UNPRF - Uniper: Looking If There's Any Upside To This Nationalized Legacy Player

2023-10-10 14:41:16 ET

Summary

- I believe Fortum's divestment of its stake in Uniper was a major strategy failure in the utility sector in Europe.

- Fortum had initially paid a significant amount of money for Uniper but later decided to sell its entire stake.

- The divestment has been considered as one of the most frustrating experiences in my career as an investor.

- Uniper is a doubtful investment here. It has eventual appeal, but at this stage, I would be at more of a "HOLD" even if you think for the long term. I believe better options exist.

Dear readers/followers,

When I wrote about Fortum (FOJCF) over a year ago, Uniper (UNPRF) (UNPPY) was an important part of that equation - Fortum paid massive amounts of money for it, only to end up divesting the entire stake a few years later in what I believe was one of the most annoying strategy failures in the utility sector in Europe I have experienced in my career as an investor.

Moving forward from this, I believe it is time to look over this investment to see if it can offer us anything of value in terms of upside and fundamentals, not as a component of a different company such as Fortum, but as its own stand-alone investment.

In this article, I'll offer you a basic overview of Uniper, and show you why at the right price, legacy assets may be something you want to look at - as it stands though, the company is a tricky investment in an otherwise appealingly priced market, given its fundamentals.

Uniper - the Fundamentals of the company

So, Uniper has its roots in E.ON (EONGY) (ENAKF). The historical split of E.ON's electricity generation business from its retail selling business was first announced almost 8 years ago, back in 2015. This new split company became active in January 2016 with 14,000 employees and a positive outlook for its earnings and future.

So essentially, Uniper was a carve-off of E.ON's fossil fuel assets into a separate company, with around 30% of the company's employees based in Germany. Until the Russian invasion of Ukraine, Uniper also owned Unipro, a Russian subsidiary company.

It's the last company that operates coal-fired plants in Germany, and also the last company to open new coal-fired plants, the latest one as late as May of 2020. Uniper was also one of the financiers of the Nordstream 2 project - and we know what happened with that project in the wake of the Russian invasion of Ukraine, and those rings on the water spread out all the way to companies like BASF (BASFY) and others which through one way or another had stakes in this, and similar projects.

The big part of the history of course, is that Fortum bought 47% of Uniper back in 2017. This was meant as a bit of a "cash cow", but is what sadly turned out to be nothing but what I'd call a failure. At most, Fortum owned 75%+ of the company. But back in late 2022, Fortum agreed to the finalized terms of the sale of all of its shares in Uniper back to the German state.

The Uniper Extraordinary General Meeting (EGM) on the stabilisation measures is held today on Monday 19 December 2022. The EGM will resolve on the capital increase of Uniper and all newly issued shares will be subscribed by the German State for EUR 1.70 per share. After the equity capital increase, the German State acquires all of Fortum's approximately 293 million shares in Uniper SE for EUR 1.70 per share, a total consideration of approximately EUR 0.5 billion. Uniper will repay the EUR 4 billion shareholder loan, which Fortum has granted to Uniper.

( Source: Fortum )

The short of it is that it went better than many Fortum shareholders believed, given what had happened to Uniper at that point - but to call this deal and the following year's anything but a failure is erroneous in my opinion. Fortum essentially said "Oh, we want this", and then only 4-5 years later due to the macro situation being "forced" to say "It's time to refocus on renewables".

