UL - Unilever: Defensive Investment In An Uncertain Year

2023-04-30 02:32:49 ET

Summary

- Consumer goods giant Unilever has seen a nice price recently, but considering its competitive P/E compared to peers, it could rise more.

- It has seen strong revenue growth, and its operating margin looks all right too, considering the inflationary environment.

- Its outlook is also healthy, and a presence in emerging markets can cushion from the recessionary conditions in advanced economies, making it a Buy for now.

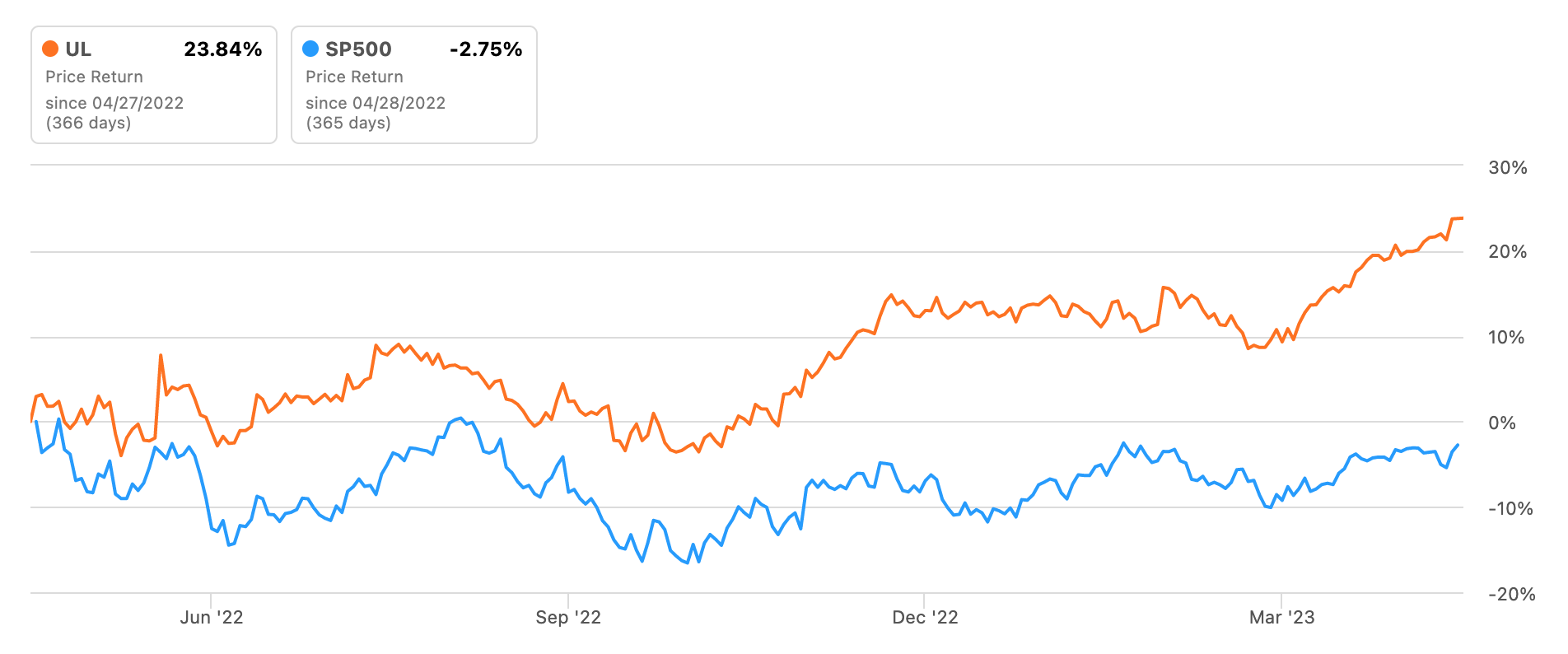

During periods of economic weakness, like right now, defensive stocks can make for good investments while the stock markets look uncertain. Consumer staples giant Unilever PLC (UL), of well-known brands like Dove, Knorr and Lux is one of them. It is little wonder that in the past year, its price has risen by almost 24%, far outstripping the S&P 500 ( SP500 ), which has actually fallen by almost 3% during the time (see chart below). Even year-to-date [YTD], when the S&P 500 has seen much better performance, with an increase of 9%, Unilever is slightly ahead with a 10% rise.

