction idea of mine.

- Bears remain focused on the currently lower margins and the probability of a lower revenue growth going forward.

- In the meantime, margins are set to improve over the coming quarters as the scenario that the market is pricing-in appears unlikely.

A large multinational consumer staples business like the one of Unilever ( UL ) does not bring any associations with high and speculative returns over the short-term.

Instead, a company like UL is a vehicle for wealth preservation and above market returns once risk is taken into account. Of course, there are periods of time when perceived risk in the market is low and a business like this is put at a significant disadvantage to the high growth names.

That is why, it is important for long-term shareholders to accumulate more stock when it's favourable to do so. In my view, one such period was last October, when I covered Unilever as a high conviction idea for my subscribers.

In spite of all the headwinds, UL delivered a total return of nearly 14% since then, thus significantly outperforming the Consumer Staples Select Sector SPDR® Fund ETF ( XLP ) on an absolute basis.

Unilever is also among the largest positions in my personal portfolio and the portfolio that tracks all of my high conviction ideas.

{kind=link}

Now that growth stocks are at significant risk of underperforming due to changing monetary conditions, value names like Unilever are once again attractive. On top of that, Unilever in particular has some important characteristics that bears are ignoring or missing out due to emotional biases.

Where Bears Are Getting It Wrong

Lagging revenue growth and slower than expected turnaround in margins are among the key talking points of Unilever's bears. This highlights the poor understanding of the business and is often due to the framework of evaluating growth stocks being applied here.

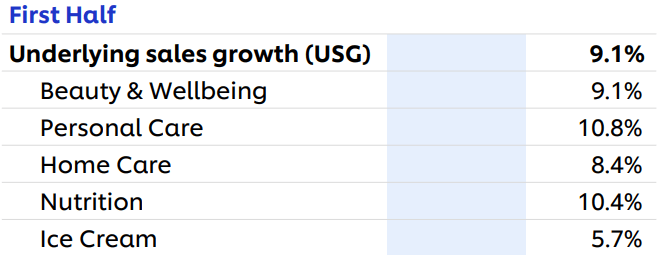

I will talk about margins in the next section of this article, since it is one of the key aspects of my investment thesis. But when it comes to growth, Unilever's topline figure has expanded by 17% since 2019 (pre-pandemic) which is almost 5% on an annual basis.

This might not sound as much, but it doesn't take into account the significant amount of disposals that Unilever's management has made in recent years. Moreover, after the severe hit on Unilever's business during the pandemic and the recent inflationary pressures, the strong brand portfolio has allowed for significant price increases which ultimately led to a near double-digit growth rate for the first half of 2023.

{kind=link}

More importantly, investors should be following closely Unilever's margins and return on capital, which has improved considerably over the past year.

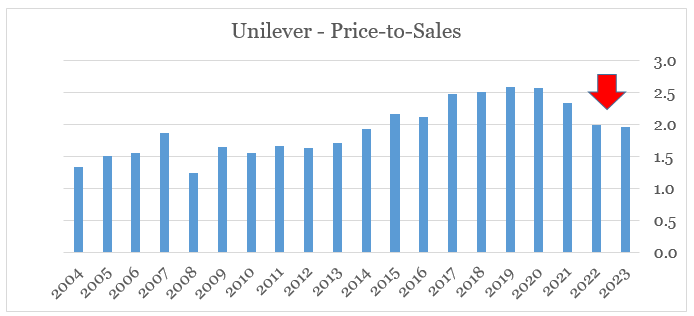

As Unilever's business is slowly improving and the more focused brand portfolio allows for significant price increases without loss of market share (more on that later), the market has become increasingly bearish on the stock. To illustrate that, we could have a closer look at the company's Price-to-Sales multiple, which has declined from 2.6 in 2020 to less than 2.0 as of today.

