UNLYF - Unilever: Well-Positioned For Attractive Returns

2023-12-04 17:58:13 ET

Summary

- Unilever is a defensive blue-chip company, which can provide stability in your portfolio.

- The company currently offers an attractive dividend yield of almost 4% and is significantly higher compared to its peers.

- Unilever is well-positioned for a turnaround, which could result in increased profitability and further dividend growth.

- Based on my own discounted cash flow analysis shares are 3.5% undervalued.

Investment thesis

Unilever PLC ( UL ) is a famous European consumer staple giant that has been around since the beginning of the 18th century. Over the years they grew tremendously and they have built an amazing product portfolio with lots of famous brands. As a dividend growth investor I like businesses that generate predictable growing profits which result in predictable growing dividends. When it comes to long-term dividend growth UL is no exception.

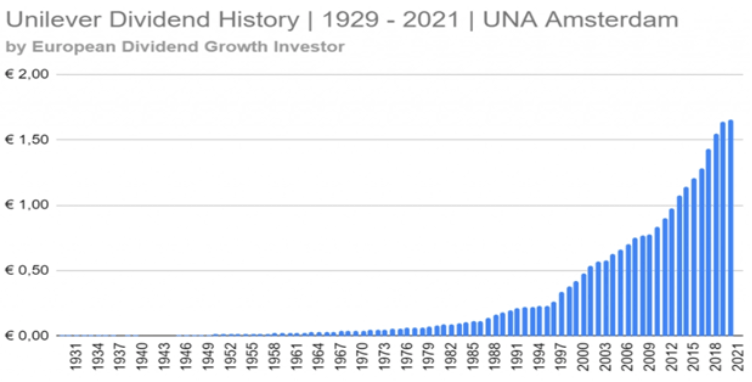

UL dividend history (europeandgi.com)

{kind=link}

However, the last three years the dividend per ordinary share (euro) literally went nowhere. During the last 5-10 years UL also underperformed significantly compared to peers like The Procter & Gamble Company ( PG ).

{kind=link}

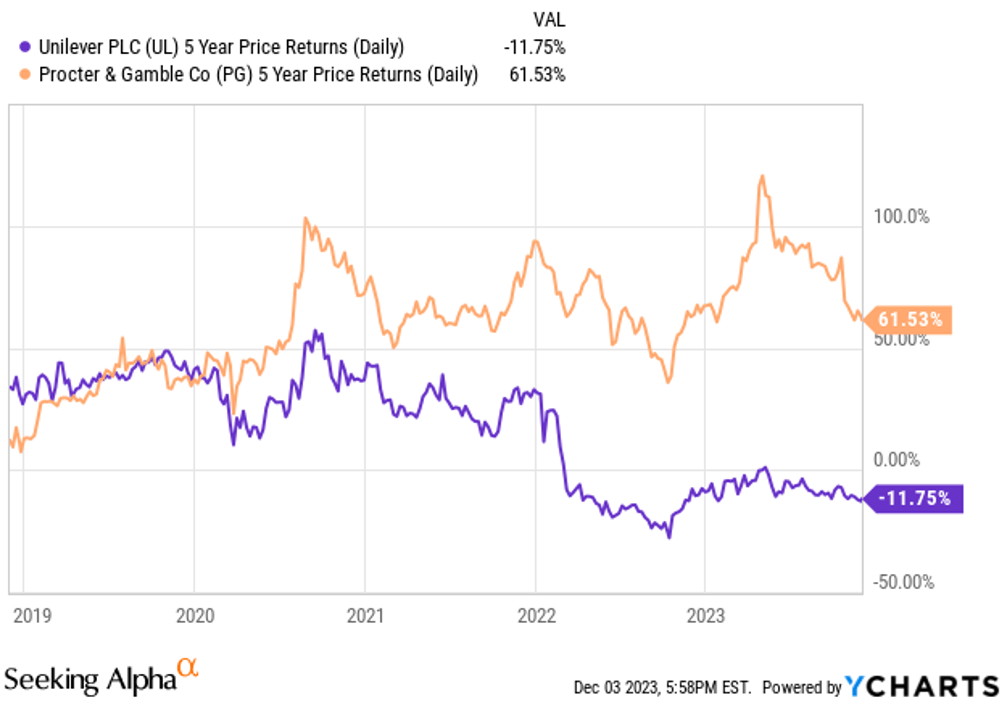

On the 17th of May I wrote an article about ((UL)) as a potential dividend turnaround investment . Since the article has been published, the share price went down almost 10%.

Share price development (Seeking Alpha)

Since then the share price also dropped below my calculated fair value. This was a great opportunity for me to revisit my investment thesis and I would like to explain why UL could be a great long-term investment opportunity.

So let's begin!

Why Unilever?

So why could UL be a well worth addition to your dividend portfolio?

