UNLYF - Unilever: SKU Rationalization And Growth Prospects

2023-06-06 13:00:42 ET

Summary

- Unilever is a low-risk investment with a high dividend yield of 3.71% but slow growth.

- The company is focusing on SKU rationalization to optimize costs and boost growth by investing in its top-performing brands.

- Unilever's fair value is estimated at $60.88 per share, making it slightly undervalued.

Business Overview

Unilever ( UL ) is a major fast-moving consumer goods company and its products are purchased by millions of consumers every day. Being headquartered in London, Unilever is often referred to as the European Procter & Gamble, not so much because of its earnings results but because of the similarity of its business model. The latter is divided primarily into five segments:

- Beauty & Wellbeing: responsible for 21% of total revenues; the best known brands are Vaseline, Sunsilk and Dove.

- Personal Care: responsible for 23% of total revenues; best-known brands are Dove, Rexona , and Axe .

- Home Care: responsible for 22% of total revenues; best-known brands are Domestos, Cif and Comfort .

- Nutrition: responsible for 23% of total revenues; best-known brands are Hellmann's, Bango and Knorr .

- Ice Cream: responsible for 11% of total revenues; best-known brands are Ben & Jerry's, Magnum and Wall's .

About a month ago I commented on Unilever's Q1 2023 and it had been positive overall as all segments had experienced good underlying sales growth. In this article, I will instead analyze its dividend, its future strategy, and its fair value.

{kind=link}

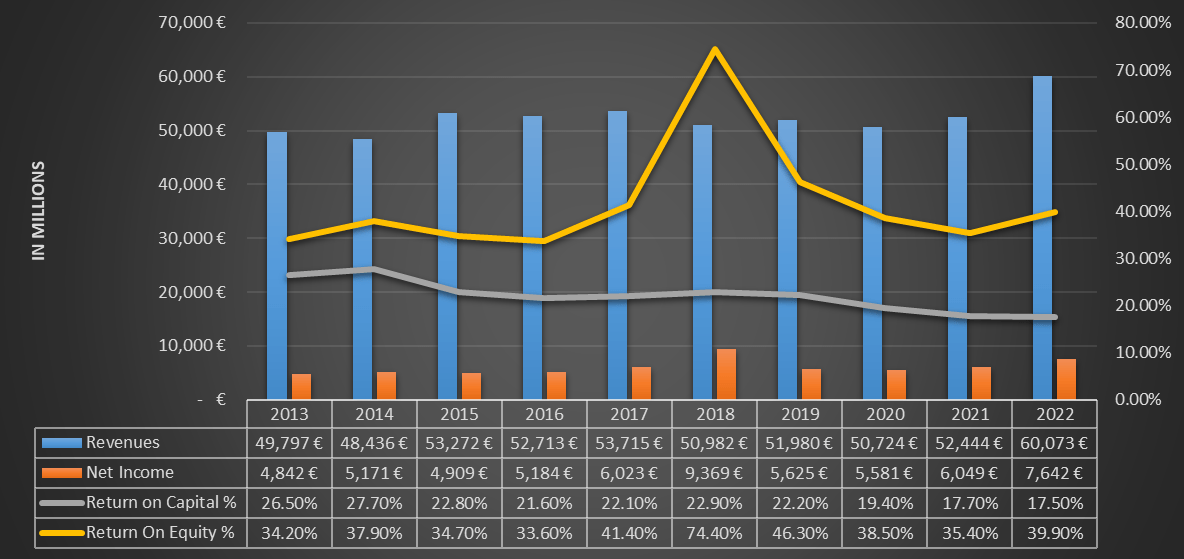

Over the past 10 years, Unilever has achieved stable income results but with rather slow growth. The latter, is mainly due to the market in which it operates that does not allow for substantial improvements from one year to the next. For that matter, it is even more difficult to assume a strong growth scenario given that Unilever is also one of the most established leaders. Return on Capital and ROE have always been quite high, a sign that this company knows how to invest its money.

