UNB - Union Bankshares: Highly Profitable Regional Bank With Attractive Dividend Yield

2023-05-15 14:06:34 ET

Summary

- Union Bankshares has a multi-decade track record of delivering positive bottom-line results.

- The company is paying a well-covered dividend with a yield of almost 7%.

- Long-term Returns on Equity are significantly higher than the industry average.

- Shares trade at a discount to their fair value.

Union Bankshares, Inc. ( UNB ) is a well-capitalized regional bank with a high-quality loan portfolio and well-structured deposits. The company since going public in 1999 managed to slowly and profitably grow its business without recording a loss in any year. The company is paying a well-covered dividend with an attractive 7% yield based on the current stock price.

I rate the stock as a "buy" because according to my valuation, the shares are trading at a discount to their intrinsic value and in my opinion offer a potential for capital appreciation and dividend income for investors.

Business Overview

Union Bankshares, Inc. is a one-bank holding company with Union Bank as its sole subsidiary. It was incorporated in the State of Vermont in 1982 to serve as a holding company for Union Bank. it provides full retail, commercial, municipal banking and wealth management services throughout its 18 banking offices, three loan centres and several ATMs spread over northern Vermont and New Hampshire. The company has 188 full-time employees.

They compete with local and regional commercial banks, credit unions and many other financial institutions. To differentiate themselves from larger financial institutions the company emphasises personal service, local promotional activities and community service. They also engage in educational programs to promote sound personal financial habits. One of the examples is their "Save for Success" program which aims to educate children. They target small to middle-market businesses and residential customers that tend to be under-served by larger institutions. The company is doing this by promoting an increased level of personal service and expertise within the community.

Union Bank profits from interest and fees on loans and earnings coming from money held in investment securities mostly long-term U.S. government bonds and mortgage-backed securities ((MBS)).

They take deposits to fund those investments. Some deposits are noninterest-bearing and on others, the company must pay interest to retain them. Other expenses come from salaries, wages, health insurance and other employee benefits.

The most important measure of profitability for a bank like Union is the spread between interest earned on loans and other securities (interest-earning assets) and the interest paid on the deposits, brokered deposits and other borrowings. This metric is called net interest income and it is highly dependent upon the level of interest rates and the degree of change in those rates.