{kind=link}

Strong sales growth

Underpinning its superior share price performance is its robust performance, which is really the reason to consider consumer staples during a recession. Their demand remains steady even during hard times because we need necessities like soaps, food ingredients and toothpastes. In line with this, the company’s underlying sales grew by 10.5% year-on-year (YoY) in the first quarter of 2023 (Q1 2023), up from 7% in Q1 2022. This is after it reported a 9% growth for the full year 2022, up from 4.5% in 2021. In GAAP terms, its turnover grew even faster at 14.5% during the year.

Largely sustained margins

It is not as if its volume has not suffered, though. It is actually down, but only just, by 0.2% YoY in Q1 2023. But here’s the rub. Its underlying price growth of 10.7% YoY was strong enough to increase overall sales, indicating the company’s ability to pass on cost inflation to consumers. In other words, it has the capacity to sustain margins, for the most part at least.

We do not have the figures for operating margins for the latest quarter since it is a trading update. But in 2022, the underlying operating margin stood at 16.1% while the GAAP margin came in stronger at 17.9%. In underlying terms, it did decline in 2022, by 230bps, though, as gains from disposals were not factored into this calculation.

For the purpose of assessing the company’s business performance, the non-GAAP figure is the one to consider. Its decline, driven by cost inflation is disappointing but needs to be seen in line with a softening in margins seen for other consumer companies like Procter & Gamble ( PG ), Nestle (NSRGY), Colgate-Palmolive ( CL ) and The Kraft Heinz Co. ( KHC ) too.

