UNLYF - Unilever: Upgrading To Buy Despite Headwinds And Challenges

2023-11-02 10:13:36 ET

Summary

- Unilever has continued on its solid growth trajectory after reporting 14.5% growth in 2022 by reporting 7.7% underlying sales growth for the first nine months of this year.

- The company’s strong portfolio of brands, which are used on a daily basis by billions of people is giving the company incredible pricing power and resiliency.

- In terms of revenue diversification, the company is looking really good and de-risked, further solidifying its defensive character.

- CEO Hein Schumacher introduced a new action plan to primarily boost underlying volume growth and improve the gross margin as both have been lagging in recent years.

- With the company showing improvements in the underlying business, having a new CEO, and a new action plan, I believe shares hold quite some value, warranting a Buy rating.

Introduction

I move my rating on Unilever PLC ( UL ) from Hold to Buy as the company is starting to look more attractive under a new CEO and the introduction of an action plan to boost volume growth. Furthermore, shares seem valued at a slight discount of 4% to fair value. Therefore, I am turning bullish on this defensive giant.

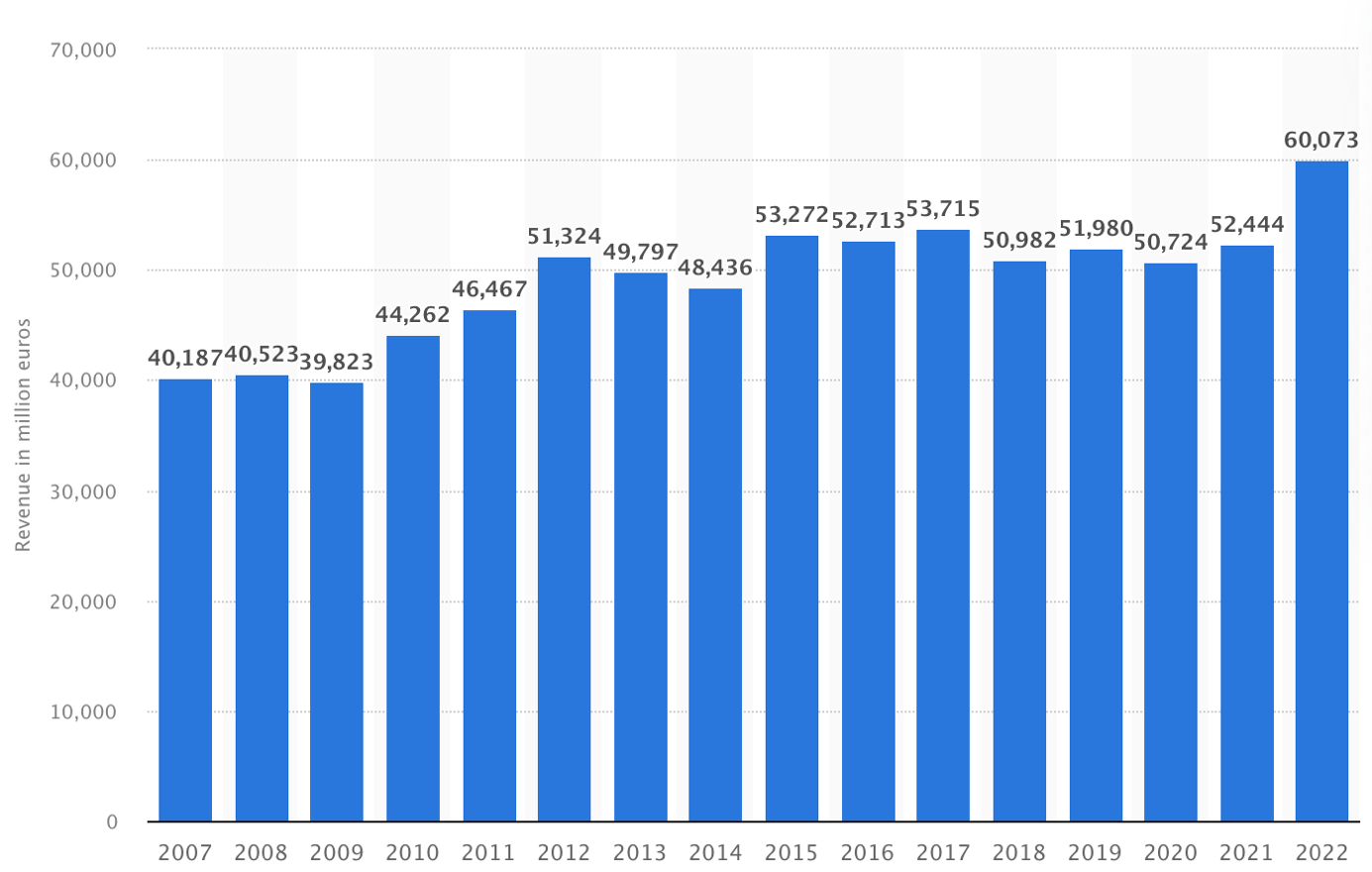

Unilever has been anything but an exciting investment over the last decade, returning 20% over the last ten years (excluding dividends) and a negative 11% over the last five years. Unilever has grown revenue at a very meager 1.5% CAGR over the last decade, and while in part the result of several divestitures and acquisitions, this still falls short of most of its peers and global GDP growth , which I believe is the minimum growth rate should be able to expect from a massive global consumer staples conglomerate.

{kind=link}

Therefore, this is no more than a disappointing performance from one of the largest consumer goods conglomerates in the world, carrying many of the world’s most famous consumer brands like Ben & Jerry, Magnum, Knorr, Dove, and Axe.

For those unfamiliar with the company, Unilever is a multinational consumer goods company that operates in various consumer goods industry sectors, including food and beverages and home and personal care products. Unilever operates in many countries worldwide and has a significant global presence. The company reports across five product segments: Beauty and wellbeing, Personal Care, Home Care, Nutrition, and Ice Cream.

Now, I last discussed Unilever on Seeking Alpha a little over a year ago when I called the company a “ defensive stronghold .” Back then, I rated shares a hold as I could not see much more upside for the shares without some management changes and a new growth strategy. And indeed, while delivering a positive return, Unilever has underperformed the major indices since my last article, providing a total return of 11.5% (including dividends), sitting below the 14% returned by the S&P 500 (not a disastrous underperformance, though)