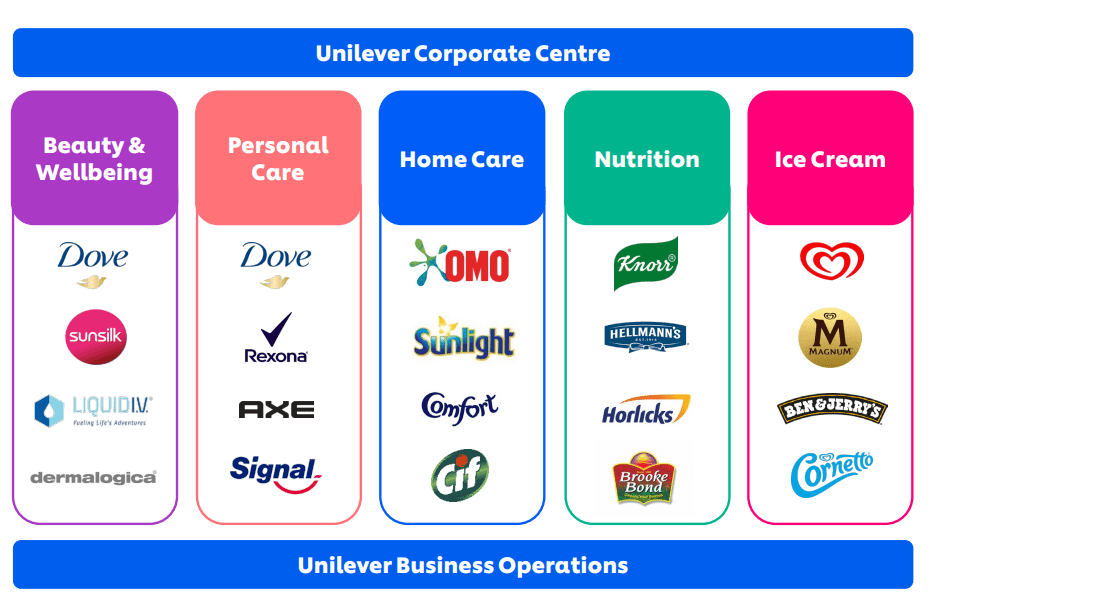

UL is the definition of a defensive blue chip, which can provide stability in your portfolio. The company is well-established and more than 3 billion people worldwide are using products from UL. Their portfolio is packed with lots of recognizable brands and I am sure that many of you have products of UL at home.

Core products (Investor relations)

{kind=link}

Their portfolio is well diversified in terms of different segments and their revenue is well distributed among different continents. What is good to know is that 60% of their revenue comes from emerging markets, which could be a great opportunity for UL to achieve sustainable growth.

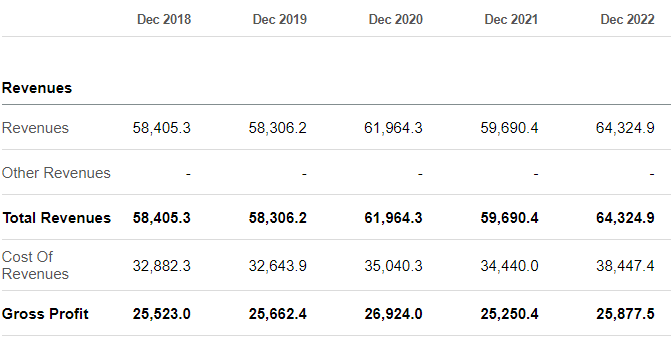

The company also showed decent pricing power during times of higher inflation and this is clearly reflected in the turnover development in FY 2022.

revenue and gross profit development (Seeking Alpha)

{kind=link}

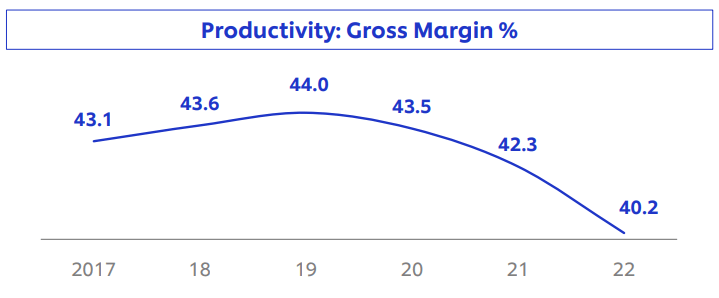

However the company has a difficult time to keep up it's margins, because of the higher cost of revenues.

Gross margin development (Q3 2023 trading statement presentation)

{kind=link}

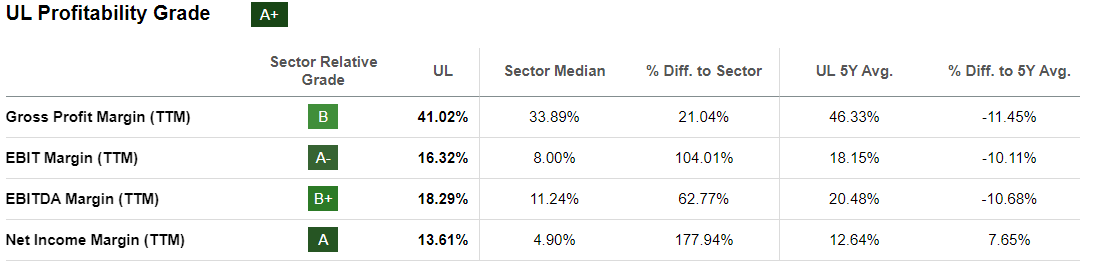

Compared to other consumer staples the margins of UL are solid. A gross margin of 41.02% is higher compared to its sector median of 33.89%. The 41.02% is also 5% lower than its own 5Y average.

UL profitability grades (Seeking Alpha)

{kind=link}

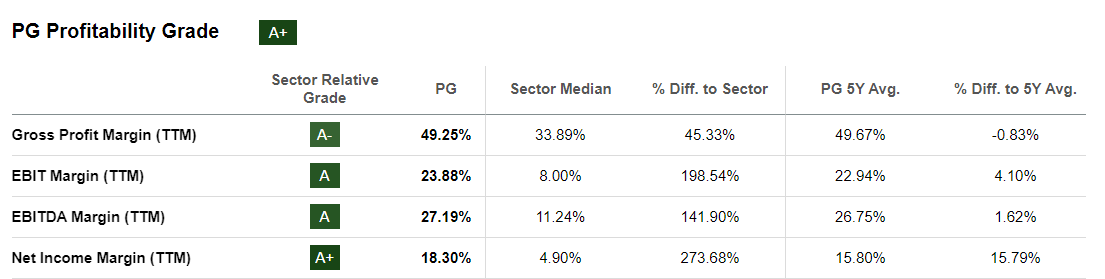

Compare the profitability margins of UL with PG and it is clear that there is a lot to win, but this is part of the turnaround.

PG profitability grade (Seeking Alpha)

{kind=link}

Dividend

UL is a very consistent dividend payer. In 1929 the company started paying dividends and there were only a few years where UL wasn't able to pay a dividend (for example during the second world war).