Diversified markets

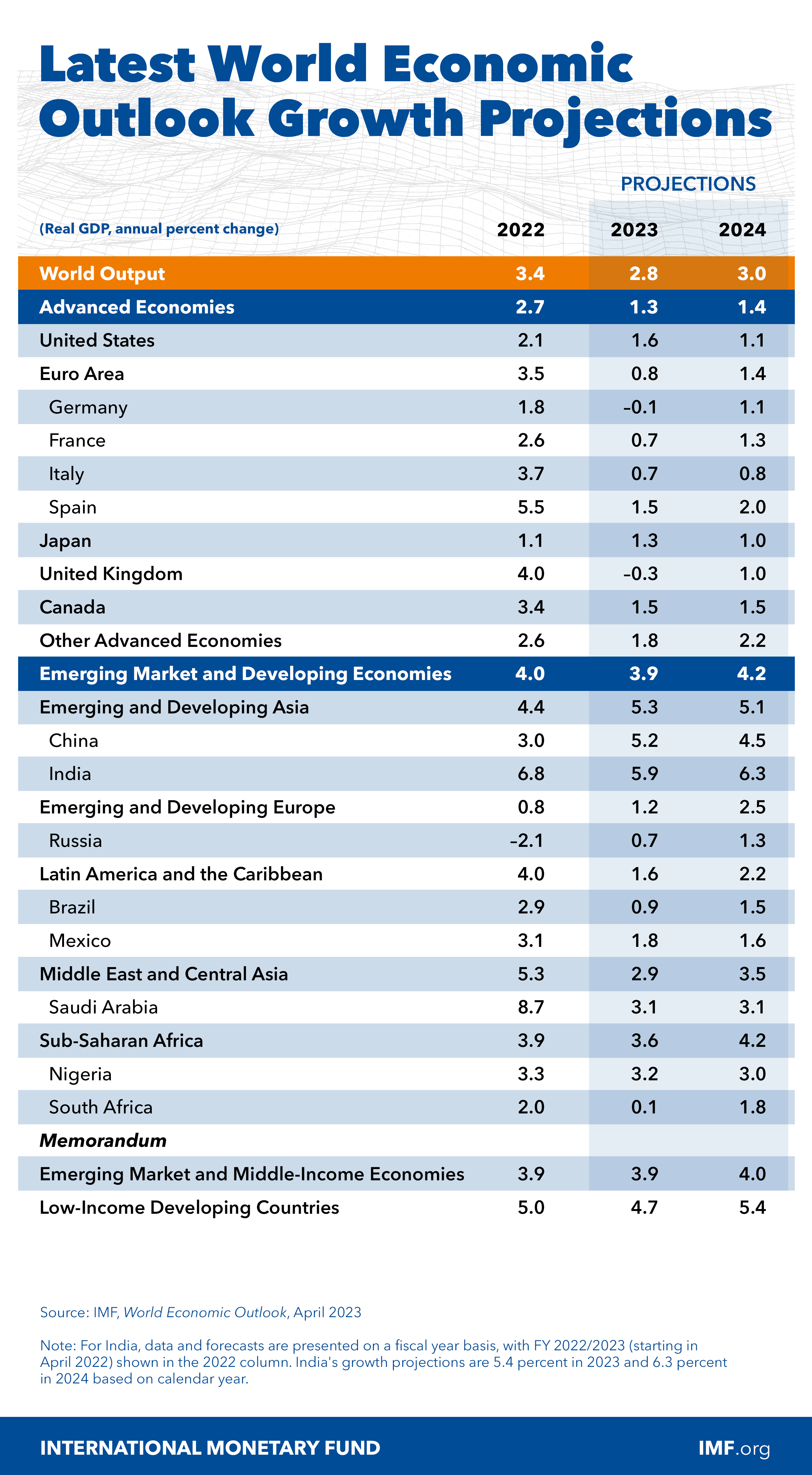

Its geographical diversification also goes in the company’s favour. Emerging markets contributed to almost 59% of its revenues in 2022, and as a group the IMF does not expect a recession, or even a slowdown there. Growth expectations for this set are at 3.9% in 2023, almost the same as a 4% rise seen last year, with big economies like China and India actually expected to grow at 5%+ rates during the year.

Developed economies, on the other hand, are expected to see softer growth, down from 2.7% last year to 1.3% this year. Even here, though, the fund only sees Germany and the UK going into recession. There are other forecasters who predict the same fate for the US , but not the fund. Whichever way we look at it though, the fact remains that there is expected to be a demand slowdown from this market. But it can be cushioned by the emerging markets.

