UMC - United Microelectronics: Cruising Past The Semiconductor Slump

2023-10-05 11:57:06 ET

Summary

- UMC is a leading semiconductor foundry trading at an attractive discount to peers, offering a compelling risk/reward for long-term investors.

- UMC has a strong market positioning with geographically diversified capacity and a broad portfolio, allowing it to capitalize on key long-term trends.

- UMC boasts a clean financial profile with an investment-grade balance sheet, robust cash position, and steady cash generation, providing insulation during cyclical swings.

Investment Thesis

United Microelectronics ( UMC ) is one of the leading pure-play semiconductor foundries globally, yet it trades at an attractive discount to peers. Despite near-term cyclical headwinds, UMC is well-positioned for long-term growth thanks to its strong market positioning, clean financial profile, and excellent management. I believe the current bear thesis on UMC is shortsighted, overlooking the company's strengths. At current valuations, UMC offers a compelling risk/reward for long-term investors.

Strong Market Positioning

UMC is a top 5 global pure-play foundry with geographically diversified capacity in Taiwan, Singapore, China and Japan. It has a broad portfolio spanning both mature and advanced process nodes, including leadership in specialty process technologies like RF-SOI, BCD, and embedded non-volatile memory. As UMC states in its annual report, its "goal is to be the foundry solution for SoC (system-on-chip) customer needs" by providing differentiated solutions that "help customers deliver successful results in a timely fashion."

This strong market positioning is allowing UMC to capitalize on key long-term trends like 5G, IoT, EV/autonomous driving, and AI. In recent earnings calls, UMC has noted how its automotive segment has been delivering higher-than-expected growth and is expected to remain a key growth catalyst going forward. The company's exposure to high-growth markets like automotive and commitment to technology innovation position UMC well for the future.

UMC is also aligning capacity expansion with customer demand through long-term agreements (LTAs). As stated on its Q2 2023 call , "LTA is a mechanism to support both customer and us for longer-term perspective, because we want to make sure that the -- the customer wants to make sure their supply is resilient, and we want to make sure that our investments are also somewhat protected." This provides revenue visibility and ensures continued relevance with key customers.

Clean Financial Profile

In addition to its strong market positioning, UMC boasts an exceptionally clean financial profile. The company has an investment-grade balance sheet, with cash and cash equivalents of $5.2 billion against long-term debt of only $1.15 billion.

This robust cash position provides UMC with a substantial buffer during semiconductor down cycles. UMC has been using its cash flows to fund capital investments and pay an attractive dividend. Its dividend payout ratio stands at a reasonable 46%, with an attractive forward yield of 8.37%.

UMC's profitability and returns also remain at healthy levels despite the current downturn. Over the past decade, the company has focused on enhancing its cost structure and efficiency. This allows UMC to deliver mid-30s% gross margins even at lower utilization rates today.

Looking ahead, UMC is making disciplined investments aligned with customer demand. This includes its planned capacity expansion for 28nm and 22nm technologies. UMC's financial strength ensures it can self-fund these investments without taking on significant leverage. Overall, UMC's fortress balance sheet, steady cash generation, and structurally improved profitability provide insulation during cyclical swings. This reduces downside risk while creating potential for upside as demand recovers.

Shortsighted Bear Case

The bear case against UMC appears shortsighted in my view. Bears point to potential loss of orders from integrated device manufacturer (IDM) customers like Texas Instruments (TXN) as they bring capacity back in-house. However, on its Q4'22 call, UMC mentioned its "long-term alignment with the customer" makes this risk unlikely. The foundry business is now viewed as more strategic and IDMs recognize "semiconductor supply chain is essential."

Others suggest UMC may lose orders to Chinese foundries amid geopolitical tensions. However, UMC's specialty technology leadership, manufacturing excellence, geographic diversity, customer relationships, and ESG commitment give it an edge over local players. When asked about China competition on one of its recent earnings calls, UMC expressed confidence in its competitive advantages to "navigate through this current market condition, as well as the competition landscape."

The bear case also overlooks UMC's resilience through past downturns and actions to structurally improve profitability. UMC notes its "effort put in, but there's also the whole big cycle, cyclical impact" on financials. At trough levels, UMC's profitability is clearly higher than past down cycles, thanks to years of productivity enhancement. I believe the market's already pricing in the cyclical slowdown.

