UNLYF - Unilever: Margin Expansion Likely Valuations Attractive

2023-07-23 21:37:32 ET

Summary

- Unilever's stock has fallen by 5.5% since April, trailing the S&P 500 index. However, this can change as the company expects improvements in its underlying operating margin for 2023.

- Earnings per share growth is also expected to show healthy growth, which bodes well for its price at a time when its market valuations are already competitive.

- Unilever's dividends are consistent and add to total returns, making the stock attractive. Additionally, in an uncertain macro economy, it makes a good defensive to have in the portfolio.

When I wrote about the British-Dutch consumer goods giant Unilever ( UL ) in April this year, its performance was far superior to the S&P 500 ( SP500 ), which had actually been on a declining curve. Cut to now, and the stock is actually trailing the index marginally. In fact, the stock has fallen by 5.5% since the time I wrote while the index is up by almost 9% in that time.

I had given a Buy rating to the stock at the time, based on its strong defensive qualities in a time of a slowdown, which was also cushioned by its large emerging markets presence. Its outlook wasn’t too bad either and its valuations were competitive. In the run-up to its earnings release on July 25, here I look at what, if anything, has changed for Unilever, and what that means for the stock going forward.

Sales growth to stay strong

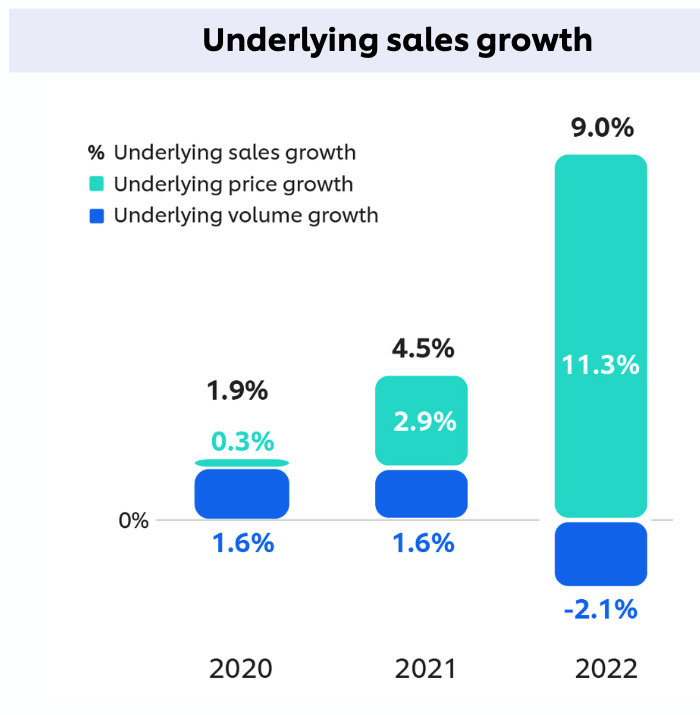

The sales figures are encouraging up to Q1 2023, where the company saw a 10.5% year-on-year (YoY) increase in underlying sales growth [USG]. This was mostly due to a huge increase in underlying price growth [UPG] and despite a small correction in underlying volume growth [UVG], continuing the trend from last year (see chart below).

{kind=link}

I do believe, however, that growth figures can soften in Q2 2023, as cost pressures are coming off. Producer price index [PPI] based inflation in some of its key markets like China and Europe have actually tripped into deflationary territory recently. This in turn means that Unilever is likely to pass on any cost increases at a slower rate. Further, there’s a base effect to consider. The company saw a higher 8.8% USG in Q2 2022, up compared to a 7.3% increase in Q1 2022. This too could affect sales growth downwards.

However, overall sales growth for the first half of 2023 (H1 2023) is still likely to be in excess of the 3-5% USG forecast for the full year 2023.

Optimism on operating margins

In 2022, Unilever reported an underlying operating margin of 16.1% . Its outlook for 2023, however, suggests that it expects improvements there. It pencils in an underlying operating margin of at least 16% for H1 2023, with a “modest improvement” expected for the full year.

