UIHC - United Insurance: A United Business Model With Solid Returns And Sound Fundamentals

2023-05-23 11:20:33 ET

Summary

- United Insurance Holdings Corp. started the year with impressive results.

- Its excellent financial positioning remains one of its sturdy foundations.

- Macroeconomic headwinds are evident, but improvements are starting.

- The stock price keeps increasing but stays reasonable.

United Insurance Holdings Corp. (UIHC) has been through massive challenges in the past three years. The pandemic, hurricanes, and insurance exodus in Florida led to continued disruptions. It intensified in 2022 as Hurricane Ian hit the state while the company was in the process of discontinuing personal lines. With that, revenues, policies-in-force, and margins dropped. Inflationary headwinds did not help the company cope with these problems. Despite this, the company still demonstrated resilience. Thanks to its sound financial positioning, allowing it to sustain its operations. And now, it has started regaining its footing with its impressive rebound. It may have a better grasp of its operations with its smaller size and adequate liquid assets. It can also sustain its capital returns through share repurchases. Unsurprisingly, the stock price has increased substantially in a short period. Yet, it stays reasonable with decent upside potential.

Company Performance

It's been quite a while since I last covered United Insurance Holdings Corp. And since my first coverage, I've seen improvements in its core operations. The Florida market for P&C insurance providers remains challenging. Yet, UIHC proves it can withstand headwinds while streamlining its business. It may be smaller today, but it is better than it was in the past three years.