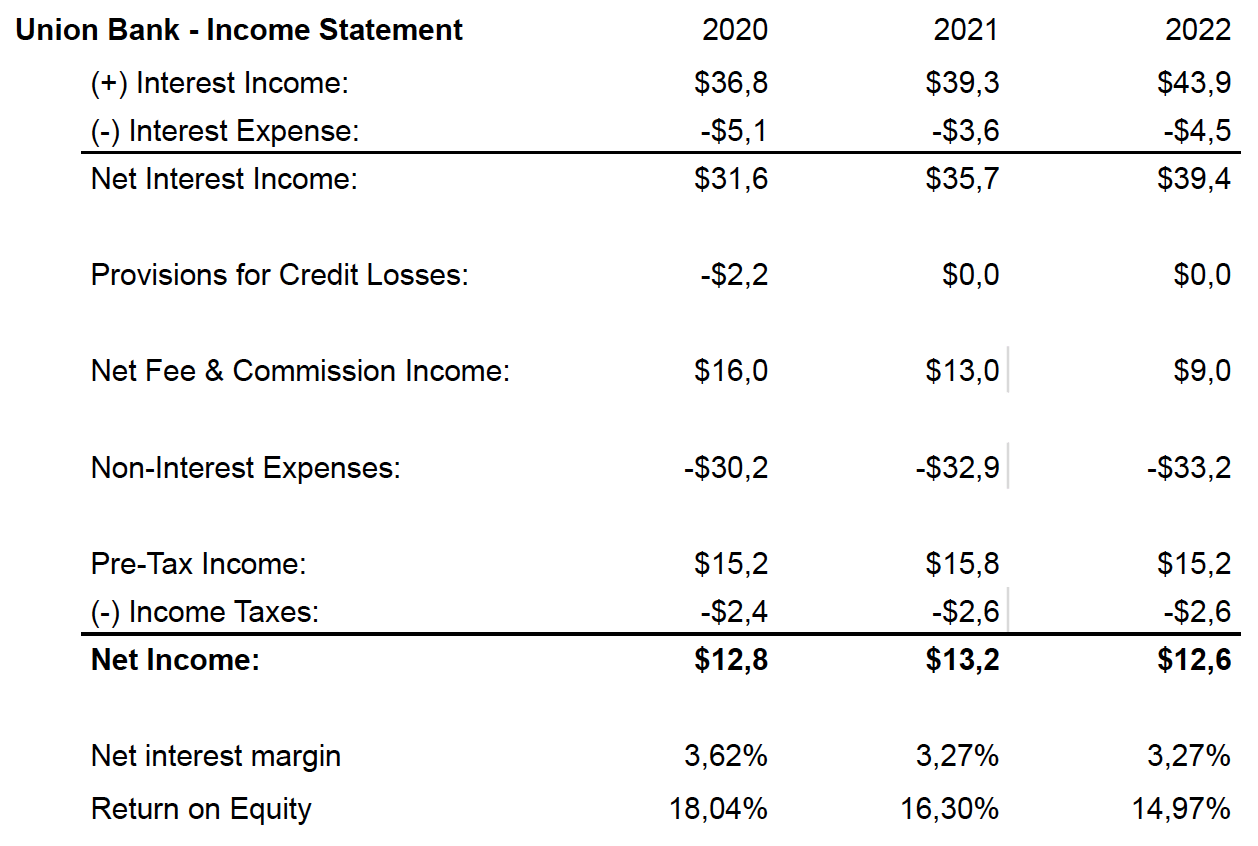

Union Bank's Income Statement (Author's Calculations based on 2022 Annual Report)

{kind=link}

Over the last three years, the Net Interest Margin for Union Bank averaged 3,39% and was slightly higher than the industry average during this time period. It recorded a regression in recent years in line with other community banks in the industry.

