UL - Unilever: Not Appealing In Spite Of Decent Dividend Yield

2023-09-23 05:02:16 ET

Summary

- Unilever has been able to maintain performance despite high inflation, but its competitiveness is deteriorating due to price increases.

- The company's free cash flow generation is reverting to a level of about €5Bn, limiting its ability to spend on buybacks.

- Household budgets will remain under pressure due to inflation, affecting Unilever's bottom line.

- Against this backdrop, management intends to raise spending on marketing, R&D, and capex.

- in spite of Unilever being a stable company with a decent dividend yield, bonds are more appealing.

In a prolonged period of high inflation Unilever ( UL , UNLYF) has been able to maintain performance, but now the price increases are starting to show in a deteriorating competitiveness. As inflation has not been contained yet, household budgets will remain under pressure, thereby affecting the bottom line. Given the macroeconomic environment and the plans of management to increase spending, the alternative of bonds is more appealing, in spite of Unilever being a stable company with a decent dividend yield.

Pricing power

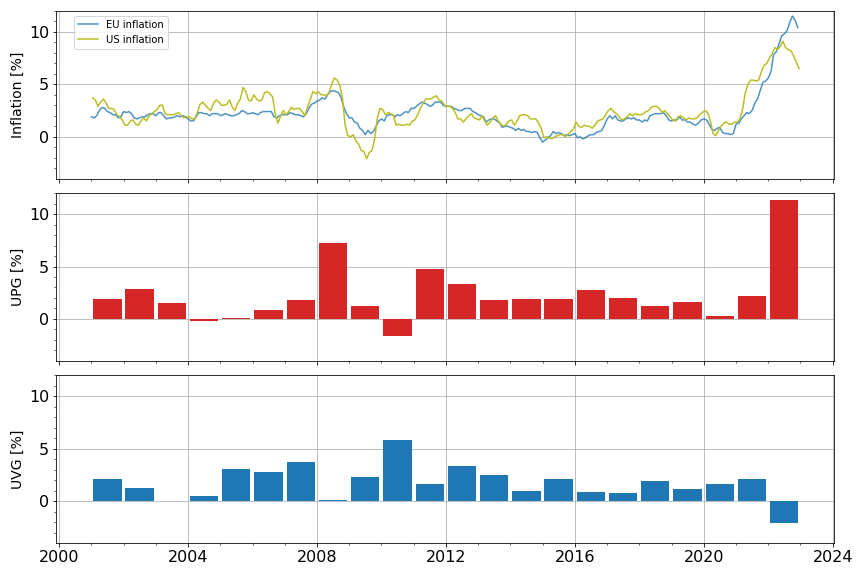

In the past, Unilever has proven to navigate price swings quite well. Last year, this is exactly what the company did again, and price increases boosted turnover to new highs. Whereas turnover hovered around €50Bn over the last decade, in 2022 this number increased to €60Bn. In no small part, this number was achieved by price increases of more than 11%, see figure 1.

Figure 1 - Unilever underlying price and volume growth against US and EU inflation (ec.europa.eu/eurostat, bls.gov/cpi, unilever.com; chart by author)

