KMB - Unilever: Delivers For Shareholders In A Difficult Period

2023-03-29 12:22:37 ET

Summary

- Unilever got a buy rating from us about a year back.

- We review the recent results and the stock performance.

- We run comparative valuations against its own history and peers and give you our verdict.

The Company

If you are one of the 3.4 billion people that use Unilever PLC (UL) products on a daily basis, you can skip this introduction.

{kind=link}

Unilever is a consumer goods global conglomerate, and one of the largest of its kind. Its product range comprises beauty & wellbeing, Personal Care, Home Care, Nutrition and Ice Cream. These five categories also form its reportable segments or business groups for financial results.

{kind=link}

The above business groups cover several popular brands. Of course, many identify the products with their brand name (and we are guilty of it too) and not the source of origin, so the following graphic may provide a "aha" moment to them.

{kind=link}

Our Prior Coverage

The stock hit our price target in half the expected time. March of last year is when we last wrote on it. It was among the cheapest in the consumer staples sector and we were impressed with its then recent financial results. Sure, the operating margins had declined, but the drop was minor considering the prevailing macro conditions. So in relative terms it got top marks from us. The forward estimates looked more than a tad unrealistic to meet in our opinion, however, the company was finally cheap enough to slap a buy rating on it.

Our contention is that when you are under 2.0X on a price to sales ratio, for a quality company like Unilever, you dramatically improve your odds of getting a 7-9% total return. This is not too hard when you are starting off at a 4% dividend yield, as you are doing in this case. Even the earnings yield is close to 6.7%, so you need very little nominal growth to hit your numbers. Unilever also uses relatively low leverage and that insulates it from any credit stress that we might see elsewhere in the levered consumer staples names.

Source: Unilever Hits The Sweet Spot

While we acknowledged the ongoing geopolitical risks and inflation headwinds, we had placed our bets that the monetary and fiscal policy would normalize sufficiently in 24 months to give the commodity prices some breathing room. This in turn would help the company deliver. That is exactly what happened, but in a shorter time frame. Our protagonist delivered and beat several of its peers.

What was particularly satisfying was that we had Hormel Foods Corporation ( HRL ) as a "Strong Sell" and Unilever outperformed by 45%. Unilever breached our $50 price target in 12 rather than 24 months. So today we review the current fundamentals in light of the macro conditions to see if this one is still a buy in our books.

2022 Results

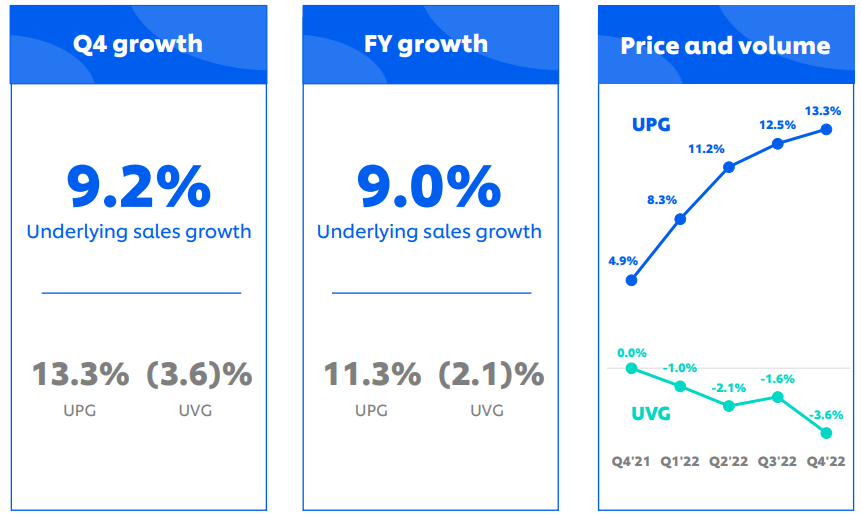

The sales growth doubled in 2022 compared to the previous year (9% vs 4.5%). While the 2021 number had volume growth make a reasonable contribution to the overall sales growth number, 2022 was a different story altogether.

2022 Annual Report

Q4-2021 was a precursor when volume growth came to a standstill. It was mostly downhill from there for each successive financial result.