{kind=link}

So far, so good

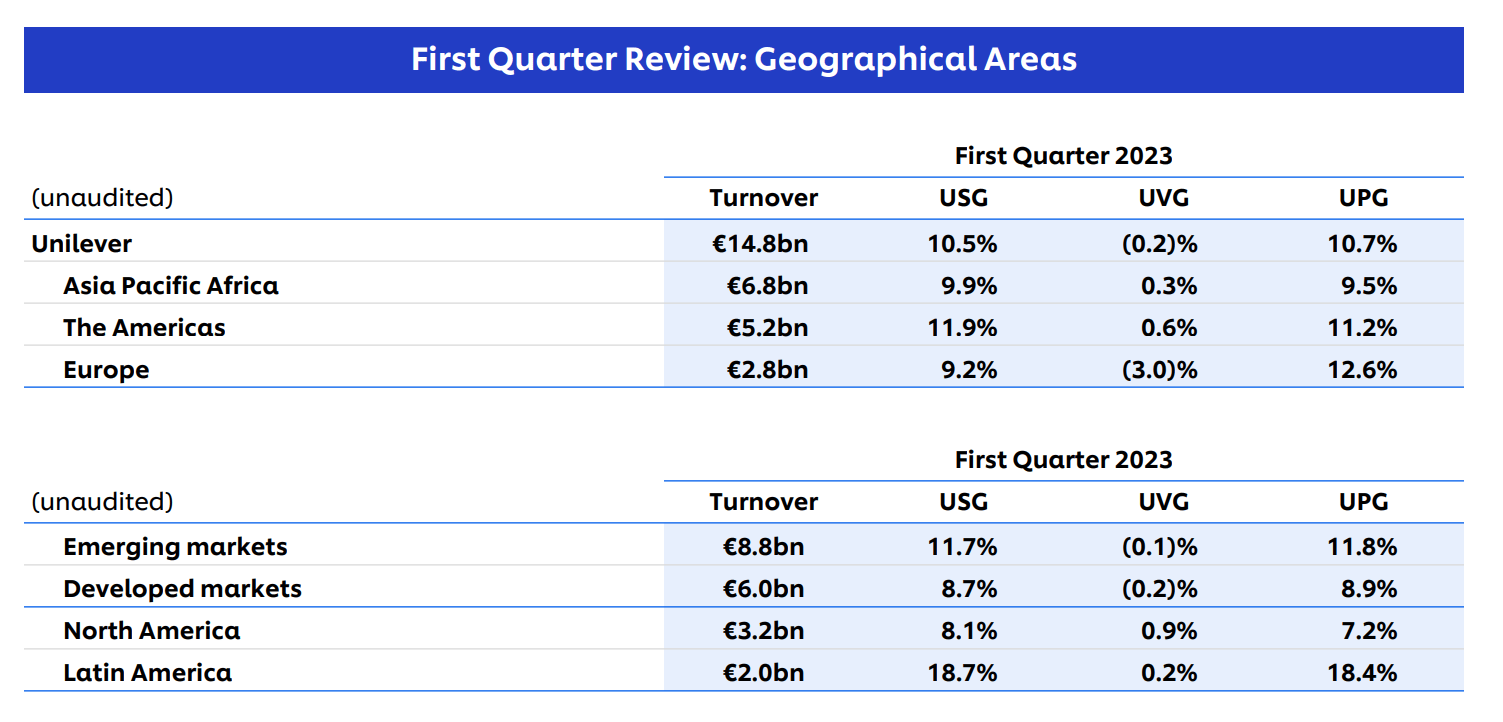

Further, numbers up to Q1 2023 do not show a slowdown. While emerging markets led underlying sales growth, with an increase of 11.7%, developed markets also grew by 8.7%.

Zoning in on North America reveals that the company actually saw 8.1% growth there. And this was not just driven by price, it also saw a volume increase of 0.9% (see page 5 of Q1 trading statement linked above). The volume increase is actually in stark contrast to the 0.2% decline seen in developed markets’ volumes. This is an even stronger indication that the slowdown is not visible yet. The only exception is Europe, where volumes have declined by 3%, even though sales stay robust otherwise.

Note: USG - underlying sales growth, UVG - underlying volume growth, UPG - underlying price growth (Source: Unilever)

{kind=link}

Positive outlook

In its outlook, Unilever says that it expects “underlying sales growth for the full year 2023 to be at least at the upper end of our multi-year range of 3 – 5%.”. Essentially, this means that growth will be at least 5%, if not higher. It sounds like a significant come-off from the figures seen until Q1 2023, but it does need to be seen in the context of the fact that over the past three years, its revenue has seen a compounded annual growth rate [CAGR] of 4.9% , which is a bit lower than what this year’s growth could be. Further, over the past five years, the revenue CAGR has been even lower at 2.3%.

Also, a slowing down in sales growth should be expected as inflation comes off. Recall that in the recent past, price growth has driven much of the sales rise. In fact, alluding to price rise, Unilever says “Underlying price growth will remain high in the first half and soften through the year.”. To me, this translates into another quarter of robust growth followed by a slowing down. That sales growth would slow down largely due to price disinflation is also indicated by the fact that it expects to sustain its operating margins at “at least” 16%.

Competitive valuations

The valuation picture is complex at first glance. It has a trailing twelve months [TTM] GAAP price-to-earnings (P/E) ratio of 17.3x is competitive compared to the 22.7x for the consumer staples sector. If we consider closely related stocks, it looks even more attractive. Here, I considered four related stocks mentioned earlier here, Proctor & Gamble, Nestle, Colgate Palmolive and Kraft Heinz. Turns out that UL has the lowest TTM P/E even among these, with the rest at at least 20x and CL with the highest figure at 36.6x.

Broadly, these numbers indicate that UL’s price can have some further upside. Further, if we consider the rising probability of recession, defensives can start looking far more attractive as such.

