UBSI - United Bankshares: Growth And Sustainability In Unity But Stock A Bit Pricey

2023-04-05 04:54:58 ET

Summary

- United Bankshares, Inc. maintained its operational stability amidst macroeconomic volatility.

- Its financial positioning remains in good shape.

- Market headwinds may slow down its near-term performance, but improvements are evident.

- Its well-covered dividends are continuous, matched with attractive yields.

- The stock price keeps decreasing but is not cheap.

United Bankshares, Inc. (UBSI) operates in a highly volatile market today. Even so, its solid 2022 performance is proof that it can stabilize its business and withstand headwinds. Thanks to its well-diversified earning asset portfolio. Yet, it must watch out for its borrowings that may raise expenses further and reduce liquidity. But as of this writing, its financial positioning is still in excellent shape. It has more than enough reserves to sustain its capacity size and raise dividends. Meanwhile, UBSI stock price stays in a downtrend.

Company Performance

The market landscape remains tough and fluctuating today. But thankfully, many banks remain flexible to the massive changes. One of these solid companies is United Bankshares, Inc. It was successful at balancing growth and margins. Despite this, it must watch out for the still elevated inflation. It has relaxed but prices remain higher than pre-2022 levels. Interest rate hikes continue, although increments have slowed down recently. UBSI is still exposed to risks associated with macroeconomic changes. But long-run advantages may stimulate its performance. Indeed, we can see how it moved with market changes in three years. The bank continues to show its durability while ensuring stability.

Its operating revenue amounted to $1 billion , a 26% year-over-year increase. It was also 32% higher than 2019 levels, showing continued revenue growth amidst market disruptions. Indeed, interest rate hikes helped stimulate its revenue growth. It was favorable for the company since it raised yields on its portfolio. It was most evident in 4Q 2022 as the value peaked at $308 million, a 58% year-over-year growth. Even more noticeable was the consistent quarterly revenue increase. This trend proved the direct relationship between interest rates and revenues. Aside from that, efficient loan and investment diversification and solid asset quality became primary driving forces.

Interest Income And Interest Expense (MarketWatch)

{kind=link}

Interest Income And Interest Expense (MarketWatch)

{kind=link}

Interest and fee income on loans comprised over 80% of the total revenues and was 19% higher than in 2021. It was most evident in 4Q, given the 49% year-over-year increase. Like in most US banks, interest rate increments were the primary growth driver. The Fed raised them by 75 bps for four consecutive quarters. To that end, UBSI had to reprice its loan offerings to sustain its growth. It proved fruitful as it sustained its loan volumes, matched with impeccable loan quality. In fact, non-performing loans were only 0.29% versus 0.50% in 4Q 2021 and 0.35% in 3Q 2022. This attribute showed that the company maintained its conservative approach to sustained growth. It helped keep the risk of loan defaults and delinquencies at bay. It was also efficient at loan collection despite interest rate hikes. We can also attribute it to prudent loan diversification, with C&I loans comprising 56% of the total loans. These are also more secure due to collaterals, fixed payments, and higher borrowers’ financial capacity. Although they can pose more risks due to their real estate nature, yields can be higher as property value appreciates. I will discuss more of these in the next section.

Meanwhile, interest income on investment securities covers 14% of the total revenue. It may be small, but it still has a substantial impact on the core operations, as shown by its most recent performance. Its value had a 92% year-over-year increase due to higher yields. And similar to loans, prudent diversification played a vital role in it. The actual value of investment securities increased by 12%, Indeed, its investment securities yielded more in a high-interest environment. If we check the components, most of them are backed by government agencies and enterprises. They are more inflation-linked, so they have more stable yields compared to equity and other debt securities. They also maintain a solid hedge against valuation decreases.