However, one year on, Unilever has continued on its solid growth trajectory after reporting 14.5% growth in 2022 by reporting 7.7% underlying sales growth for the first nine months of this year, although still driven mainly by price increases as a result of inflation. Meanwhile, volume growth has remained negative up to the most recent quarter, and turnover was up just 0.4% YTD. Yet, I will get deeper into its most recent results in a bit.

More importantly, the company has, in the meantime, introduced a new CEO in the form of former Heinz executive Hein Schumacher, who has taken over from Alan Jope since July 1 and could bring a fresh wind to the company, something it desperately needed. The first real signs of this CEO change have become clearly visible with the introduction of an “action plan” introduced by the company with the release of the Q3 trading update.

Therefore, in this article, I will take a closer look at the company’s most recent financial result, company developments, and this newly introduced action plan to better understand the company’s prospects, valuation, and investor appeal.

Let’s get to it!

Unilever’s Q3 looked solid, but volume growth remains a problem

Before getting into the highly anticipated action plan, something I have long been waiting for, I first want to take a closer look at the company’s Q3 performance .

Unilever reported Q3 underlying sales growth of 5.8% and a turnover of €15.8 billion, down 3.8% YoY, as the better underlying performance was offset by acquisitions and disposals and a negative 8% currency impact.

This shows that sales growth has been moderating over recent quarters as inflation is easing and Unilever has completed most of the necessary price increases. As a result, Underlying price growth in Q3 was down from 9.4% in the first six months of this year to 5.8% in Q3. Meanwhile, volume growth remained weak and was down 0.6%, compared to 0.2% in the first six months.

This combination of developments is what drives the slowdown in growth and is a somewhat worrying trend as price increases should moderate further, but underlying volume growth is so far showing little improvement sequentially.

However, the growth we witnessed in the last two years of mid-teens and high single-digit growth is not a realistic expectation. Eventually, growth will moderate to the more realistic low to mid-single digits. It is safe to assume growth will continue falling over the next few quarters as price increases continue to moderate, but volume growth will turn positive again by the end of the year. As a result, growth should remain within management’s long-term targeted range of between 3% and 5%, although continued consumer weakness could result in volumes remaining suppressed for longer.

