UL - Unilever: Higher Quality Growth Needed

2023-11-01 05:59:11 ET

Summary

- Unilever stock hasn't risen much over the last 10 years, and its underlying EPS has been stagnant in the past few years.

- With a new CEO, Unilever plans to focus more on its top brands and invest more in innovation to help with higher quality growth that ideally has higher volumes.

- With the odds of an economic slowdown elevated, there might be reason to be cautious on the stock before seeing how the new CEO strategy works.

- I rate the stock a Hold, meaning it might be better to be on the sidelines for now.

Unilever PLC ( UL ) is a leading consumer staple.

In terms of performance, Unilever's 10 year performance hasn't been all that great as the stock price is only modestly higher than where it was 10 years ago.

When factoring in the dividends, Unilever's total return in the last 10 years has been 59.68% as of October 30.

With a 10 year U.S. Treasury bond yielding 4.88% as of October 30, that specific U.S. government bond would generate a total return of 48.8%, which is actually pretty close to Unilever's total return over the last 10 years.

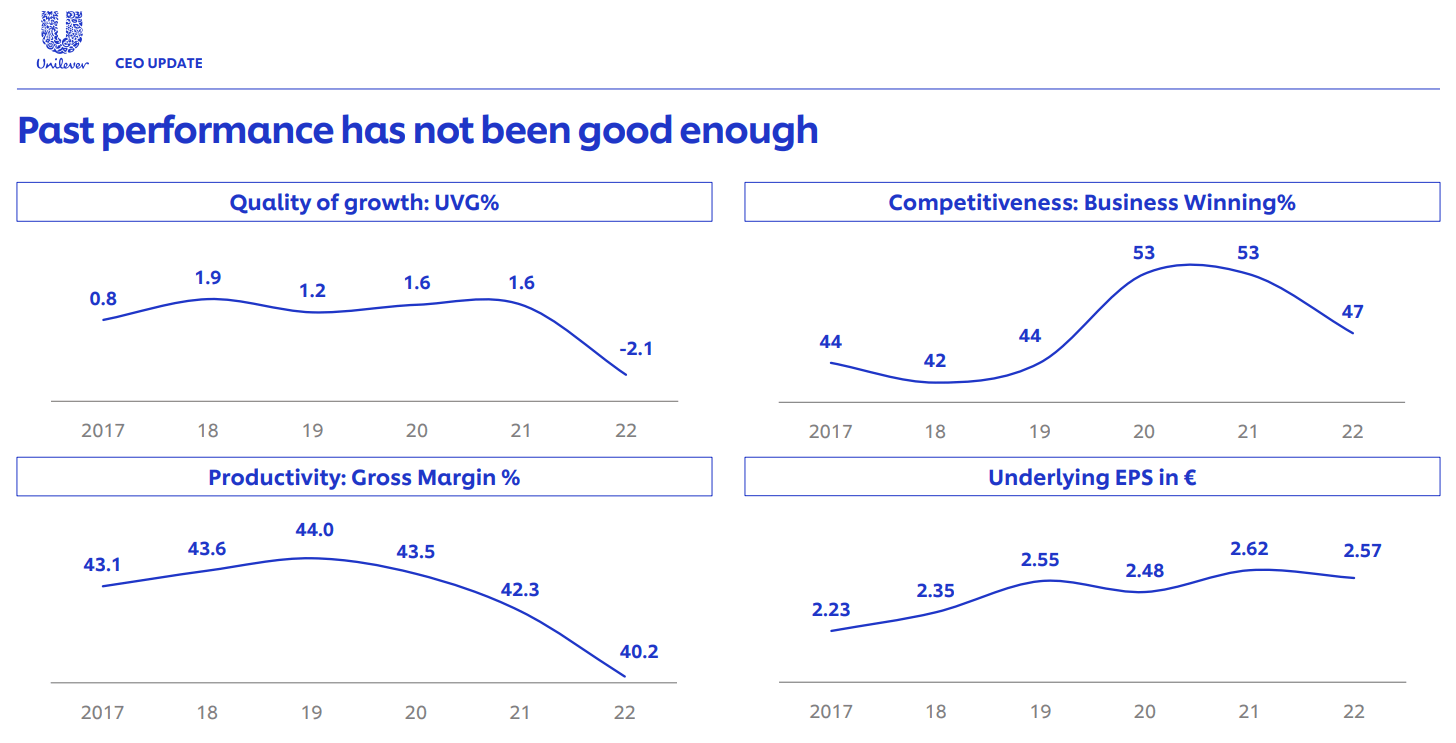

One reason for the lagging stock performance is that the company's quality of growth hasn't been all that great in recent years.