But what made its operations solid were its increased market presence and improved efficiency. Its non-interest segment remained stable. Expenses decreased as inflation continued to relax. Although loan repricing and productivity did not offset the impact of deposits and borrowings, viability remained high. Its operating margin reached 42% compared to 31% in 2021. In 2022, quarterly values were decreasing, but its 4Q margin of 38% was better than in 4Q 2021 with 35%. Indeed, it was able to stabilize its operations while sustaining growth and stabilizing expenses. This year, its near-term performance may be similar to 4Q 2022 as macroeconomic indicators stay volatile. Even so, the continued inflation decrease may help stabilize expenses better. There may also be improvements in the second half as interest and mortgage rates become more manageable. The Fed may remain conservative but may start to ease its monetary policy. It can help the company improve portfolio diversification to generate more yields and attract more banking clients and borrowers.

Operating Margin (MarketWatch)

{kind=link}

Operating Margin (MarketWatch)

{kind=link}

Why Union Bankshares, Inc. May Remain A Solid Company

In the past three years, we have seen how the pandemic and macroeconomic volatility caused disruptions across industries. Banks were not exempt and were even more exposed to risks. Yet, they learned to cope with the drastic changes while ensuring stability. Union Bankshares, Inc. demonstrated the same, given its solid performance. It was highlighted in 2022 as it stayed viable while sustaining revenue growth amidst market volatility. This year, near-term headwinds may persist as inflation, interest, and mortgage rates remain elevated. But improvements may take place in the second half due to various reasons.

Inflation remains higher than pre-pandemic levels. The current rate is still higher than the rates before 2022. Despite this, the downtrend was continuous and substantial. At only 6% versus the 9.1% peak, there is a difference of 34%. We already saw its impact on the company operations, given the decreasing non-interest expenses. Meanwhile, interest rate hikes may continue to ensure inflation stability. The Fed may stick to its conservative approach. But we may expect increments to cool down in the second half. In fact, the most recent increment was only 25 bps. So, interest rates may keep increasing but at a more manageable rate. With regard to mortgage rates, the market may start to stabilize as sales cool down. It may be a concern for UBSI as most of its loans are related to real estate. But I'm optimistic about the market despite the anticipation of another bubble burst. First, house prices were driven by demand, not by the price of building materials. Second, property inventories remained low, only about a quarter of that in 2008. In a more recent report, shortages rose by about one million properties in 2022. Third, property builders stayed conservative to avoid the repetition of the Great Recession. Given this, there may be an offsetting effect between lower demand and higher shortages. Prices and mortgage rates may slow down in the following years, but they may be more stable and manageable.

Inflation Rate, Interest Rate, And Mortgage Rate (Author Estimation)