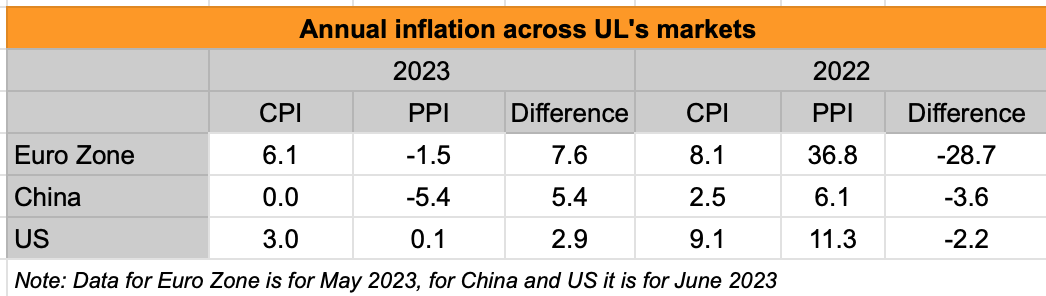

However, in the current environment, I believe there’s a case for margin expansion sooner going by the gap in trends between producer and consumer prices. There’s no denying consumer prices have come off too, but there’s a big difference from last year. Across Unilever’s markets, which include the US besides China and the EU, last year at this time, PPI inflation was much higher than consumer price inflation. But the tables have turned now (see table below).

{kind=link}

This is encouraging for companies’ margins, especially those like UL, whose growth in recent times has been derived entirely from price increases. Even if the rate of price rise slows down for its products and volumes continue to decline, its profits can still grow as long as costs fall faster. I’ll look out, particularly, for the update on margins in its upcoming results.

EPS growth seen in 2023

In any case, analysts are positive about the company’s earnings per share [EPS] for the year, with growth of 7% expected in 2023. This is a significant softening from the 21.2% rise seen last year, but it is still slightly ahead of the compounded average growth rate [CAGR] of 6.9% over the past five years.

