UMC - United Microelectronics: Cyclical Improvement Offers A Positive Outlook For 2024

2024-01-11 17:25:47 ET

Summary

- UMC's revenue fell this year owing to weak end markets, but both PC and wireless markets are seeing signs of recovery.

- The company has niche offerings in mature semi processes which have proven resilient while its customer base is diverse and sticky.

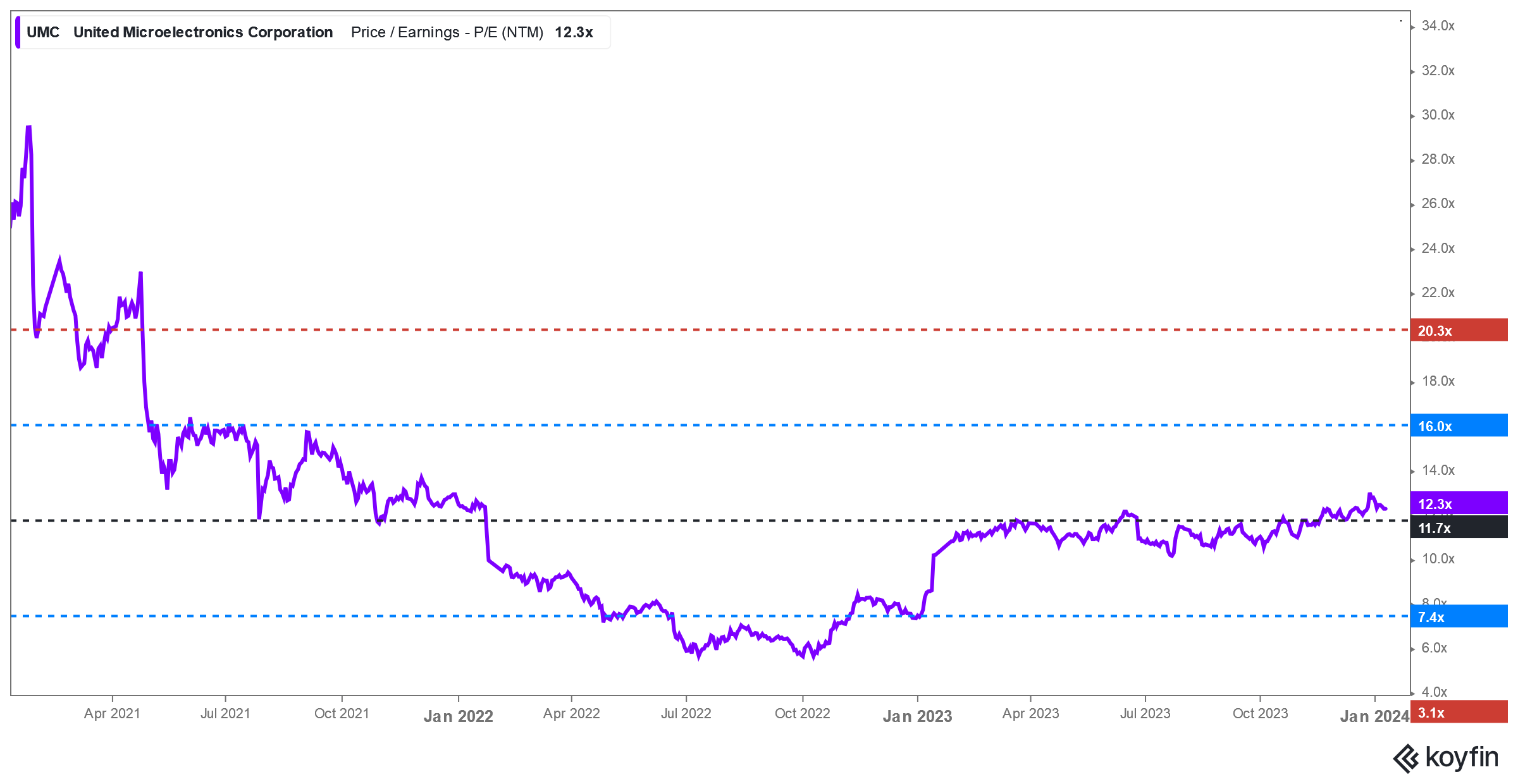

- UMC trades at about 12x P/E which is undemanding for a company that is looking at cyclical improvements as the industry recovers.

