UOVEF - United Overseas Bank: Attractive Growth Potential And Dividend Yield

2023-07-24 11:08:01 ET

Summary

- United Overseas Bank has acquired Citigroup’s consumer banking businesses in various Asian markets, diversifying its portfolio and doubling its customer base in these regions.

- The acquisition is expected to contribute positively to UOB's earnings per share and return on equity by 2023, with a target of achieving a return on equity of over 13% by 2026.

- UOB's strong capital position and reasonable non-performing loan ratio make it a worthwhile long-term investment, offering a solid dividend yield and good growth potential.

Editor's note: Seeking Alpha is proud to welcome Young Investor Analytics as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

United Overseas Bank Limited [UOB] ( UOVEY , UOVEF ) is one of the three major Singapore-based banks. UOB presents an appealing investment opportunity with strong growth prospects and solid fundamentals. It has a long history of excellent performance and its recent acquisition of Citigroup's consumer banking business in several Asian markets is expected to be a key driver of growth in the coming years, diversifying its portfolio and reducing dependency on the Singapore market.

In my view, the bank's strong capital position and limited impact of the Basel IV regulations on capital adequacy ratios make the need for a dilutive capital raise unlikely, ensuring its shareholder-friendly dividend policy remains intact. UOB's undemanding valuation, with a low forward P/E ratio and reasonable forward P/B ratio, coupled with a competitive dividend yield, make it an attractive stock for investors seeking long-term growth potential and stable dividends to buy.

The Citi Group Consumer Banking Acquisition

UOB announced its acquisition of Citigroup's consumer banking businesses in Indonesia, Malaysia, Thailand and Vietnam early last year. In terms of the agreement, UOB would purchase these consumer banking units from Citigroup for around $3.7 billion, marking UOB's biggest acquisition in nearly two decades. This acquisition also doubles UOB's customer base in these four South East Asian nations, where it already had sizable existing operations.

The bank has recently completed the acquisition of the Vietnam business after earlier completing the acquisition of the units in Thailand and Malaysia. The management expects to finalise the acquisition of the Indonesian business by the end of 2023. It also anticipates that the deal will immediately enhance the earnings per share ((EPS)) and return on equity ('ROE') if one-off transaction costs are excluded. Even after factoring in these costs, the deal is expected to contribute positively to EPS and ROE by 2023. By 2026, the management's target is to achieve an ROE of over 13% and a Return on Risk-Weighted Assets (RoRWA) of approximately 2%.

From early indications, the parts of the acquisition which have been completed have already contributed positively to UOB's overall results. While the bank has seen declines in loans in its home market of Singapore, loans in its ASEAN portfolio has expanded by 9% in the first quarter of 2023. The acquisition has further positioned UOB as one of the top three card issuers in both Malaysia and Thailand. Upon the completion of the acquisition in Indonesia, its status will also be elevated from the 9th largest bank in the country to the 5th largest bank. As growth in loan demand slows down in its home market, the greater demand in these fast-growing emerging markets will become increasingly important to the bank.

The Bank's Capital Position And Asset Quality

Singapore is engaged in an ongoing reform of its banking regulations to implement the Basel regulations. The latest changes in terms of the Basel IV regulations will see a revision of the methodology used to calculate risk-weighted assets. These changes will reduce the level of control that banks have over the risk-weighting attached to assets and seek a somewhat more standardized approach.

Nevertheless, most analysts expect that the changes will have a limited impact on the Singapore banks given their diversified portfolios. While UOB's Common Equity Tier-1 (CET1) Capital Adequacy Ratio ((CAR)) is the lowest of the Singapore-based banks, it remains comfortably above the regulatory minimum of 6.5%. In my opinion, even a change in the calculation of risk-weighted assets is unlikely to result in a substantial decline in the bank's capital ratios.

Capital Adequacy Ratio (Author created chart based on data from company fillings)

The bank has also indicated that it expects the fully implemented Basel IV to have a limited impact on its capital adequacy ratios. The bank had initially expressed concern that the updated methodology would see extra risk weightings attached to its SME portfolio. However, in a recent earnings call, the CFO noted, "At the final number [of the fully implemented Basel IV regulations], we will be neutral or slightly positive. Our SME portfolio will benefit. We were worried during the transition that [regulators] would put additional weights there. So, the SME portfolio is a lot better [than previously]".