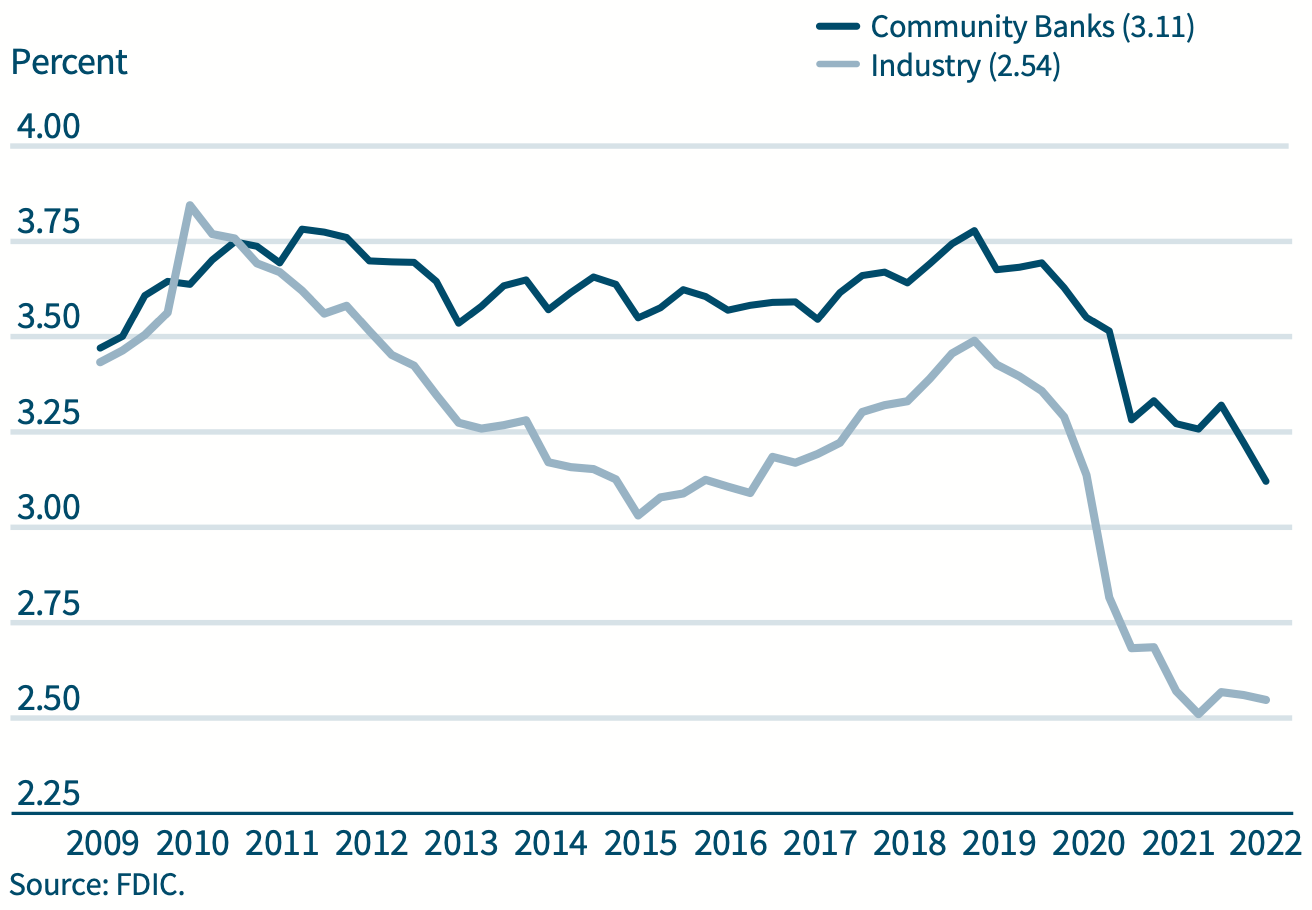

Net Interest Margin for the Community Banks and the industry average, 2009-2022 (FDIC)

{kind=link}

According to the data presented in the graph above, smaller community banks like Union Bank presented higher and more stable net interest margins during the last decade.

{kind=link}

Moreover, the company over the last three years, averaged Return on Equity ((ROI)) of 16,44%, which is substantially above the industry average of 11,29% over the same time period.

Overall, Union Bankshares, Inc. based on the profitability measures is an exceptionally well-run bank that earns above-average returns on its investments and during its history presented an ability to withstand the pressure coming from falling and rising interest rates and recorded consistently growing bottom line.

Financial Condition

As the profitability of the bank seems to be superb, now it is necessary to assess whether the bank is also safely run. Does the company maintain the necessary regulatory capital buffers to absorb potential future losses?

