USFD - United Natural Foods: Still A Fantastic Prospect Despite Mixed Results

Summary

- United Natural Foods has successfully outperformed the broader market in recent months, despite mixed financial performance.

- Even so, the stock has fallen and investors seem to be pessimistic at this time.

- Given how cheap shares are, though, the company does offer nice upside potential from here.

Normally, when you think that a company might be a bullish prospect, you might think that a positive outcome by buying into the stock in question would be to see that share price rise. But during times of extreme market volatility, sometimes it's good just to beat the market. One great example of this can be seen by looking at United Natural Foods ( UNFI ). This food distributor, which provides natural, organic, specialty, produce, conventional grocery, and other related offerings to its customers, has been doing well to grow its top line while generating attractive cash flows during what has been a difficult economic environment. On top of this, shares of the business look significantly undervalued compared to what other opportunities exist in this space. Although the company has experienced some downside in recent months, shares still have meaningfully outperformed the broader market, aligning with my view of what it means to be an attractive prospect for value-oriented investors.

Not as tasty as I would have liked

Back in the middle of March of this year, I wrote an article that took a very bullish stance on United Natural Foods. In that article, I talked about the company's robust fundamental performance. I felt as though revenue and profitability were likely to continue growing year over year. On top of this, even though the broader market looked uncertain, shares of the business were attractively priced on both an absolute basis and relative to what other firms were trading for. At the end of the day, this all led me to keep my 'strong buy' rating on the business, indicating my belief that shares should significantly outperform the broader market for the foreseeable future. Normally, I would have liked to see shares actually increase since writing about the firm. But by definition, the company has achieved the kind of outperformance I anticipated, with shares generating downside of only 7.8% while the S&P 500 declined 15.2%.

{kind=link}

To understand why the company has been performing at a level that is so much higher than what the broader market has achieved, we should discuss how the company's fundamental performance has been. For starters, let's touch on how the business finished off its 2022 fiscal year . During that year, sales came in at $28.93 billion. That represents an increase of 7.3% over the $26.96 billion the business generated the same time last year. There were multiple components behind this sales increase. In absolute dollar terms, the largest portion of the revenue increase came from its independent retailer customer channel. Revenue there jumped by 10.9% from $6.64 billion to $7.36 billion. This was driven largely by a supply agreement that the company established with a new customer in the first quarter of 2022, and it was also driven in part by an increase in sales to existing customers. On a percentage basis though, the biggest increase involved its Supernatural business, with revenue there spiking 13.2% from $5.05 billion to $5.72 billion. This was really thanks to growth in existing store sales, including the supply of new product categories that were previously impacted negatively by the COVID-19 pandemic. New fresh food categories like bulk and ingredients used for prepared foods, as well as the impact associated with inflation, all playing a role here as well.

With the rise in revenue, profits for the company also improved. The company went from generating a net profit of $149 million to generating a profit of $248 million. Other profitability metrics were somewhat mixed. For instance, operating cash flow actually declined, plummeting from $614 million to $331 million. But if we adjust for changes in working capital, this metric would have risen from $461 million to $697 million. Over that same window of time, EBITDA of the company also improved, rising from $770 million to $829 million. Management attributed much of these improvements to increases in the firm's wholesale segment margin rate because of efficiency initiatives embarked on by the firm. Other factors also came into play, such as a reduction in restructuring, acquisition, and integration-related expenses. But those should be considered more one-time in nature.

{kind=link}

When it comes to the 2023 fiscal year, the picture for the business remains mixed. Revenue in the first quarter of the year , for instance, came in strong at $7.53 billion. That's 7.6% above the nearly $7 billion reported at the same time in 2022. Once again, the independent retailer side of the business was the heavy lifter here, with sales jumping 11.3% from $1.75 billion to $1.95 billion. Just as was the case previously, management attributed this to a new supply agreement with a new customer. Existing customers were also a source of revenue growth during this time. Supernatural sales came in second on a percentage basis, with revenue there jumping by 9.8% thanks largely to growth in existing store sales, including the supply of new fresh categories. Inflationary price increases and increased sales to new stores were also instrumental in this regard.

On the bottom line, the picture has also been mixed. Net income went from $76 million in the first quarter of 2022 to $66 million the same time this year. Much of this was driven by a reduction in the company's cost of sales category, with changes in customer mix as the company continues to grow revenue with its larger customers, playing a vital role in this regard. Operating cash flow fared even worse, going from negative $81 million to negative $262 million. But if we adjust for changes in working capital, it would have inched up from $165 million to $167 million. Over that same window of time, we saw a similar increase in EBITDA, with the metric climbing from $200 million to $207 million.

When it comes to the 2022 fiscal year in its entirety, management expects adjusted earnings per share of between $4.85 and $5.15. Given the company's current share count, this would imply net income of $308 million at the midpoint. Of course, the company could end up reducing its shares. In the first quarter alone, management completed the purchase of 339,000 shares for $12 million. As a side note, the company also factored some of its accounts receivable in order to bring in $253 million that it elected to use to pay down debt. But that is not reflected in this article due to a lack of clarity. The only other substantive guidance involved EBITDA. Management is forecasting that to come in at between $850 million and $880 million. If we assume that adjusted operating cash flow should rise at a similar rate, then a reading of $727.3 million would appear logical.

