UNB - Union Bankshares: Uniting Growth And Sustainability Makes The Stock Enticing

2023-05-16 19:22:23 ET

Summary

- Union Bankshares, Inc. had a nice start with its steady revenue growth and decent margins.

- Its excellent financial positioning remains one of its sturdy cornerstones.

- Current market prospects remain quite pessimistic right now, but potential tailwinds are present.

- Dividends remain exciting, given the consistent payments and high yields.

- The stock price downtrend continues, making it a good bargain.

The banking industry deals with a difficult market environment. Macroeconomic volatility and softening demand are some headwinds they are facing. Despite this, many small and mid-sized banks are still maneuvering their core operations very well. Union Bankshares, Inc. (UNB) is one of the perfect examples. It started the year strong with its stable performance. It sustained its revenue growth while staying viable.

Margins contracted, but actual returns remain decent. Also, it maintained adequate capacity to sustain its operations. Its stellar Balance Sheet shows impressive liquidity levels and sustainability. Unsurprisingly, it continues to raise its dividend payments with enticing yields. Meanwhile, the stock price decrease makes it quite divorced from the fundamentals. But its evident undervaluation gives it high upside potential.

Company Performance

Banks like Union Bankshares, Inc. have a higher macroeconomic risk exposure these days. They operate in a highly volatile market landscape. Recession fears intensified after the collapse of banks of different sizes. Indeed, the banking crisis must not be discounted. The most popular was the discontinuation of the Silicon Valley Bank. Despite this, some banks try to prove their capacity to stay afloat amidst market disruptions. Their operations may be hammered, but rebound potential and portfolio management are still sound. UNB continues to show it can withstand external forces hindering its growth potential.

Its operating revenue amounted to $13.04 million , a 34% year-over-year increase. More importantly, there was a consistent increase in revenues in five quarters. As a banking company, its revenue streams are loans and investments. Both of these earn in the form of interest income. Loans remained its primary driving force, comprising over 80% of the total revenues. The remaining portion was composed of its investment securities and deposits in other banks.

We must note that interest rate hikes were a crucial part of it. They led to higher loan yields and raised interest income on loans. Yet, it is more important to look at its operational strategies that used the situation to its advantage. First, its active loan repricing helped it improve its flexibility with its loans. It made loan demand, volume, and yields more manageable despite higher interest rates. Second, it maintained efficient and prudent loan portfolio diversification.

There was a proportionate split among its loan compositions. In many banks of its size, about 70% of loans came from C&I and CRE loans. But UNB’s CRE and C&I loans only comprised 43% of the total loans. The remaining portion came from residential with 37%, construction with 11%, and municipal loans with 9%. What was more noticeable was that the nature of its loans was mostly real estate loans.

In fact, 87% of loans were commercial, residential, and construction real estate loans. It can be risky, given the potential changes in the real estate market. But there are many opportunities present in the market, which we will discuss later. Also, real estate loans can have higher yields as properties remain a macroeconomic staple. Third, it kept its conservative approach to loan growth to minimize the risk of defaults and delinquencies. We can associate it with its loan repricing and timely adjustments in credit loss provisions.