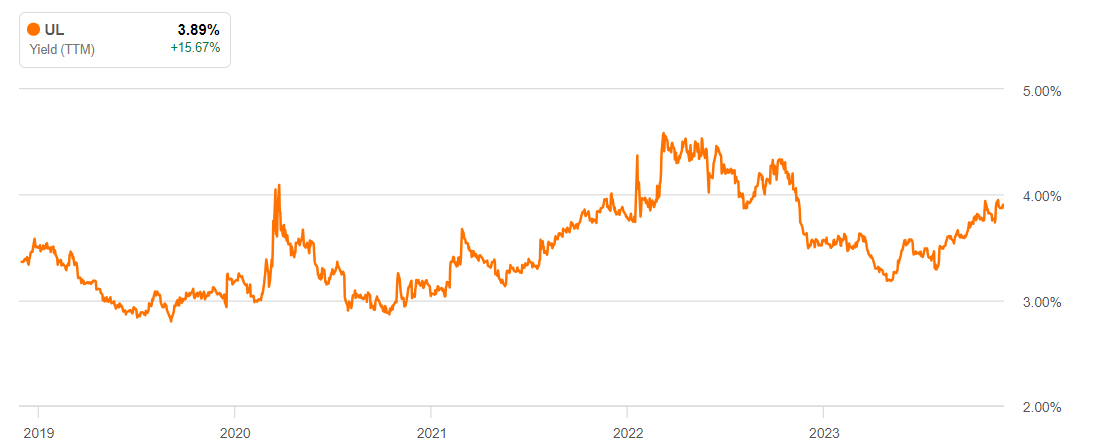

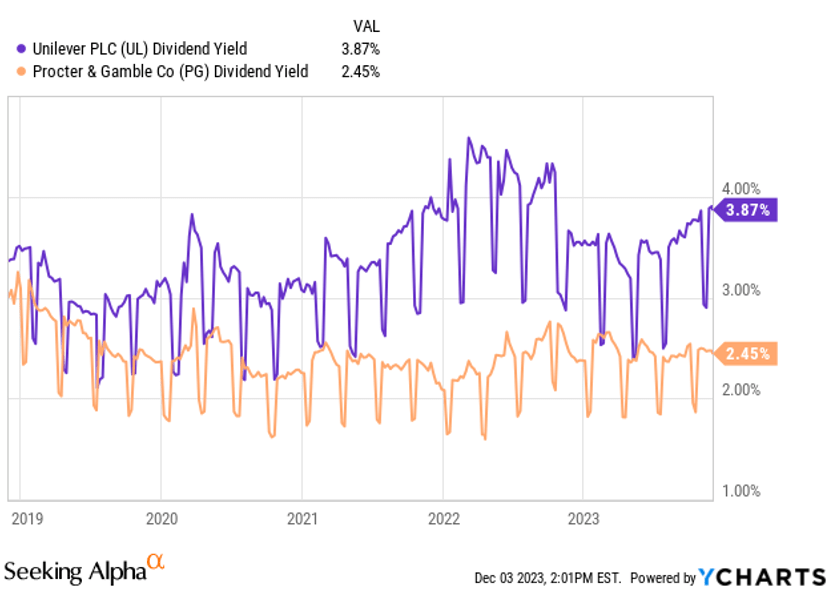

At the moment UL has a dividend Yield of 3.89%, which is high compared to its 5 year average.

Dividend yield development (Seeking Alpha)

{kind=link}

Also compared to its peers the yield is considerably higher, for example PG has a current dividend yield of 2.45%. You don't have to expect dividend growth from UL in the short-term. However, purely from an income perspective, PG needs quite a few years of dividend growth to match the yield of UL.

Dividend yield comparison (YCharts)

{kind=link}

Based on the annual dividend per share ($1.82) divided by the TTM EPS ($3.57) the pay-out ratio of UL would be 50.9%, which seems to be safe. The percentage would be 71% if we take the TTM FCF per share ($2.56). From a free cash flow point of view it would not be wise to further increase the dividend.

If UL can enhance profitability in the future, I expect a further trend in dividend growth for the company. If this is not the case or there is a delay in the turnaround, I expect the dividend to remain flat in the coming years. But once the dividend growth train leaves, the combination of yield- and growth can become really attractive.

Balance sheet and financial health

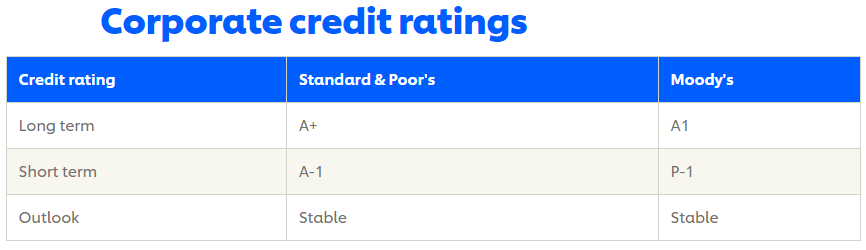

The financial health of the company can be called decent. Using the TTM numbers, UL has a net debt / EBITDA ratio ($26,597.6 / $12,151.9) of 2.18, which is isn't great but not terrible either. I think the company is fully capable to handle its debt. In addition, the company enjoys a long-term S&P credit rating of A+ and a Moody's credit rating of A1.

UL credit rating (Unilever investor relations)

{kind=link}

The change of management

During the last years there were a lot of changes in management. In 2022 billionaire and activist investor Nelson Peltz joined the board, which I think it is a good sign. He has an excellent track record in the consumer staple space and also managed to turn the tide at PG.

In September 2022 former CEO, Alan Jope, has announced his intention to retire. Personally I wasn't a fan of Jope and during his period as a CEO he was not been able to create significant shareholder value. The new CEO Hein Schumacher has just started his journey at the 1st of July. Schumacher was previously CEO of Royal FrieslandCampina and has also worked for The Kraft Heinz Company ( KHC ). Also his experience in emerging markets will come to good use at UL.

A good question to ask yourself is: Do you have enough confidence in management to initiate this turnaround?

H1 2023 results and CEO update.