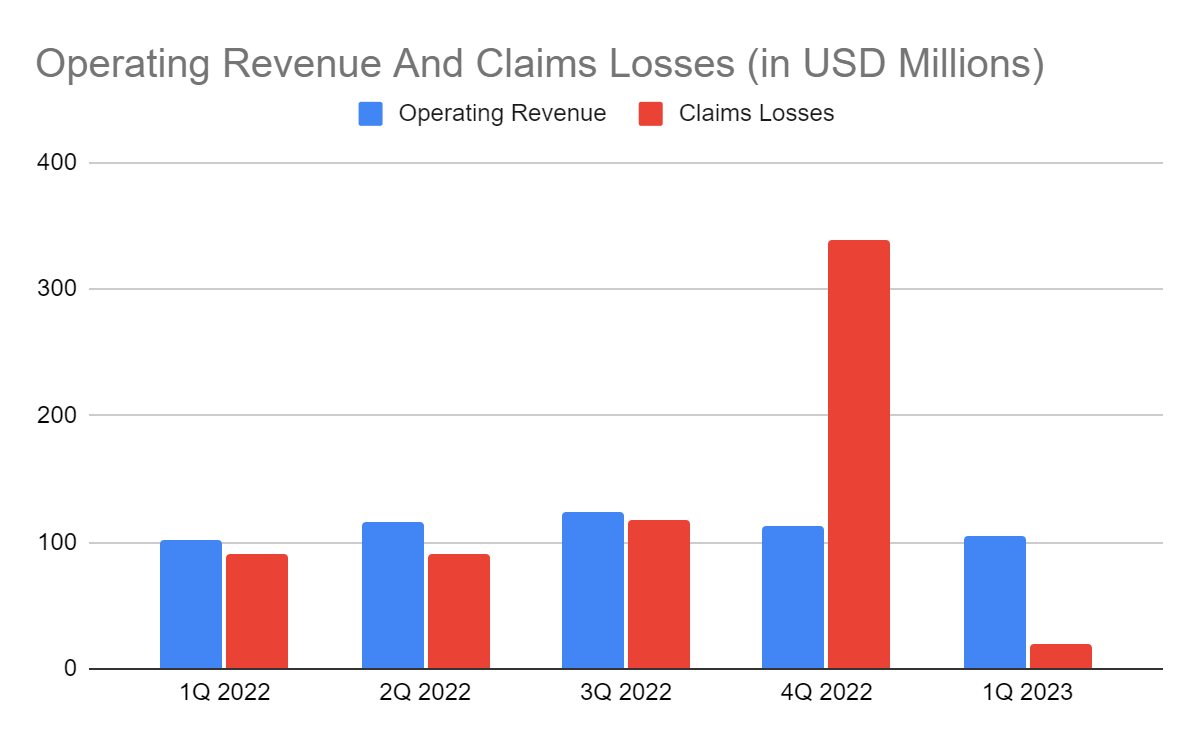

It started the year with a more stable performance despite the contraction of its core operations. The operating revenue reached $104.05 million , a 2% year-over-year increase. Although the growth rate was low, it was still impressive considering macroeconomic volatility and personal lines withdrawal. We can attribute it to the company's efforts and strategies as transitions to specialty commercial lines. Indeed, it was nice to see increased demand from the commercial segment. We can attribute it to the increased number of businesses from 2020 to 2022. Business openings sped up amidst the easing of restrictions and economic improvement in Florida. The primary challenge was inflationary headwinds, which disrupted purchasing power. Also, interest rate hikes discouraged borrowings and investments, making it harder for policyholders to continue paying their insurance policies. Thankfully, inflation has slowed down since 4Q 2022. The company also remained active in its policy repricing to keep the maintain its policies-in-force.

Operating Revenue (MarketWatch)