United Microelectronics ( UMC ) shares have generally lagged the broader market in the past year and well behind semi leaders such as Nvidia ( NVDA ) and TSMC ( TSM ). UMC's revenue is estimated to be down about 21% in FY23 after growing 31% in FY22 due to a lackluster smartphone and PC market. The company does not currently have any advanced node processes for AI chip development, which can explain why it has not participated in the AI fueled rally. But, traditional end markets are showing signs of recovery and trailing-edge semis are poised to make a comeback.

3Q23 was better than feared

The company's margins were better than previously guided, with gross margin and operating margin at 35.9% and 26.8%, respectively. That is in-line with 2Q's 36% and 27.8%, respectively.

Based on the company's post-quarter announcements, 4Q23 sales is estimated to be about TWD54.9B, which implies a decline of 19% y/y. However, this is a sign of stabilization, as the prior two quarters registered 22% and 24% y/y drops.

Robust guidance

The company sees rush orders in 4Q for both PC and smartphone markets, partially offset by declining automotive demand due to inventory correction. UMC guides for a 5% q/q wafer shipment drop in 4Q, but a flat ASP. Because of a lower expected utilization rate of low 60%'s compared with 3Q's 67%, gross margin is set to fall to the low 30%'s.

But since we now know of 4Q sales, the figure is predicted to come in with about 3.9% q/q decline, which is better than previously guided. Gross margins will also likely see a better outlook.

Its US$3B capex for 2023 remains unchanged as management sees 22nm/28nm demand longer term.

Revenue growth to turn positive midyear 2024

UMC is likely to gain market share in the global AMOLED driver IC market. The company's 22nm/28nm offerings are competitive due to customer stickiness, diverse product portfolio, and technology differentiation, so it will continue to expand its 22nm/28nm market share with applications in OLED, driver ISP, Wi-Fi, and SoC processors.

UMC will transition into more specialty technology for its mature 12-inch nodes where new promising market opportunities will possibly come from notebook and tablet space such as RF SOR, non-volatile memory, and high voltage.

Stabilizing end markets

Downstream customers have generally given better outlooks for end markets such as PC and wireless. The PC market is expected to rebound with growth in the mid-single digits after a mid-teens decline in 2023.

Driven by an uptick in Android demand, the wireless market appears to be recovering. Mobile chipmakers are seeing stronger growth in Chinese OEMs and we expect smartphone shipments to increase near 10% in 2024 after a high single digit decline in 2023.

The datacenter outlook appears to be mixed due to an ongoing inventory correction, but partially offset by AI tailwinds.

DRAMs are also seeing a strong lift, according to Trendforce's DRAM exchange. DRAM contract prices are predicted to surge 13-18% in 1Q24, led by mobile. Manufacturers are keen on cutting production to maintain a steady supply and demand landscape. Given that DRAMs are key components in many consumer electronics, ASPs going up tend to indicate that end demand is gaining.

Valuation

UMC is trading at about 12 times forward earnings, near its 3-year historical average. The company and the industry are coming out of a prolonged earnings recession due to excess capacity during the pandemic. Helped by its niche technological offerings and a diverse and sticky customer base, the company is expected by the market to deliver about 14% average sales growth for FY24E/FY25E and about 6% average EPS growth during the same period.

Thus, valuations are undemanding for a company/industry returning to growth.

{kind=link}

Himalayas Research, Koyfin

For further details see:

United Microelectronics: Cyclical Improvement Offers A Positive Outlook For 2024