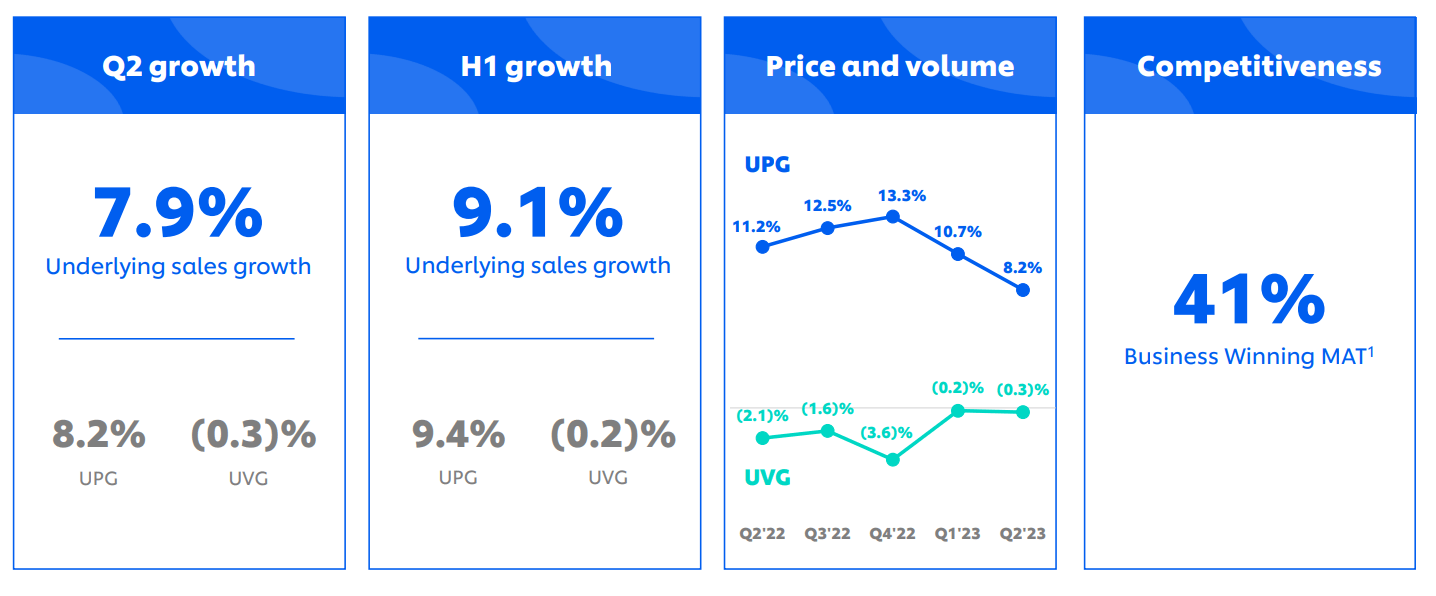

The H1 2023 results of UL were received well by the market.

H1 2023 results (UL presentation)

{kind=link}

The sales growth of H1 was mainly achieved due to higher prices. While they still experience volume decline, the trend seems to be improving.