Looking at the individual segments, Beauty and Well-being and Personal Care delivered balanced volume growth of 3.6% and 3.9%, partly thanks to these segments containing products that are less sensitive to the decrease in consumer spending power. In combination with continued price increases, these segments saw underlying sales increase by 7.4% and 8%.

Home Care also returned to positive volume growth in Q3 of 0.4%. With prices up 5.4%, this segment saw underlying sales growth of 4.8% YoY. So far, so good.

Yet, the Nutrition and Ice Cream segments continued to see volumes pressured in response to high input cost inflation, especially in Europe. These segments are generally far more discretionary and experience lower pricing power. Whereas people tend to be very close to their usual beauty brands or deodorant, we cannot say the same about their ice cream.

Volumes in Nutrition remained down 3.8% YoY, bringing total growth to 5.6%. Volumes in Ice Cream were down 10.1% as prices increased 8.2%, resulting in negative underlying sales growth of 2.8%. This segment should rebound in the next few quarters as price increases moderate.

Overall, in terms of top-line growth, it was a very respectable quarter for Unilever with decent underlying sales growth, but clearly the company continues to depend heavily on price increases to drive this growth, and even as these moderated, volumes did not respond accordingly.

Regarding this, there are two points worth highlighting. For one, while Unilever (and its peers, for that matter) are often criticized for the fact that growth is largely being driven by price increases as opposed to volume growth, perfectly highlighted by the last three years, I believe Unilever also deserves a compliment for its performance over this period.

The company showed its excellent pricing power and the non-discretionary nature of its products as it was able to grow its top line and offset inflationary pressures in a very challenging environment. The company’s strong portfolio of brands, which are used on a daily basis by billions of people is giving the company incredible pricing power and resiliency, which is precisely what makes this company such an enticing investment - no matter the economic climate or macroeconomic headwinds, one can be sure of Unilever to keep its top line strong.

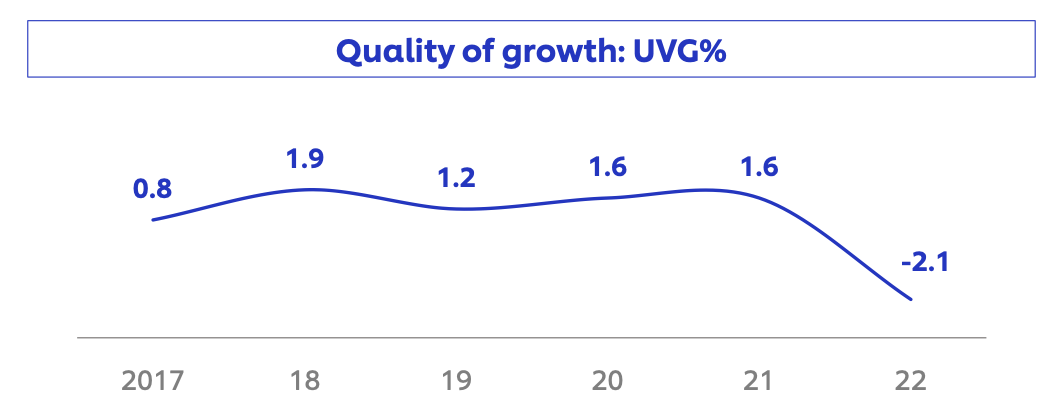

Yet, returning to the subject of its dependence on pricing power, this is actually something investors should worry about. Unilever has reported volume growth of below 2% annually for most of the last decade, with pricing indeed being the main contributor of growth, something which should ideally be the other way around. It is this weak volume growth that has largely caused Unilever’s underperformance over the last decade. Without any meaningful strategy changes coming from the management team, I am not expecting this to change despite it having an incredible brand portfolio. Positively. management acknowledges this problem as highlighted by this quote from CEO Hein Schumacher during the earnings call :

Taken over the last six years, volume growth has been lagging.