{kind=link}

Net debt continues to increase over the years, aided by Unilever's strategy of globally enlarging its presence through acquisitions and investments in its top brands. In any case, relative to EBITDA, net debt remains sustainable.

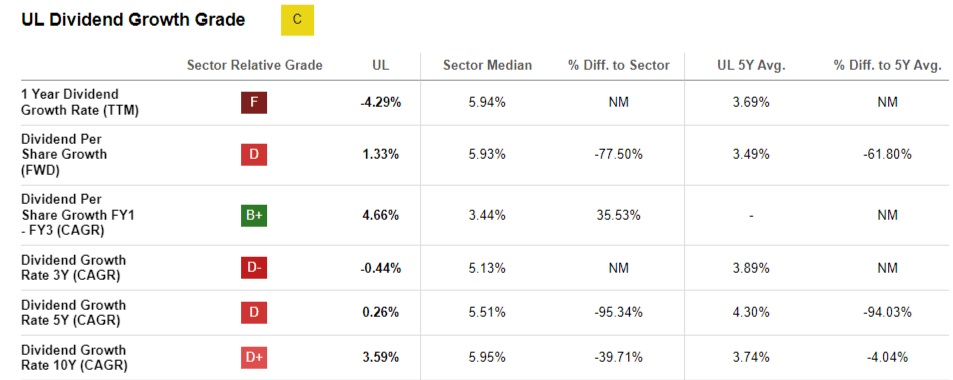

Dividends

Like most consumer staples companies, Unilever makes dividends one of its most important traits. Its earnings stability has enabled it to issue increasing dividends over the long term, and currently the dividend yield is 3.71%.

{kind=link}

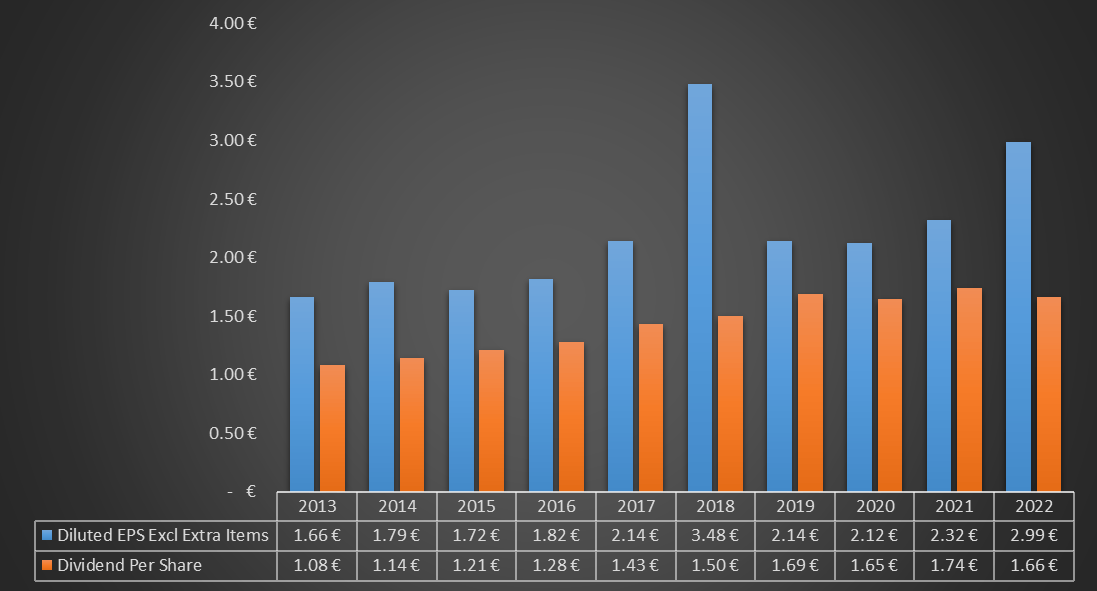

EPS has shown steady growth over the past 10 years, which is why the dividend per share has not only been growing but also sustainable. However, it is worth noting that if we wanted to evaluate the sustainability of the dividend based on cash flows, the picture of the situation is not the same.