{kind=link}

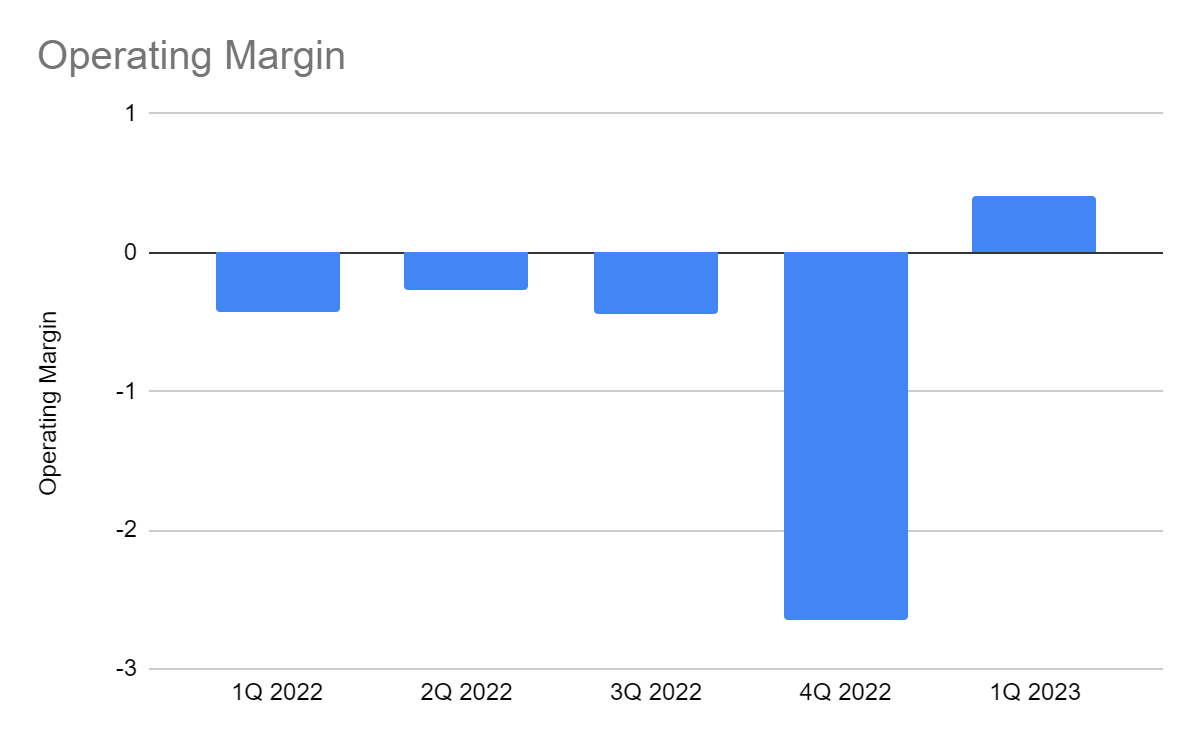

Even better, its claims and losses dropped by 80%. Meanwhile, operating expenses remained relatively flatter, but the decrease was also evident. We can attribute it to the decreasing inflation and personal lines withdrawal. Also, it has already paid the claims from Hurricane Ian in personal and commercial lines. With its smaller business size, it became easier for the company to manage policies and claims. It matched with its strategic pricing and lower inflation to increase operational efficiency. I believe its decision to focus on commercial lines was advantageous to the company. After all, Florida was one of the riskiest states for P&C insurance. There are higher hurricane occurrences along the Atlantic coastline. Hurricane Ian was a massive scourge to the company. It was the costliest hurricane to have ever hit Florida, with property damages exceeding $100 billion . As it regained its footing, it was able to stabilized claims and operating expenses. As such, its operating margin reached 41%, a massive rebound from 1Q-4Q 2022 margins. It also helps that 1Q has less natural calamities like wildfires and hurricanes.

Operating Margin (MarketWatch)