Unilever YoY volume growth (Unilever)

{kind=link}

But what causes this structurally disappointing volume growth? Fundamentally, the company’s revenue stream is looking extremely good and low risk. Of course, the company has its strong branding, which meaningfully lowers risk, as communicated before, but its revenue stream is also exceptionally well diversified across end markets, with not a single segment accounting for over 24% of turnover.

The company is also nicely diversified in terms of regional exposure, with its largest region in terms of sales – the Asia Pacific Africa region - accounting for only 43% of turnover, The Americas for 36%, and Europe for 20%. Furthermore, the company has 40% exposure to emerging markets, and while this revenue might be perceived as riskier and more volatile, it also generally is faster growing due to growing wealth in these regions, boosting growth for the conglomerate as a whole.

So, in terms of revenue diversification, the company is looking really good and de-risked, further solidifying its defensive character.

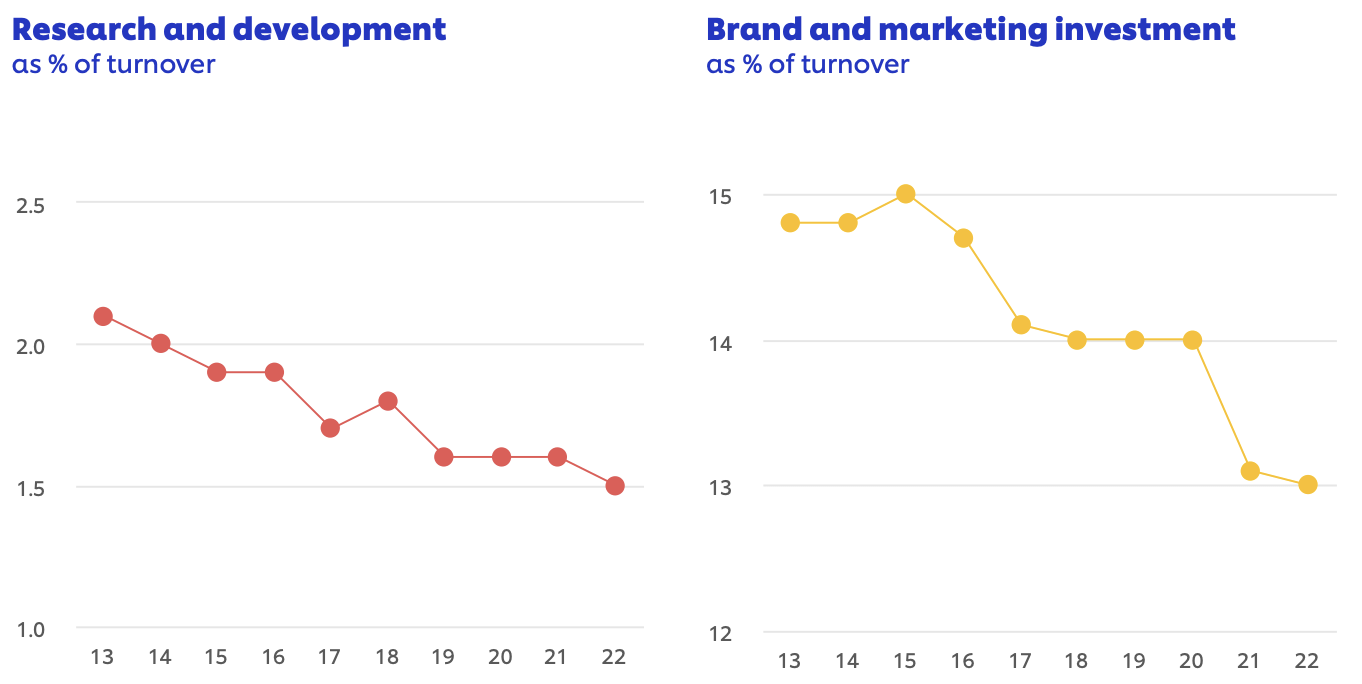

Yet, what looks less good are the company’s R&D and brand and marketing investments, which have been trending down over the last decade as a percentage of turnover. Also in terms of €, the FY22 R&D and brand and marketing expenses were sitting below 2016 and 2015 levels. While lowering these expenses has worked in favor of the company’s margins, I firmly believe this has cost it in terms of volume growth as Unilever clearly fails to get the most out of its brands.