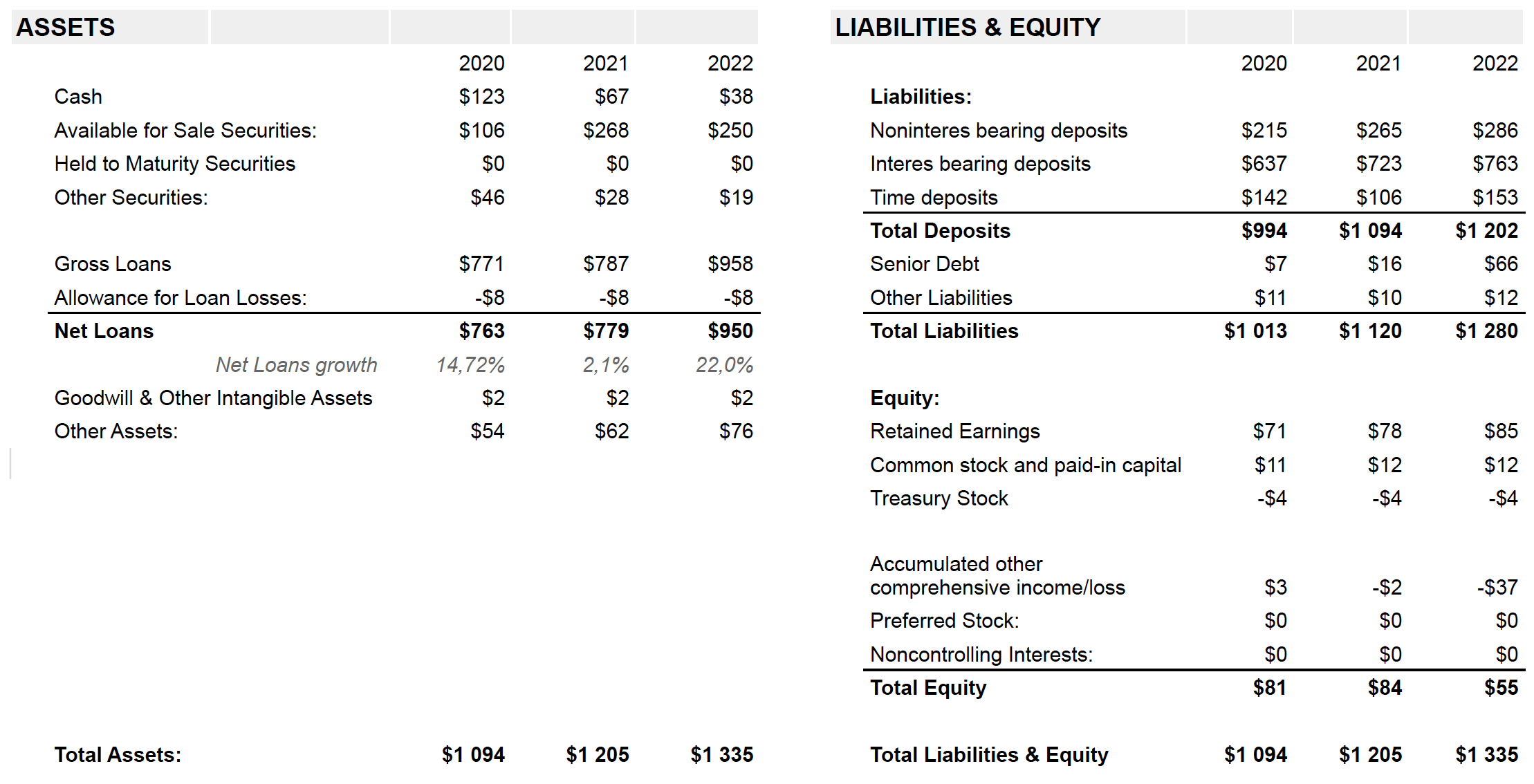

Union Bankshares, Inc. Balance Sheet (2022 10-K and 202110-K)

{kind=link}

The asset side of the balance sheet consists primarily of Loans, Securities Available for Sale and Cash. Over the last three years, loans grew substantially from $763 million to $950 million. Also, the amount of investment in securities more than doubled from $106 million in 2020 to $250 million at the end of 2022. These securities are recorded on the balance sheet at their fair market value. The company doesn't hold any Hold-To-Maturity ((HTM)) securities so there is no risk of unrecorded losses that are not visible on the balance sheet.

The deposits are the primary source of funds for the assets. At the end of 2022, the company had $1,202 billion of deposits of which $286 million - 24% - were noninterest-bearing. The higher the number of such deposits the better, because it is free money on which the company can earn interest.