{kind=link}

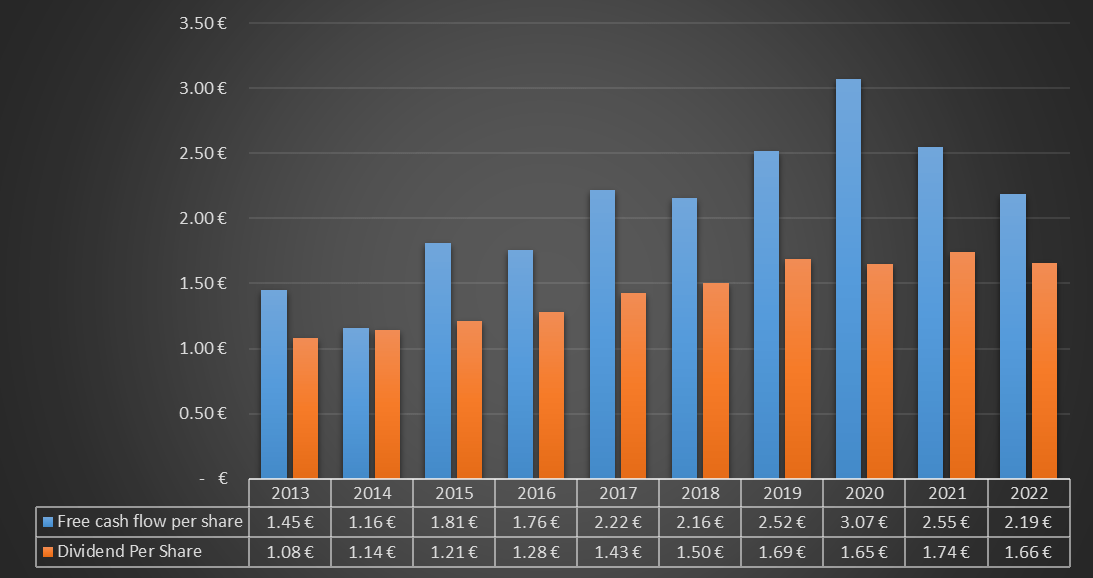

As can be seen from this image, the trend in free cash flow per share does not show steady growth as in the case of EPS, far from it: there has been no improvement since 2017.

As of today, the problem does not exist since the dividend per share is still covered, but it is better that Unilever's free cash flow gets back to growth as in the past as soon as possible. The reasons for this divergence between net income and free cash flow results are explained by analyzing the cash flow statement.