Unilever financial data (Unilever) Unilever financial data (Unilever)

{kind=link}

{kind=link}

There is a lot to gain here for the company. I believe its success over the next decade will largely depend on its execution on this front, which will require more significant investments in branding and R&D. Luckily, management has finally introduced a clear action plan to take this one, making me slightly more confident in the company’s future volume growth.

But before we move to this plan, let’s quickly look at bottom-line developments.

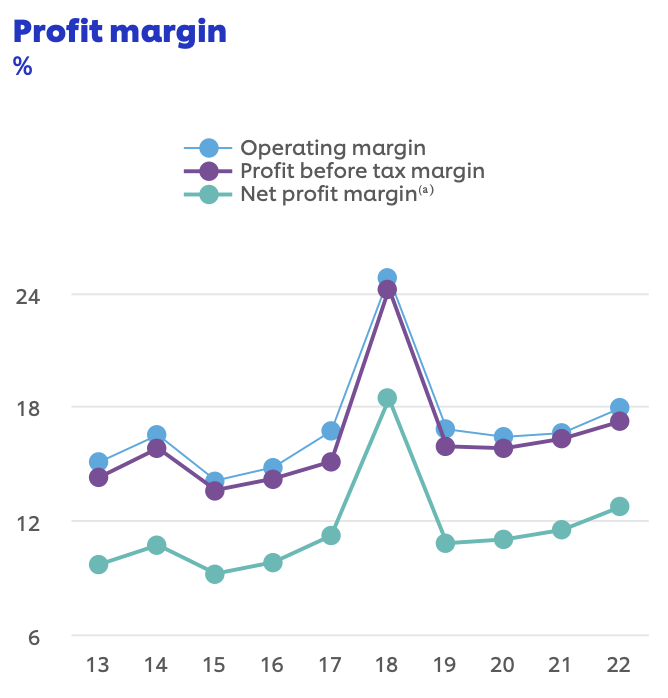

The margin trend is strong as margins remain best-in-class

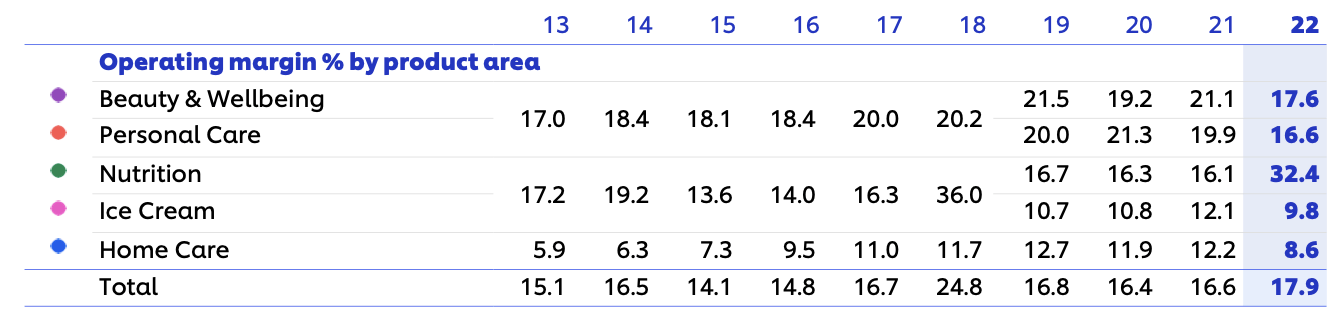

The company’s margin profile has been all over the place over the last decade. Still, it has been on an improving trend recently, with operating and net income margins growing steadily over the last two years as Unilever was able to offset inflationary pressures.

{kind=link}

As Unilever does not provide any bottom-line insights with the Q3 trading update, we will have to look at the H1 results for the most recent data, and this showed some solid margin improvements.

The H1 operating margin expanded by 290 basis points to 18.1%, further trending upward from the 17.9% reported for 2022 and sitting at the highest level since 2018, resulting in a 22.6% increase in operating profits. Yet, the net income margin declined slightly YoY by 80 basis points to 12.8%, causing a slight dip in a strong improving trend. Excluding the 2018 standout year, Unilever has steadily improved margins. I see no reason for this not to persist over the next few years, although possibly at a slightly slower pace, as the company will be focused on increasing R&D and marketing expenses. Still, margins remain best-in-class, and I see 30-50 basis points of margin expansion annually as a realistic target here.