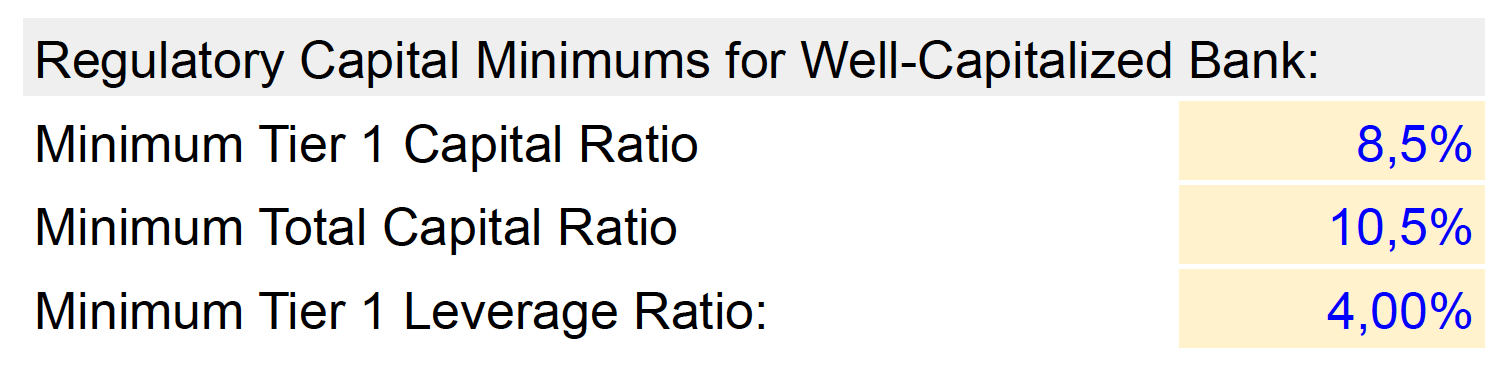

Banks must comply with numerous regulatory requirements in order to be able to protect depositors from any losses, but also to be allowed to pay dividends to their shareholders. The most important requirements concern the minimum equity capital - Tier 1 Capital - as a percentage of the bank's risk-weighted assets.

{kind=link}

As the company is taking new deposits and wants to offer new loans it is also obliged to maintain the above-listed equity reserves. Thus, it must retain some portion of its profits to fulfil those requirements. The part of net income that the financial institution must retain in order to grow can be treated as a capital expenditure and I am going to use this approach to forecast future cash flows in the next part of this article.