{kind=link}

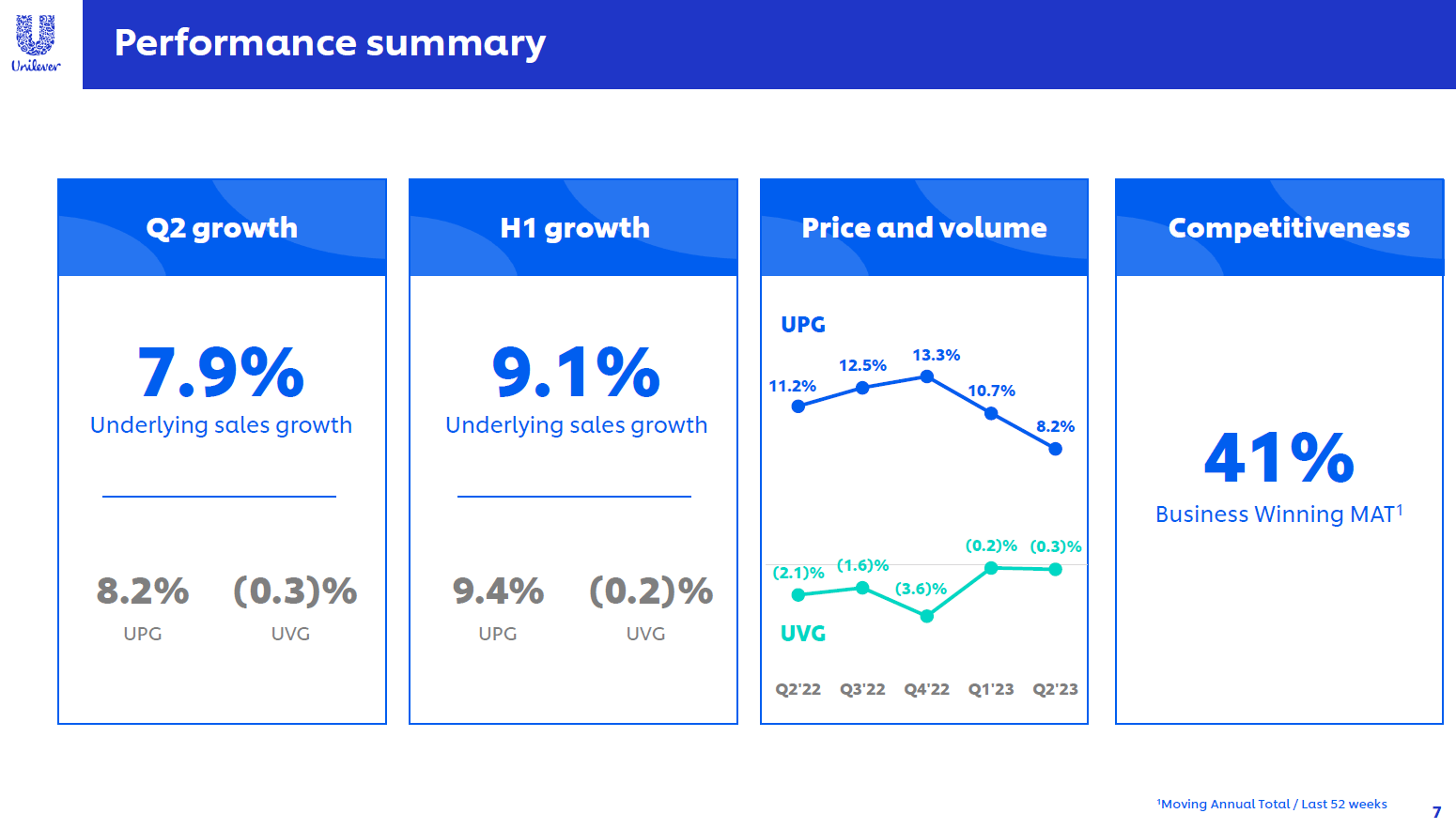

Raising prices comes at a penalty, meaning volume growth turned negative. Even so, the prices were raised to such an extent that this more than offset the decline in volumes. In other words, underlying sales growth remained positive. This performance continued in 1H23, see figure 2.

Figure 2 - Unilever 1H23 performance summary (unilever.com)

