UMC - United Microelectronics Corporation: A Solid Long-Term Choice

2023-04-21 18:49:15 ET

Summary

- The company is about to report earnings and is currently trading at 7x earnings, which seems very cheap to me.

- The semiconductor sector is not getting much love and geopolitical tensions between China and Taiwan makes investors hesitant.

- The balance sheet, strong FCF generation, and a conservative DCF analysis suggest the company will recover and is a good long-term investment.

Investment Thesis

With Q1 earnings just around the corner, I wanted to take a look at United Microelectronics Corporation ( UMC ). Due to the current slowdown in demand for semiconductors and negative sentiment towards businesses closely associated with China, I believe these factors present a great entry point into a company that can generate very strong free cash flow, coupled with a solid balance sheet, the company is a no-brainer in the long run if we don’t see any escalation of invasion of Taiwan by the Chinese government.

Outlook

The company is reporting earnings at the end of April, which may bring a lot of volatility in the short run. I'm expecting to see a lot of negative numbers in terms of growth and demand. This is expected as a slowdown and a correction is playing out in the semiconductor industry at the moment. The demand has been dropping quite considerably for the last few months and may continue, as witnessed by a decline in sales in January , and substantial drops in February and March , for a little while longer, which will present some volatility in companies such as UMC.

This in my opinion is going to be short-lived and in the long-term investors should welcome this correction as it will present a very good entry point for an industry that will no doubt bounce back strong once supply chain issues, recessionary period, demand, and what I think is the largest risk that makes investors stay away from companies like UMC is an ever-present threat of invasion by China, so let’s look into that a little further.

A lot of investors may be weary of investing in a company that is very closely related to China. There has been a lot of fear coming recently that China may invade Taiwan very soon, with Taiwan making live-fire drills on a monthly basis. The US isn’t helping ease investors’ worries also with their rhetoric that the semiconductor industry in Taiwan is “very vulnerable to invasion”.

Is there an actual possibility that China will invade? Most recent past events, like the invasion of Ukraine, which I thought no way can happen, happened, so nothing's off the table. China's policy of "Unifying Taiwan by Force" doesn't sound like a non-threat. Is China going to follow in Putin's footsteps and try to annex Taiwan? We have to take that into our risk assessment for sure and hope that the government will be smart enough not to engage in such atrocities that we see in Ukraine. There will be countries, like the US that will protect Taiwan if this does come true.

The above risks need to be taken into account when considering investing in companies like UMC, but I believe the fears are slightly overblown which presents a great opportunity to invest in a company and an industry that is not seeing a lot of love currently.

Financials

One of the reasons I wanted to look into the company is that the balance sheet is in a very good position and the company is currently trading at around 7x earnings, which is very cheap.