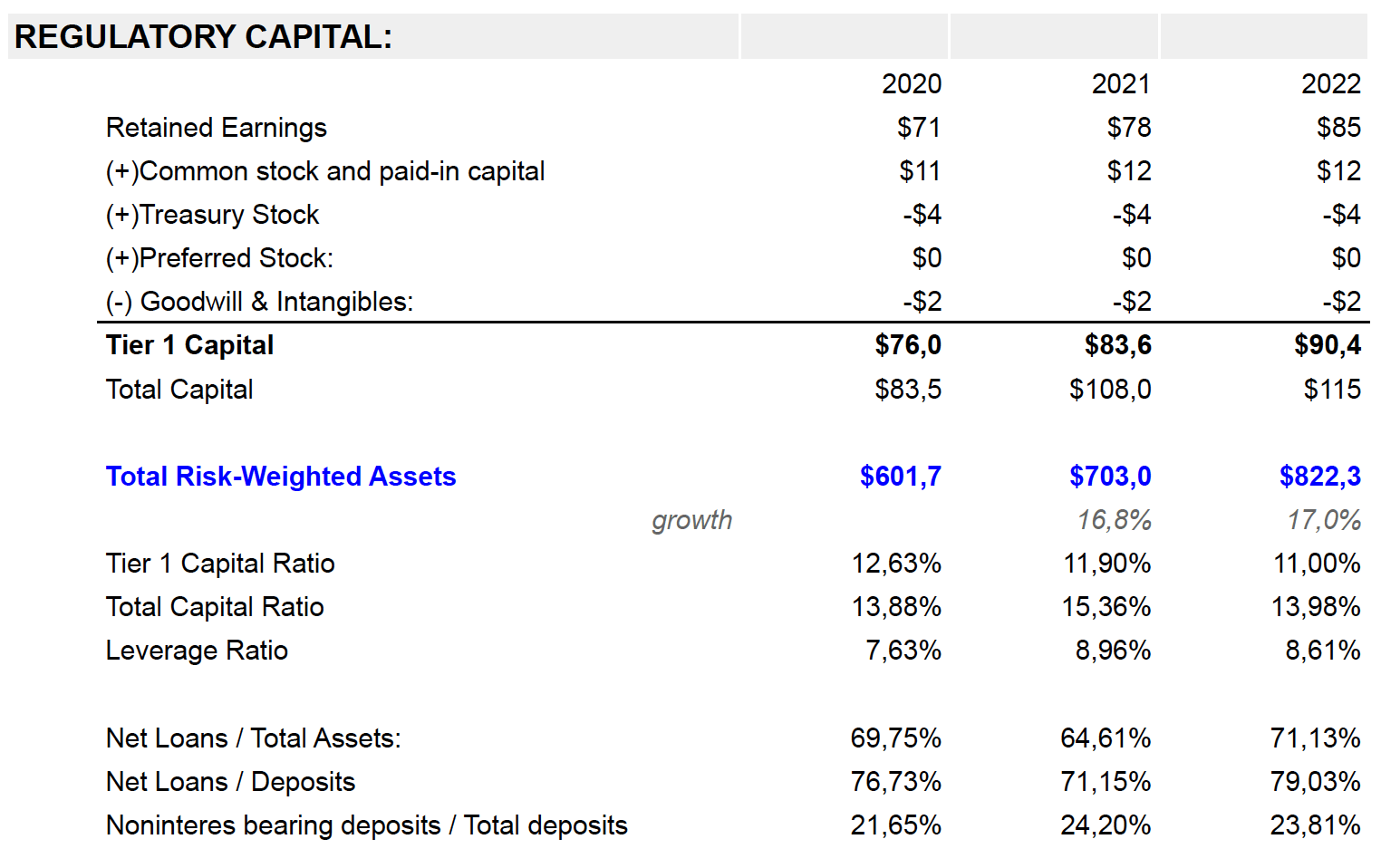

In the table below I calculated Tier 1 Capital for Union Bankshares, Inc. to see if this bank is maintaining necessary capital reserves. I used the following formula:

Tier 1 Capital = Retained Earnings + Treasury Stock + Common Stock and Paid-in Capital + Preferred Stock

Regulatory Capital and key financial ratios (Author's calculations)

{kind=link}

According to this calculation, it looks like Union is complying with all regulatory requirements and also has a substantial buffer built up. However, I noticed that the company is not including in the Tier 1 Calculation the Accumulated Other Comprehensive Income/Loss ((AOCI)) coming from their unrealized gains from investment securities.

The explanation in the 10-K in the Capital Adequacy Guidelines section is as follows:

The FDIC and other federal bank regulatory agencies adopted a final rule for leverage and risk-based capital requirements (..) The final rule also required accumulated OCI to be included for purposes of calculating regulatory capital unless a one-time opt-out election was made during the first quarter of 2015. The Company and Union both made the election.