{kind=link}

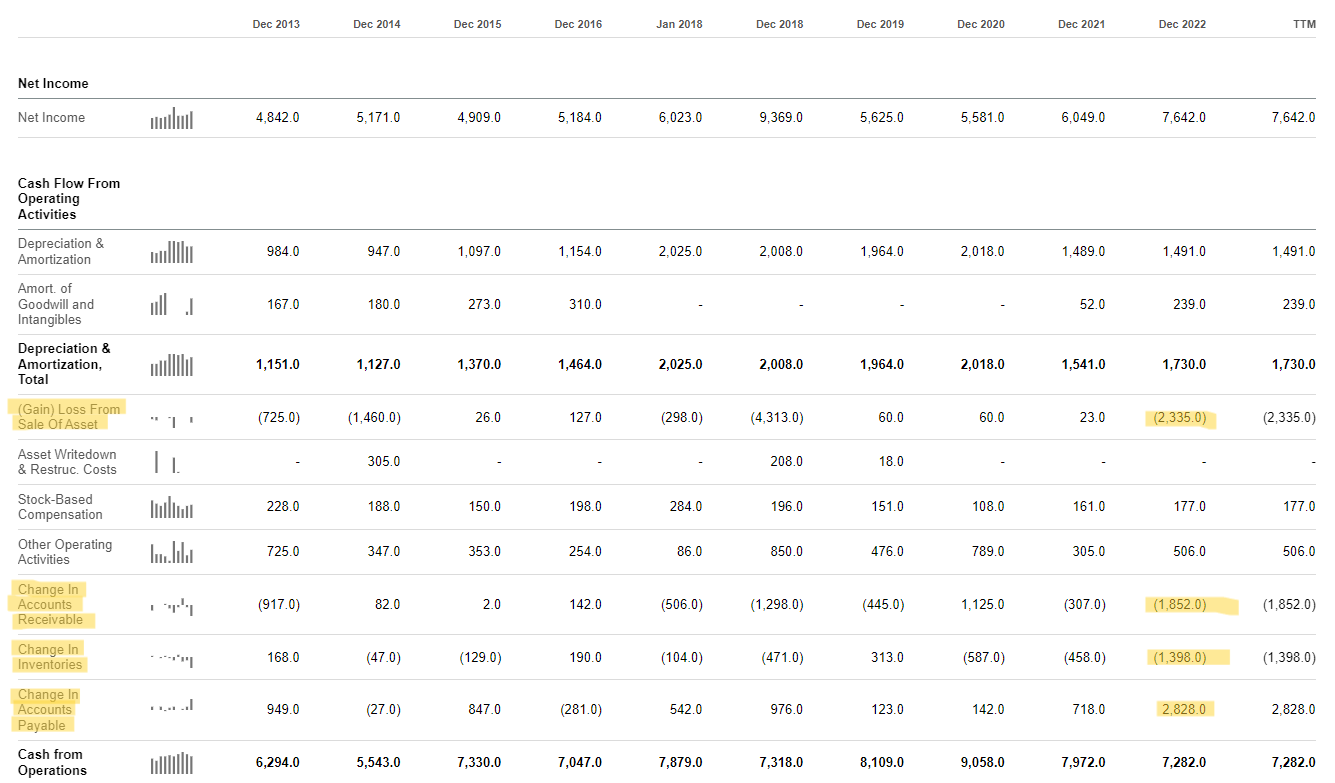

Mainly, there are 3 most important factors:

- The first concerns a major increase in Accounts Receivable of €1.85 billion over the previous year, offset, however, by Accounts Payable increasing by €2.82 billion.

- The second concerns a €1.39 billion increase in inventory, a signal that the economy is slowing down and Unilever is accumulating unsold inventory.

- The third concerns the sale of assets worth €2.33 billion, a move in line with the company's product rationalization strategy that we will discuss later.

In any case, even considering this divergence, the dividend yield is quite high and, above all, sustainable at the moment. Probably, the main problem is growth.

{kind=link}

If the dividend remains sustainable, it is mainly because its growth has been rather limited in recent years: the CAGR has been only 0.26% in the last 5 years, 3.59% in the last 10 years. In short, the dividend yield remains high, but based on what has happened in the past, I expect the dividend per share not to increase considerably in the coming years.

Unilever, like most European companies, gives little weight to statistics and dividend track record, which is why management does not care to become a dividend aristocrat or a dividend king. The dividend issued in a given year is simply what the company can afford to issue, and if it is lower than the previous year it matters little. In fact, in 2021 the dividend per share was €1.74, while in 2022 it dropped to €1.66 due to worsened macroeconomic conditions.

Overall, investing in Unilever can have a number of advantages and disadvantages:

- The main advantages are associated with a rather high dividend yield and the possibility of making a decent capital gain as well. In addition, due to stable earnings, Unilever should not struggle too much in the event of a recession.

- The main disadvantage is related to the slow growth, which does not allow a substantial increase over the long term in the dividend issued. What is more, the dividend cannot be expected to grow every single year, as this is not the company's priority.

Growth Expectations

As discussed at length above, growth is the main problem for Unilever, which is why management's focus is primarily on this issue. The key strategy Unilever is adopting to solve this problem is called SKU rationalization, or increasing profits by optimizing costs.