Attractive Valuation

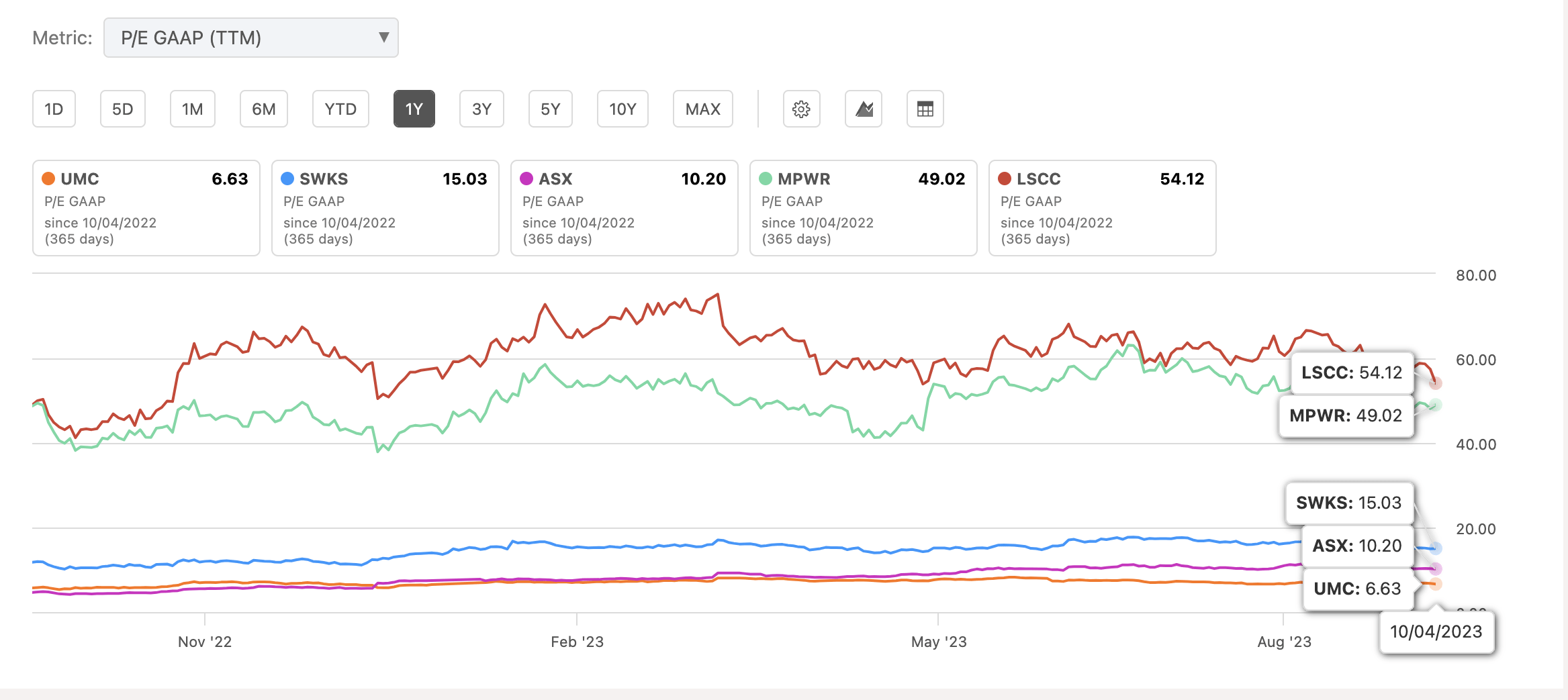

UMC offers a compelling valuation versus peers, trading at just 9.3x P/E on a forward basis, that's way below its peers.

{kind=link}

Critically, UMC has a pristine balance sheet that provides downside protection in case of a prolonged downturn. UMC also pays an attractive dividend yield that is supported by a reasonable payout ratio.

For long-term investors, UMC offers a quality business at a substantial discount to intrinsic value. Assuming a modest 5% Revenue CAGR and a valuation expansion to 15x earnings in 2027, I estimate over 50% upside in the stock.

Risks

Key risks to UMC include cyclical semiconductor downturns, competitive pressures, technology transitions and geopolitical issues involving Taiwan/China. However, UMC has successfully navigated past industry cycles and is well-positioned competitively. While additional volatility is likely given macro uncertainty, and there may very well be a better entry point in the future, I believe UMC's risk/reward remains compelling for long-term investors at current valuations.

Conclusion

In summary, UMC is a high-quality semiconductor foundry with strong market positioning and technology leadership. Concerns around customer loss and China seem overblown compared to UMC's competitive strengths and customer alignment. Despite near-term headwinds, UMC is poised for long-term growth from key trends like EV, 5G, and AI. Trading at just 9 times forward earnings, UMC offers compelling value for investors with a 3-5 year time horizon.

For further details see:

United Microelectronics: Cruising Past The Semiconductor Slump