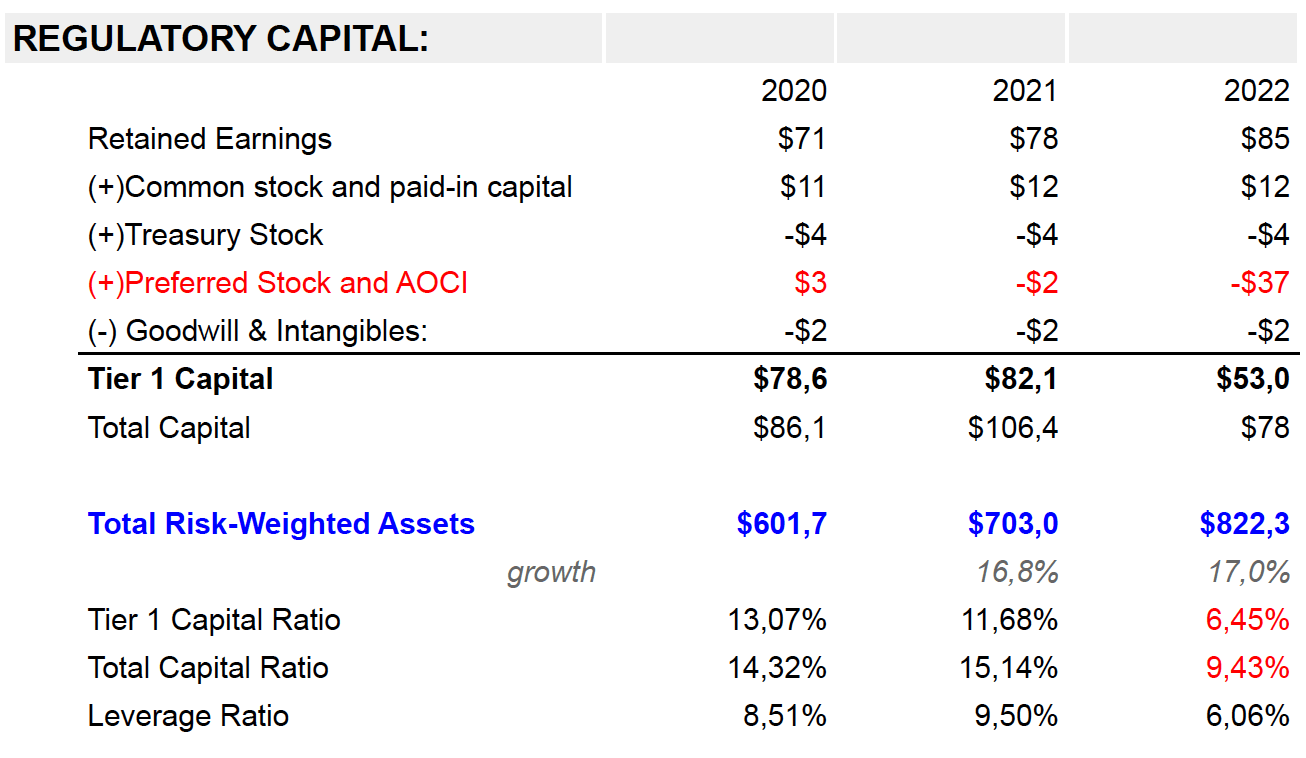

FDIC rule about Accumulated Other Comprehensive Income from 2015 allows the companies like Union Bankshares, Inc. not to include this metric in Tier 1 Capital. In my opinion, for the purpose of this analysis it is important to understand what would happen with Tier 1 Capital Ratios had we included AOCI or had the unrealised losses had to be realised.

Regulatory Capital calculation including AOCI (Author's Calculations)

{kind=link}

In this case, the Bank would not fulfil the requirements for a well-capitalized Bank and could be restricted from paying dividends until the regulatory capital was restored by retaining a higher portion of the company's earnings or by raising additional equity.

I consider this scenario to be unlikely and so does the management. They mention this in their November 2022 Shareholder Letter. However, in my opinion, this is the only major risk that could discourage potential investors from investing in this company.

The recent failure of Silicon Valley Bank showed that the panic and money withdrawal caused by lack of thrust can severely damage any bank. For this, reason in my calculation of the intrinsic value I decided to account for the risk of possible bank failure.