Although underlying EPS in euros increased from €2.23 in 2017 to €2.57 in 2022, volume decreased by 2.1% in 2022. Underlying EPS growth in recent years hasn't increased much and gross margin shrank to 40.2% in 2022 from 42.3% in 2021.

Unilever Investor Presentation

{kind=link}

While 2022 was a special case as the war in Ukraine increased supply costs that shrank margins, 2023 hasn't been a bounce back year in terms of quality of growth. In 2023, overall volume decreased year over year 0.2% in Q1 2023, 0.3% in Q2 2023, and 0.6% in Q3 2023.

With that being said, Unilever in the next 5 years is certainly going to be a different company than it was in the last 5 years. Unilever also has a new CEO in Hein Schumacher who officially became the CEO in July 1, 2023 .

Q3 2023

In terms of Q3 2023, the quarter is the first under Schumacher's leadership as CEO.

For the third quarter, Unilever's turnover decreased 3.8% year over year to €15.2bn.

Meanwhile, underlying sales growth was 5.2%, with 5.8% due to pricing and -0.6% due to volume.

One reason for the difference between turnover and underlying sales growth was the sale of a swab brand . Unilever also faced currency headwinds which had a negative 8% impact.

For the quarter, price growth moderated and Unilever had positive volume growth in three business groups, Beauty & Wellbeing, Personal Care and Home Care.

Given headwinds, the company's Nutrition and Ice Cream businesses had negative volume growth, however.

Year to date, Unilever has had underlying sales growth of 7.7%, with 8.1% due to pricing and -0.4% due to volume.

For 2023, Unilever has underlying sales growth guidance of over 5%. The company expects increased levels of investment in BMI, R&D, and capex. Management also expects price growth to continue to moderate throughout the year.

Volume Growth Lagging

In recent quarters, Unilever has had to rely on price increases for sales growth rather than volume increases indicating that the quality of growth remains not that great.

Unilever Investor Presentation

Not having volume increase indicates that Unilever isn't winning that many new customers or market share. While increasing prices help with sales, it arguably isn't the most sustainable method as eventually some customers will switch to cheaper brands. In terms of the past few years, Unilever's volume growth has also been behind its peers .

In the near term, Unilever's results could face headwinds if there is a recession or economic slowdown. China is one of Unilever's largest markets and the economy is slowing there. The U.S. economy could also slow in the future given the Federal Reserve's multiple interest rate hikes in the past year and a half.

If there is a recession or an economic slowdown, Unilever may have a difficult time raising prices as much, and its volume could decline in the near term.

If there is a severe enough slowdown, Unilever might not meet its EPS estimates.

As of October 30, analysts expect the company to earn $2.77 per share for the fiscal period ending December 2023, and $2.95 per share for the fiscal period ending December 2024. As of October 30, that gives Unilever a forward PE ratio of 16.72 for 2023 and 15.69 for 2024.

Unilever's expected earnings more than cover the annual dividend of $1.82 per share, which as of October 30 is a dividend yield of 3.92%, however.