{kind=link}

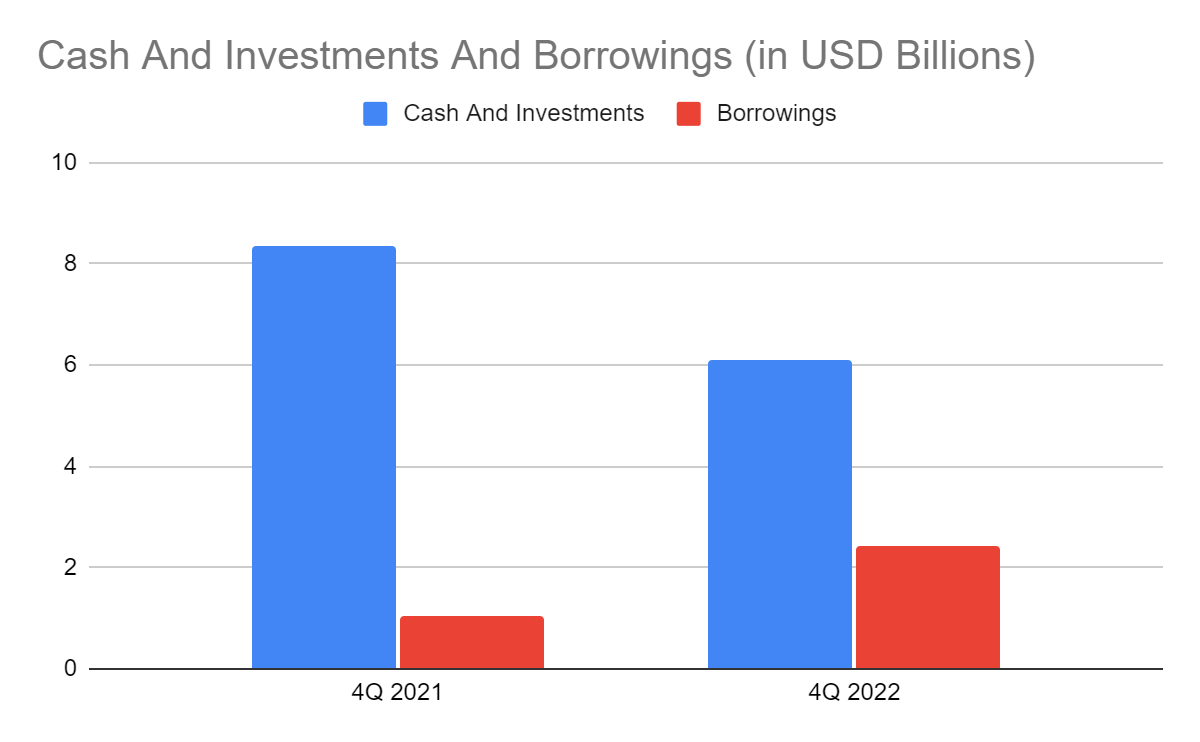

What makes it a force to reckon with is its solid financial positioning. Again, its loan quality and repricing stays excellent. Also, the actual loan volume had a substantial increase. Despite this, the rate of non-performing loans decreased, showing prudent loan portfolio diversification. Deposits increased as well, allowing the company to stay liquid. The current loan-to-deposit ratio is 91%. It is quite higher than the ideal range of 80-90% but reasonable. It is more enticing to lend out funds to generate more yields. Even so, the company stays prudent to avoid or at least minimize defaults and delinquencies. It also has enough reserves to cover late payments and bad loans. It may even raise its deposit rate to attract more clients, lend to more borrowers, and stabilize liquidity. Likewise, cash and investments are adequate to cover borrowings. Cash and cash equivalents decreased, mainly due to bank deposits. But the value of investment securities rose substantially. Their combined value amounted to, % of the total assets. Hence, the company is very liquid and can cover its operating capacity, borrowings, and dividend payments.

Loans, Deposits, And Loan-To-Deposit Ratio (MarketWatch)

{kind=link}

Cash And Investments And Borrowings (United Bankshares, Inc. 4Q Financial Report)

{kind=link}

Stock Price

The stock price of United Bankshares, Inc. has increased and bounced back to pre-pandemic levels in the past two years. But the downtrend has been evident since 4Q 2022. At $34.90, the stock price is 1% higher than last year's value and 19% lower than the 2022 peak. Yet, the downtrend appears logical since the stock price does not reflect the intrinsic value of the company. The PB Value adheres to it, given its current BVPS and PB Ratio of 33.51 and 1.13x. But if we use the current BVPS and the yearly average PB Ratio of 1.04x, the target price will be $34.73. The stock price is now fairly valued with limited upside potential.

Meanwhile, it is an attractive dividend stock due to its consistent payouts and high yields. Its dividend yield of 4.13% is way better than the S&P 400 and NASDAQ average of 1.68% and 1.47%. Indeed, the stock price is reasonable relative to the dividends the company distributes. Dividends also stay well-covered with the Dividend Payout Ratio of 51%. To assess the stock price better, we will use the DCF Model.

- FCFF $295,190,000

- Cash $294,150,000

- Borrowings $2,430,000,000

- Perpetual Growth Rate 4.8%

- WACC 9.2%

- Common Shares Outstanding 134,745,000

- Stock Price $34.90

- Derived Value $33.84

The derived value justifies the reasonability of the stock price downtrend. There may be a 3% downside in the next 12-18 months. So, investors may have to wait before buying shares.

Bottomline

Union Bankshares, Inc. is a solid company with well-balanced revenue growth and margins. It has an excellent financial positioning that allows it to cover its operating capacity, borrowings, and capital returns. Dividends are attractive due to consistent payouts and high dividend yields. Meanwhile, the stock price is fairly valued, but upside potential remains limited. The recommendation, for now, is that Union Bankshares, Inc. is a hold.

For further details see:

United Bankshares: Growth And Sustainability In Unity, But Stock A Bit Pricey