{kind=link}

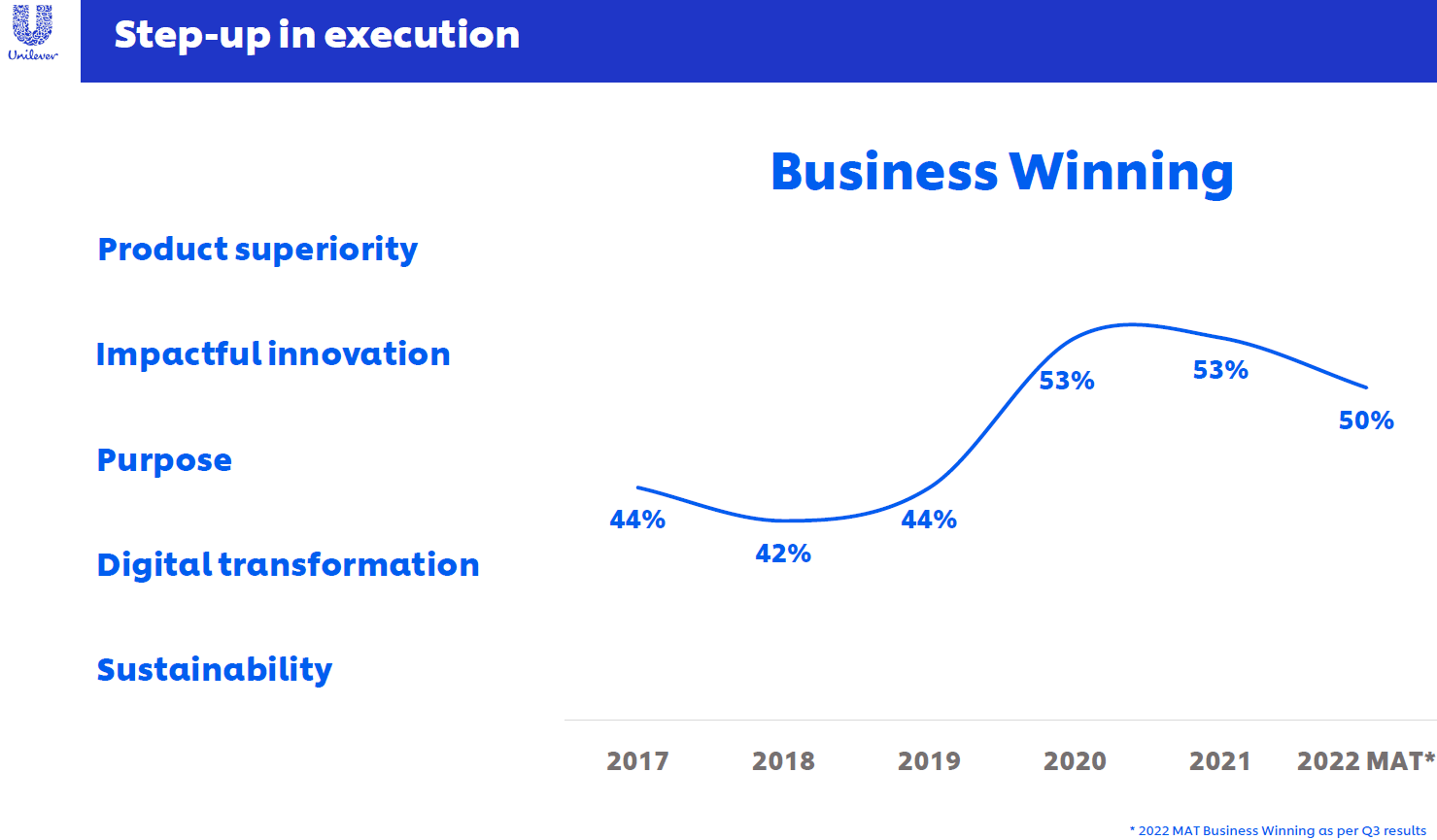

While turnover and prices showed growth, the competitiveness has reduced significantly. Unilever targets a Business Winning Moving Annual Total of 50%. Clearly, this figure was not achieved, as it came in at 41%. For readers interested in the calculations of this number, the concept of Business Winning MAT is explained in detail under this link . To put the current number in perspective, the annual Business Winning values since 2017 are visualized in figure 3.

Figure 3 - Unilever 5-year history of Business Winning MAT, Unilever Investor Event 2022 (unilever.com)

{kind=link}

As Business Winning is a synonym for competitiveness, a number below 50% is a reason for concern. This was acknowledged by management at the latest earnings call , yet concrete answers were not given. One of the questions asked by analysts sums the mood quite well:

I'm kind of losing quote now of how many quarters we're here talking about it's bad but we're doing X, Y, Z, then it should get better. How confident are you that this is actually the low point and we should be getting back to good growth from here?

Flow reversal

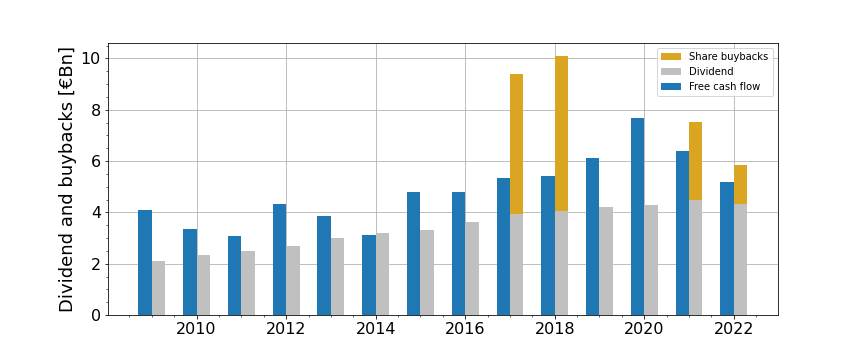

Previously covering Unilever, it was forecasted free cash flow growth would slow down or even reverse. The rationale was quite simple as income tax and capex simply could not go lower meaning these would take a bigger bite out of cash flow from operations and hence reduce free cash flow. Figure 4 shows FCF declined from a high of €7.6Bn in 2020 to approximately €5.2Bn last year.