{kind=link}

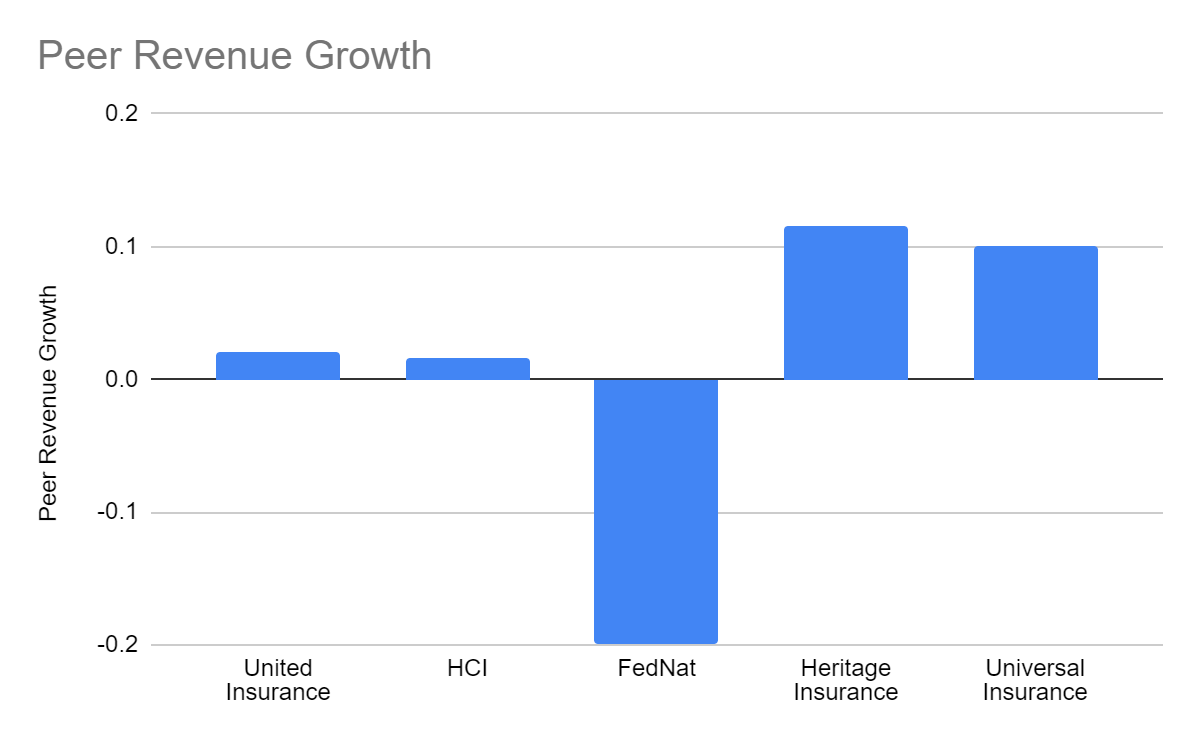

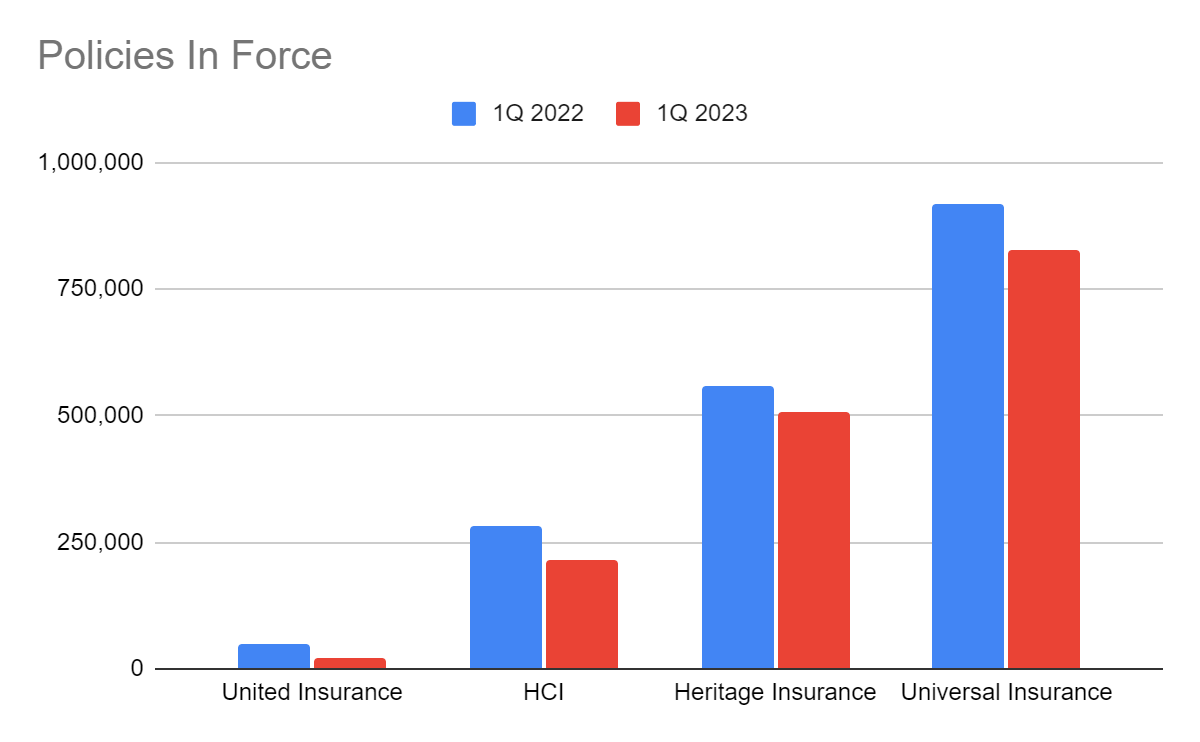

With regard to its peers, UIHC goes head-to-head with them. It may be a dwarf in the midst of giants like Heritage Insurance ( HRTG ) and Universal Insurance ( UVE ). But it is still a durable company in a risky market landscape. Its revenue growth was higher than the market average of 1%. Meanwhile, it had the lowest number of policies-in-force. It was expected after leaving its personal lines segment. Also, it has already foregone UPC and the policies in its previous subsidiary. Today, it has 23,473 active policies versus 48,152 in 1Q 2022. Despite this, it emerged as the most viable company among them. It had the highest margin compared to UVE with 11%, HCI Group ( HCI ) with 20%, FedNat ( OTC:FNHCQ ) with -101%, and HRTG with 11%.