{kind=link}

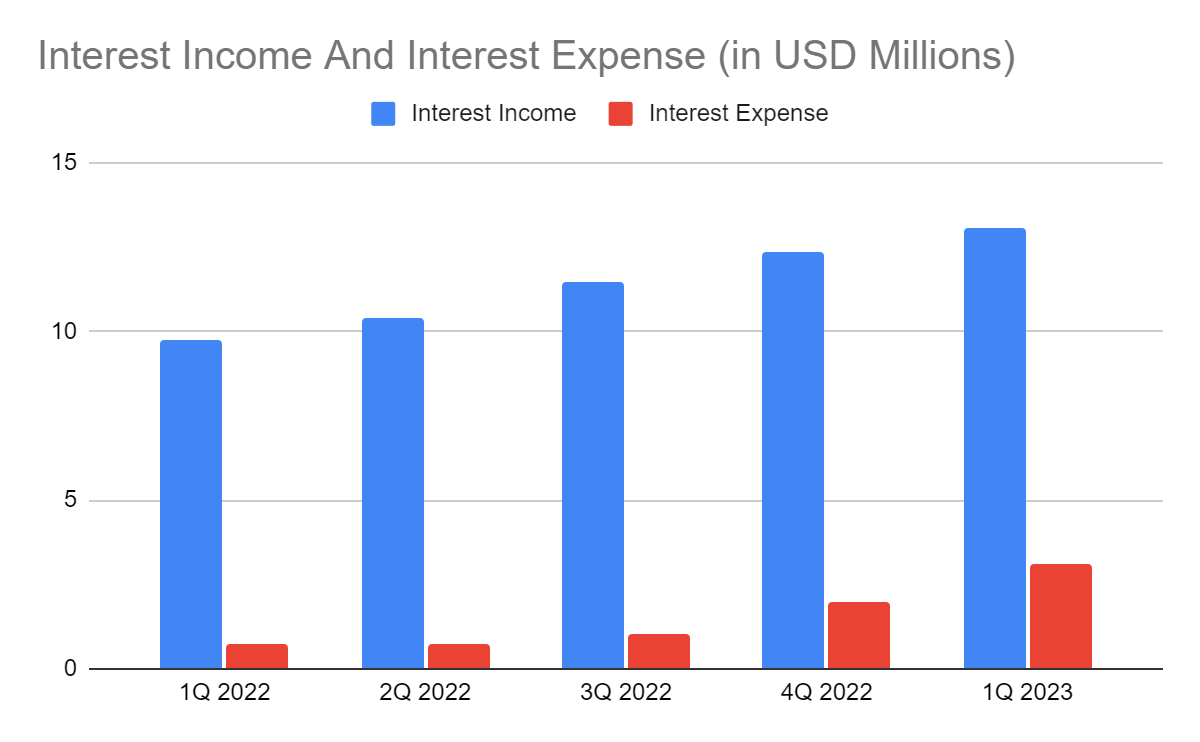

Interest Income And Interest Expense (MarketWatch)

Its prudent investment portfolio management also helped drive its steady revenue growth. Investment securities and deposits comprise 14% of its interest income. As such, their composition was also crucial for the company. Thankfully, 97% of its investment securities were backed by government and quasi-government agencies. They came in the form of bonds, notes, and debentures, And these securities are more suitable in a high-interest environment. They can have better yields and hedges against valuation decreases.