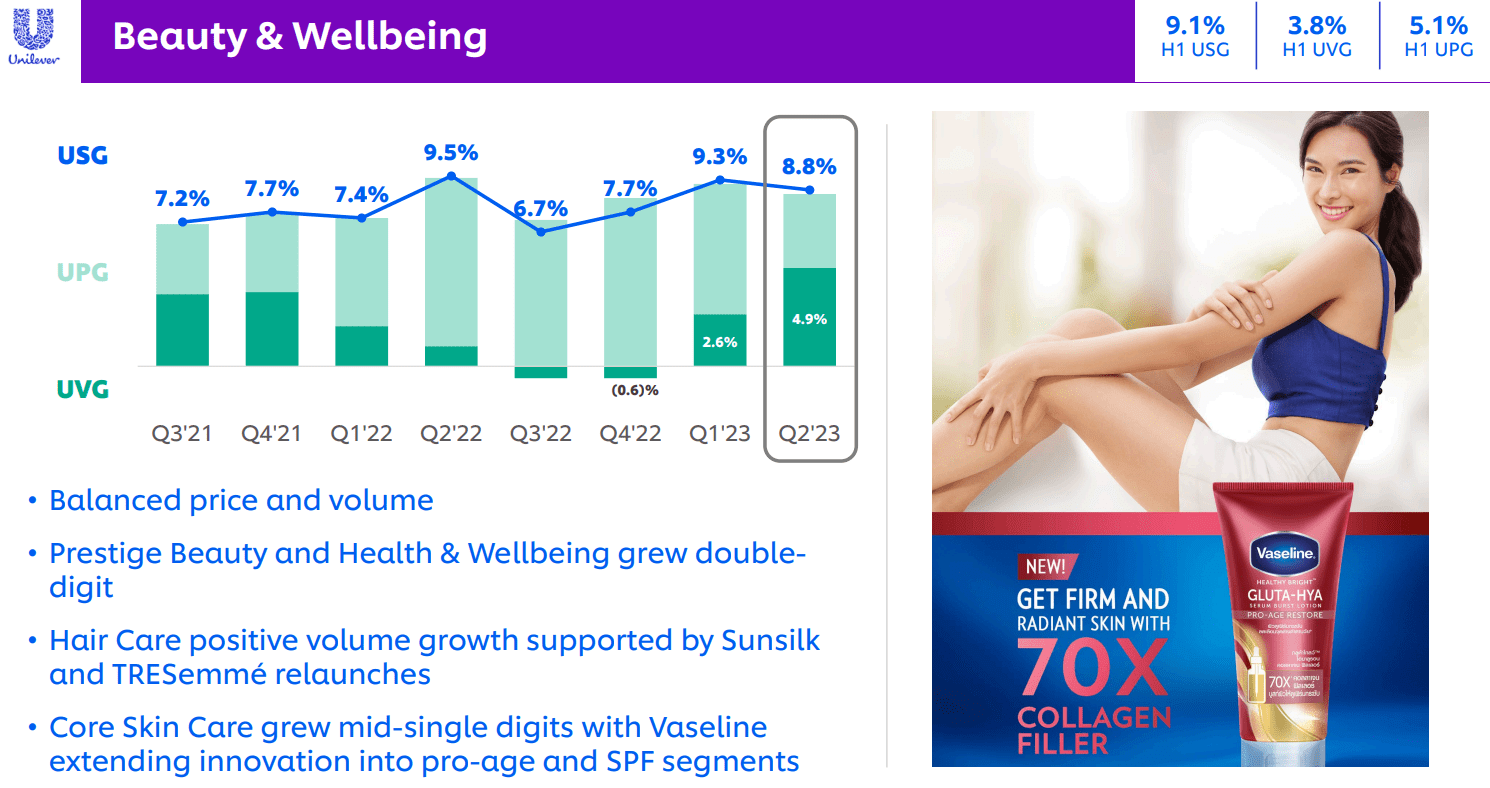

The difference in performance varies considerably per segment. Beauty and Wellbeing was a real standout with a H1 underlying volume growth of 3.8%.

Beauty & Wellbeing segment (H1 2023 Results)

{kind=link}

This is a good development, because Beauty & Wellbeing is also one of the segments with better margins.

The underlying operating margin of 17.1% was also 10bps better compared to H1 2022 and despite negative currency impact the underlying EPS was also improved by 3.9%.

EPS Bridge (H1 2023 results presentation)

{kind=link}

All in all, solid numbers.

I have been looking forward to Unilever's Q3 trading update. Not because of the numbers since they were only revenue related, but it was the first time we could get a good impression of the CEO's new plans.

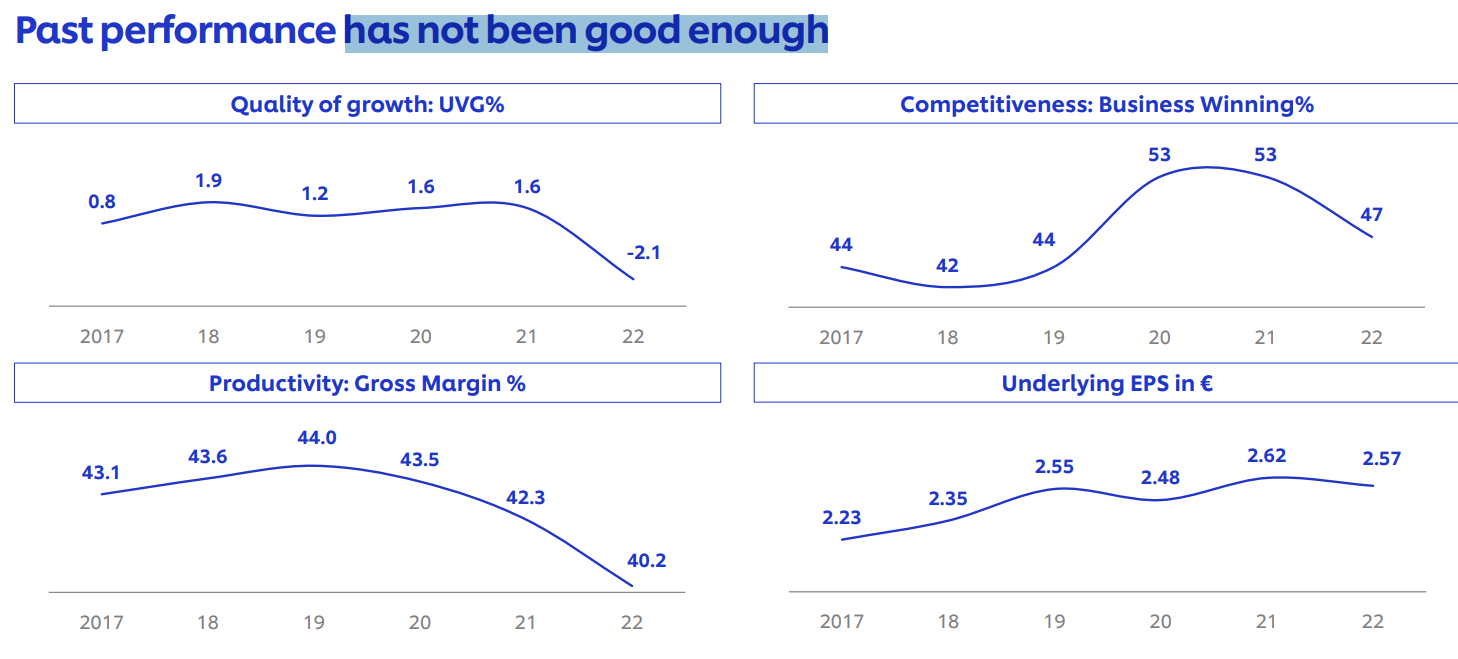

There was plenty of time for Schumacher to talk about its plans to make UL a better performing business. Personally, I liked his Dutch directness. He highlighted the long-term underperformance, lagging gross margin and poor EPS growth.

UL past performance (Q3 2023 CEO update)