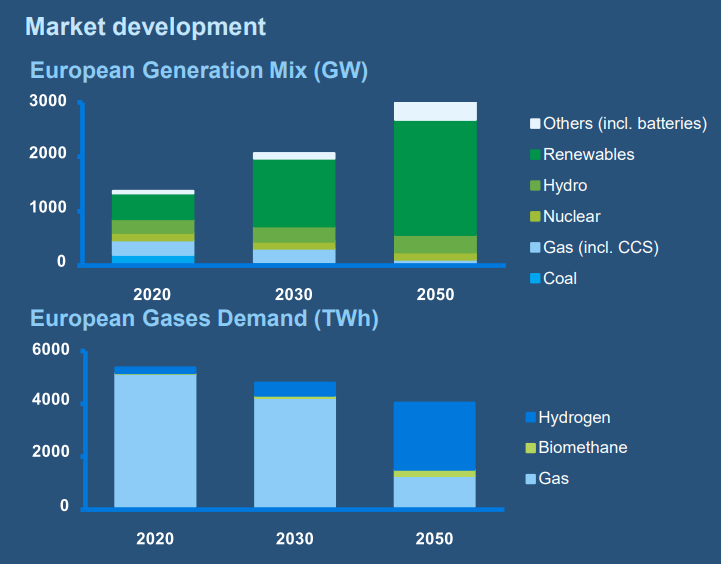

The main argument for investing in Uniper is that you're investing in a transformation of the European energy system. Uniper is holding most of what is "unattractive" if we're to believe trends perhaps 15-25 years in the future, based on the prospective and forecasted generation mix.

{kind=link}

So where, may you ask, is the appeal for a business like this?

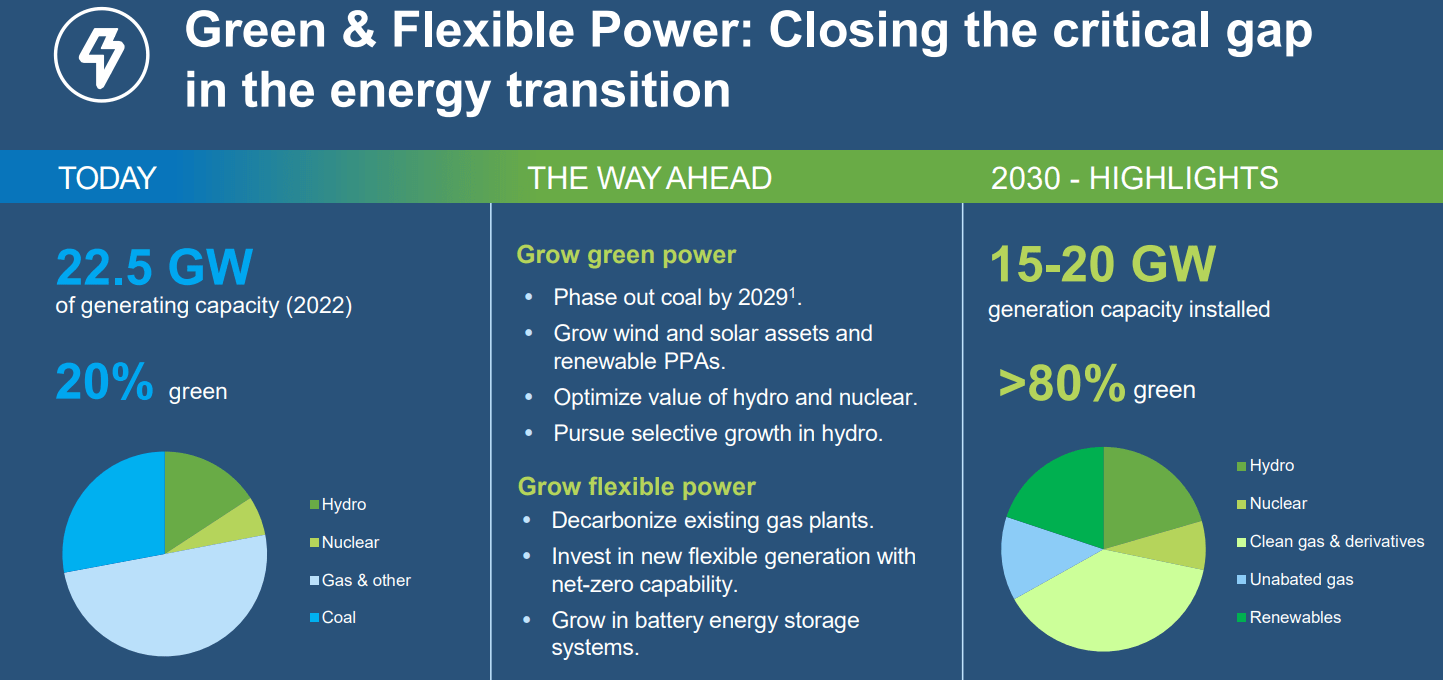

Its 2030 targets work based on a 15-20 GW capacity, of which 80% or above would be "green", with additions of ancillary services and decarbonization solutions, as well as over 200 TWh of gas sales and 1 GW of electrolyzer capacity for the gas sector, with focus on Hydrogen and similar products.