Figure 4 – Development of free cash flow, AR22 (unilever.com)

Merely looking at this figure, the wrong conclusion may be drawn that FCF is not holding up since it dropped by more than 30%. Taking the long term view, however, 2022 free cash flow generation aligns better with long term performance. For this reason, my base case is the company will generate approximately €5Bn in FCF annually. This estimate is supported by the €2.5Bn FCF achieved in 1H23.

Shareholder returns

The distributions to shareholders have been a source of debate in the recent history of Unilever. For example, readers may remember the hostile takeover bid of 3G in 2017. While this bid failed, UL management was prompted to distribute significant amounts of cash through share buybacks. The size of these buybacks in relation to the dividend and free cash flow is visualized in figure 5.

Figure 5 - Unilever FCF and shareholder distributions (unilever.com; chart by author)

{kind=link}

After the storm subsided and everything went back to normal, share buybacks were forgotten again until Nelson Peltz built a stake in the company and obtained a seat in the board. While Peltz did a tremendous job at P&G (PG), the effect at Unilever has been limited so far.

The current quarterly dividend per share has remained constant at a level of €0.4268 since Q4 2020 and the amount of buybacks has been limited. In all honesty it must be said net debt doubled after 2017 meaning a repetition of the aggressive buybacks is not possible as the balance sheet was more levered already. Also, in recent years inflation has been out of control, meaning the company preferred continuity to distributions.

Going forward, buybacks may be expected buybacks to remain limited in magnitude. The reason is free cash flow is mainly used to fund the dividend and on top of this the company intends to increase spending on R&D, marketing and capex. Even though returns will be mainly in the form of dividends, this may not be a bad thing as recent history showed buybacks did little to prop up the share price.

Since the move of Unilever to Britain, the dividend is not subjected to withholding tax anymore. It also means we are now talking about a British company. In this context, it is worth to note, 1-year gilts currently trade below par at a yield of 5% and 1-year Treasuries trade above 5%. Although Unilever is seen as a stable company with a decent yield, the alternative of bonds is more appealing to park ones cash for the coming year. Especially as shareholder distributions may not grow, the alternative of bonds is more appealing. It can even be argued Unilever currently is no match for bonds.

Premium risk

Companies such as Ahold Delhaize (ADRNY) have been lambasted for both increasing prices when inflation was high and now not reducing prices fast enough as inflation is falling. As a response, and to maintain earnings, supermarkets have started to push their own brands which are both cheaper and commend a higher margin.

Therefore, retailers are now essentially competing with Unilever and its competitors. So, essentially, the candle is burning on both ends. Volume has been under pressure due to high inflation and to maintain steady income prices were raised. As this means pressure on volume will continue, my base case is pricing will need to do the heavy lifting to maintain sales growth. Obviously, this may have a detrimental effect on volume, and so the vicious circle starts. Unilever needs to navigate through this dynamic, as highlighted by CFO Pitkethly at the 1H23 earnings call :

There is a trend of value as consumers look to balance the household budget. This can be seen in the growth of unbranded loose tea in India and the growth of very low-priced laundry brands in Brazil. These are very low profitability segments where we choose either not to play or to play very selectively. Therefore, we look to limit our losses while maintaining our investment levels so that we are well placed to capture the return to our brands as economies improve.

This comment also puts attention on another issue. CEO Hein Schumacher has been very clear about the focus on Unilever’s sustainability agenda. In this respect, it seems Schumacher has been listening carefully to his fellow countryman and former Unilever CEO Paul Polman. Polman, who describes himself as ‘ business leader, climate and equalities campaigner ’, was CEO of Unilever from 2002-2018.