Longer Term

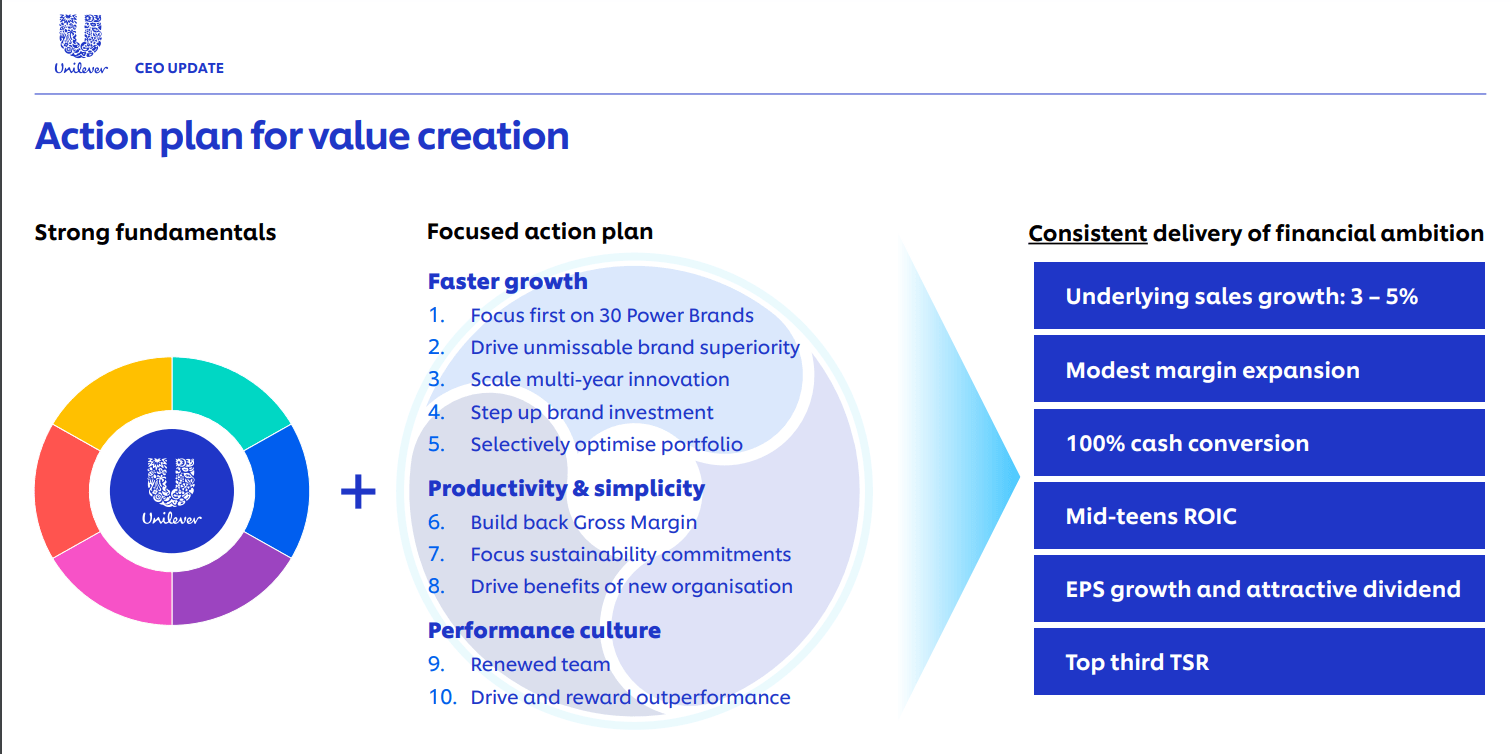

While 80% of the company's business is either number one or number two in their category positions, Hein Schumacher wants to increase the company's competitiveness so that hopefully the quality of its growth improves.

While Unilever is targeting a relatively modest underlying sales growth of 3-5% , the company will try to improve its volume growth and also try to increase gross margins. If that happens and management does well on margins, EPS growth could be faster than 3-5% given the potential for margin leverage.

Unilever Investor Presentation

{kind=link}

To increase competitiveness, the new CEO plans on focusing on the company's 30 Power brands which account for around 70% of 2023 turnover. According to management, the company's top 30 brands are growing 7.5% versus the company's overall growth of 5.2%.

Unilever also hopes to consistently grow R&D investment and prioritize differentiated technologies. The company hopes to prioritize platforms with bigger but few projects, some of which are multi-year.

Better M&A could also help if done correctly. Since 2015, Unilever has rotated 20% of its portfolio and acquired 22 businesses but not all acquisitions have met expectations. For the future, Unilever plans on further pruning and to focus on value-accretive bolt-on acquisitions.

To improve gross margin, management hopes to improve its mix through premiumization, realizing volume leverage, and realizing more productivity.

While many of Unilever's brands are number one or number two in their market positions, demand for them could nevertheless weaken if economic conditions slow too much as consumers switch to less expensive alternatives.

Although the stock could go higher given its fair valuation and its potential, macroeconomic headwinds could make it more difficult in the near term. As such, I rate Unilever a 'hold' as it might be better to be in a 5 year U.S. Treasury bond until the company can show it can consistently achieve high quality growth.

For further details see:

Unilever: Higher Quality Growth Needed