{kind=link}

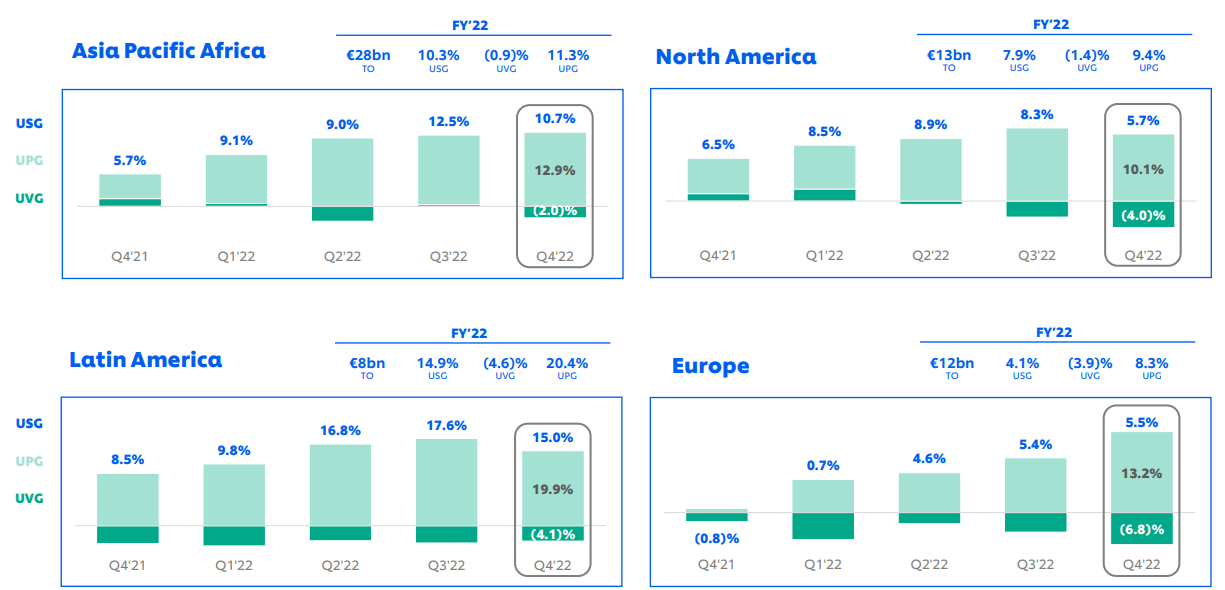

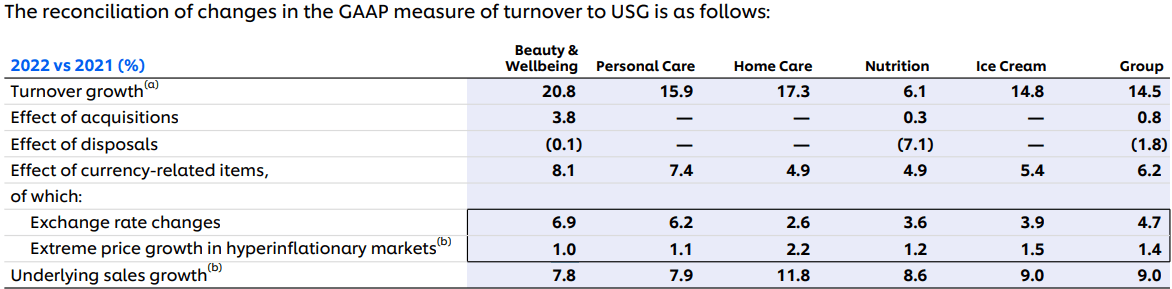

Not apparent in the above graphic, but the Beauty and Wellbeing segment actually had a slight volume growth of 0.3% year over year. However, in Q4 it had joined the rest in volume declines. Region wise, Latin America followed by Asia Pacific Africa led the overall growth numbers with Europe being the laggard.

{kind=link}

All the business groups were comfortably in the sales growth territory with Home Care leading the charge.

{kind=link}

While Unilever results reflected good pricing power, it was still not sufficient to stop the decline in the year over year gross and operating margins.

{kind=link}

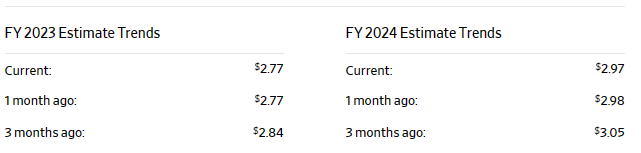

In our previous piece we had spoken about the unrealistic forward estimates for 2022. We did not think the $2.81 number would come to fruition. While Unilever did not hit that exact mark, it came pretty close at $2.77. At that time, the 2023 estimate was for $3.07 EPS. That, along with the 2024 estimate has been steadily declining.

{kind=link}

There is some downside risk to the 2024 numbers in a recession and one cannot ignore the volume trends which need to be reversed soon. The stock is not as cheap as it was last March, and the yield is lower due to price appreciation, despite the recent dividend hike . It is still better priced than it has been for the better part of the last decade.

Of course most of the last decade did not have the interest rates we have today. So by default we would expect a lower valuation and multiple. At present the upside is muted, though one could argue it is cheap at 17X earnings especially relative, to many consumer staples stocks including Clorox ( CLX ) at 34X, Procter & Gamble ( PG ) at 25X, and Kimberly-Clark ( KMB ) at 22X. Generally the relative argument has only held up if you try and do a paired trade. In a generalized market slide, both sets of stocks, cheap and expensive will fall. At present we have to dial back our enthusiasm and we are downgrading this to a Hold/Neutral.

For further details see:

Unilever: Delivers For Shareholders In A Difficult Period