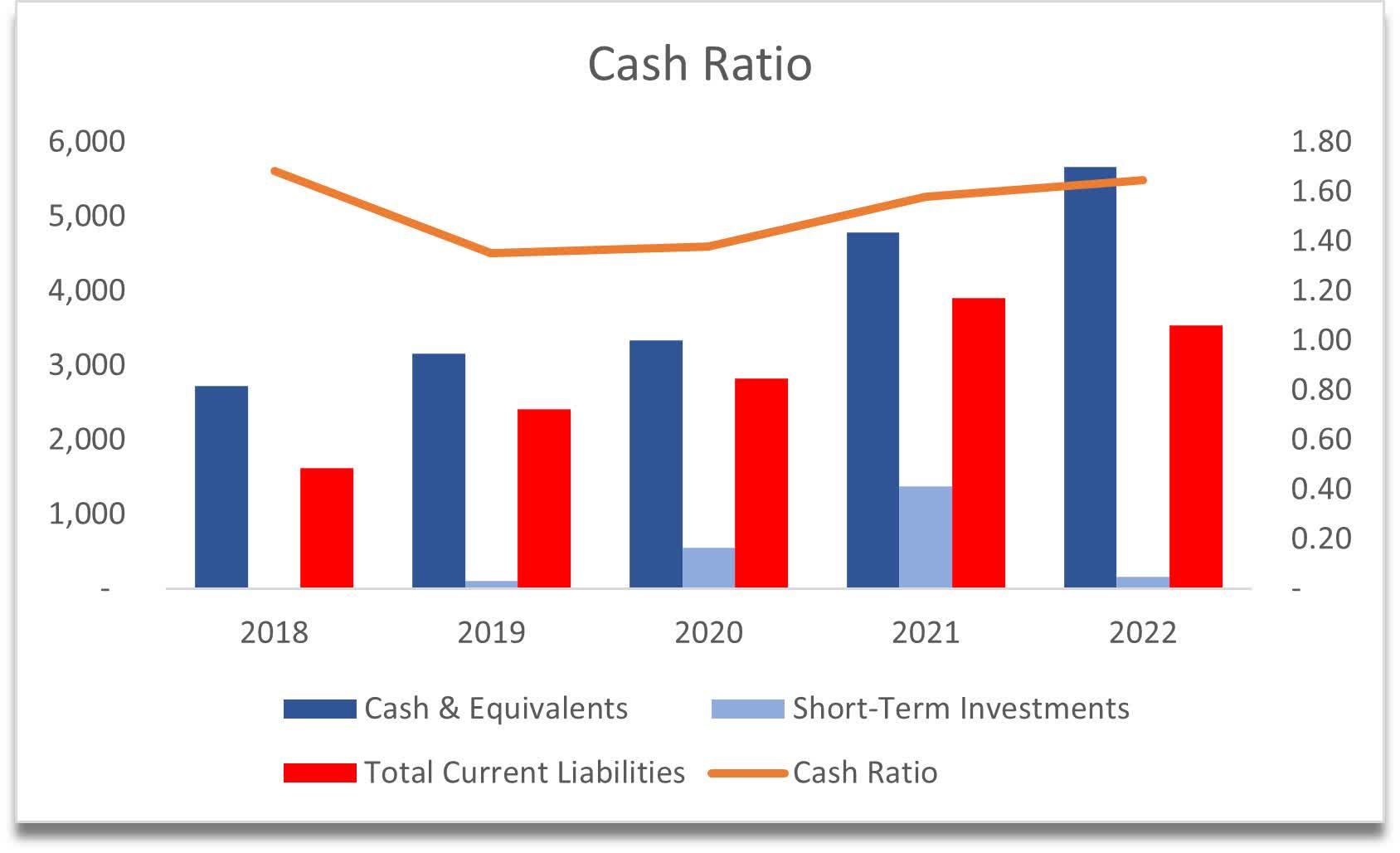

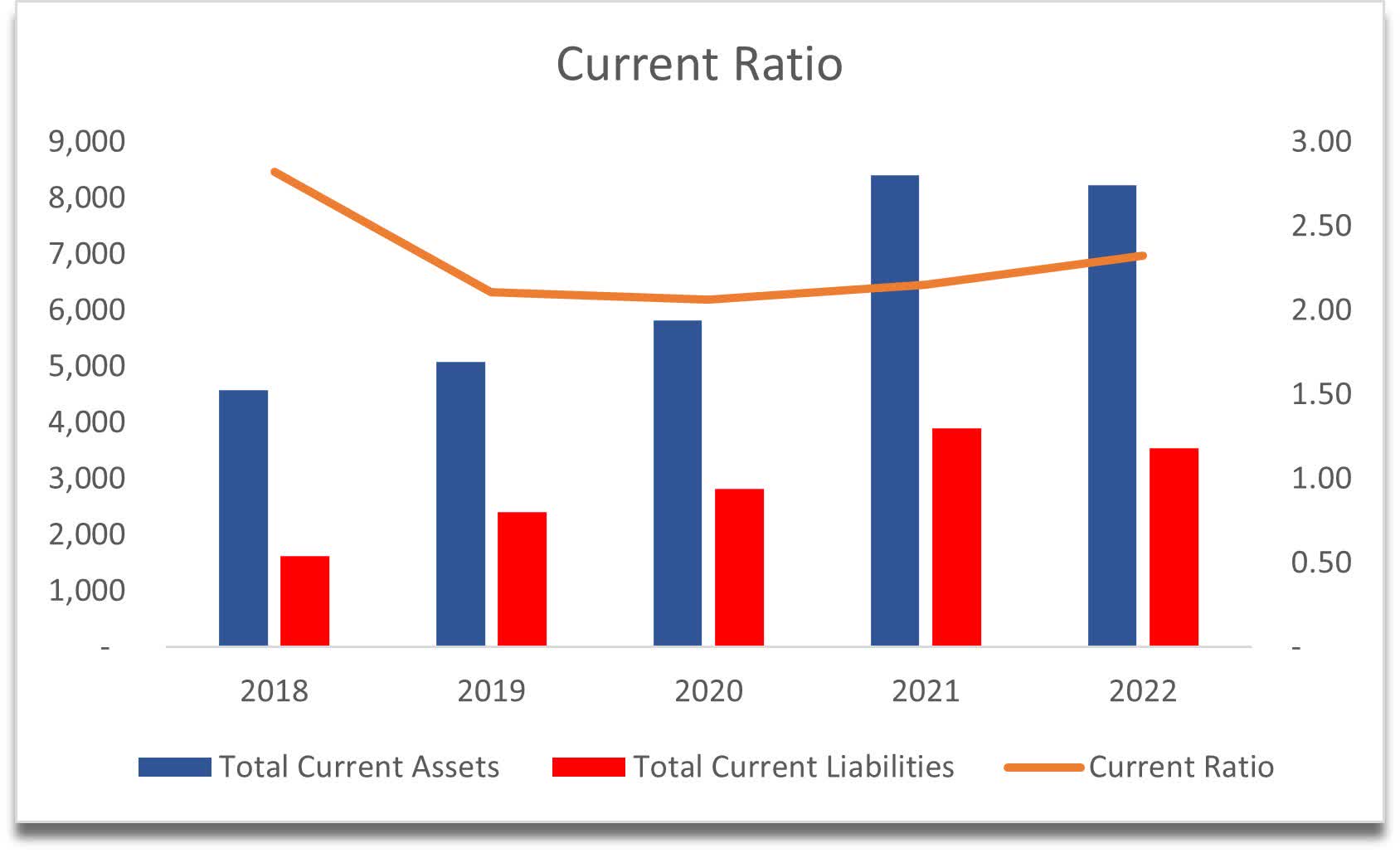

The company has amassed a very healthy cash pile that can be deployed for further growth, whether that is organic or inorganic, through acquisitions. The cash pile at the end of '22 stood at around $5.6B. The company is one of the rare gems that has a very solid cash ratio, which looks at the company's liquidity in a more conservative way which only takes into account cash on hand and short-term investments to see if the company can pay off its short-term obligations. The company is very liquid with a cash ratio of 1.6 at the end of ’22 so this also means that the current ratio is well above 1 also.

Cash Ratio (Own Calculations) Current Ratio (Own Calculations)

{kind=link}

{kind=link}

The company also has some debt, but there are quite a few reasons why it is not an issue at all. The amount of cash exceeds the outstanding debt over 4 times, and EBIT and operating cash flow are well above the interest expense on outstanding debt.