Its strong current capital position and limited impact of the Basel IV regulations on capital adequacy ratios accordingly make the need for a dilutive capital raise somewhat unlikely. Furthermore, the bank's strong capital position means that its shareholder-friendly dividend policy can be retained without attracting concern from banking regulators.

UOB has also retained a reasonable non-performing loan ('NPL') ratio of around 1.6%. While this is again somewhat higher than that of its Singapore-based peers, this remains relatively low for the banking sector at large. Furthermore, there appears to be some positive signs as NPL formations have slowed down in the first quarter of 2023 compared to previous quarters. In the first quarter of 2023, non-performing asset formation came in at around SGD 301 million compared to an average of more than SGD 400 million in the previous four quarters. In my view, improving asset quality and lower loan-loss provisions could have a material positive impact on the bank's earnings in the near term.

Earnings Outlook

UOB was the first of the major Singapore-based banks to report a slight decline in its net-interest-margin [NIM] quarter-over-quarter. The bank reported a NIM of 2.14% compared to a NIM of 2.22% the previous quarter. This decline came about after the bank started offering depositors higher interest rates in an effort to attract more deposits amidst increased outflows of deposits which had presented itself in early 2022.

Deposits seem to have stabilized since, with deposits in its core Singapore market increasing by around 2% QoQ. Deposits in its ASEAN portfolio has increased by around 12% YoY. Furthermore, while its NIM declined by 8 basis points on a QoQ basis, it was still up by around 56-basis points on a year-over-year basis. Nevertheless, the bank's NIM seems unlikely to increase substantially in the near future in light of the repricing of deposits in its key Singapore market.

The key earnings growth factor in the months ahead will come from a growing ASEAN portfolio and the bank's continued success in achieving a lower cost-to-income ratio rather than NIM expansion. The bank's cost-to-income ratio (excluding one-off expenses from the acquisition) declined by 1.7% in the first quarter of 2023 on a QoQ basis and 3.9% on a YoY basis. The bank expects to reduce its cost-to-income ratio to below 40% from its current 40.9% in the full year. This would also ensure that UOB's cost-to-income ratio is more closely aligned with that of its peers.