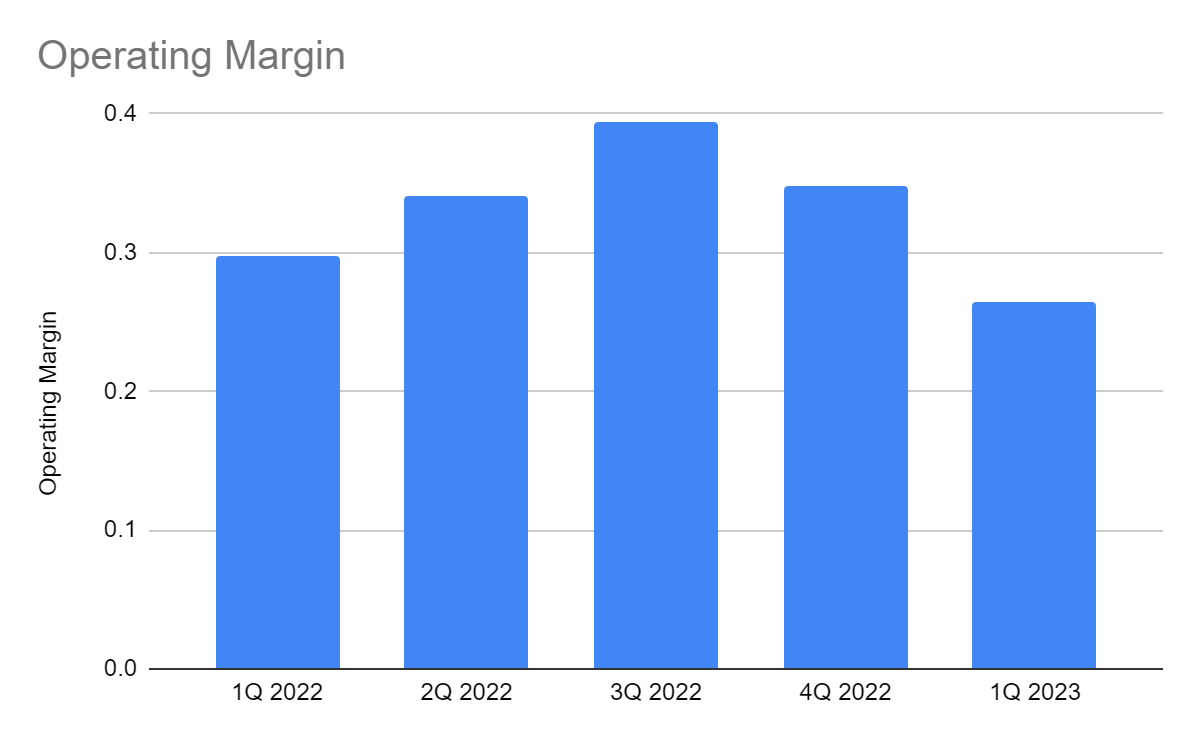

Likewise, higher inflation and interest rates also had an unfavorable impact. They made deposits and borrowings costlier, leading to higher interest expenses. In only a year, interest expenses more than quadrupled. And from just 8%, the percentage of interest expense to interest income rose to 24%. The trend was similar in its non-interest segment. Both the non-interest income and expense increased, but the latter was more substantial. Unsurprisingly, the operating margin decreased from 29% to 26%. But the actual operating income still increased from $2.9 million to $3.4 million. It was still fruitful since UNB generated higher returns to fund its core operations.

{kind=link}

Operating Margin (MarketWatch)

This year, the company may face similar challenges. Interest rate hikes may still increase and affect yields on loans, investments, deposits, and borrowings. Despite this, there are still market opportunities as inflation starts to relax. The thing is, the company must determine how to handle and diversify its portfolio to stabilize its performance. We will discuss it further in the following section.

How Union Bankshares, Inc. May Stay Afloat This Year

The banking crisis remains intense as recession fears continue. Despite this, we saw how Union Bankshares, Inc. handled its operations with caution. But before it can heave a sigh of relief, it must account for every risk that may disrupt its performance. Interest rate hikes remain the number one problem in many banks. While it led to higher loan yields, it already reached the point where risks equate to benefits. If it continues, deposits and borrowings may become more expensive. Lenders and investors may get discouraged, leading to lower yields. Defaults and delinquencies may increase. The only consolation we have is that interest rate increments appear to have already cool down.