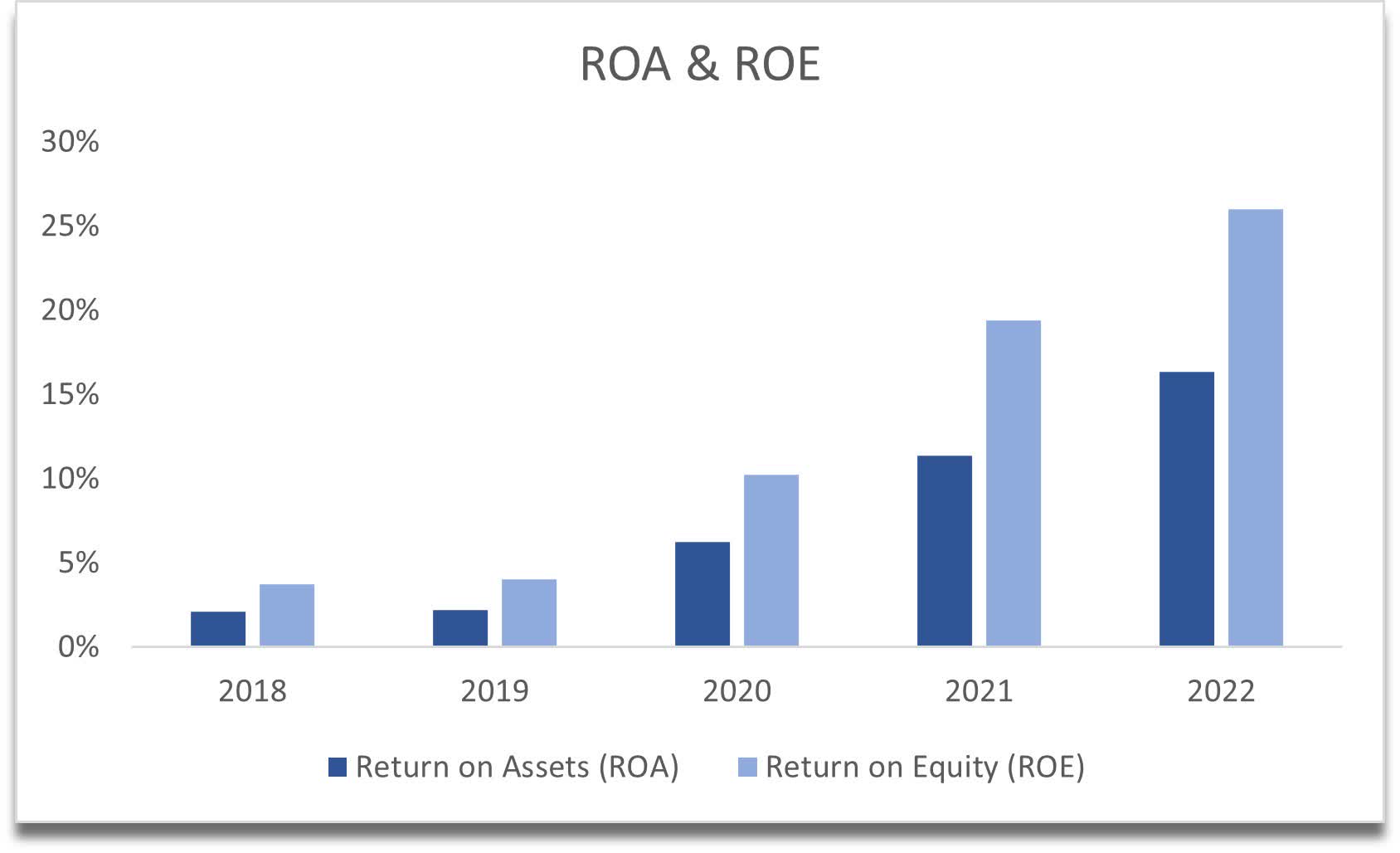

In terms of efficiency and profitability, the company has been performing very well in these metrics too. All of these have seen a very strong uptrend which shows that the management is capable of distributing the capital correctly, which should reward shareholders in the long run for sure.

ROA and ROE (Own Calculations)