{kind=link}

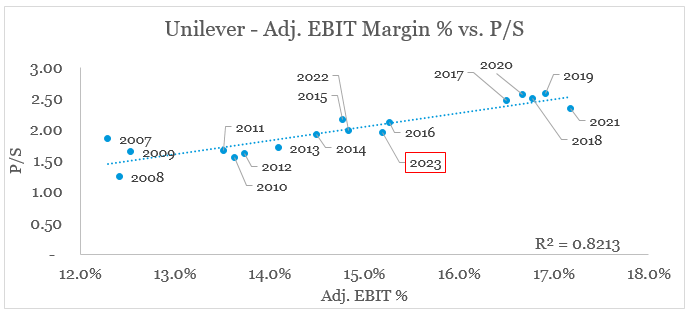

Although I see no justifications for this beyond the short-term, the reality is that Unilever's current operating margin can't support a higher multiple even as topline growth remains elevated. The reason why I am saying this is because of the more than a decade-long strong relationship between UL's Price-to-Sales multiple and its Adjusted Operating Margin.

prepared by the author, using data from annual reports and Seeking Alpha

{kind=link}

What this means is that the 14% return we saw at the beginning of this article was almost entirely due to Unilever's elevated sales growth, which was more than enough to offset the recent decline in profitability. As we look forward, however, margins are set to improve while growth will slow down but is unlikely to be below the rate of inflation.

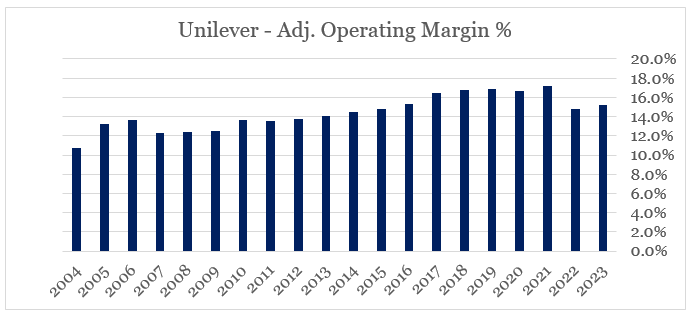

A Bottom In Profitability

As I mentioned above, Unilever experienced a major drop in operating margin in 2022, and although there has been some improvement over the first half of 2023, they remain at of their lowest levels in 2016.

{kind=link}

We also saw that the market is currently pricing in a scenario in which this level of profitability will remain constant. In my view, this is where the market is getting it wrong and where the opportunity lies.

