UMC - United Microelectronics: Solid Upside Despite Sales Slide (Intrinsic Valuation)

2023-07-07 05:30:50 ET

Summary

- In this article, I aim to conduct an intrinsic valuation on UMC's stock to see if the recent dip in sales has affected its long-term upside.

- UMC's profit is expected to face temporary pressure during the current semiconductor downcycle, with recovery anticipated from 2024.

- UMC is shifting its strategy towards increasing sales to the automotive market, driven by electrification, autonomous driving, and improved connectivity.

Investment Thesis

Even after taking into account the declining sales trend, United Microelectronics Corporation (UMC) looks undervalued by over 20%, based on a discounted cash flow ((DCF)) analysis. UMC is well-equipped to maintain market share and protect margins in the long run due to its strong competitive position in the microchip foundry industry and strategy to further penetrate the automotive segment, where demand is being driven by the electrification wave.

(For an excellent relative valuation of UMC's stock, and in-depth competitive assessment, see Seeking Alpha Analyst Robert Castellano's newly-published article here ).

Strong Market Position

UMC on Thursday revealed that June sales dropped over 23% year-over-year, a month after a similar dip in May. Revenue is now down 18.4% for the first six months of 2023. The stock price is down over 6 percent since the May sales report, despite being up 20% in the past year. However, the long-term outlook looks positive given the company's strong market position.

