UL - Unilever: Pricing Drives Growth And Sales Volumes Improve Fairly Valued

2023-05-02 04:45:43 ET

Summary

- Unilever's core brands continue to be a guarantee.

- Buybacks and high dividends reward shareholders even in difficult times.

- High inflation still greatly affects the company's costs, which is why it is forced to continually raise prices.

Unilever's ( UL ) Q1 2023 was positive overall, as a substantial increase in selling prices was followed by a rather marginal reduction in volumes. According to the words of CEO Alan Jope , elasticity of demand performed better than expected, in fact sales volumes decreased less than in the past. Let's see in detail what this means.

Comment on Q1 2023

Before commenting on the results obtained , I think it is useful to show the meaning of the acronyms most frequently used by the company in its quarterly report, so as to make the reading more understandable.

- USG (underlying sales growth)

- UVG (underlying volume growth)

- UPG (underlying price growth)

The difference between underlying sales and net revenues lies in the fact that the former attempts to reflect business growth more accurately by excluding certain components of a nonrecurring nature. For example, excluding the effects of acquisitions, divestitures, and movements in the exchange rate. That said, here are the highlights of this quarterly report.

{kind=link}

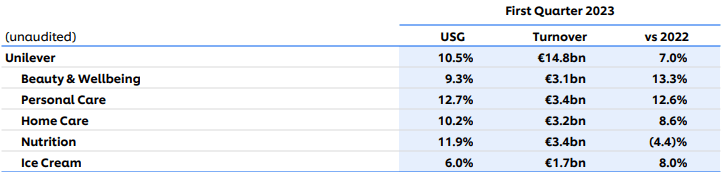

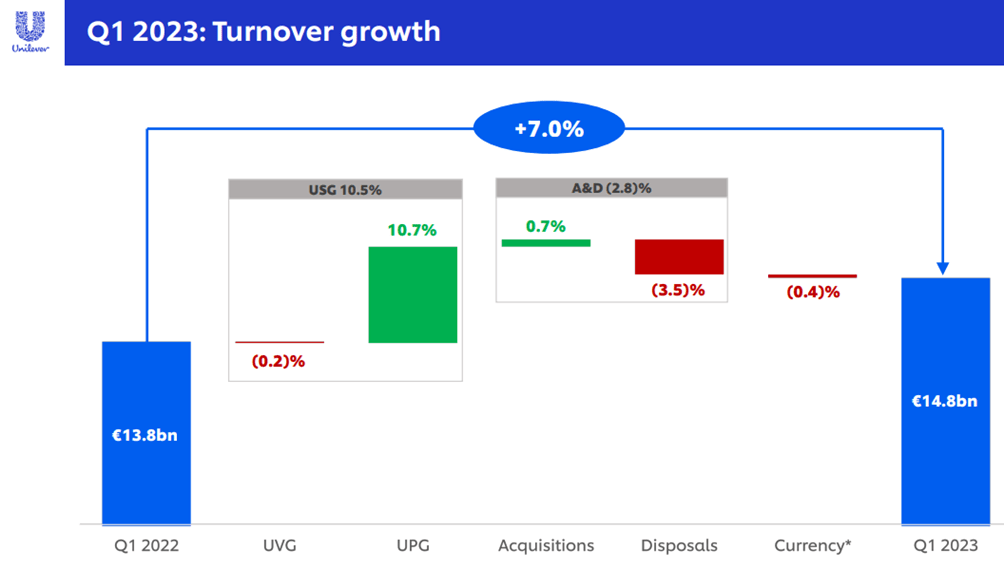

Overall, Unilever's turnover increased by 7% compared to Q1 2022, and by 10.50% considering underlying sales. But what is the reason for this difference?

{kind=link}

As mentioned earlier, the two figures differ based on the exclusion of nonrecurring components such as acquisitions, disposals and foreign exchange effect; in this case these three elements had an impact of 0.70%, - 3.5% and - 0.40%, respectively.

Let's now look in detail at how the individual segments affected this result.

Unilever Q1 2023

The Beauty & Wellbeing segment presented both increasing volumes and increasing prices. UVG was 2.60% while UPG 6.50%; overall USG was 9.30%. In contrast to previous quarters, price growth slowed down and Unilever again reported an increase in sales volumes after 2 consecutive negative quarters.

Driving the performance of this segment was double-digit growth in Paula's' Choice, Tatcha, Hourglass, Liquid I.V. and Onnit brands.

The company expects the momentum of this segment to continue as some products will be released in other countries as well. For example, Tatcha Skin Care has just a week ago been available in China.

Unilever Q1 2023

Personal Care, as well as Beauty & Wellbeing, achieved both volume and price increases. This was the best-performing segment, and again the reduction in price increases affected product demand. In fact, UVG returned to growth after four quarters in the negative. However, there is another crucial aspect to consider.