Uniper is very transparent about its goal to phase out coal by 2029E at the latest, with a move towards carbon neutrality by 2040. Its vision is to work as an interlinkage between power and gas in the core markets, the core markets in this case being Germany, the UK, Sweden, and the Netherlands.

Uniper customers today are over 1,000 municipal utilities, industrial customers, and grid operators.

That, as they say, is "today".

{kind=link}

As you can see, the company has one of the potentially most massive shifts in an industry/a company ahead of it that I have ever witnessed in the sector - so for those of you willing and experienced in these sort of turnaround investments, this may not be a terrible idea given the prospective upside this implies. However, it's also, and quite obviously when we're talking about a change of this magnitude, quite significant.

Overall, the company is targeting over €8B worth of investments to turn the company into a "green" powerhouse and to phase out what remains (and what today makes up core Uniper) of its legacy assets. This transformation process is already ongoing, and the new financial strategy and targets have been adopted. The next step is the implementation of EU-accepted remedy measures, adopting a stand-alone IG rating and independence, turning it into "Uniper 2030".

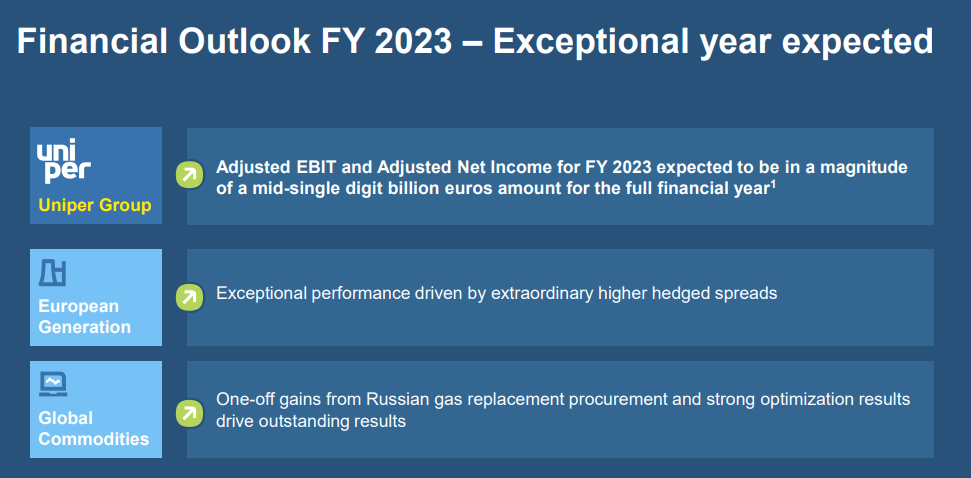

Lofty goals, and not goals that are without more than a measure of challenge. The latest results we have from Uniper that would give any indication of how this is going are the 1H23 results.

Uniper describes this as the recovery being in "full swing". Some of the major positions of uncertainty have been resolved by hedging of open positions of non-delivery related to Russian gas. At the same time, the 1H23 earnings were absolutely exceptional due to gains from gas procurement replacement volumes.

On the fundamental side, the company is now IG-rated, albeit at BBB- with a revision to stable from S&P Global. This is of course a major victory for the debt and financing side of things.

Also on the fundamental side, financing requirements are down significantly due to an early termination of a €5B tranche of a credit facility.

The company managed €4.069B worth of 1H23 EBITDA, €3.7B of operating income (adjusted), and almost €2.5B of adjusted net income.

Just how good is this?

Put it this way, the results for the same KPIs last year were negative €385M, negative €757M, and negative €490M respectively.

It once again proves the adage that when quality, even downtrodden quality, is on sale, you buy for the reversal - or you should at the very least consider it.

Why?