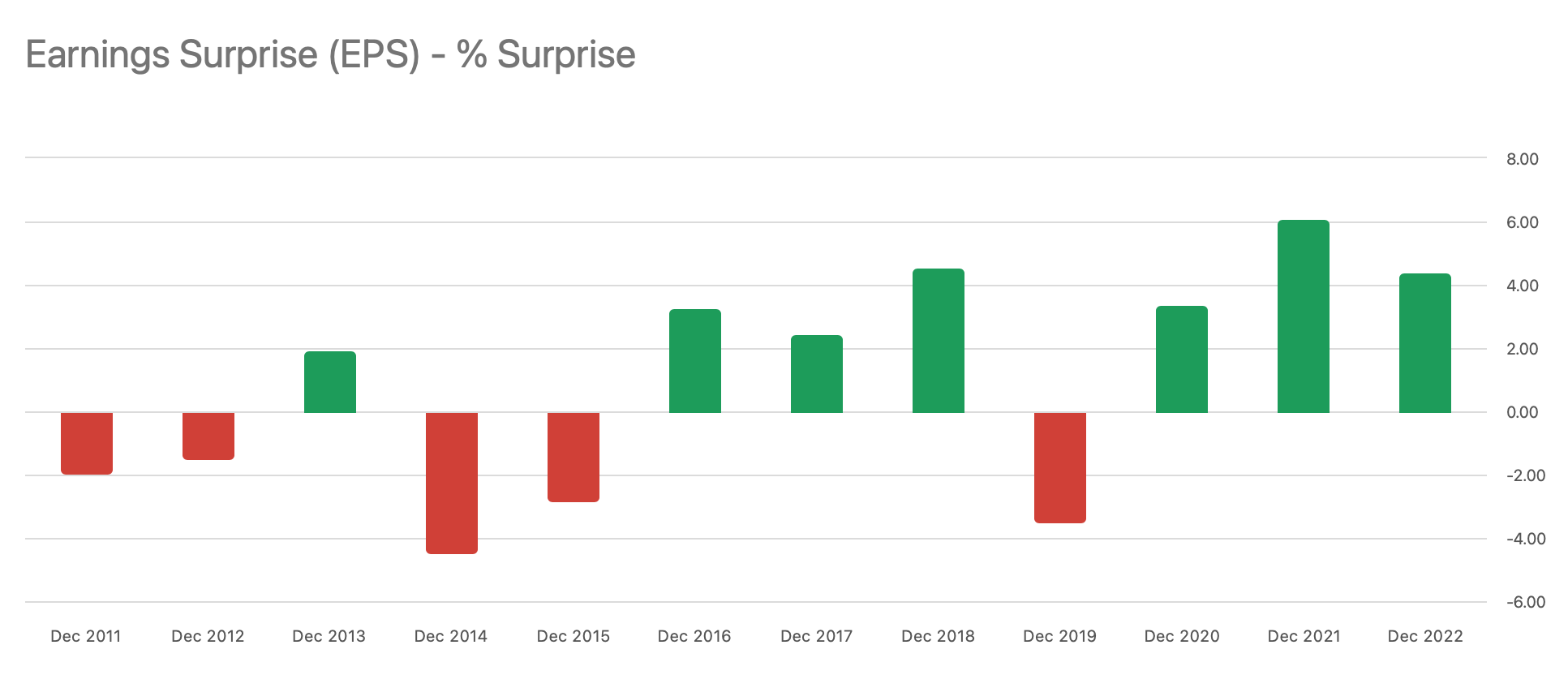

It might even be higher, considering that earnings have surprised on the upside for seven of the last 10 years (see table below). This translates into a 1.5% average upside surprise over the past decade. Based on the margin discussion above, there’s a particular possibility of a surprise this year.

{kind=link}

Market valuations

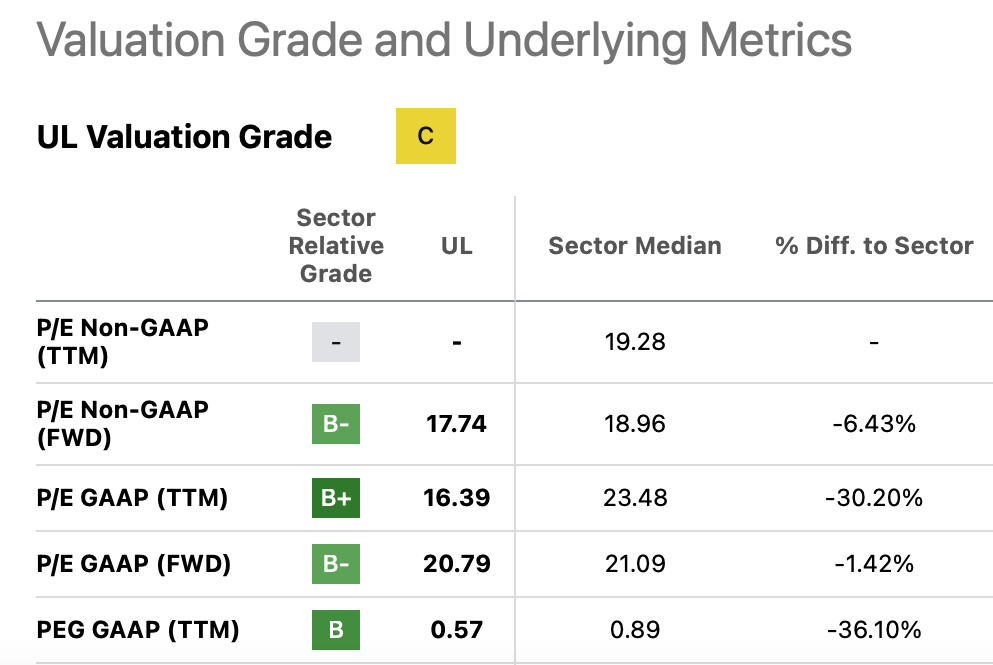

The EPS estimates indicate a forward non-GAAP price-to-earnings (P/E) ratio of 17.7x. This compares favourably to the P/E for the consumer staples sector at 20x. In fact, its other market valuations like the forward GAAP and the trailing twelve months [TTM] ratios are also lower than the sector (see chart below). I think there’s a 15% upside or so to the stock right now. And it’s not inconceivable considering that it was trading at those levels a couple of years ago.