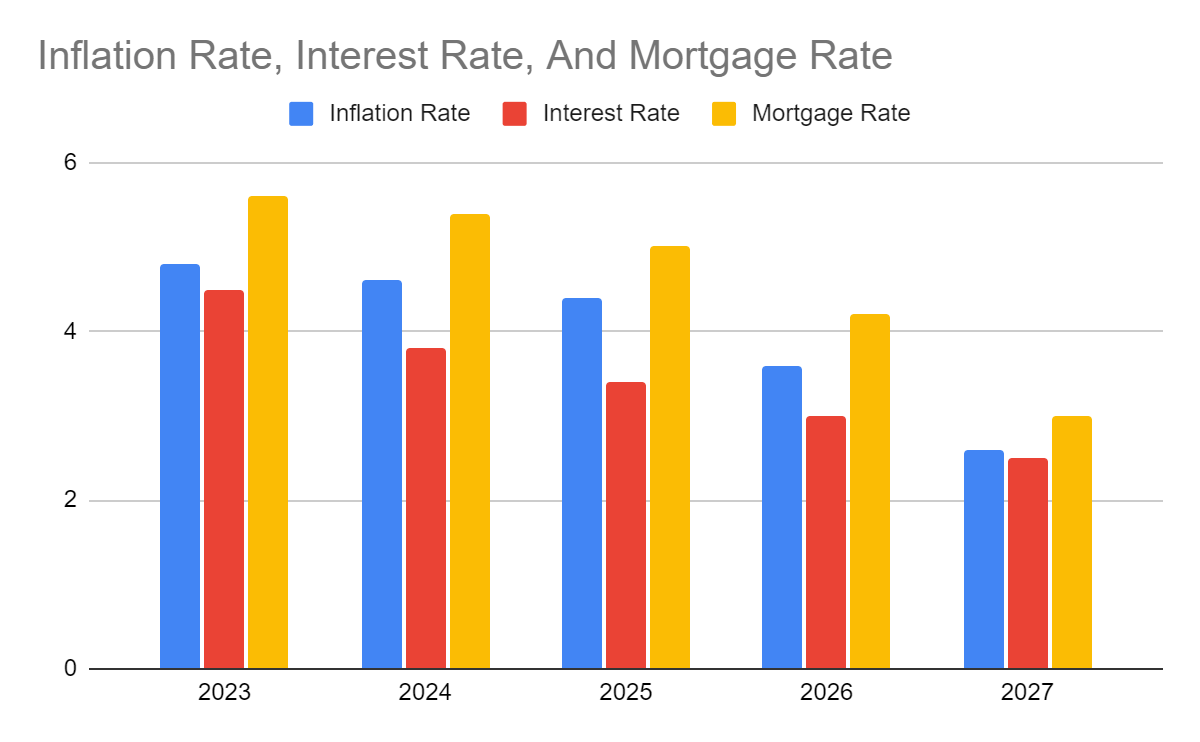

On the contrary, the decrease in inflation remains faster than expected. It was already alarming when it peaked at 9.1% in 2022. But at 4.9% today, it already decreased by 46%. Also, it is the lowest inflation rate in two years. As such, it may partially offset the impact of interest rate hikes. The positive spillovers may become evident in UNB’s non-interest expense. This year, it cannot stop interest rates from rising.

But it can at least slow down interest rate hikes to become more manageable. That way, banks can find ways to manage their yielding assets and liabilities better. In two meetings, we saw interest rate increments remaining flat at 25 bps versus 75 bps in 2022. UNB can also reprice and diversify its loans and investments easily to increase its potential. With that, the company can stay viable.

{kind=link}

Inflation Rate, Interest Rate, And Mortgage Rate (Author Estimation)

With regard to its real estate loans, UNB must keep an eye on the real estate market changes. In 2022, property sales cooled down as prices and mortgage rates peaked. But I still don’t agree with the supposition of a massive crash. Many factors must be considered before coming up with a very pessimistic conclusion. First, the US property shortages remain high, which can be attributed to the slight decrease in property prices.

It started the year with 6.5 million housing unit shortages. But a report on WSJ showed a double-digit increase in shortages in 1Q. The housing market in the US is short of 7.3 million houses. As such, it is logical to say that housing demand continues to outweigh supply, and many people remain interested in purchasing homes. Second, wages and unemployment are more manageable, increasing borrowing and purchasing power.

It may become visible if inflation relaxes more. It is possible since property prices and mortgage increases were driven by demand, not cost-push factors like labor and building materials. Third, property developers, sellers, lenders, and builders remain conservative in fear of another recession. This behavior was already seen over the past decade. And now, the market avoids speculative mania and unethical practices like overlending and overselling. So, price and valuation changes may become more manageable.