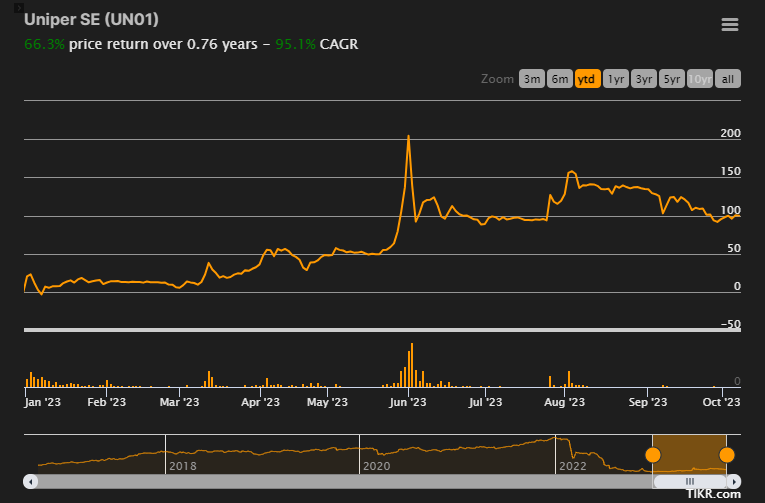

If you had, the reversal for Uniper you could have resulted in significant RoR from the trough. Take a look at the price change and RoR that this company has actually managed for the YTD period.

{kind=link}

Granted, and as you can see, this is nowhere near to what Uniper investors in the long-term have lost - but there was a reason I never invested in Uniper prior to the crash or Russian invasion, I was unwilling to pay even a slight normalized premium to legacy assets. But when they're dirt cheap, that's a different story entirely.

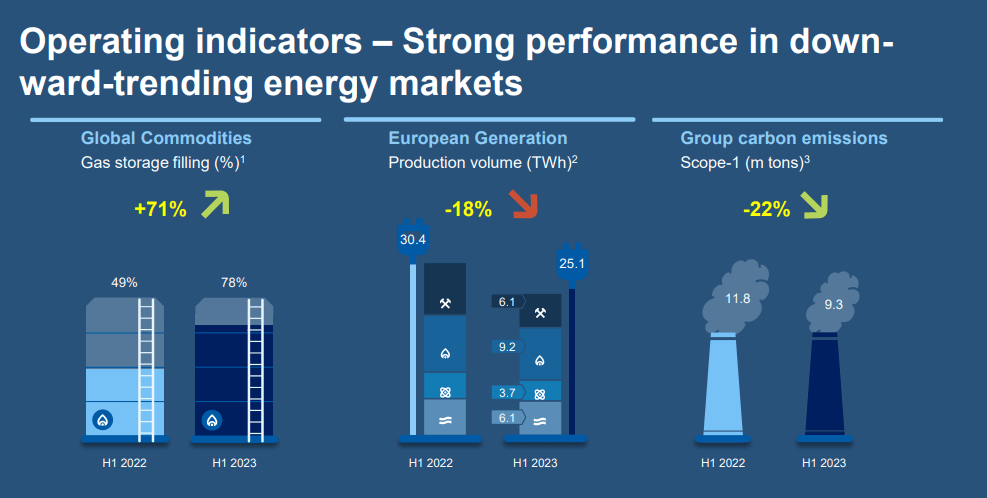

The company's indicators and metrics are solid here, not just on profit, but on volumes and emissions as well.

{kind=link}

I also don't want to give you the implication that this is all Russian gas related. A significant amount of improvements in the earnings side also came from fossil fuel generation, as well as outright nuclear and hydropower.

All of these results have turned Uniper from a net debt company into a net cash company. As of 1H23, the company has almost €1.5B of net cash currently on the books, from a net financial/economic net debt perspective.

For the FY23 period, there is an expectation of an absolutely massive fiscal result.

{kind=link}

At the same time, commodity prices are slowly normalizing to where we can expect 2024E results to be significantly less than those in this fiscal.

But Uniper has prepared well - and over 85% of the company's relevant positions are hedged for 2024E already, 90% for 2023, and 30% for 2025E for the German market. In the Nordics, those percentages are lower - 40% for 2024E - but still a decent amount of hedging given the volatility of the current market.

I want to show you what the valuation implies for Uniper here.