{kind=link}

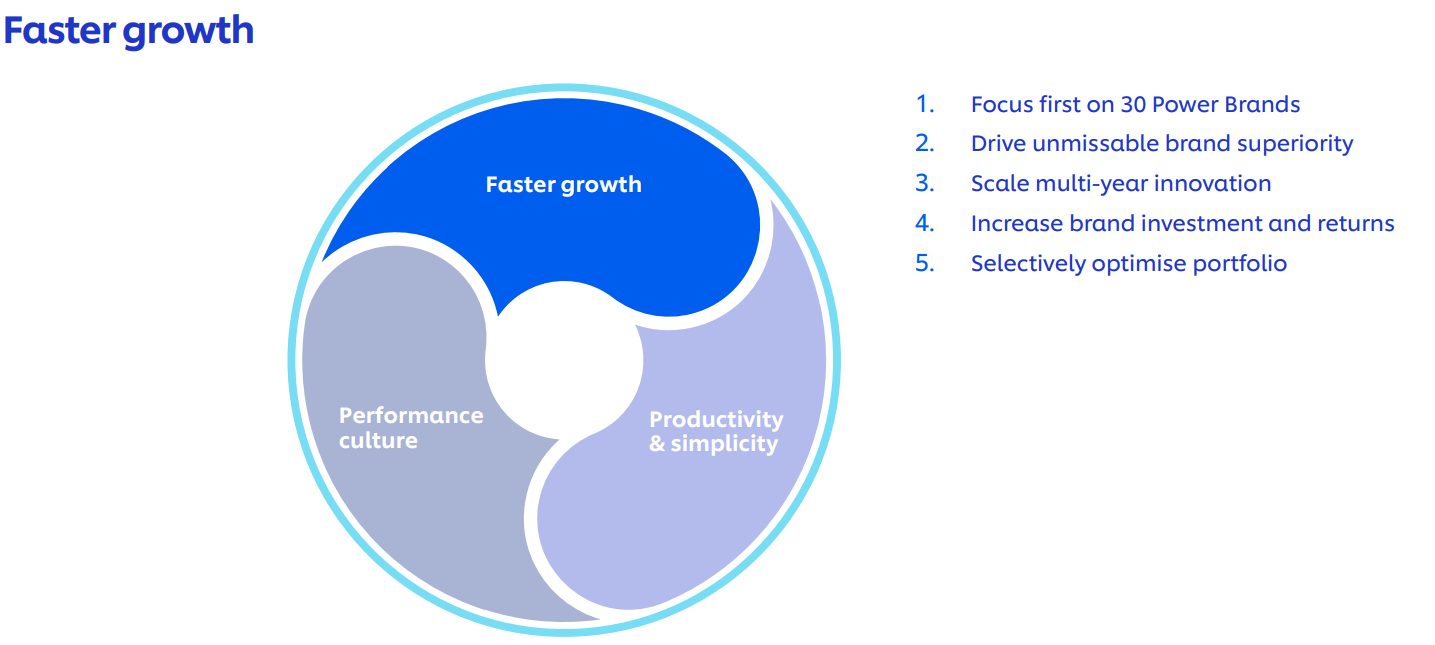

Even more important were the things that needed to be improved.

CEO action plan (Q3 2023 CEO update)

{kind=link}

Faster growth will be their main priority. Their focus will be on the top 30 power brands. What is good to know is that the top brands are growing ahead of the company's average brands (7.5% vs 5.8%). UL is going to increase brand- and marketing spend, which also will be focused towards the power brands and will be more digital oriented.

Another important part of their action plan is to further optimize their portfolio. They have been working on this for some time and this is already somewhat reflected in the company numbers. Segments like Beauty & Wellbeing are already making a more meaningful contribution to UL's profits.

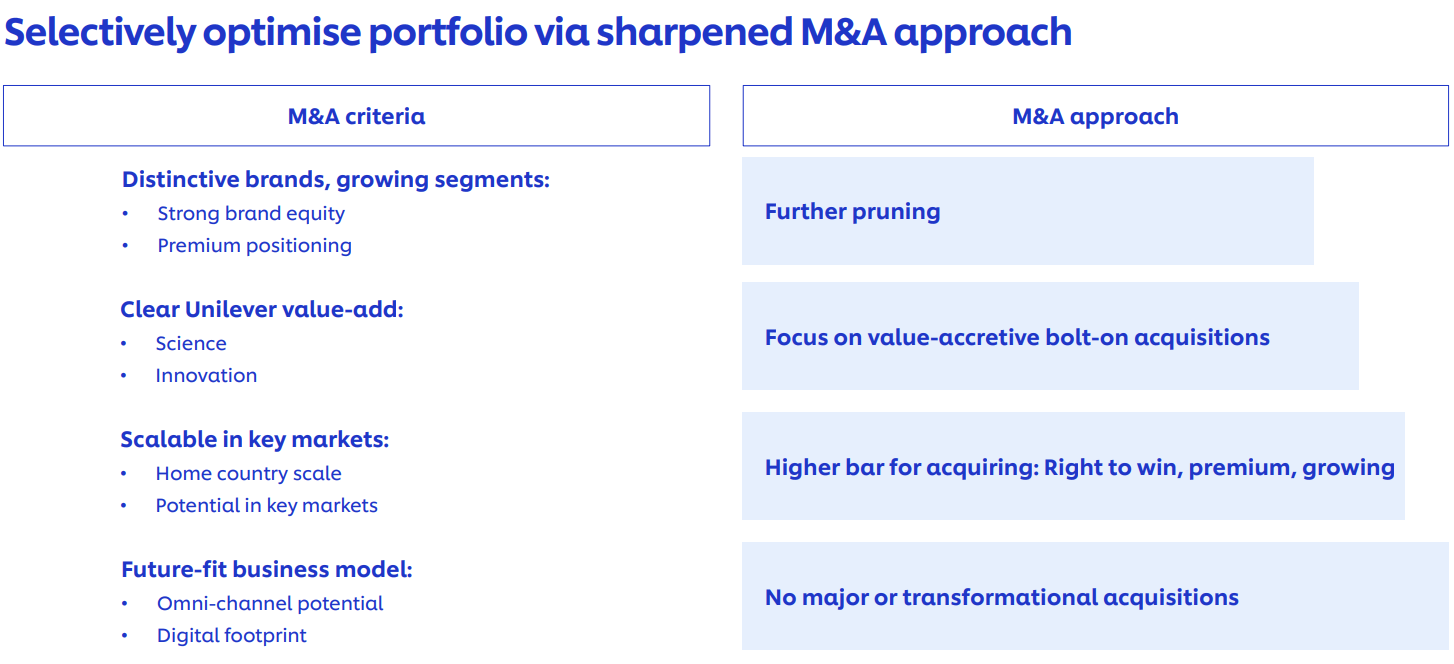

Despite their focus towards organic growth they have also made announcements about the M&A strategy. They will be more focused towards selective bolt-on acquisitions in the high-growth areas, while divesting their less profitable segments.