Peer Revenue Growth (MarketWatch) Policies In Force (Report 1Q)

{kind=link}

{kind=link}

This year, the company faces similar challenges. It must prepare for the hurricane season in 3Q 2023. Interest rate hikes are also evident. But given its current business model, the company may handle revenues, claims, and expenses better. The commercial segment has more stable policy and claim changes. We will discuss more of its potential risks and opportunities in the next section.

How United Insurance Holdings Corp. May Stay Afloat This Year

In the face of market risks, investors and analysts tend to be pessimistic about United Insurance Holdings Corp. I understand where they're coming from. I already explained the potential risks associated with investing in P&C companies in Florida. Hurricanes remain the top concern. Additionally, roofing scams remain rampant despite the efforts by policymakers. To combat this, Senate Bill 76 went into effect in 2021. This move prohibited contractors and policyholders from executing contracts for roofing repairs and replacements. Setting a minimum roof age for covering damages was one of the considerations. To further stabilize the property insurance market, Senate Bill 2-A was passed into law. It was a crucial move, given the adverse impact of Hurricane Ida and Hurricane Ian.

Interest rate hikes are still one of the problems in the P&C insurance market. It was harder for those based in Florida as insurers require more funds to cover hurricane damages. Borrowings are more expensive today due to higher interest expenses. With that, UIHC may have to be more careful of the increased frequency of natural calamities. The consolation is that interest rate hikes have become flatter in recent quarters.

Fed Funds Rates (Trading Economics)

On a lighter note, its withdrawal from personal lines may become advantageous. It can avoid claims from homeowners if another hurricane comes. In reality, this segment is more vulnerable to natural calamities due to the size of the business. Also, the materials used to build homes are often less expensive and weaker than those of the businesses. The company had to weigh the costs and benefits of the personal lines. And given its 1Q performance, its decision appeared to be wise.

In addition, inflation has started to relax in the latter part of 2022. The downtrend sped up in 1Q 2023. And now, it is only 4.9% , 46% lower than the 9.1% peak in 2022. While prices stay elevated, the more stable inflation can help increase confidence among consumers and investors. It may also continue as The Fed sticks with its conservative approach. It is one of the reasons interest rate hikes have cooled down from 75 bps to 25 bps. We can see the lower increase in the two meetings. If this trend continues, the business sector may become stable. It can increase business openings, which can drive the demand for P&C insurance. It can also help the company manage its claims and expenses better. More importantly, it can increase its pricing flexibility to set more strategic policy rates. It can attract new customers or offset the potential decrease in policies. It is more vital today, given the increased demand for commercial insurance in 1Q 2023.

United States Inflation Rate (Trading Economics)