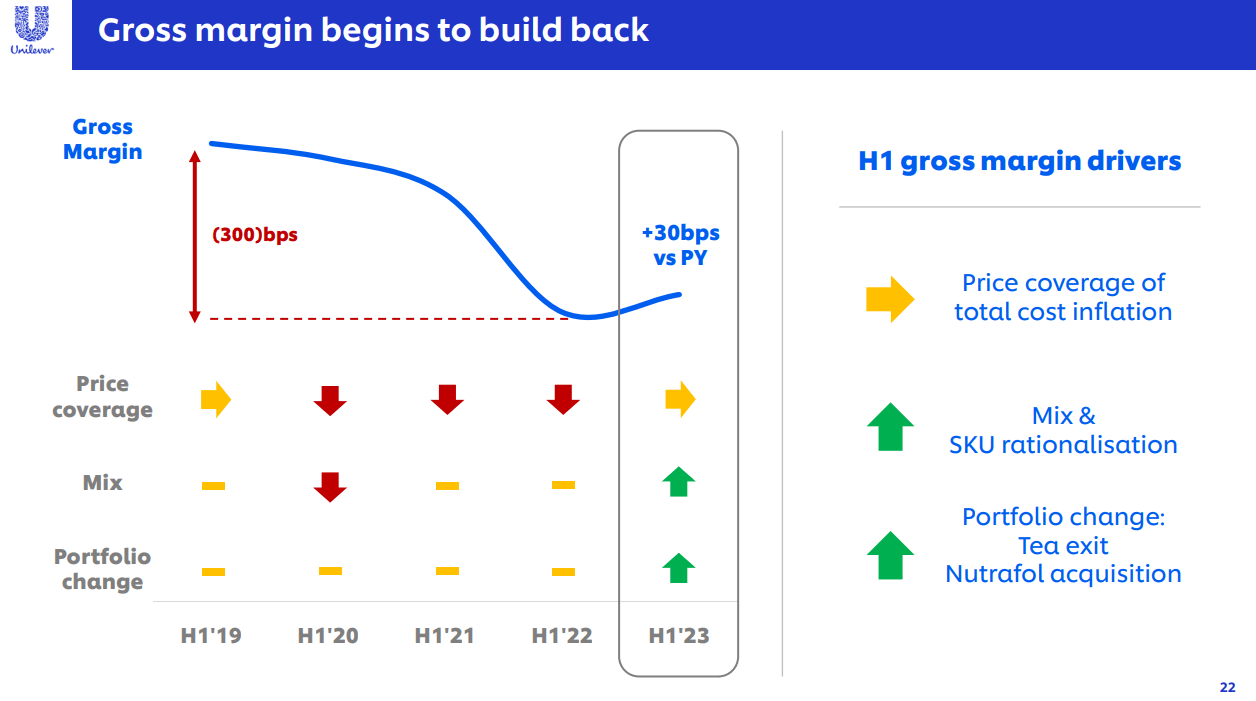

To begin with, one of the major reasons for the decline has been the drop in Unilever's gross margin. This, in turn, has been caused by the time mismatch between the recent price increase in raw materials and the full implementation of Unilever's price increases.

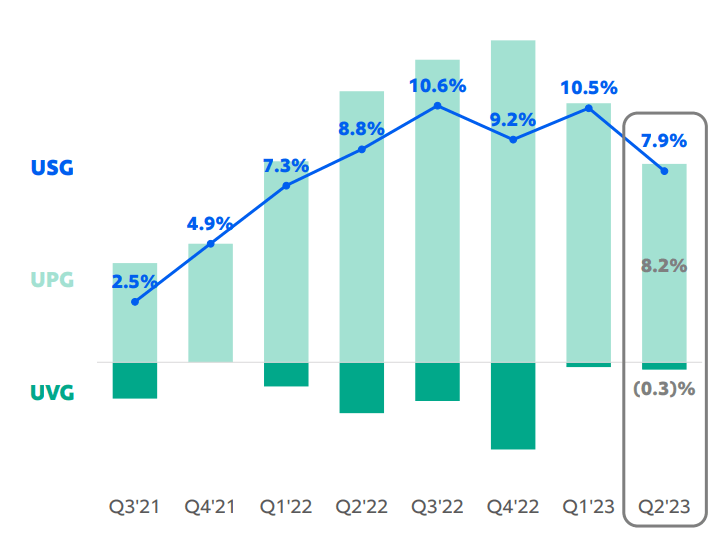

As price increases continue to flow through the topline figure, Unilever's gross profitability will experience a tailwind in the coming quarters, but more importantly is that even the double-digit price growth (UPG on the graph below) did not result in a material volume loss (see UVG below).

{kind=link}

Thus, the price coverage of total inflation would likely have a material positive impact on Unilever's gross margin going forward, in addition to the current tailwinds resulting from the portfolio optimization and restructuring.