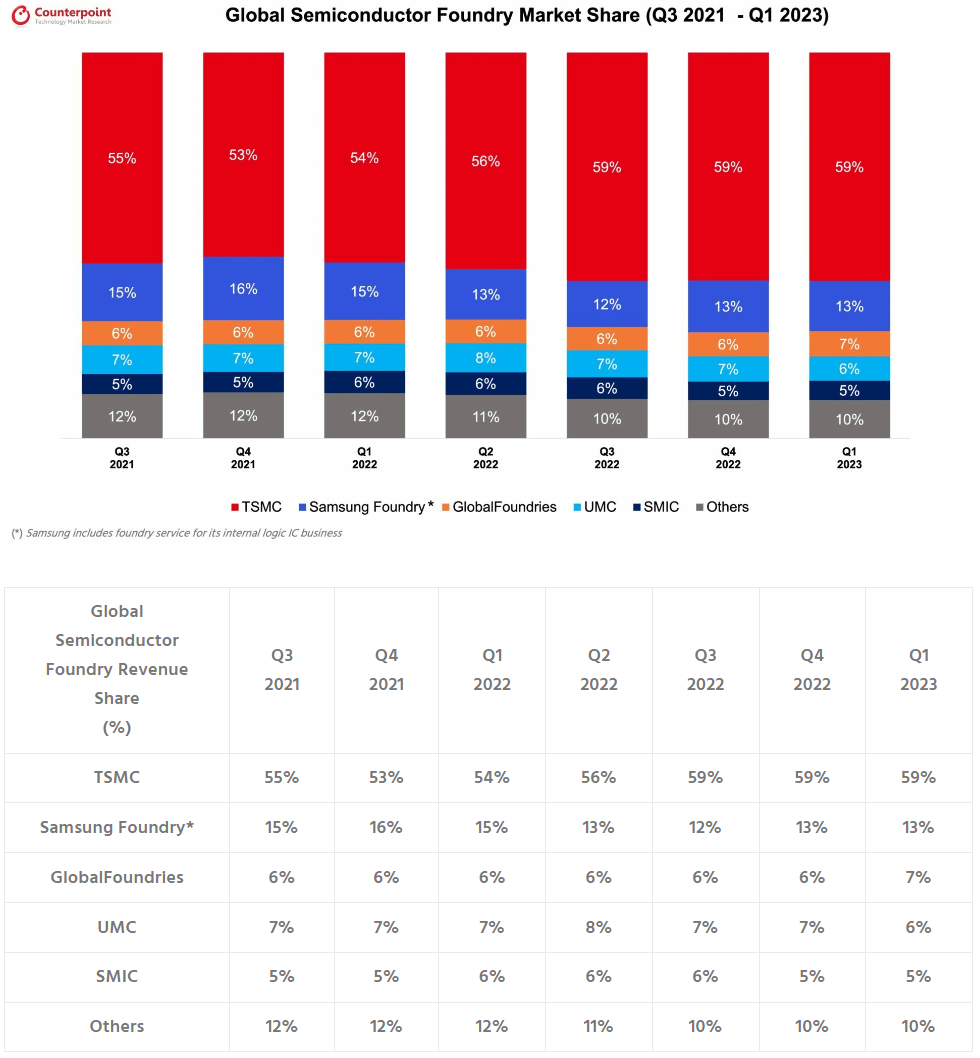

UMC is among the select few companies that are currently dominating the global semiconductor foundry industry, securing about 6% of market share in Q123, according to the Counterpoint research firm. Taiwan Semiconductor Manufacturing Company Limited (TSM) dominates the industry, with nearly 60% of market share in the most recent quarter - with SMIC, GlobalFoundries (GFS), and Samsung Foundry rounding out the top five.

Global Microchip Foundry Market Share (Counterpoint Research)

{kind=link}

The global semiconductor foundry market, which reached about $137 billion in size in 2022, is expected to grow by a CAGR of 8% from 2023-2029, according to Valuates Reports . Demand will largely be driven by integrated circuits (IC) found in vehicles, consumer electronics, medical equipment, military equipment, and smart home appliances.

This is an industry that has high barriers to entry in terms of investment, startup costs, technology, and expertise. However, a key concern is whether UMC's share will shrink in the long run as TMSC continues to increase its dominance.

That said, I believe UMC will be able to, at a minimum, maintain market share and protect margins by penetrating business segments like automotive, where growth will be driven by, as Fitch wrote in a June ratings, "electrification, autonomous driving and improved connectivity."

UMC itself indicated that the automotive end market, which accounted for 17% of company revenue in the first quarter , will be a key growth driver as the IC content in vehicles continues to increase, driven by electrification.

Moreover, TMS focused on a different segment, with over half of sales deriving from 5nm and 7nm chips. UMC, on the other hand, saw most of its revenue come from 22/28nm, 40nm, and 65 nm node chips.

To be honest, I think there is little doubt UMC will continue being a dominant player in the microchip foundry market in the long-term. The real question I have is a simple one: is this reality already fully backed into the stock price?

Intrinsic Valuation

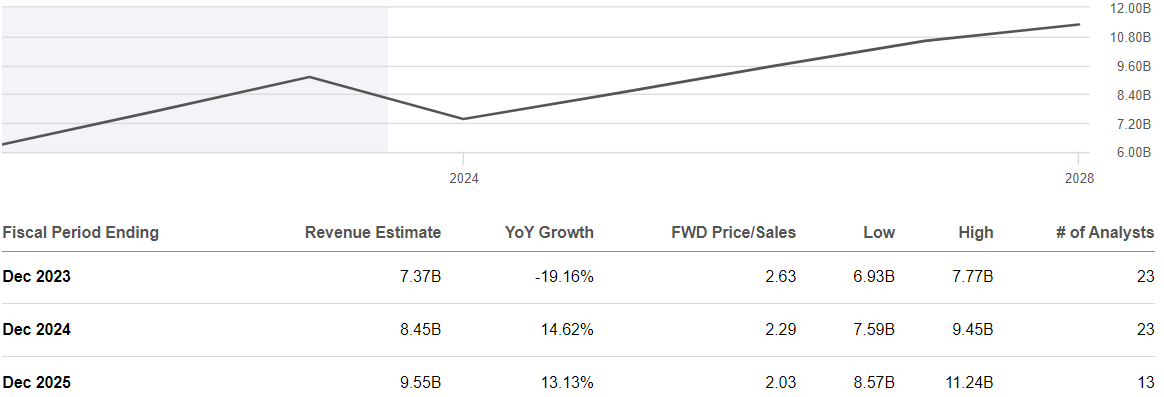

UMC has signaled 2023 would be weaker, but expected a turnaround in 2024, and analysts covering the stock appear to have a similar viewpoint. According to the average estimate of 23 analysts, after dropping almost 20% in 2023, the company's revenue is expected to climb over 14% next year. The average estimate of 13 analysts has the stock price rising over 13.13% in 2025.

{kind=link}

For the ten-year DCF analysis, I will use these figures for the top line in years 1-3, and then use the market research firm's growth rate of 8% and move toward a global GDP average GR of 3% (30-year annualized).