Valuation

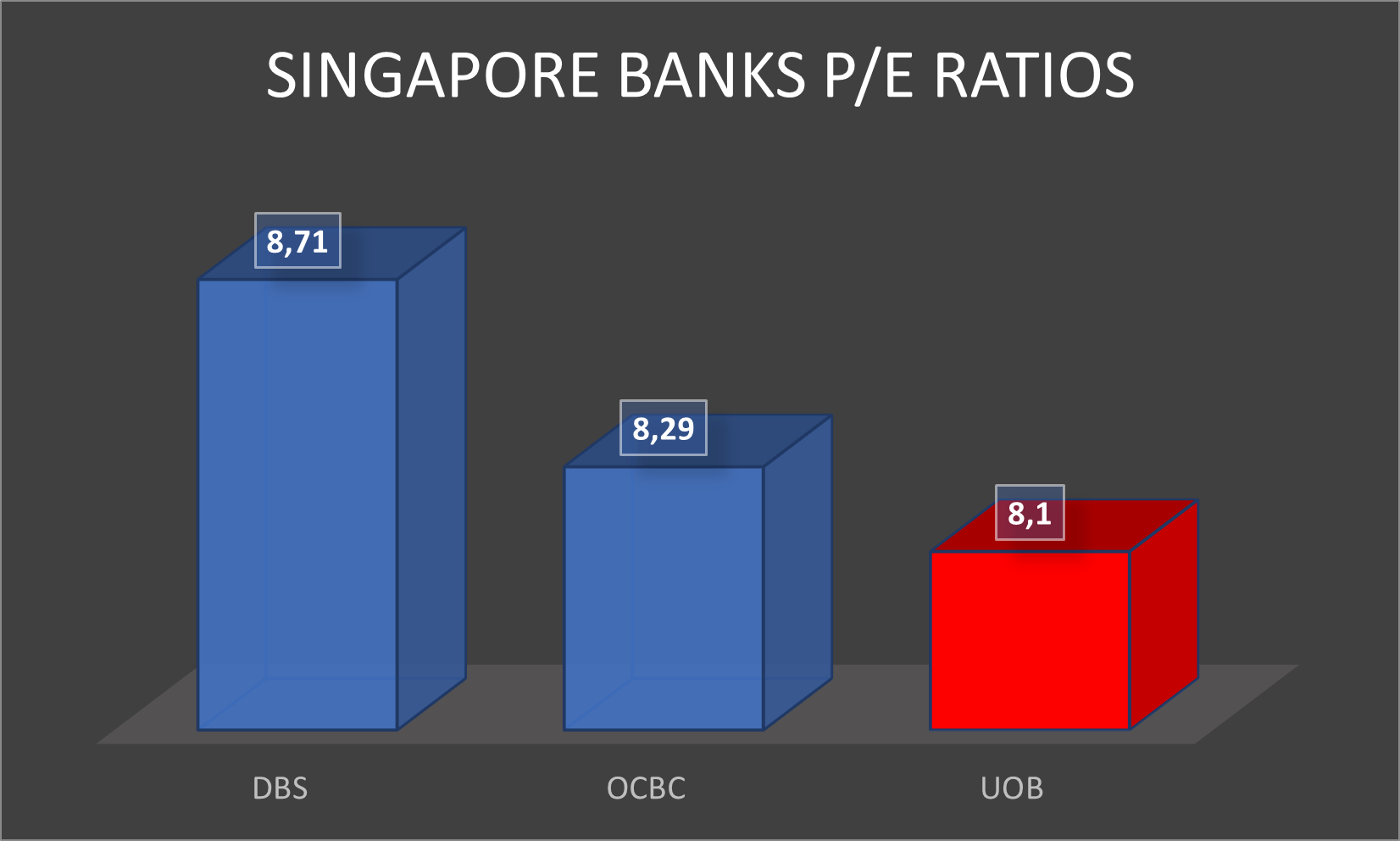

UOB trades at an undemanding valuation with a forward P/E ratio of 8.1, which is the lowest of the three major Singapore banks. It is also well below the bank's 5-year average P/E ratio of around 11 times forward earnings.

Singapore Banks P/E Ratios (Author created chart based on data from marketscreener)

{kind=link}

While the share is trading above book value, this is not concerning for a bank which maintains a high return on equity ((ROE)) and return on assets ((ROA)). Its forward Price-to-book value is currently at 1.03, which compares well to peers such as OCBC and is well below the 1.41 times book value for DBS.

Singapore Banks P/B Ratios (Author created based on data from marketscreener)

{kind=link}

The bank also offers a strong dividend yield, with its forward dividend yield around 6.23%, which is only slightly lower than that of OCBC. The dividend yield also appears to be sustainable in light of the bank's strong capital position discussed earlier and the bank's dividend policy of returning around 50% of earnings to shareholders.

Singapore Banks Forward Dividend Yield (Author created chart based on data from marketscreener)

In my analysis, a slight discount to the bank's 5-year average P/E ratio is partially justified by the integration risks. The fact that the bank's share is not trading substantially below its 5-year average price-to-book value also points to the stock not being severely undervalued. On a forward P/E ratio of around 10, the Singapore-listed stock has a value of around SGD 33 (around $49 for the US-listed ADR), which is around 17% above its current price per share. This then also implies a forward P/B ratio of around 1.2, which is broadly in line with its 5-year average.

Key Risks To The Investment Thesis

The successful integration of Citigroup's consumer banking businesses in Indonesia, Malaysia, Thailand, and Vietnam is critical to realizing the growth potential from the acquisition. Delays or difficulties in integrating these businesses could result in operational challenges, and reduce the overall benefit to investors to be derived from the acquisition.

Furthermore, while UOB maintains a reasonable NPL ratio, any deterioration in asset quality due to factors such as economic downturns, industry-specific risks, or borrower defaults could lead to higher provisioning and negatively impact the bank's earnings. A sudden increase in NPL formations would also have a material impact on the analysis, which currently foresees a continued slowing down in the pace of new NPL formations.

Conclusion

In conclusion, United Overseas Bank Limited presents a compelling investment opportunity based on its growth prospects, strong capital position, improving asset quality, and competitive dividend yield. The recent acquisition of Citigroup's consumer banking business in key Asian markets positions UOB for significant growth in the coming years while diversifying its portfolio. Despite some associated risks with the acquisition's execution, the bank's undemanding valuation makes it an attractive choice for investors seeking both long-term growth potential and stable dividends. As UOB continues to demonstrate solid performance and expands into high-growth markets, investors may find it an appealing addition to their portfolios, offering the potential for favorable returns and good dividend payments over time.

For further details see:

United Overseas Bank: Attractive Growth Potential And Dividend Yield