M&A approach (Q3 2023 CEO update)

{kind=link}

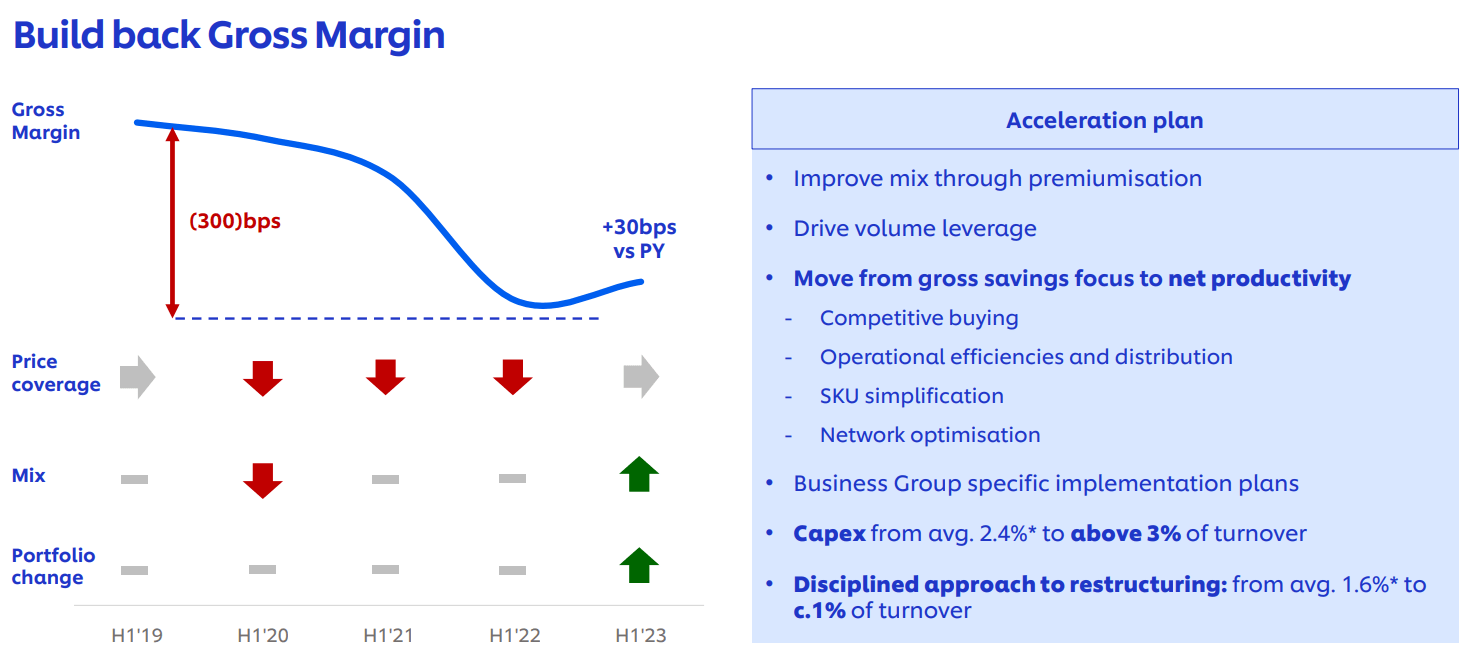

The second point of the plan is to build back gross margin.

Gross Margin plan (Q3 2023 CEO update)

{kind=link}

This is should be one of the sources to fund their investments for further organic growth. This should be done by SKU rationalization, competitive buying of material costs, product reformulations and other value chain interventions.

Finally, the company will lean more towards a performance culture. This starts with bringing transparency on the progress of the turnaround. Terms such as underlying sales growth, ROIC and TSR will now be reported and also included in the long-term incentive program.

In addition, the company will continue to return capital to shareholders. Their dividend payout will be above 60% of underlying earnings and remaining capital will be returned via share buybacks.

In summary, UL's priorities seem clear at this point. However, there are critical comments to be made about the action plan. UL has often developed plans to achieve volume growth through product innovation, but this has not always led to positive results. So what is the difference compared to previous plans? This seems a little bit unclear for now. UL wants to make better use of their strong science and technology platforms, but why haven't they done this before? Maybe they can make a difference by focusing on the power brands? Time will tell.