Over the past decades, Unilever has acquired dozens of brands to integrate within its ecosystem, but not all investments have performed as hoped. Some have performed rather disappointingly in general and others have underperformed in certain geographic areas. What's more, beyond the underwhelming revenues, producing these brands comes at a cost, and the company is no longer willing to sustain it.

We do like broad portfolios in countries, but not when one part of the portfolio is dragging down the whole operation, and that was the situation that we were in West Africa

For example, as also specified by CEO Alan Jope , the West Africa geographic segment has undergone this process and Home Care products will be delisted because they have disappointed expectations.

So, management is now focused on marketing and innovating the brands that have found the most success in Unilever's history, while inferior brands with underperformance will be removed from the portfolio. The savings generated from this latest transaction will be reinvested in the so-called billion+ Euro brands.

In fact, according to the results of the latest quarterly report, the results are already visible. The billion+ Euro brands segment is responsible for 54% of total revenues and recorded a 12.10% growth in underlying sales due to the strong performance of OMO, Hellmann's, Rexona and Lux.

{kind=link}

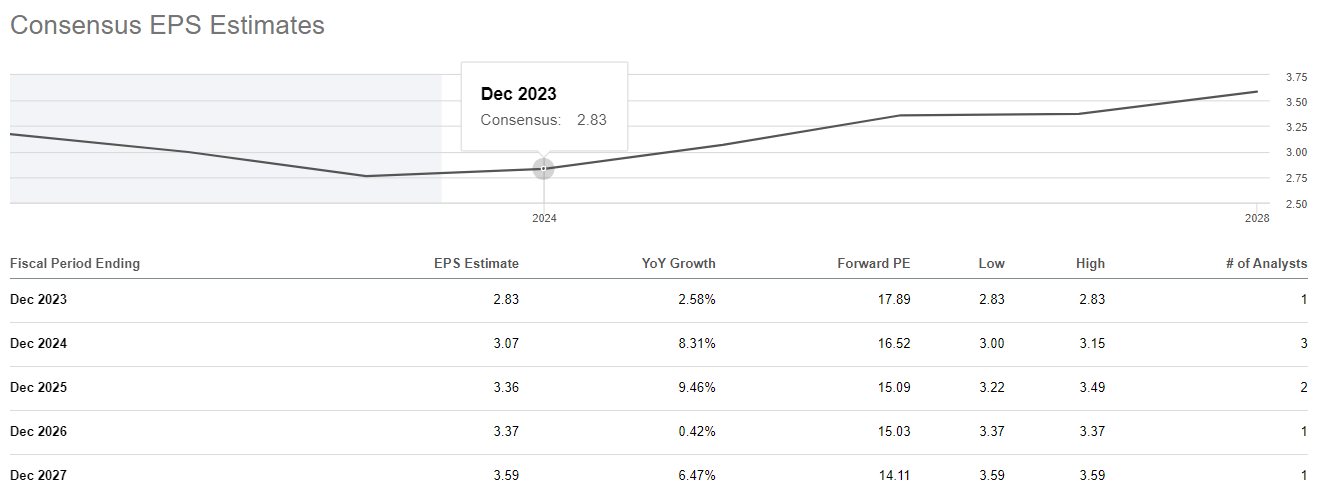

According to Seeking Alpha analysts' estimates , starting this year there will be a gradual increase in EPS until 2027, which would be justified by cost reductions and growth of popular brands. I consider these estimates rather optimistic but not unrealistic, partly because it is not only earnings but also buybacks that will increase EPS. Suffice it to say that treasury stock worth €750 million will be purchased this quarter.

Finally, heading this new Unilever organization will no longer be Alan Jope, as starting this month Hein Schumacher has been designated as the new CEO.