Valuation

{kind=link}

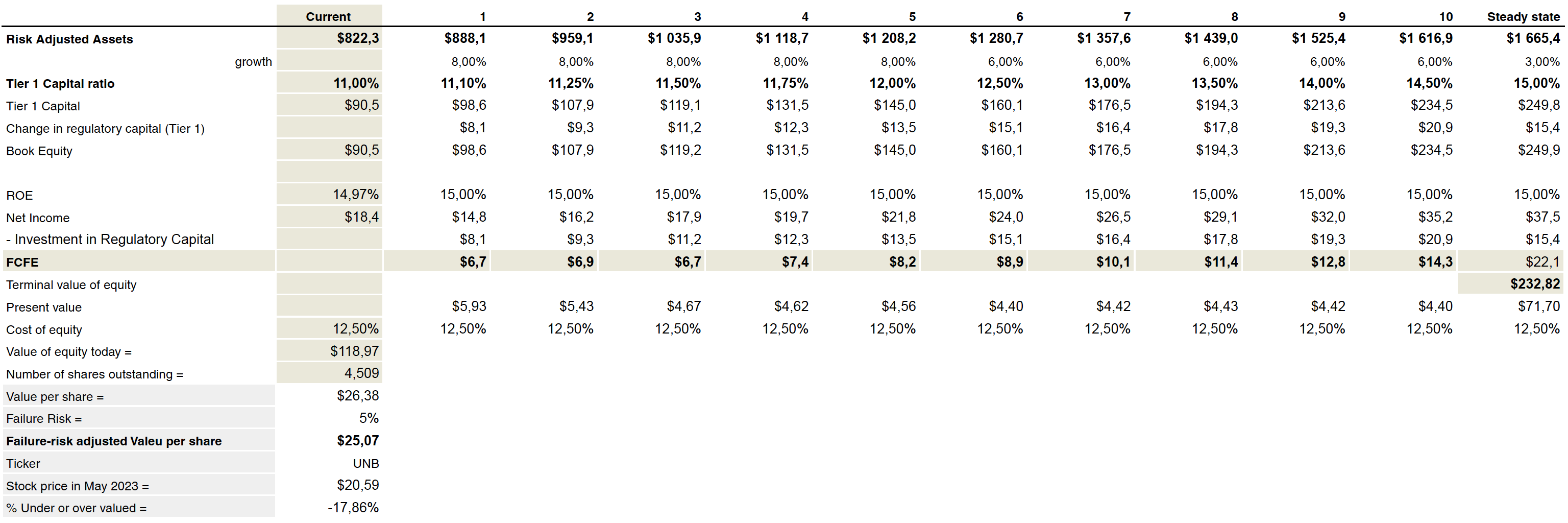

To calculate the intrinsic value of Union Bankshares, Inc. I assumed that the company is going to grow its Risk Adjusted Assets by 8% over the next five years and 6% in the following five years.

I also assumed that the company is going to improve its Tier 1 Capital ratio from the current 11% level to 15% in the pursuit of higher stability. To fund this improvement they are going to retain a portion of their net income which is going to boost the Book Equity.

To come up with future Net Income numbers I assumed that the Return on Equity is going to be similar to the historical numbers of 15%. After subtracting, the already mentioned, investments in regulatory capital I calculated Free Cash Flow to Equity which I discounted at the Cost of Equity of 12.5%. I assumed a failure risk of 5%.

My intrinsic value for Union Bankshares, Inc. is equal to $25,07 per share which means that the company's shares are currently undervalued by around 18%.

In my opinion, this is a well-run bank and the issue of unrealised losses on investment securities is not a "red flag" as this is an industry-wide phenomenon. In the end, I don't think that these losses will be realised, but they are going to be held till maturity and will be paying interest each year to the company.

Please, share your opinion about this in the comment section below. I would like to know also your opinion.

For further details see:

Union Bankshares: Highly Profitable Regional Bank With Attractive Dividend Yield