Unilever margin development (Unilever)

{kind=link}

Management introduced a new action plan and it's looking promising

Together with the Q3 trading update, CEO Hein Schumacher also introduced a new action plan to primarily boost underlying volume growth and improve the gross margin as both have been lagging in recent years. While the plan did not receive a warm welcome from investors with a drop in the share price following the announcement, I quite like the plan as it acts on my main concerns.

As I have stated before, Unilever, under the hood, is an amazing company with a mighty collection of incredible consumer brands, of which 80% hold the number 1 or 2 position in their respective categories and are used by approximately 3.4 billion people daily. Furthermore, while R&D investments as a percentage of turnover have been falling the company still holds 20,000 patents, highlighting its level of innovation. Clearly, the company has great potential, and this new action plan is designed to materialize this.

To boost underlying volume growth, management discussed multiple aspects that it aims to improve, with the most important being focusing on its top brands, increasing R&D and project size, and increasing brand and marketing investment and return.

Starting with the focus on top brands, management explained that it wants to focus resources on its top 30 brands as these account for 70% of turnover and are crucial drivers of volume growth due to their brand strength. Through this, management aims to optimize its portfolio. These 30 brands include the €1 billion club, like Dove, Magnum, and Hellmann, and 16 other brands that have the most potential to join them, like Cif, Vaseline, Liquid I.V., and Nutrafol.

Unilever focus brands (Unilever)

{kind=link}

While this prioritization led to some mixed reactions from analysts, I favor this move as I strongly believe that Unilever needs to leverage these strong brands to drive more impressive growth. The best way to do this is by focusing resources on the most promising ones. Also, management made very clear that it does not intend to leave the remaining brands underinvested or to divest these but simply wants to focus most of the resources on its most promising opportunities to be able to better compete in these markets and improve execution to drive volume growth. Eventually, it might be a good move to divest the remaining underperforming brands over time, but management is not aiming for this at this time.

Secondly, to further drive volume growth, management aims to increase innovation project sizes, as these have proven to be too small in the past, leaving Unilever unable to innovate in line with the competition. Therefore, management now prioritizes multiyear scalable programs that drive category growth. Project sizes have already tripled since 2020, but management aims for another doubling of project sizes in the near term to drive more meaningful product innovation, which sounds like a great priority to set, as Unilever needs to catch up here. If management executes these plans correctly, I see meaningfully more potential for volume growth ahead.

These larger project sizes will be supported by consistently growing the R&D investment, pushing Capex to above 3% of turnover from just 2.4% in the last three years. As I indicated earlier in the article, this is what I wanted to see from Unilever, and management seems to deliver with R&D growth. This boosts my medium-term volume growth expectations.

Turning to the next and final growth lever, management wants to increase the absolute brand and marketing investment level to maximize brand potential. This is what management added:

This is a must but we will also ensure that our brand and marketing investment spend is more focused with deliberate allocation behind bigger platforms, more consistent, fully funding our power brands, more digital and more effective increasing returns of marketing spend.

This is another great move, and I am glad to see management acknowledging and acting on the fact that it has not been maximizing brand potential over recent years as a result of declining marketing and R&D budgets. With this trend now reversing, I expect this to positively impact volume growth in the medium to long term. Yes, it might take a couple of years for this to materialize but the intention is great.

Also, with this shift to focus on its high-end brand portfolio, R&D, and marketing, management will scale back on M&A activity. Management acknowledges that past acquisitions have not always worked out and wants to up the bar, meaning acquisitions are not out of the question but will occur less frequently and will be of higher quality. Furthermore, no major or transformational acquisitions are expected in the foreseeable future, which I view as another positive at this time.

The second part of the action plan aims to stop the gross margin decline and start recovering it in the next few years through a focus on net productivity instead of growth savings, which has been holding back the company in recent years.