{kind=link}

Dividends add up

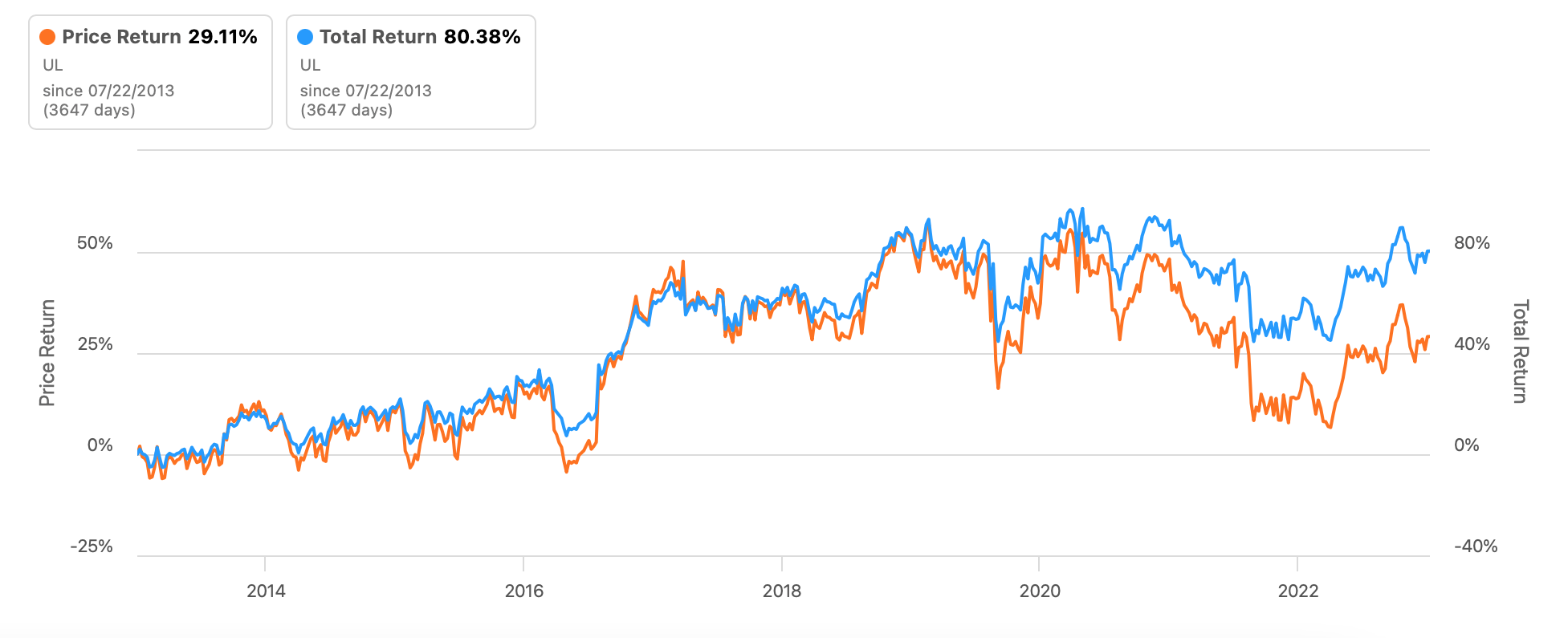

Finally, UL’s dividends are worth considering. As a predictable, defensive stock, it offers few real surprises. This shows up in its relatively muted market movements, with a beta value of 0.13 over the last 24 months, reflecting it is far less moved than the market as such. Its 10-year price returns reflect this as well, at just 29%. But add in the dividends, and the total returns jump to over 80% (see chart below).

{kind=link}

This is despite the fact that its dividend yield is not the highest, with the TTM figure at 3.4% and the forward figure at 3.6%. But there are two points to note here. One, both numbers are higher than the sector average by around 1 percentage point anyway. And second, what the company lacks in absolute dividend amounts, it makes up for in consistency. The numbers available as far back as 1999 show that it has not skipped a single year in paying them.

What next?

If I was positive about the UL stock earlier, I’m even more so now. It’s not a growth investor’s dream, by a long shot, with low single-digit USG expected in 2023. But it has a lot going for it. Its dividends are consistent and add up nicely to the total returns. They can also be depended on, going by the company’s long history of paying them.

Moreover, with EPS expected to grow above the 5-year average rate in 2023 anyway, if not higher, and the possibility of margin expansion, is price can rise too. I think we should see signs of positivity as soon as its next earnings release this week.

With competitive market valuations, the price already looks attractive. In fact, the stock is particularly attractive at an uncertain time for the global macro economy. There’s a slowdown in place in the US and Europe and China’s growth is looking less buoyant than expected. While the broader market is doing well now, if the slowdown continues to deepen, market uncertainty is a possibility. This is a good time to consider buying Unilever.

For further details see:

Unilever: Margin Expansion Likely, Valuations Attractive