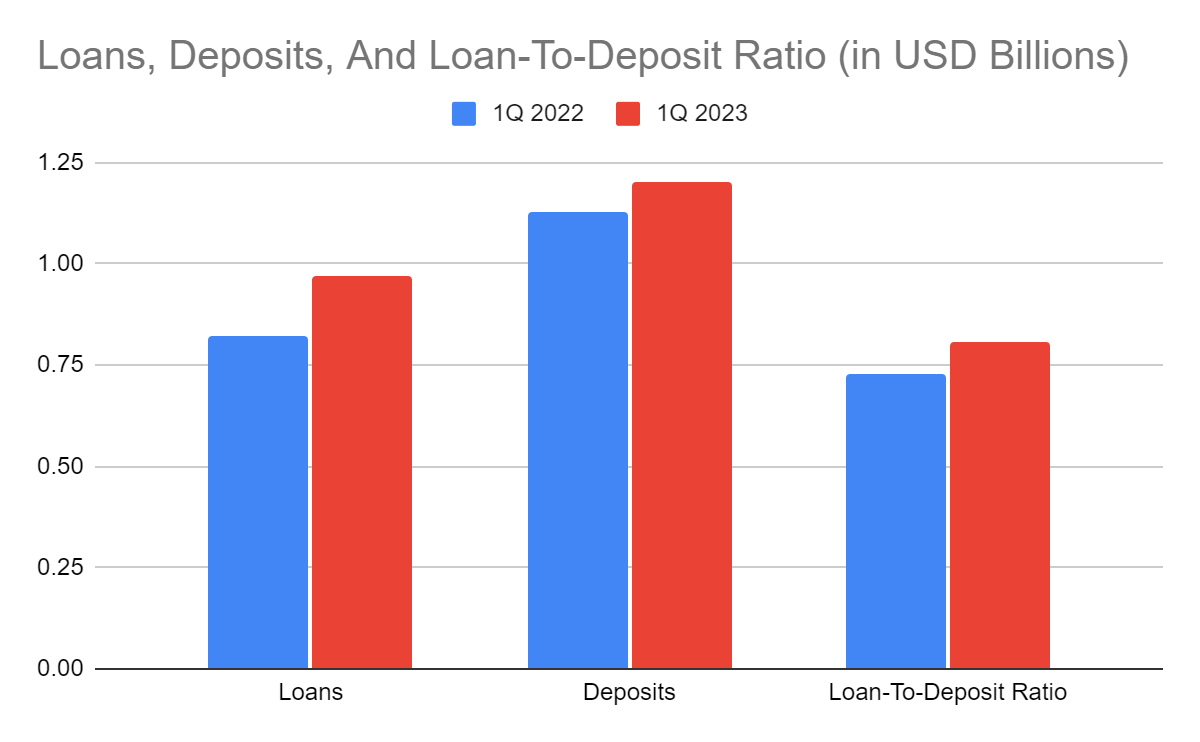

But what makes it secure is its financial positioning. We can see it in its stellar Balance Sheet, particularly loans and deposits. Despite being the primary source of revenues, the company remains conservative to stay liquid. Both loans and deposits increased, but UNB stabilized their increase to ensure profitability. The loan-to-deposit ratio of 81% shows that the company has enough reserves. It can lend more to generate more loan yields. Also, it can cover potential defaults and delinquencies. It is even more impressive today since many banks have an average ratio of 90-95%. It is still effective to offset the massive increase in deposit and borrowing interest. But the current interest income and ratio of the company make it a secure and viable company.

{kind=link}

Loans, Deposits, And Loan-To-Deposit Ratio (MarketWatch)