{kind=link}

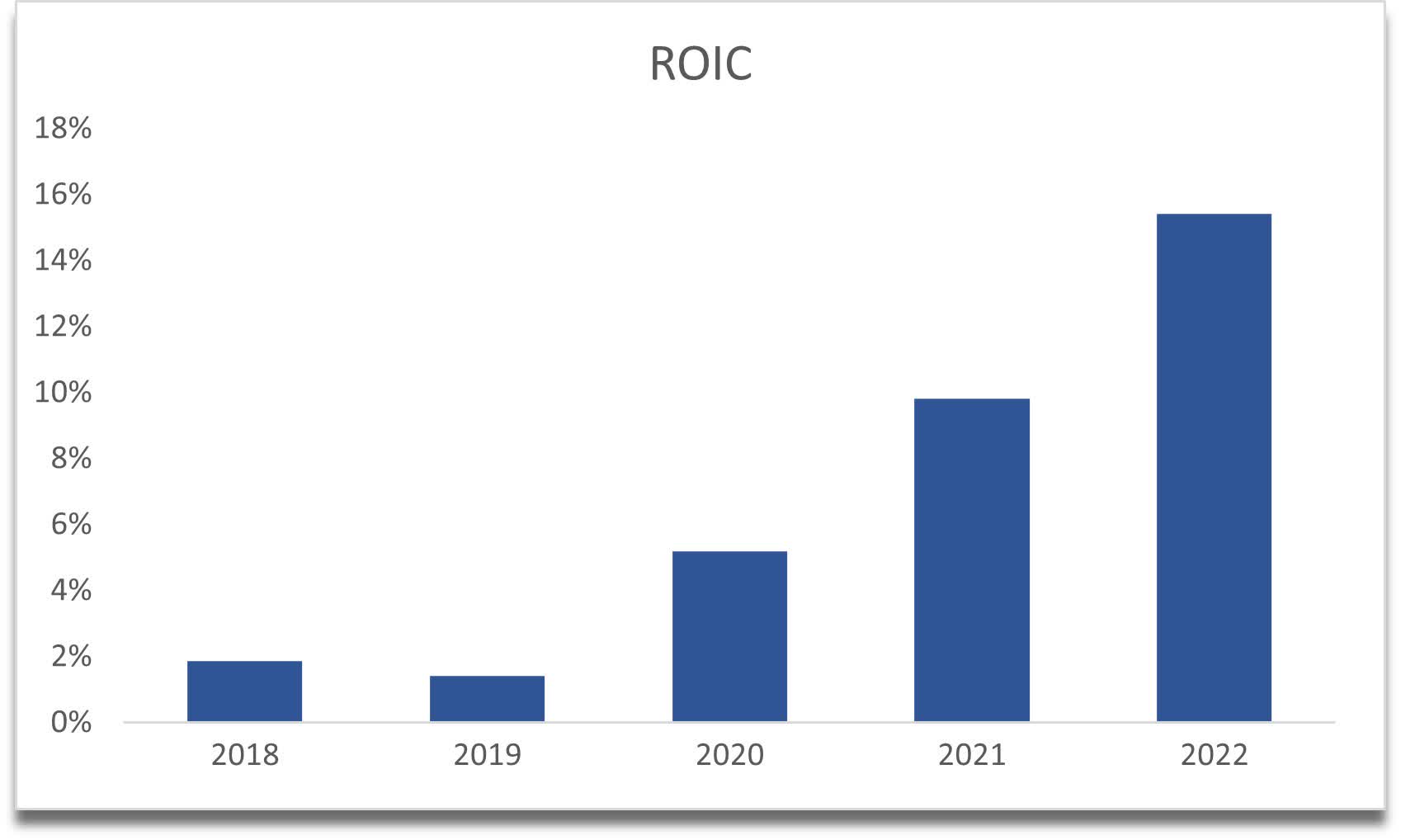

ROIC is also on a similar trajectory and is very attractive. The ROIC of 15% tells me that the management can invest the capital that will generate 15% on the invested capital and is still growing. This also tells me that the company has a good moat and a competitive advantage that cannot be overlooked. I wouldn't mind paying a premium for a company if it was able to produce such a return.

{kind=link}

Overall, the company’s financials are outstanding. I do not see any issues that it might face in the short run if we do see some economic headwinds in the next 6-12 months. It takes me a few companies to look through before I find such an outstanding balance sheet, and the company trading at 7x earnings boggles me.

Valuation

For the DCF model, I decided to go with a simple approach. For the base case, I assume a 10% decline in revenues in '23 because of the slowdown and the correction in the semiconductor space and a 5% decline in '24 just to keep it more conservative and to assume that the supply chain issues persist a little longer. After those years, the company will see a 15% increase in revenues which will linearly decline to 5% growth by '32, giving me a 6.5% CAGR over the next decade.

For the conservative case, I went with a 4.5% CAGR, and for the optimistic case with an 8.5% CAGR.

I believe these are quite conservative estimates for the company and no doubt once the love comes back to the semiconductor industry and worries of an invasion subside, the company will grow at a much higher pace. I just like to keep it on the conservative side of things as usual.

In terms of gross margins, for the base case, it will vary from 43% to 45%, in the conservative case 42% to 44%, and in the optimistic case 44% to 46%, which is still within where the company usually ends up in and slightly on the conservative side still on the base case.

I will also add a 25% margin of safety to the intrinsic value calculation. This is the minimum I would like to give to a company if the balance sheet is very solid. If it is less solid and has some red flags, I would increase it to 35%+ depending on how bad the books are.

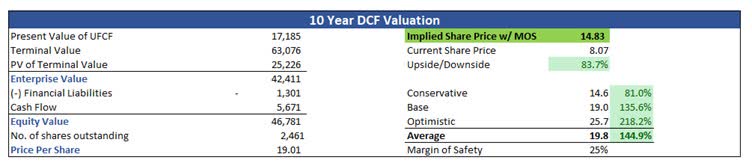

With that said, the company is very undervalued right now and potentially has an upside of 83% from the current valuation of $8.07. The intrinsic value is $14.83 a share.