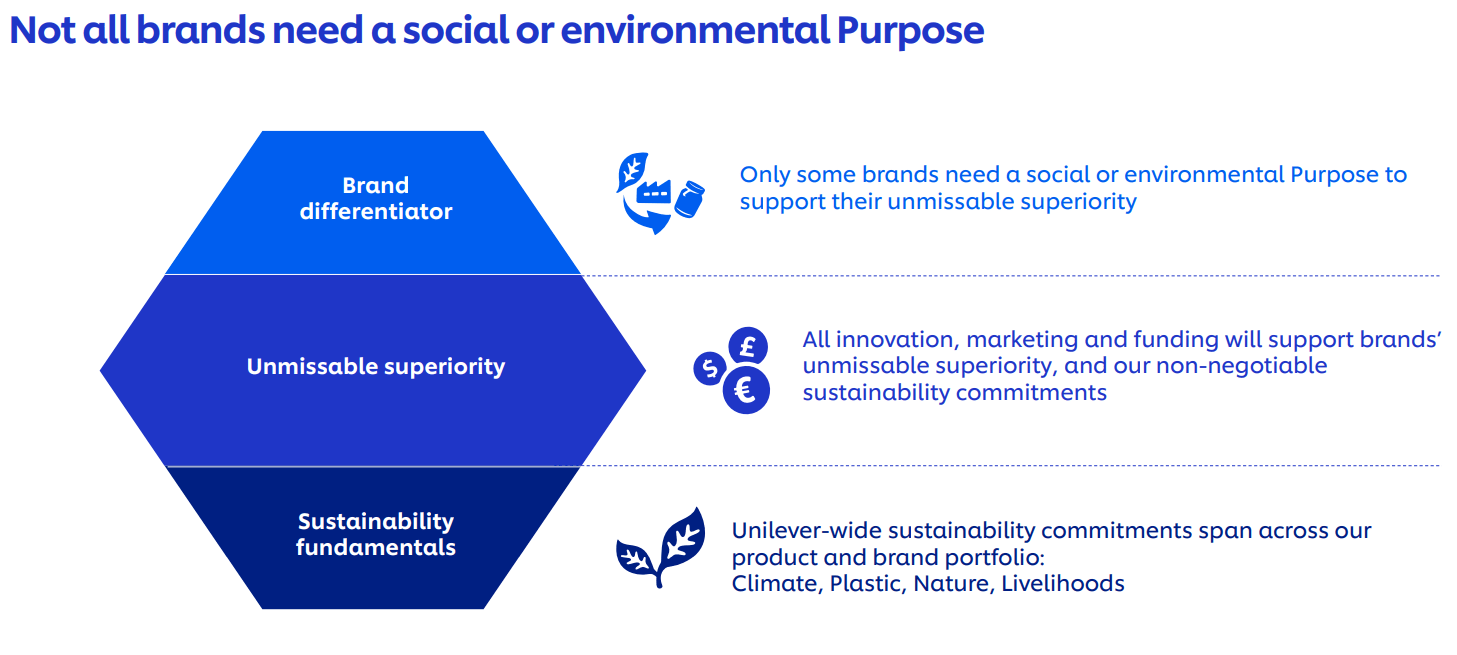

I do think that improvements can be made in the performance culture part, because Schumacher seems to be more focused on this. He also seems to have less affinity with sustainability and more with value creation for shareholders.

UL sustainability (Q3 2023 CEO update)

{kind=link}

Management wants to implement the action plan in a period of 12-18 months and if all goes well, the improvements will be visible in the numbers in this time frame.

Valuation

For the valuation of UL I used discounted cash flow analysis. I used the same free cash flow compared to my previously written article. UL itself is aiming for an underlying sales growth of 3-5%. If the company manages to achieve this and their margins are also improving, the used 5-year free cash flow growth of 5% is in my opinion achievable. For the 5 years thereafter I used a growth rate of 3%, because it's harder to make accurate assumptions over longer periods of time.

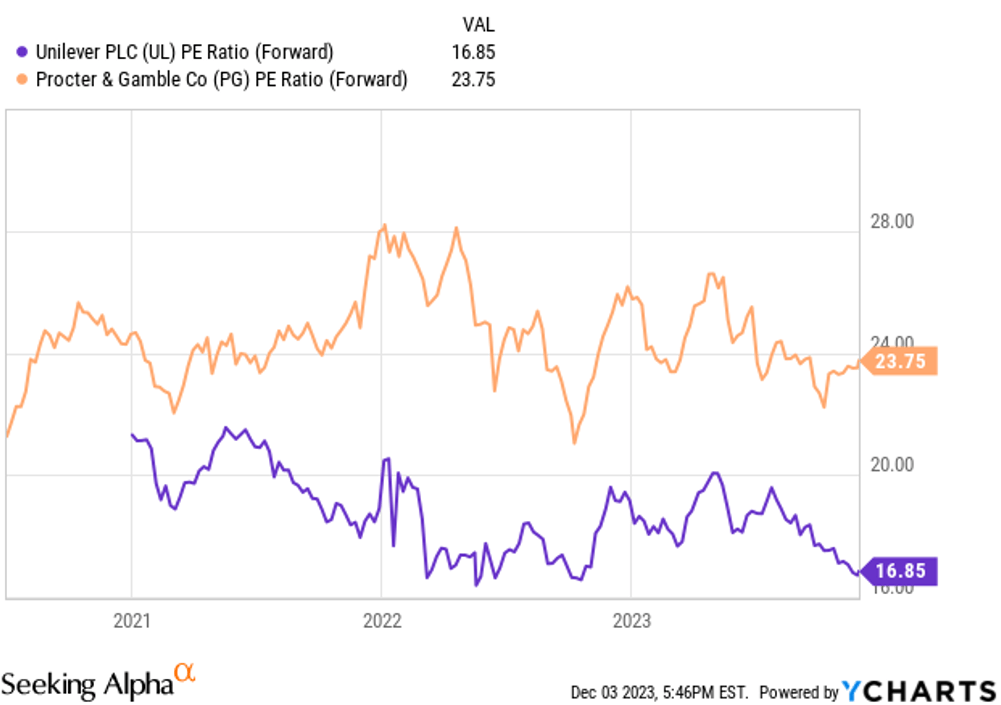

UL has a PE ratio of 17, which is lower compared to PG. I think this is justified, because PG has better profitability metrics and a better balance sheet.

PE ratio development (YCharts)

{kind=link}

However, if UL's profitability increases, multiple expansion is certainly possible. With this in mind a terminal multiple of 20 was used, which is around the 5-year pe average .

I used a discount rate of 10%, because I want an annual return close to the 10 percent range.

Discounted cash flow analysis (Google spreadsheets)

This comes to a fair value of $49.62 per share. At the moment the share price of UL is $47.94. Compared to my fair value it is 3.5% undervalued.

Conclusion

UL is an established name in the consumer staple landscape. However, it has performed poorly on the stock market in recent years and total returns have been disappointing. On the other hand, as an investor it is important to look to the future and I see plenty of reasons to see UL as an attractive investment. UL has an excellent position in emerging markets and an attractive dividend yield compared to its peers. In addition, there are also opportunities for multiple expansion and possible future dividend growth if the new CEO manages to properly implement his turnaround plan. There is still some vagueness in the plan to achieve growth, but we will see how this will work out in the next 12-18 months.

All in all, I think UL is undervalued and is in my opinion an attractive risk/reward investment. However, it remains important to keep an eye on the upcoming earnings to evaluate whether management interventions actually lead to improving profitability and return ratios.

For further details see:

Unilever: Well-Positioned For Attractive Returns