{kind=link}

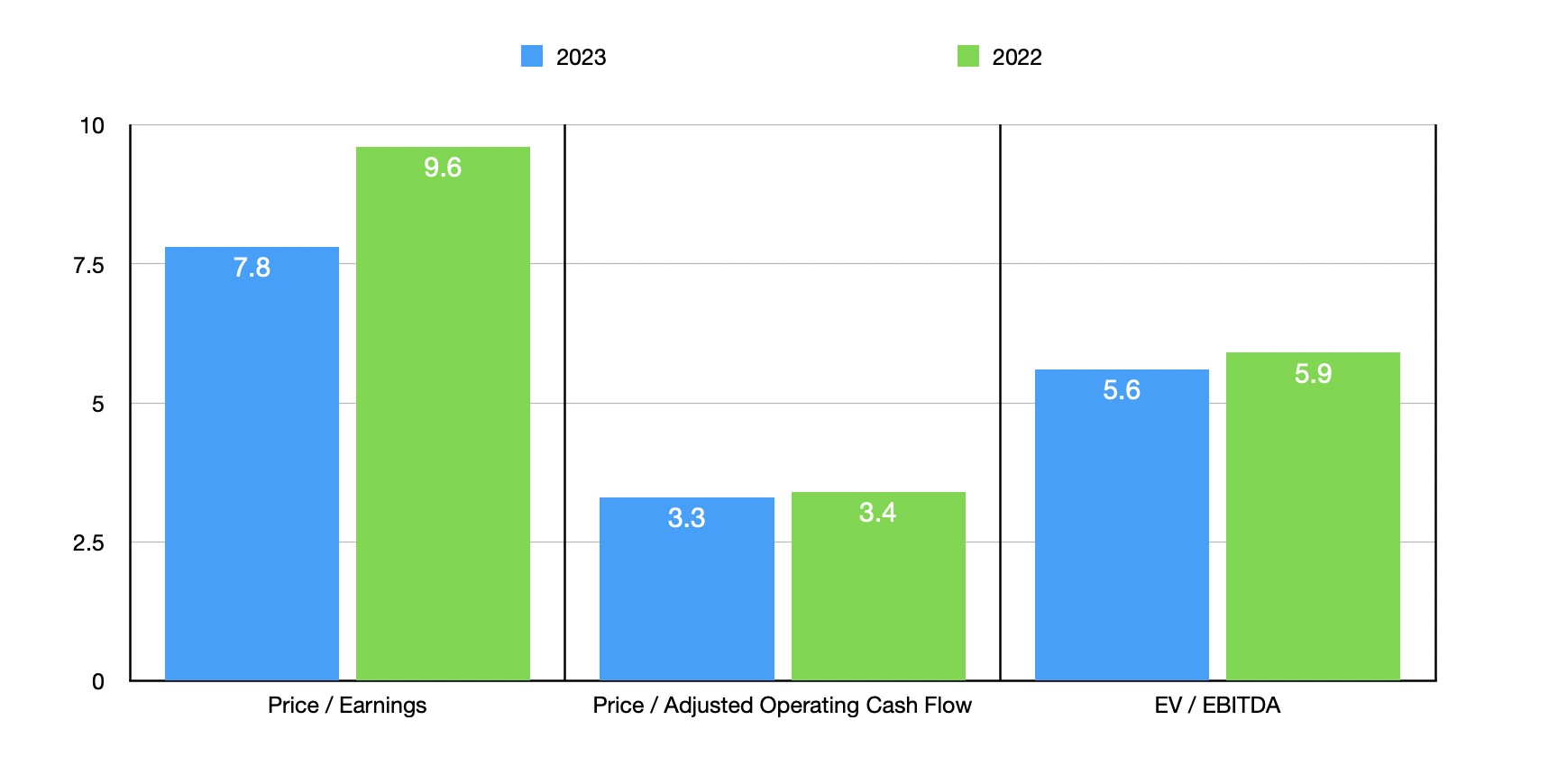

On these figures, the company is trading at a forward price-to-earnings multiple of 7.8. The forward price to adjusted operating cash flow multiple would be 3.3, while the EV to EBITDA multiple would come in at 5.6. This pricing is not too radically different from a cash flow perspective if we rely on the data from the 2022 fiscal year that can be seen above. As part of my analysis, I also compared the enterprise to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 8.3 to a high of 45.3. In this case, only one of the five companies is cheaper than our prospect. Using the price to operating cash flow approach and the EV to EBITDA approach, we can see from the table below that United Natural Foods was the cheapest of the group.

| Company |

| Price/Earnings |

| Price/Operating Cash Flow |

| EV/EBITDA |

| United Natural Foods |

| 9.6 |

| 3.4 |

| 5.9 |

| The Andersons ( ANDE ) |

| 8.3 |

| N/A |

| 6.0 |

| Performance Food Group Company ( PFGC ) |

| 45.3 |

| 16.4 |

| 13.5 |

| SpartanNash Company ( SPTN ) |

| 20.3 |

| 45.8 |

| 8.7 |

| US Foods Holding Corp. ( USFD ) |

| 38.9 |

| 15.6 |

| 14.2 |

| Sysco ( SYY ) |

| 27.7 |

| 21.7 |

| 15.0 |

Takeaway

Although we are seeing some volatility from a share price and profitability perspective, the overall picture for United Natural Foods Looks quite positive to me. The company continues to grow its revenue while largely maintaining positive and growing cash flows. Yes, net income could be better. But considering the pressures facing the firms in this space, and how cheap shares currently look on both an absolute basis and relative to similar firms, I cannot help but believe that the 'strong buy' rating I've signed to the stock previously still makes a great deal of sense.

For further details see:

United Natural Foods: Still A Fantastic Prospect Despite Mixed Results