10-year DCF Valuation (Own Calculations)

{kind=link}

Closing Comments and Investor Takeaway

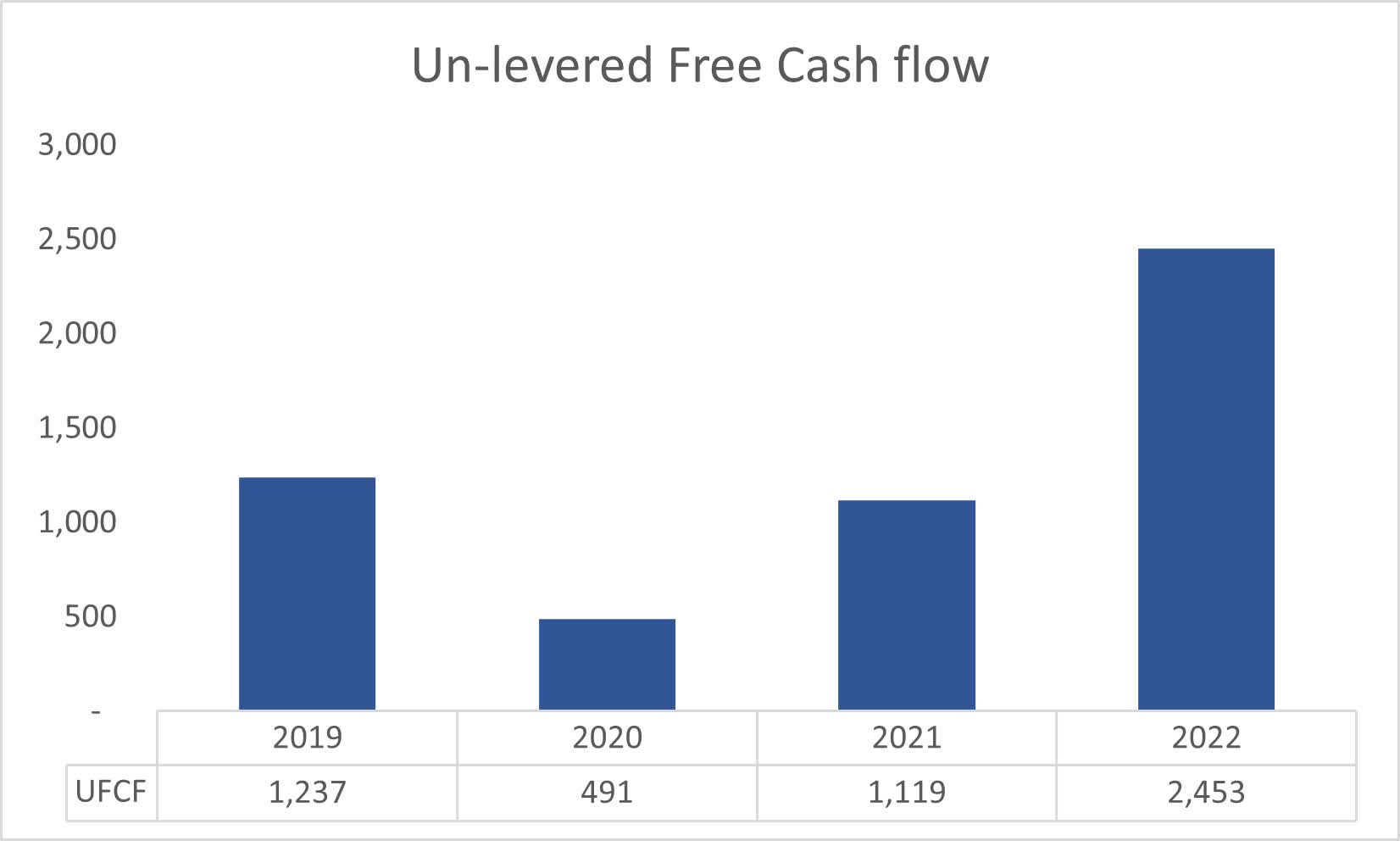

To be honest I am not surprised that the company is undervalued by this much, even with conservative assumptions. When I was going through the company’s financials, I saw that it can generate very strong unlevered free cash flow (UFCF) y-o-y and that is what played such a big role in what the company is worth. The higher the UFCF the higher the valuation of the company, as at the end of the day, the company is worth only what it is able to generate in the long run. This company is very capable of generating fantastic UFCF and I do not see how this can change, but if it does, I will reassess my thesis accordingly.

{kind=link}

Seeing that UMC stock is trading at around $8 a share, it is very easy to open a position right now with very little capital at risk. However, I will wait until the company reports its earnings because I want to hear what the management is going to say about the outlook of the sector and what kind of softness in demand they still see going forward.

I believe the company's ability to generate great FCF in the future and the strength of its balance sheet suggest that the company is a very good long-term investment, one that will reward its shareholders handsomely when the dust settles, and the industry gets more positive attention once again.

For further details see:

United Microelectronics Corporation: A Solid Long-Term Choice