Consider the dividend

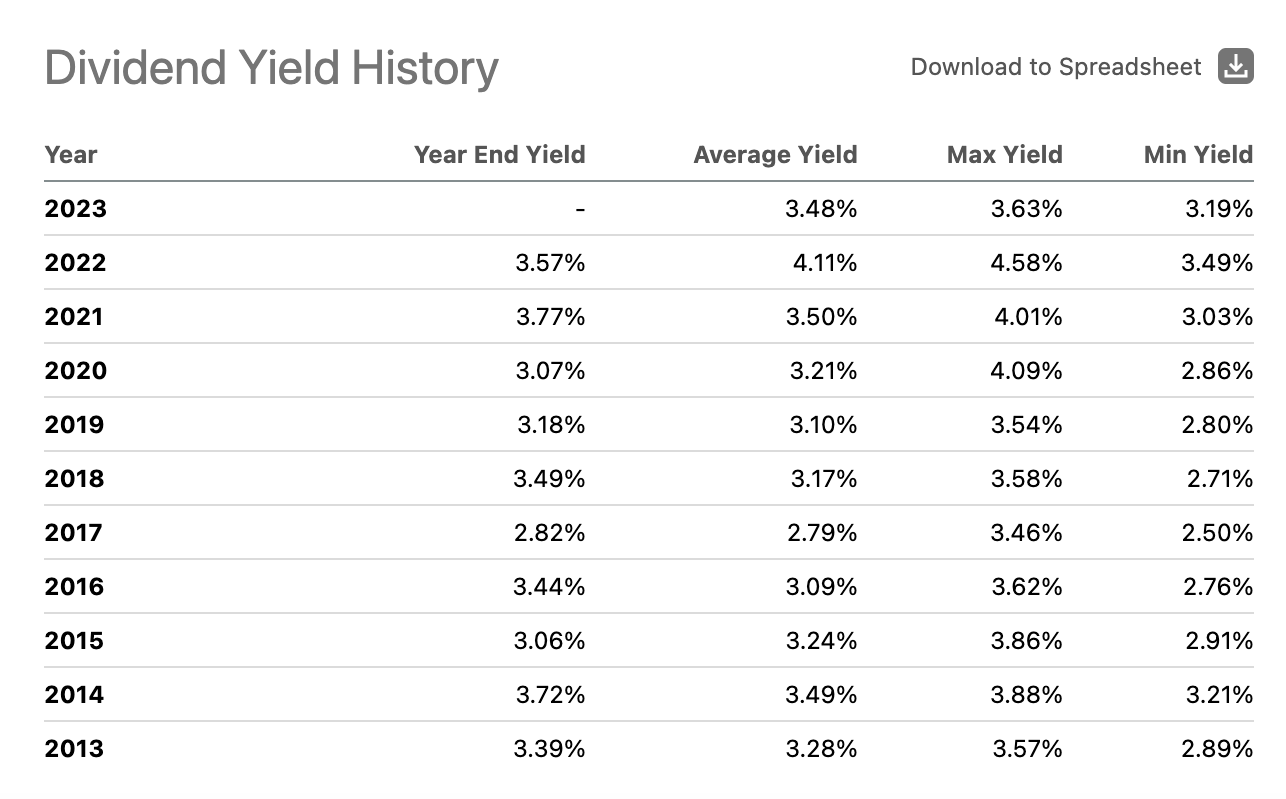

Next, there is something to be said for its consistency of dividend payouts. It has consistently paid them out for the past 13 years. In the present time of high inflation, its TTM dividend yield of 3.2% does not sound too high, but it is inflation beating at more regular times.

{kind=link}

What next?

There is no denying that 2023 is a year of uncertainty. Growth can slow down in developed markets going forward into the year. At this time, defensives that have a likelihood of giving both capital returns and paying dividends are a good idea. Unilever is one such.

The company’s performance is strong and its margins are expected to stay steady irrespective of where prices go next. It is also supported by a big presence in emerging markets that are expected to be relatively buoyant this year. Its long-term price performance leaves much to be desired, with flat performance over the past five years, making it strictly one for passive income investors. But in this year, things can continue to look good for it.

This article was submitted as part of Seeking Alpha’s Best Investment Idea For A Potential Recession competition, which runs through April 28. This competition is open to all users and contributors; click here to find out more and submit your article today!

For further details see:

Unilever: Defensive Investment In An Uncertain Year