UMC - United Microelectronics: Looks Like Tough Year Ahead

Summary

- Inventory adjustments will play a key role in the performance of UMC in the first half of 2023 - especially in the PC and smartphone space.

- Over the long term, auto and industrial will be the primary focus of the company.

- Based upon current visibility, management sees that overall, 2023 is going to be a challenging year.

United Microelectronics ( UMC ), as with most companies competing in the semiconductor industry, has had its share price take a hit over the last couple of year, with it reaching a 2-year high of approximately $12.70 on November 29, 2021, and falling to a low of $5.36 per share on October 10, 2022, afterwards rebounding to $7.00 per share as I write.

{kind=link}

In its last earnings report, it had a decent beat on revenue but missed on EPS, as the company guided for 2023 to be a challenging year; lowering expectations in the PC and smartphone space while saying auto and industrial were stable at the time of the earnings call.

As for full-year 2023, it sees the total addressable market declining, with the first half being particularly challenging, based upon the visibility the company has at this time.

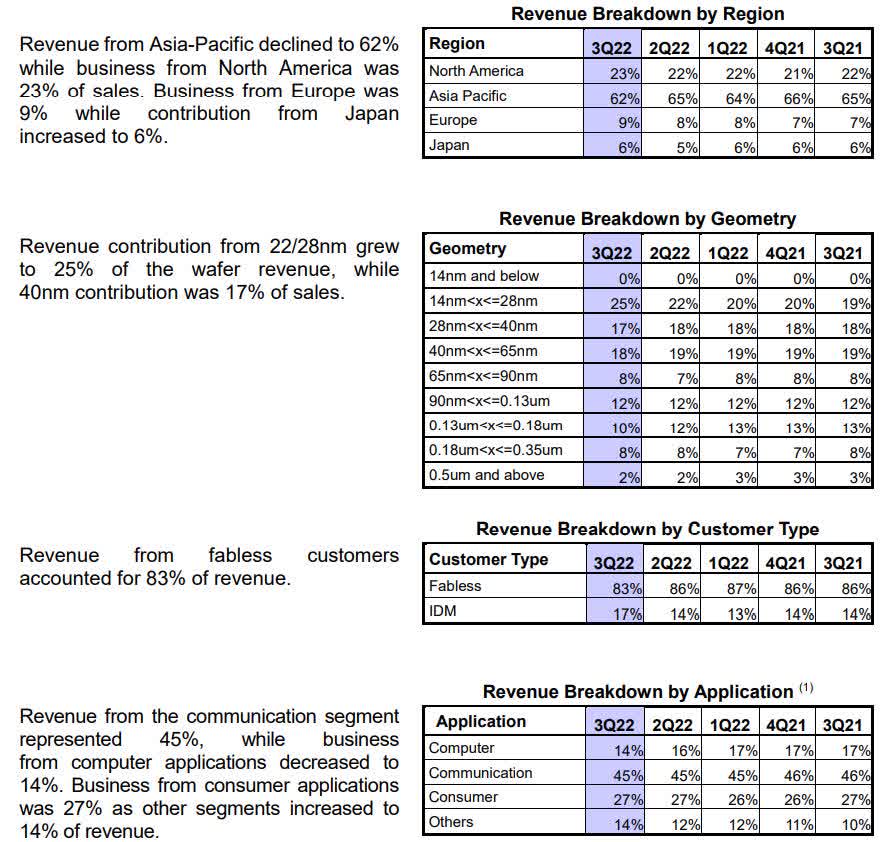

While automotive revenue grew in the double digits in the third quarter and consumer in the low single digits; consumer and communications grew in the low single digits; and computing was down in the high single digits.

As the company headed into the fourth quarter of 2022, it saw all the segments dropping, with the exception of automotive. In this article, we'll look at some of the numbers from its latest earnings report, the inventory challenges in some of the segments it competes in, and how 2023 looks to be shaping up.

Some of the recent numbers

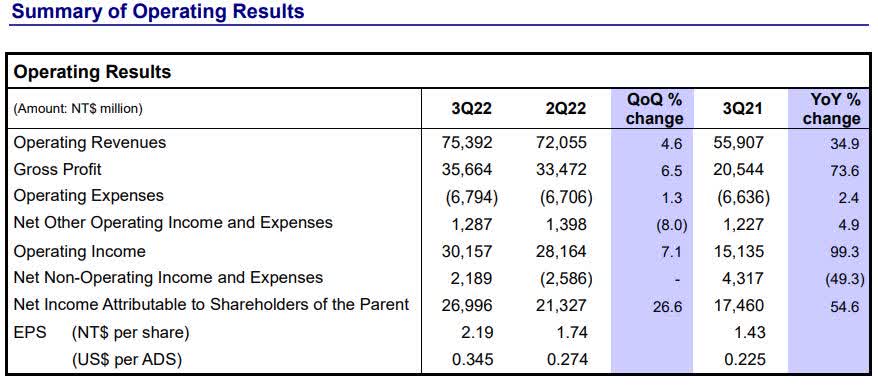

Revenue in the third quarter was NT$75,392 billion, an increase of 34.9 percent from revenue of NT$55,907 billion in the third quarter of 2021, and up 4.6 percent from the NT$72,055 billion in revenue in the prior quarter.

{kind=link}

The quarterly revenue increase came from a more favorable product mix and foreign exchange rate.