Valuation

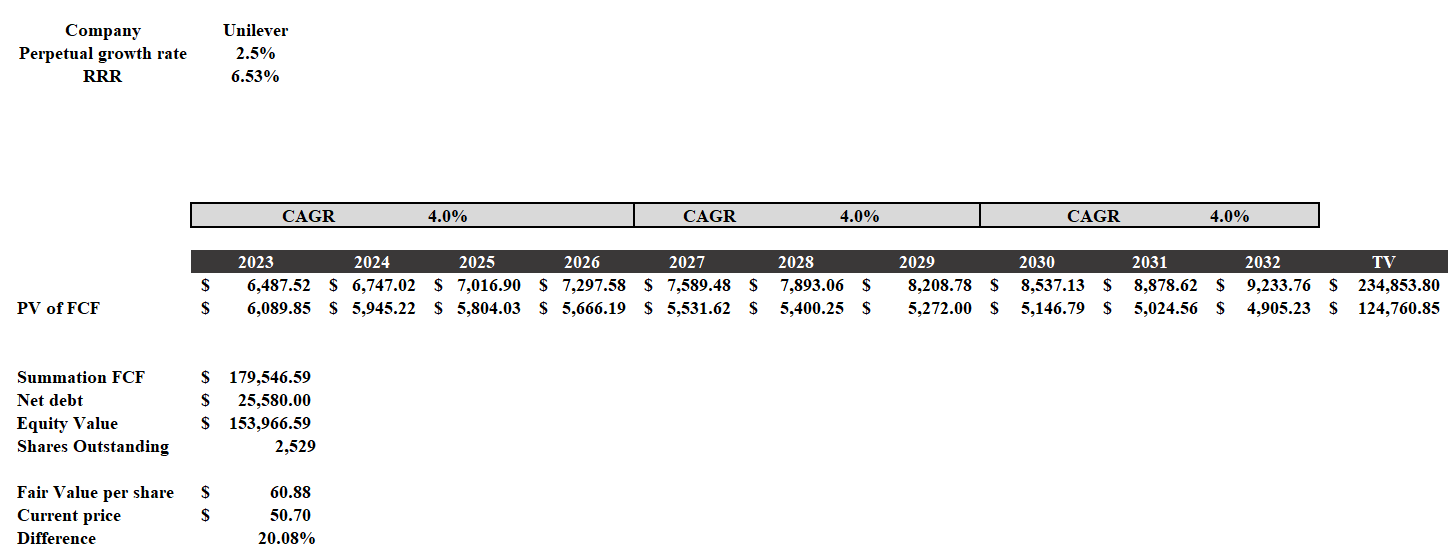

In this last section, I will focus on the Unilever's fair value, and I will do so through a discounted cash flow model. This model will be constructed as follows:

- All figures are converted to dollars.

- The source of net debt and shares outstanding is Seeking Alpha.

- The 2013-2022 CAGR of free cash flow was 4.30%; therefore, the growth rate for the next 10 years will be 4% from the 2022 free cash flow of $6.23 billion. The perpetual growth rate will be 2.50%.

- The RRR is equivalent to the cost of equity, or 6.53% . Such a low figure comes from Unilever's low volatility; in fact, the beta is only 0.48.

{kind=link}

The result, is that Unilever's fair value is $60.88 per share, so it is slightly undervalued. However, a RRR of 6.53% is objectively low, and according to this valuation we should settle for a modest return given the low riskiness of the investment. Requiring an annual return of 8%, the fair value would drop to $41.56 per share, and at that point Unilever would be overvalued.

Overall, Unilever is not an investment for everyone but for those who want to have low-risk exposure to the stock market. To expect more than 8% per year from such a company is in my opinion unlikely, as there is no basis for it to grow that much in the future. SKU rationalization may ease the structure and costs incurred, but it will not change the way this company makes money.

In short, for those with a long-term view and looking for a defensive portfolio stock with a dividend yield above 3% Unilever may be an idea. On the other hand, those looking to beat the market over the long term are unlikely to succeed with Unilever, especially at the current price. What's more, regarding the dividend, one must also consider double taxation for non-UK residents, which makes the dividend less attractive.

For further details see:

Unilever: SKU Rationalization And Growth Prospects