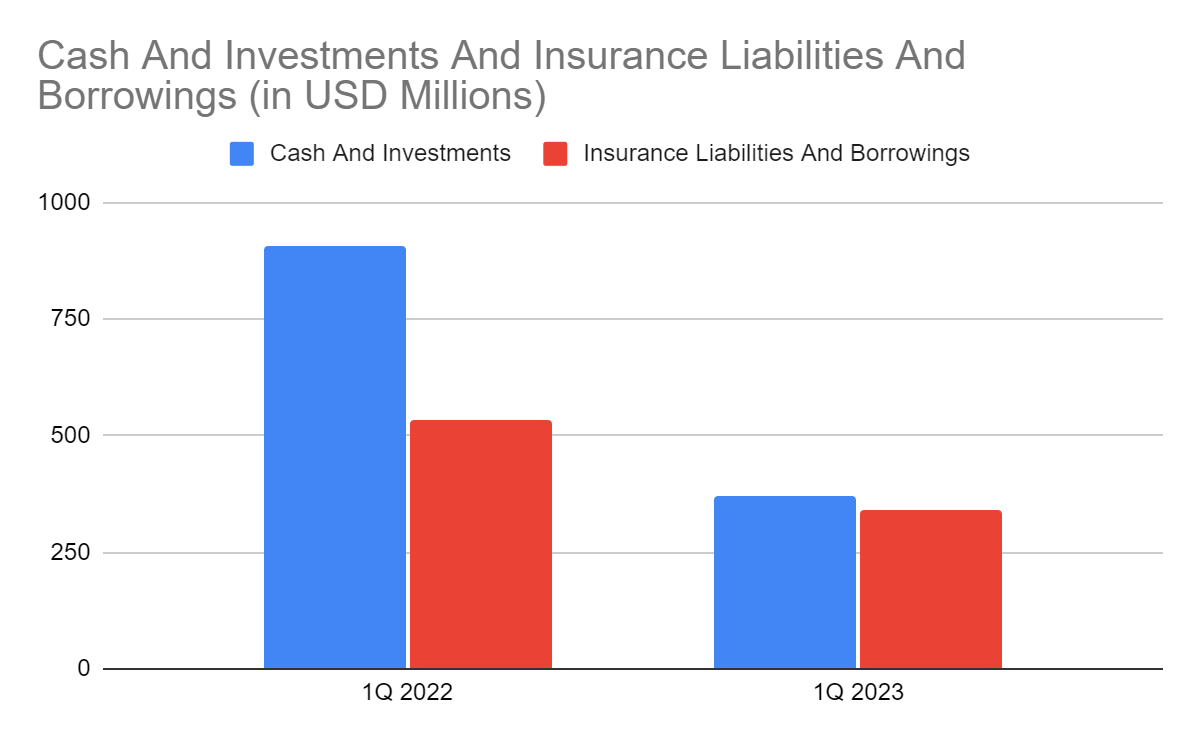

But what makes United Insurance a secure company is its sound financial positioning. It still has adequate cash levels even after the massive claims and withdrawal from the personal lines segment. Even better, the amount of $142 million can sustain its current operations. Meanwhile, borrowings are only a little higher at $150, and the whole amount will not mature this year. It shows decent liquidity levels. If we combine cash with investments, their amount will be $373 million, or 26% of the total assets. They are also higher than the combined value of insurance liabilities and borrowings. With that, the rebound of the company remains reasonable and realistic. The company maintains the balance between viability and sustainability.

Cash And Investments And Insurance Liabilities And Borrowings (MarketWatch)

{kind=link}

Stock Price Assessment

The stock price of United Insurance Holdings, Inc. has rebounded from its 2022 lows. There has been a continued increase since my first coverage. At $6.32, it is already 270% higher than last year's value. It is also 170% higher than the stock price in my previous coverage and exceeded my target price. Indeed, it was a great decision to buy its shares before. Despite this, the stock price remains reasonable. The EV/EBITDA Model confirms it, given the target price of ($305 M EV - $7.69 M Net Debt) / 43,288,000 shares = $6.89. To assess the stock price better, we will use the DCF Model.

FCFF $21,240,000

Cash $142,250,000

Borrowings $150,000,000

Perpetual Growth Rate 4.4%

WACC 9.2%

Common Shares Outstanding 43,288,000

Stock Price $6.32

Derived Value $9.99

The derived value agrees with the supposition of a potential undervaluation. There may be a 58% upside in the next 12-18 months. It is possible since 2Q is not a hurricane season. Even better, it has a more streamlined business model, allowing it to manage revenues better. Income may also increase as inflation relaxes and claims decrease. With that, the potential increase is consistent with the performance and fundamentals of the company. The stock price also reflects the intrinsic value. So, interested investors may consider it a good bargain.

Bottomline

United Insurance Holdings Corp. is a resilient company in a rugged Florida market. It continues to regain its footing and stabilize its core operations. With its concentration on commercial lines, its operating capacity has already contracted. But this move may help simplify its revenue streams. Expenses and claims may become more manageable even if another hurricane comes. More importantly, it stays sustainable with its solid financial positioning. Its cash and investments are high enough to cover insurance liabilities and borrowings even in a single payment. With that, the stock price remains cheap with decent upside potential. The recommendation is that United Insurance Holdings Corp. is a buy.

For further details see:

United Insurance: A United Business Model With Solid Returns And Sound Fundamentals