Uniper - Potentially positive valuation

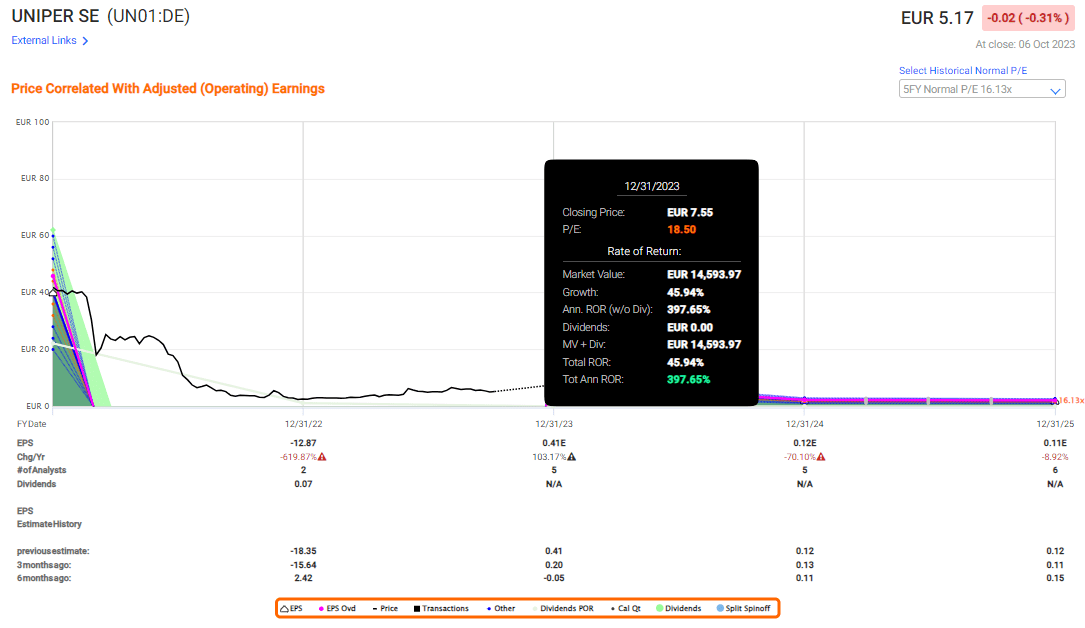

Uniper is very tricky to value, given that it's in the midst of a change/set of changes that heavily impact the valuation and earnings. The company came in at negative earnings for 2022 and is set to significantly improve this going into 2023, to a degree that sees this sort of valuation at an 18.5x P/E, which is not outside the characteristics of this business.

F.A.S.T graphs Uniper Upside (F.A.S.T Graphs)

{kind=link}

This is obviously not a time when you should consider such an estimate to be indicative of a high degree of accuracy in any way. I view this, in fact, as extremely problematic.

Instead, we're seeing S&P Global averages in targeting based on 7 analysts starting at €1.5/share and going up to €3.3 with an average of €2.4/share, accounting for some of the outsized fossil/carbon risks inherent with the company's current assets, both legacy coal and nuclear.

Not a single analyst has a "BUY" recommendation, and 4 are either at "SELL" or "Underperform" here.

My stance is this. If you hold the company here and you're in it for the long term, then you can "HOLD" the company. That's where my stance comes from. But my question to you would be why you have this investment and at that upside, with a zero prospective yield (2023E), when there are far better upsides out there at far better fundamentals.

Uniper is an interesting play in that it's not a risky tech business that's unprofitable. It's a solid legacy utility - an "upstream" utility that has attractive coal and nuclear assets if this can be qualified or said to be attractive. But we must always see these potentials in light of what else is available on the market today. And given current market trends, I do not see that this is an attractive potential in any way, shape, or form - unless you hold that long-term view hoping for a reversal to €15/share and above.

Then it's a "HOLD".

Here is my thesis on Uniper.

Thesis

- Uniper a European class-leading company in legacy fossil fuel generation, has gone through very hard times. With a market cap of over €43B, it's a solid play at the right valuation, but this "play" also requires you to have a very long-term outlook for the business. Because any upside investors can see here, is likely to be longer term in coming.

- If we consider Uniper at a 16-18x P/E, the company's upside is nearly 400% annualized until 2023E, estimating a PT of €7.55. However, this would be an extremely exuberant valuation.

- I consider Uniper to be interesting only at a valuation of below €3/share as the risk-reward stands today. This means that I am currently at a "HOLD".

- However, you should be aware that the upside, if the company's estimates turn out as expected, is very significant.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansions/reversions.

The company fulfills only 2 out of my 5 investment criteria, making it a "HOLD" here.

Thank you for reading.

For further details see:

Uniper: Looking If There's Any Upside To This Nationalized Legacy Player