UVG has been positively affected mostly by Deodorants , and the company does not expect volumes to grow in this way throughout the year. Here are Graeme Pitkethly's ((CFO)) words on the matter:

The standout performance in Personal Care was from Deodorants, where it was volume driven. This is a business where we experienced supply restrictions through most of 2022, both in North America and in Europe. Some of the reported volume improvement this quarter is due to refilling depleted pipeline and getting our trade stocks back more normal levels. So we do not anticipate the exceptional volume performance of Deodorants in the first quarter to sustain through the rest of the year.

Finally, it is worth noting that in this segment Unilever is eliminating a large number of inferior brands and is also working on a rather significant SKU rationalization. In short, it is better to eliminate underappreciated brands that are a cost to the company anyway.

To date, the billion-plus brands account for 54% of Unilever's revenues, and the company is investing mainly in these.

Unilever Q1 2023

Home Care unlike the first two segments recorded an increasing UPG but still negative UVG. Indeed, this is not surprising, as the price increase is still too significant although less than in the past.

In any case, we cannot consider the result achieved in this segment as weak; the growth was double digits, and the company seems to be very satisfied with the result achieved as it has repeatedly mentioned how difficult the current operating environment was particularly in rural areas.

Fabric cleaning was the main growth driver with excellent performance especially from the premium ranges, while Domestos contributed to the recovery of Household Care. Also in this segment it was preferred to disinvest in some unprofitable brands and focus on a new reorganization in products sold in Europe, Africa and West Africa.

Unilever Q1 2023

Nutrition grew strongly due to the umpteenth price increase that largely covered the reduction in sales volumes. According to the company, such an increase was necessary because of rising commodity prices, energy costs, the impact of climate change on agricultural yields, and rising wages. Either way, the peak of inflation seems to have been reached, and the company expects that prices in the future will not rise as they have in the past. However, there is no guarantee that then sales volumes will immediately return to growth.

Hellmann's and Knorr are the best performing brands this quarter.

Unilever Q1 2023

For the Ice Cream segment, the basic reasoning is the same as for Nutrition. These segments have been the hardest hit by inflation, and as a result, the company has been forced to raise prices a great deal so as not to see its margins deteriorate. In any case, this maneuver has led to a loss in sales volumes.

Again, the company is removing less profitable brands by focusing more on premium brands that have wide acceptance. Brands such as Cornetto have seen double-digit growth, while Talenti Ice Cream Sticks are experiencing success in the United States. Finally, the strong earthquake in Turkey negatively affected the final result, as this nation is a very important market for Unilever's Ice-Cream segment.

Final thoughts

Overall, Q1 2023 was positive as all sectors experienced a positive USG, but it is evident that the Ice-Cream segment performed the worst. The restructuring of the company's portfolio is continuing efficiently, and gaining from this are the brands that individually generate more than €1 billion. The latter grew by 12.10% compared to Q1 2022.

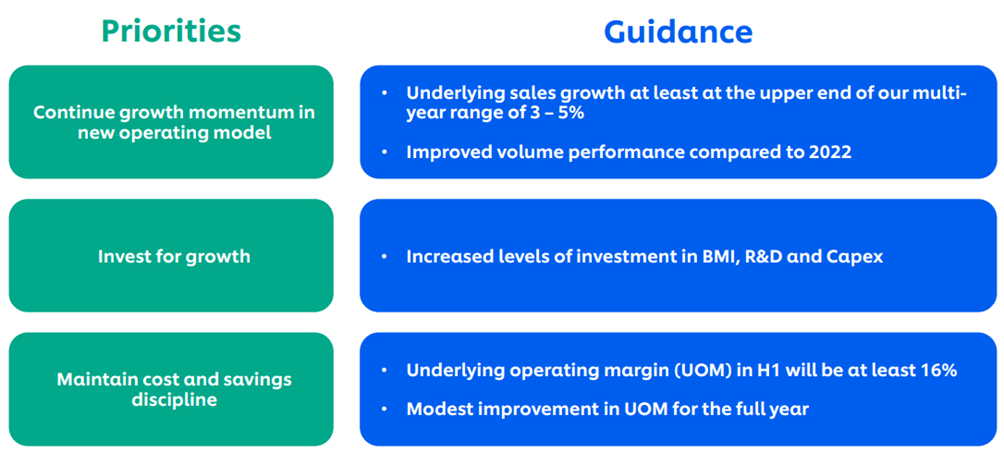

However, there is not only revenue growth in this quarterly, but also shareholder remuneration. The third tranche of share repurchase for €750 million will be completed in July 2023, while the next dividend will be maintained at €0.4268. Such a solid company that consistently remunerates its shareholders could prove to be a good choice for anyone who wants to include a defensive stock in their portfolio. Finally, I conclude this quarterly analysis by showing you the guidance for the full year 2023.

{kind=link}

For further details see:

Unilever: Pricing Drives Growth And Sales Volumes Improve, Fairly Valued