{kind=link}

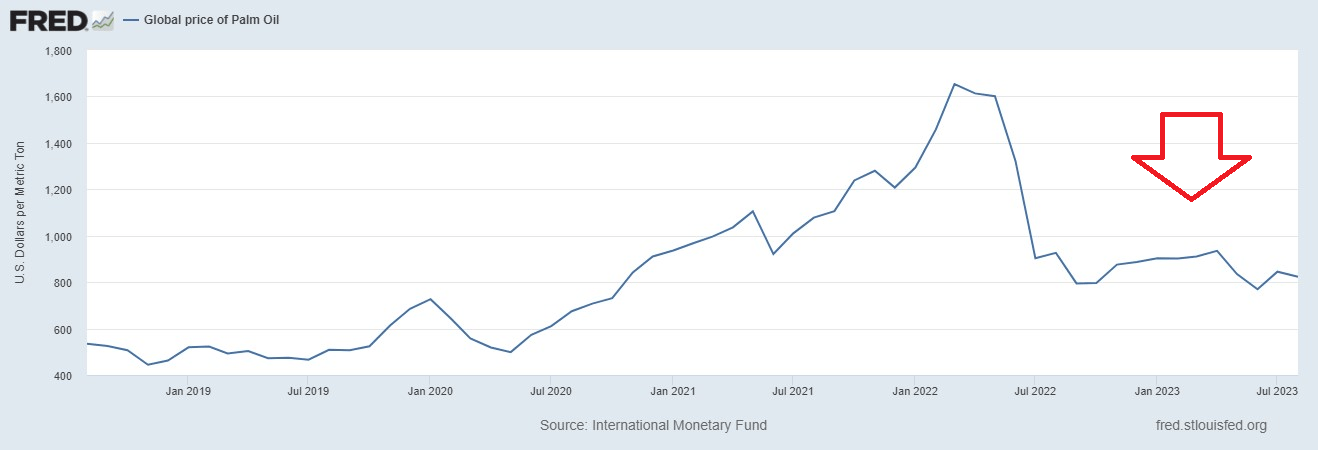

As usual, commodity prices remain as the wild card in the equation, but we are already seeing a notable cool-off in some of Unilever's main raw materials used. For example, the company is one of the largest buyers of palm oil in the consumer goods industry and the global price of the oil is already down significantly.

{kind=link}

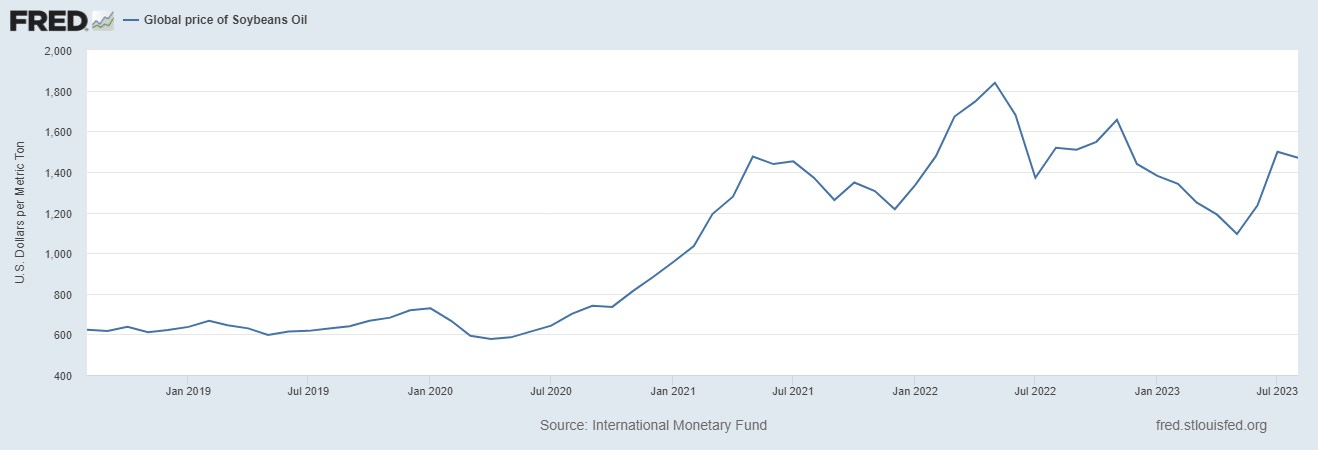

Another important input for Unilever is soybean oil, which remains elevated in price, but has come down slightly from its recent top and now trades well-below the 2022 highs.

{kind=link}

Conclusion

Over the past year, Unilever has outperformed the broader consumer staples sector as topline growth figure came in higher than expected. In the meantime, bears remain focused on things in the rear-view mirror, such as lower profitability and the fading impact of higher product pricing. The mistake they are making is that margins are now set to improve and should drive an upward multiple repricing. Last but not least, the more optimized and very strong brand portfolio will allow for moderate topline growth.

For further details see:

Unilever: Bears Are Getting It Wrong Again