Unilever financial data (Unilever)

{kind=link}

This new focus will extend across all P&L lines like material costs, through competitive buying, value chain interventions, and product reformulations. Also, regarding production and logistics costs, the company has set challenging targets to reduce the cost per unit produced, contributing to a recovery of the gross margin, which should indirectly result in a faster-growing EPS as well.

Management has yet to set direct gross margin targets, which I found disappointing as I hoped for management to set clear targets. Throughout the presentation, while clear in goals and actions, I missed a couple of solid targets and timeframes, which indicates the plan isn’t very solid yet.

Of course, this makes sense as the new CEO has only been active for a couple of months. Nevertheless, so far, Hein Schumacher has impressed me with his actions and commentary and makes me somewhat more confident of Unilever’s growth potential.

Outlook & UL stock valuation

Following the Q3 results, management left the FY23 outlook unchanged and expects underlying sales growth to be above 5%, with price growth continuing to moderate. I expect volume growth to remain negative in Q4 as a result of weak consumer spending power and underlying sales growth to moderate to a 3-5% level.

Furthermore, we can expect a modest improvement in underlying operating margin as the recovery in gross margin is reinvested in marketing spend, in line with management’s action plan.

Looking on to next year, I expect continued consumer weakness to result in volumes remaining suppressed for longer, which, combined with moderating price increases, will put FY24 underlying sales growth under pressure and sit at the low end of management’s targeted range.

Combined with an increase in R&D and marketing spend, I expect margins to also fall slightly, putting pressure on EPS. I expect FY24 to be a challenging year for Unilever due to a combination of factors, but this should recover from the second half of the year and into 2025. In the long term, I have become more confident in Unilever’s growth outlook, which I believe should eventually sit at the high end of management’s guided range (USG of 3-5%), with EPS growing even faster due to a gross margin recovery leading to margin expansion. As a result, I project long-term EPS growth at high-single digits.

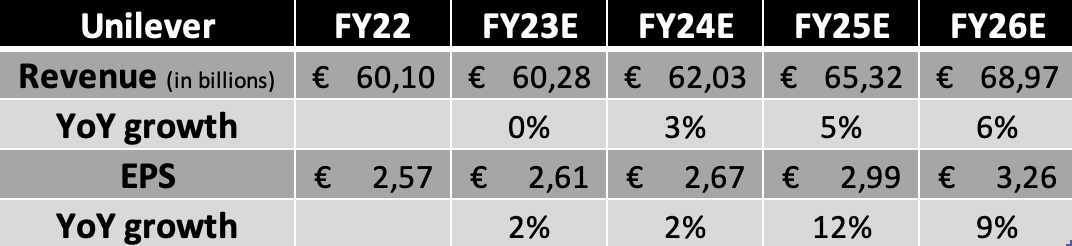

These expectations result in the following financial projections.

Financial estimates (By Author)

{kind=link}

Based on these estimates, Unilever shares are currently valued at a forward P/E of 17x or at a 14% discount to its 5-year average. Arguably, the company is looking better than five years ago despite a challenging FY24 ahead.

Furthermore, if we compare this to peers in the beauty and household products market as well as other consumer staple companies, we can see that Unilever is priced quite favorably compared to its defensive counterparts. Meanwhile, its current valuation sits roughly in line with the industry average.

Overall, with the company showing improvements in the underlying business, having a new CEO, and a (slightly unclear) action plan, I believe shares hold quite some value and Unilever could be an excellent value play from this point out.

Fundamentally, Unilever has always been an enticing investment option due to the necessity of its products in the daily lives of billions of people, the defensive nature of its operations, and its incredible brand portfolio. However, execution over the last decade has been far from ideal, and this now seems to be turning around, or at least, it is planning to.

Therefore, I am awarding shares a fair value P/E of 19x, still sitting slightly below its 5-year average as risks remain and a real volume growth turnaround is yet to materialize. Still, based on my FY24 EPS estimate and a 19x P/E, I calculate a target price of €51. From a current share price of €44.70, I believe investors are poised for double-digit returns, even when excluding the very decent dividend, which currently yields close to 4%, above most of its peers, and making this an exciting investment opportunity for those who believe in a growth turnaround.

Therefore, I moved my rating on Unilever shares to Buy from Hold with a price target of €51.

For further details see:

Unilever: Upgrading To Buy Despite Headwinds And Challenges