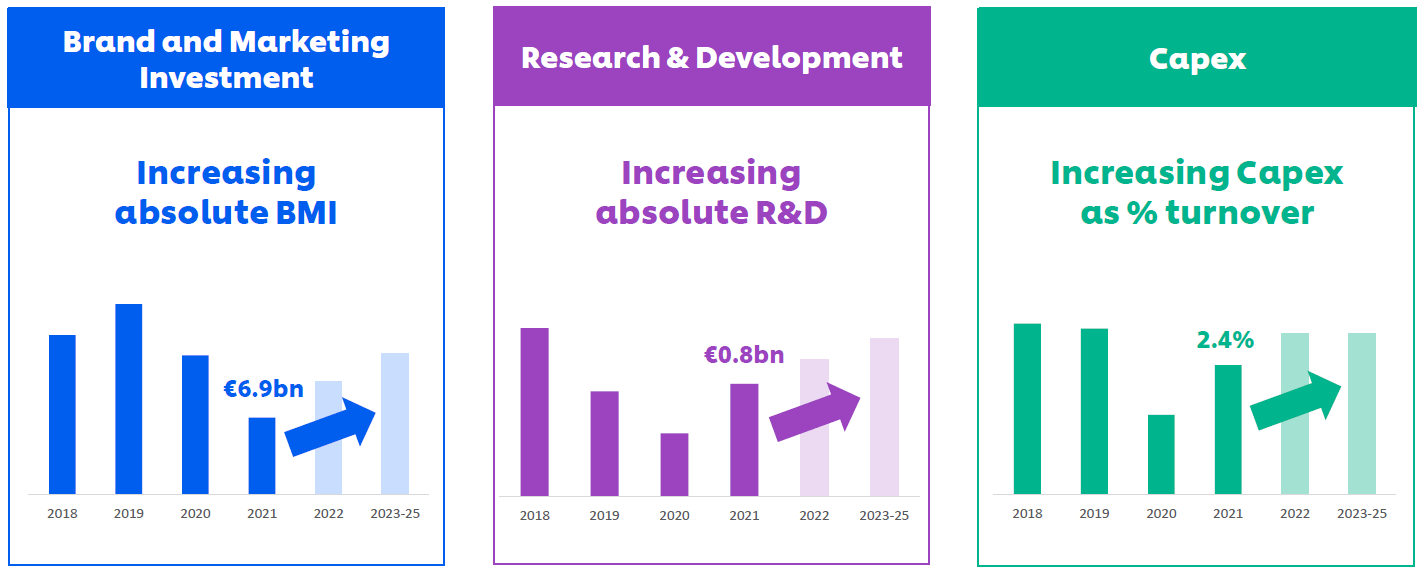

Figure 6 shows the company will increase investments in the coming years. These investments are required to achieve growth, but also to execute a transition to more sustainable products. While no doubt these investments are required, the issue is it will not pay dividends in the short term. And that is meant both literally and figuratively.

Figure 6 - Investments, Unilever Investor Event 2022 (unilever.com)

{kind=link}

After all, the comments made by Pitkethly highlight this, but more important, products that are biological, organic, sustainable or whatever name it is given, are generally priced at a premium.

Moreover, sustainable products require more research but also a fair amount of marketing to persuade consumers to pay for this premium. As household budgets are under pressure, and Unilever is booking the majority of turnover in emerging markets, the question becomes to which extend the sustainability of its products can be monetized. Moreover, consumers willing to pay this premium exist, but do not necessarily buy Unilever’s products:

We've also seen growth of the premium segment in U.S. Personal Care categories such as deodorants and skin cleansing. This is a price segment with an average index of between 140 and 200, where we are underrepresented today. This super premium opportunity shows the somewhat bipolar nature of the market just now, with both value and super premium segments growing at the same time.

Tying these comments to the previous highlighted remarks, the company is losing market share in emerging markets to low-priced laundry brands, for example, while it can't fully capture the premium opportunity in developed markets. Summarizing, the company appears to be stuck in the middle.

Conclusion

In a prolonged period of high inflation, Unilever has been able to maintain performance, but now the price increases are starting to show in a deteriorating competitiveness. While cash flow from operations is maintained at a rather constant level, free cash flow generation is reverting to a level of about €5Bn. This number means the dividend is covered, but little extra can be spend on buybacks, save for other management actions.

As inflation has not been contained yet, household budgets will remain under pressure, thereby affecting the bottom line of Unilever. Against this backdrop, the management team intends to raise spending on marketing, R&D and capex. This implies profit will likely be under pressure in the short term until this investment start to pay-off.

Given the macroeconomic environment and the plans of management combined with a deteriorating competitiveness, the alternative of bonds is more appealing in spite of Unilever being a stable company with a decent dividend yield.

For further details see:

Unilever: Not Appealing In Spite Of Decent Dividend Yield