SB - United Maritime: Upgrading To Buy On Vastly Improved Charter Rates And Generous Dividend

2023-10-09 02:06:25 ET

Summary

- Over the past twelve months, United Maritime has sold all of the tanker vessels acquired in July 2022 at an aggregate gain of $48 million.

- The company has shifted its focus back to the larger dry bulk vessel classes. Currently, the fleet consists of eight dry bulk carriers with an average age of 14.5 years.

- The recent rally in dry bulk charter rates should benefit United Maritime's Q4 results quite meaningfully thus providing support for the company's generous quarterly cash dividend of $0.075 per share.

- While shares are currently changing hands at an approximately 60% discount to net asset value, investors should be wary of the ongoing warrant overhang.

- With the vastly improved chartering environment supporting the continuation of the company's substantial quarterly cash dividend, I am upgrading USEA's shares from "Hold" to "Buy".

Note:

I have previously covered United Maritime Corporation ( USEA ), so investors should view this as an update to my earlier articles on the company.

It has been almost a year since my last update on United Maritime Corporation or "United Maritime". Over the past twelve months, the company has sold all of the tanker vessels acquired in July 2022 at an aggregate gain of $48 million as outlined by management in the Q2/2023 earnings release:

In the second quarter of 2023, we agreed to sell our remaining tanker vessel, the M/T Epanastasea, completing our first highly profitable investment cycle. (...)

This sale marks the end of a series of successful tanker sale and purchase transactions, resulting in a solid profit of approximately $48 million, less than a year from the delivery of the first vessel to United.

The net sales proceeds have been reinvested to regrow our fleet with focus on the larger dry bulk vessels.

In addition, we have distributed significant returns to our shareholders through share repurchases and cash dividends. For the second quarter, our board has approved another dividend of $0.075 per share. Since the commencement of our operations, we have declared cash dividends of $1.225 per share (...).

Moreover, in the last 12 months following the only equity offering, since initial listing, we have bought back $6,194,328 worth of our shares at an average price of $1.84 per share.

With the sale of the remaining LR2 tanker, the company has shifted its focus back to the larger dry bulk vessel classes. Currently, the fleet consists of eight dry bulk carriers with an average age of approximately 14.5 years:

{kind=link}

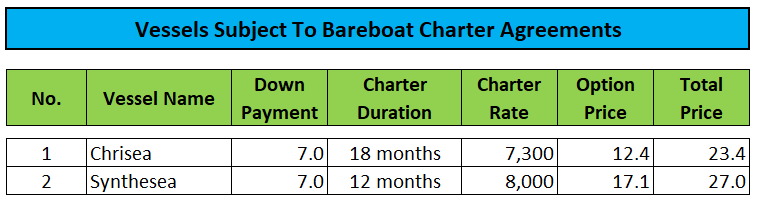

Please note that the Panamax carriers Chrisea and Synthesea are bareboat chartered-in with United Maritime holding purchase options at the end of the respective charter periods:

{kind=link}

While the company continues to pay a respectable quarterly cash dividend of $0.075 per common share, the sale of the highly profitable tanker fleet has resulted in slightly negative cash flow from operations in H1/2023.

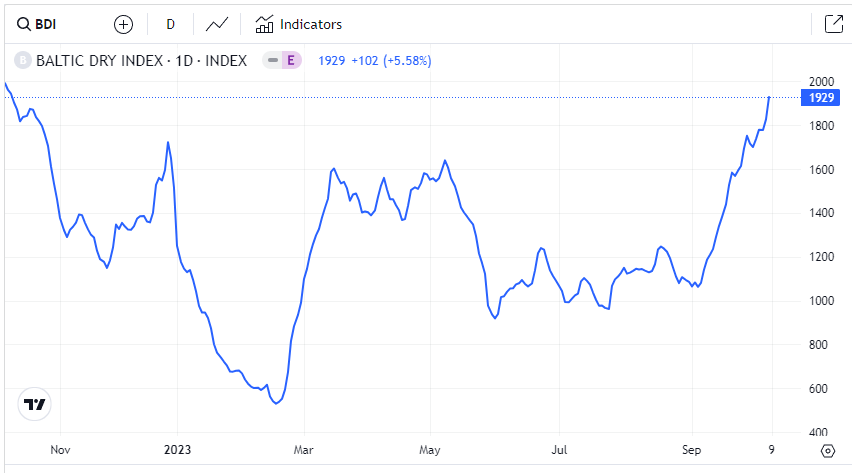

However, the recent rally in the Baltic Dry Bulk Index ("BDI") should benefit United Maritime's earnings and cash flow generation quite meaningfully even when considering the fact that the Capesize carrier Gloriuship has been fixed at a below market daily time charter equivalent ("TCE") rate of $17,600 until year-end.

{kind=link}

With Capesize charter rates at 52-week highs and two additional Capesize carriers employed on index-linked time charters, I would expect the company's fourth quarter results to be positively impacted.

On the flip side, rate improvements for the company's smaller Panamax and Kamsarmax carriers have been more muted but still sufficient for these vessels to generate meaningful positive cash flow from operations.

Consequently, United Maritime's operating cash flow for the remainder of the year should easily cover the company's generous quarterly dividend.

Despite the positive developments, the stock price has barely moved in recent weeks likely as a result of the warrant overhang from the company's $26 million public offering last year.

Remember that following the payment of a $1.00 special cash dividend on January 10, the exercise price of the warrants was adjusted from $3.25 to $2.25.

As of June 30, approximately 7.0 million warrants remained outstanding. Should the company's share price continue to support warrant exercises, outstanding shares could increase by almost 80% to 15.9 million with a resulting reduction in net asset value ("NAV") per share:

Regulatory Filings

But even on a fully diluted basis, the discount to NAV still calculates to approximately 45%, very similar to former parent Seanergy Maritime Holdings ( SHIP ) and close peer Safe Bulkers ( SB ).

Bottom Line

Following the recent sale of its last remaining LR2 tanker, United Maritime has become a pure dry bulk shipping company again with a focus on the larger, ungeared vessel classes.

The recent rally in dry bulk charter rates has improved United Maritime's near-term outlook quite meaningfully. As a result, I would consider the company's generous quarterly cash dividend of $0.075 to remain safe for the time being.

While shares are currently changing hands at an approximately 60% discount to NAV, investors should be wary of the ongoing warrant overhang.

With the vastly improved chartering environment supporting the continuation of the company's substantial quarterly cash dividend, I am upgrading United Maritime's shares from " Hold " to " Buy ".

Risk Factors

Please note that particularly the larger vessel classes remain highly dependent on Chinese iron ore imports so any meaningful reduction in iron ore shipments would negatively impact charter rates.

In addition, dry bulk shipping is subject to seasonality with Q1 usually being the weakest quarter of the year.

Lastly, a highly cyclical industry like shipping requires investors to keep a close eye on charter rate developments in order to avoid potentially outsized losses.

For further details see:

United Maritime: Upgrading To Buy On Vastly Improved Charter Rates And Generous Dividend