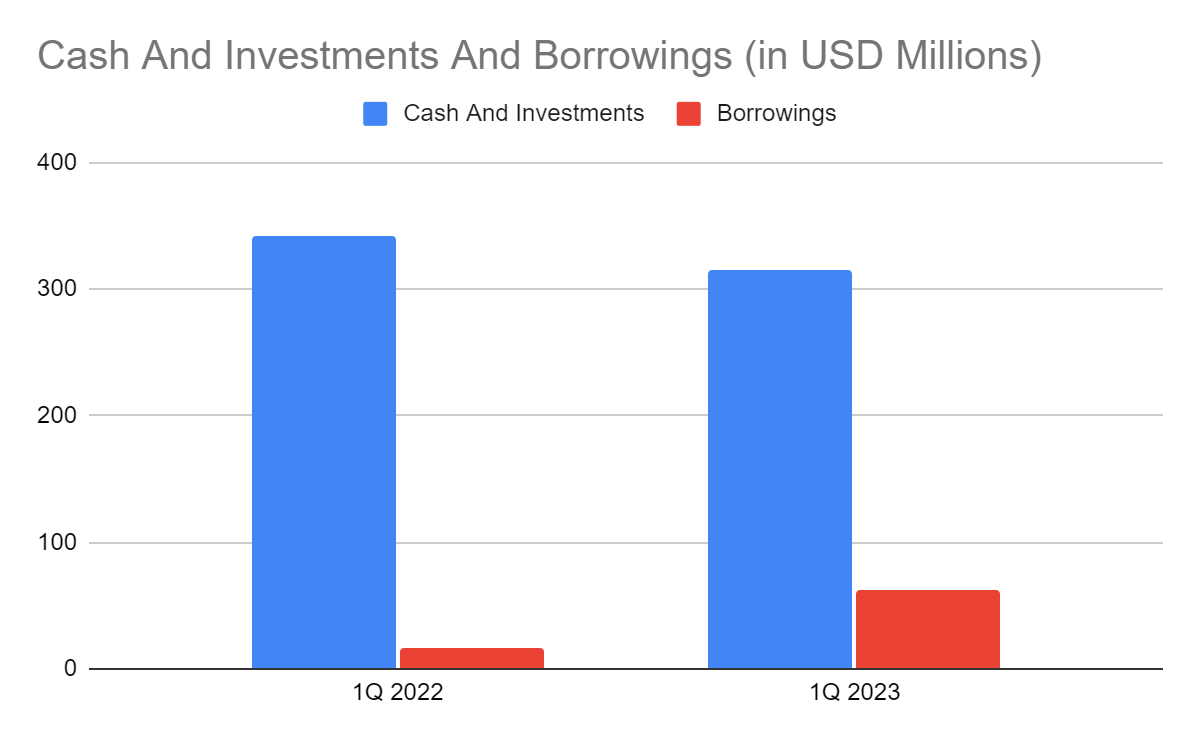

Moreover, its cash reserves remain stable at $38.3 million , which we can associate with well-maintained viability. Despite lower margins, the actual operating income remains higher than in the comparative quarter. The value gave an average cash burn of $2.22 million per month. Using the historical average, we can assume that it may take 17 months to deplete its cash and cash equivalents.

It may be a relatively shorter period, but we must understand that UNB does not heavily rely on cash and financial leverage. It is not a capital-intensive company contrary to freight and logistics and construction companies. There may be risks, but these are still low, given its impressive loan-to-deposit ratio. It has adequate room to cover potential defaults and delinquencies. Also, its investment securities remain relatively stable.

If we combine it with investments, their value will comprise 24% of the total assets. They are also more than five times the amount of borrowings. More importantly, its Net Debt/EBITDA is only 2.5x and verifies the adequacy to cover the operating capacity and borrowings. The company maintains the balance between growth and viability with sustainability.

{kind=link}

Cash And Investments And Borrowings (MarketWatch)

Stock Price Assessment

The stock price of Union Bankshares, Inc. remains in a downtrend. It remains quite divorced from the fundamentals, but it is logical due to the banking crisis. At $20.5, the stock price is 26% lower than last year’s value. And while stock price growth remains sluggish, it offers an opportunity for gains. We confirm it using the PB Ratio, given the current BVPS and PB Ratio of 13.43 and 1.57x. If we use the current BVPS and the average PB Ratio of 1.93x, the target price will be $26.03.

Moreover, it is an ideal dividend stock, given its consistent payment and adequate cash reserves. It has a high yield of 6.96% versus the S&P 600 and NASDAQ average of 1.72% and 1.59%. Dividends are also well-covered, given the Dividend Payout Ratio of 56%. To assess the stock price better, we will use the DCF Model.

FCFF $12,192,000

Cash $21,819,000

Borrowings $59,370,000

Perpetual Growth Rate 4.4%

WACC 9.2%

Common Shares Outstanding 4,509,000

Stock Price $20.50

Derived Value $32.50

The derived value agrees with the supposition of potential undervaluation. There may be a 58% upside in the next 12-18 months. So, investors may take this opportunity to purchase its shares at a discount.

Bottom line

Union Bankshares, Inc. remains a stable and secure company amidst the risks and headwinds it faces. It is a sustainable bank with efficient and prudent asset management. It has stable cash levels to cover its operations, borrowings, and capital return. Also, the stock price stays undervalued with decent upside potential. The recommendation is that Union Bankshares, Inc. stock is a buy.

For further details see:

Union Bankshares: Uniting Growth And Sustainability Makes The Stock Enticing