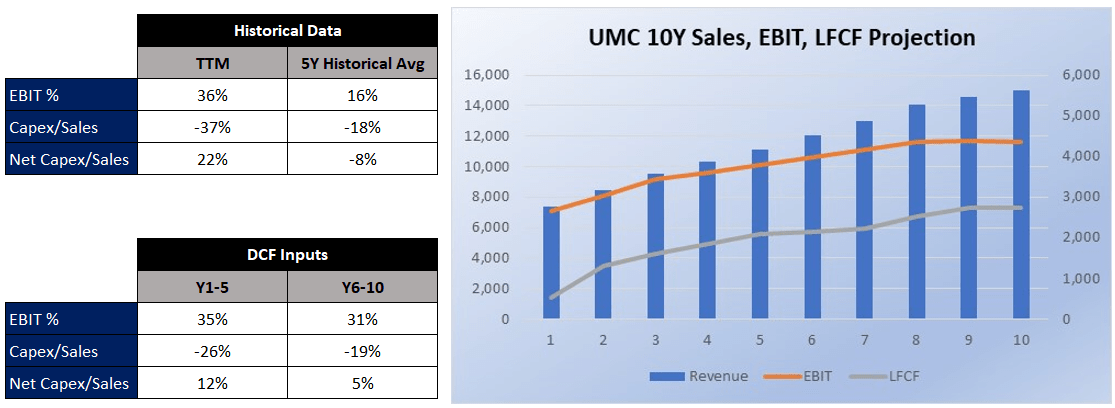

Here is a table summarizing assumptions used behind the other inputs. The first table shows historical data including TTM, 5-year averages, and industry average for EBIT and capex figures, which partly guided my thinking on the DCF inputs in the lower table.

{kind=link}

I relied on TTM for year 1 for EBIT and capex numbers and then moved them toward the industry average initially and then the company's historical average in some cases. The current 10 year EBIT average in the model is 33%, which seems a bit ambitious. But we are starting from a TTM of 36%, and then gradually lowering after the first 5 years. The first five years of heavy investment will lead to even more efficiencies.

If anything, one could argue the margins should improve - toward TSMC's operating margin of 49%. However, I'm not prepared to go that far. I think maintaining margins alone is a reasonable expectation. Anything much lower is being conservative beyond reason, and the other route is being bullish without facts or historical grounding given the type of products they are focused on versus TSMC.

The semiconductor industry averages for capex/sales (~30%) and net capex/sales (~9%) I sourced from Aswath Damodaran . Finally, the discount rate is based on the 30-year average annual return of the S&P 500, including dividends, rounded up to 10 percent. As you can see, according to the DCF calculation, UMC is undervalued by 22%.

{kind=link}

Risks

A major key external risk is that the microchip foundry industry does not bounce back in 2024 as widely expected. Or, UMC's strategy to more deeply penetrate the automotive segment does not pan out. Internally, there is the risk UCM fails to maintain both market share and operating margins. The company is investing quite a bit on capital expenditures over the next 1-3 years. If UMC fails to convert these capital layouts into growth, the margins will get squeezed. There is also a chance they do not execute in pursuing the right product mix and end up feeling price pressures. They will not be afforded the same types of luxuries as TSMC on this front, and will have to be more vigilant and active in protecting margins.

Finally, one of those elephants in the room. Geopolitical risks are obviously real - and something UMC explicitly mentions in its company filings. The problem is, I am at a loss at how to quantify that type of geopolitical risk. The best case scenario is that the U.S., China, and Taiwan peacefully coexist to an extent that does not impede free market transactions. Should the trade war heat up, there is actually a chance UMC might benefit if customers are forced away from China. However, if the worst case scenario occurs, all bets are off. I would say such a development is unthinkable - but I also never imagined Russia would invade Ukraine.

Conclusion

UMC may be a bumpy ride in 2023, with the overall market weakening, but a turn-around is widely expected next year. In the long run, there is little doubt UMC will continue being a dominant player in the microchip foundry market. The real question is determining if this upside is priced in yet. Based on a DCF calculation, I concluded that it is not. The stock remains undervalued, despite the June drop in sales, and in my mind is a solid long-term buy.

For further details see:

United Microelectronics: Solid Upside Despite Sales Slide (Intrinsic Valuation)