Net income in the reporting period was NT$26,996 billion, or NT$2.19 per share, compared to net income of NT$17,460 billion, or NT$1.43 per share in the third quarter of 2021.

Gross margin in the third quarter of 2022 was 47.3 percent, with operating margin at 40 percent in the quarter, up sequentially from 39.1 percent.

For the first nine months of 2022 revenue was up 37 percent year-over-year. That was attributed to depreciation in the NT dollar, ASP enhancement, and an increase in shipments.

Net income in the first nine months of 2022 was NT$68,131 billion, up 71 percent year-over-year, and EPS for the first nine months of 2022 was NT$5.54 per share.

At the end of the third quarter of 2022 the company had cash and cash equivalents of NT$180.65 billion, compared to cash and cash equivalents of NT$113.11 in the third quarter of 2021. Total liabilities at the end of the third quarter of 2022 were NT$204.21 billion, compared to total liabilities of NT$171.19 billion at the end of the third quarter of 2021.

{kind=link}

Latest sales confirm slowdown

In its third quarter earnings report, the company pointed out the total addressable market for full-year 2023 was probably going to drop, and at the time saw it already starting to fall heading into the fourth quarter.

After releasing a couple of monthly sales releases since then, the numbers confirm its addressable market is already contracting.

{kind=link}

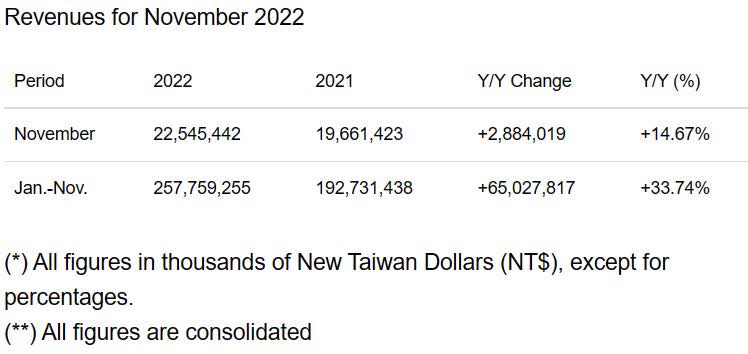

For example, revenue in the third quarter of 2022 was up 34.9 percent, while sales in November 2022 , came in at NT$22,545 billion, up 14.67 percent, but showing signs of slowing down.

Most recently it released its December sales numbers , and they were at NT$20,946 billion, up 3.29 percent year-over-year. With full-year 2022 revenue up 30.84 percent, it reinforces the company's outlook that the market is rapidly slowing down.

{kind=link}

Assuming the pace continues, we will see comps start to be negative concerning sales, especially with some decent numbers in the first two quarters of calendar 2022.

Inventory levels, a big catalyst

When analyzing UMC at this time, the biggest factor, in my opinion, is the inventory levels in the various segments it competes in.

Looking at Q4, the company saw auto and industrial segment inventory levels as being at healthy levels, which is why management said the auto and industrial segment remained stable for now.

I'm not convinced that is going to continue if the economy continues to weaken as expected. Under that scenario, combined with the ongoing inventory challenges in computer and smartphones, it would be a big headwind for the company throughout the next year, and possibly beyond if the recession goes deeper for longer.

As for PCs and smartphones, the company sees the correcting of inventory an ongoing process, and it's not likely to be mitigated in the near future. With lower demand it and the time it'll take to work through existing inventory, it will likely take through at least the first half of 2023 before those segments start to turnaround.

The company acknowledged that it won't be until the bottom of the down cycle before momentum returns to those segments. With that in mind, management says there is little visibility at this time as to when that will happen.

One thing they did say was the digestion of PCs and the smartphones is happening at a slower pace than they have previously estimated, suggesting those segments are going to be a drag on the company for some time.

In other words, until there is a sell-through to end markets, the inventory drag will remain on UMC. And as mentioned above, if auto and industrial demand starts to falter, that could create inventory challenges in those segments too. At this time, the company hadn't seen that happening, but considering the macro-economic environment, it's definitely a strong possibility if the economy goes further south.

Conclusion

The major metric to watch for UMC is the inventory levels of the markets it competes in. We already know the PC and smartphone markets are going to remain under pressure because of high inventory levels that will take time to sell through.

Taking into account the correction in inventory and inflation increasing costs, management clearly stated it expects the "semi and foundry industry" to decline in 2023.

With revenue growth already losing momentum in the last two months of 2022, and tough comps for the first two quarters of 2023, I think the stock is going to take some tough hits in 2023.

That's especially true because the share price, for no visible reason, has jumped Since October 10, 2022, and is trading over $1.50 more per share since then, when it was trading at $5.36 at a low. I think the stock is set up for a pullback, and if the numbers in the next earnings report confirm and reflect the slowdown, it's going to take a big hit. Further out, I believe UMC has the potential for a nice rebound, but that isn't likely to happen in the near future, especially with the weaknesses associated with inventory levels and if auto and industrial slows down and creates another inventory choke point.

The best way to look at UMC at this time, in my view, is to wait for a pullback to add to a position or take a new position, if you like the company. I see nothing in the short term that would suggest it can surprise to the upside, which means the money to be made will be after it corrects. I don't think it's going to take too long before that opportunity comes, even with the share price of the stock showing some strength in the last three months.

For further details see:

United Microelectronics: Looks Like Tough Year Ahead