USM - United States Cellular Is Priced Above Likely Sale Value

2023-12-16 04:09:39 ET

Summary

- US Cellular's wireless business continues to struggle with declining volumes and stagnant rates.

- Bottom-line growth is driven by short-term levers, indicating a potential setup for a sale.

- The market cap of US Cellular exceeds its potential sale price, suggesting overvaluation and limited upside potential.

I am following up on my Q1 thesis for the United States Cellular ( USM ) in light of Q3 earnings and the announcement of the parent company looking to sell.

Previously, I rated US Cellular a sell, noting the following:

- Their well-articulated but poorly executed strategy wasn't working in the market, with rate and volume metrics deteriorating.

- The financials and weak balance sheet did not support the level of 5G investment needed to keep up with Verizon, AT&T, and T-Mobile.

- I felt the most likely scenario was a buyout for spectrum, but with elevated valuation multiples, even in this scenario, shareholders would likely come out below the current price.

Since my last analysis, US Cellular is up 181% on the back of an announcement that parent company TDS was looking for " strategic alternatives " for this business.

USM Share Price (Seeking Alpha)

{kind=link}

Clearly, my last analysis did not account for the timing of the announcement or the market reaction. However, the announcement has now driven the stock price above what I believe is a potential sale price. In addition, the wireless business continues to struggle, and bottom-line growth came largely from short-term levers to make the company attractive to buyers. I continue to rate US Cellular a sell, especially if you entered the stock prior to August 2023.

Wireless Business Continues To Struggle

Despite putting an aggressive strategy on paper, US Cellular's wireless business continues to struggle across key metrics.

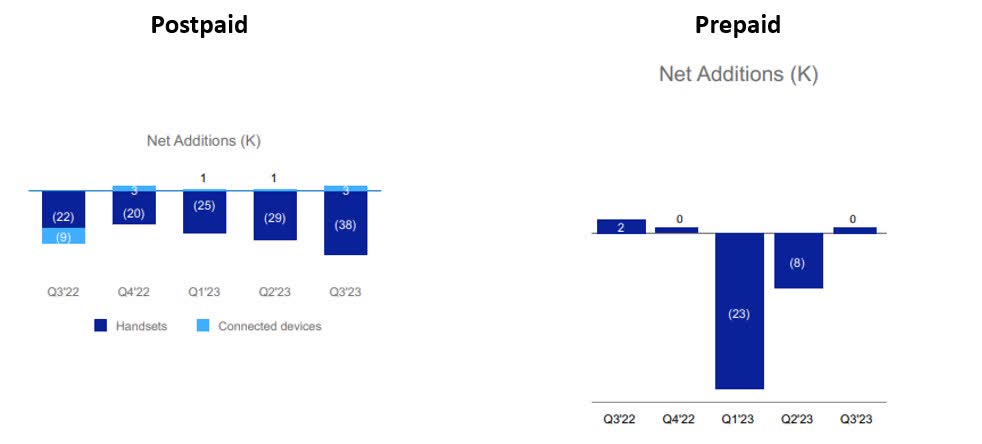

On the volume side, postpaid volumes continue to decline at an accelerated rate and prepaid volumes have stagnated.

Wireless Volumes (USM Investor Relations)

{kind=link}

Things aren't much better on the rate side. Postpaid ARPU was only up 2% year-over year. Despite management congratulating themselves in the earnings call for moving customers to premium plans, this growth actually fell behind the overall industry by over 2ppt.

ARPU (USM Investor Relations)

Prepaid ARPU fared even worse, falling 4.5% from $35.04 to $33.44.

The only brightside in the business was fixed wireless subscribers, but this represents less than 5% of overall subscribers and can't offset much of the pain in the rest of the business.

Fixed Wireless (USM Investor Relations)

Sale or no sale, the long-term value of the business will continue to deteriorate, and management's strategy isn't moving the needle.

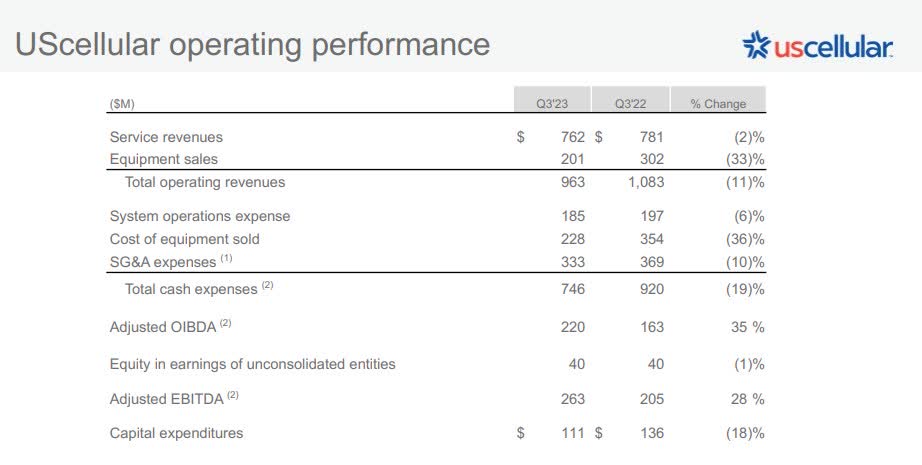

Bottom-Line Growth From Short-Term Levers

In the earnings release, management touted the following Highlights:

-Increased profitability

-Net income, Adjusted OIBDA, Adjusted EBITDA up significantly

-Growth in cash flows from operating activities and positive free cash flow

Digging into the results, profitability improvements seem to be more than what is reasonable for ongoing operations, and I believe management is merely setting up for a sale.

Profitability (USM Investor Relations)

{kind=link}

Despite inflation of 5%+ across telecom expense, US Cellular decreased systems operations expenses by 6% and SG&A by 10%. Per the earnings call, systems operation was driven by a reduction in off-network roaming, while SG&A was driven by a decrease in bad debt as well as a workforce reduction. This cut puts US Cellular on a similar % of revenue to T-Mobile despite a much smaller scale.

Despite an aggressive growth strategy on paper, these cuts represent a bare-bones approach to the business. Not to mention the 18% reduction in CapEx that reflects lower investments in the future.

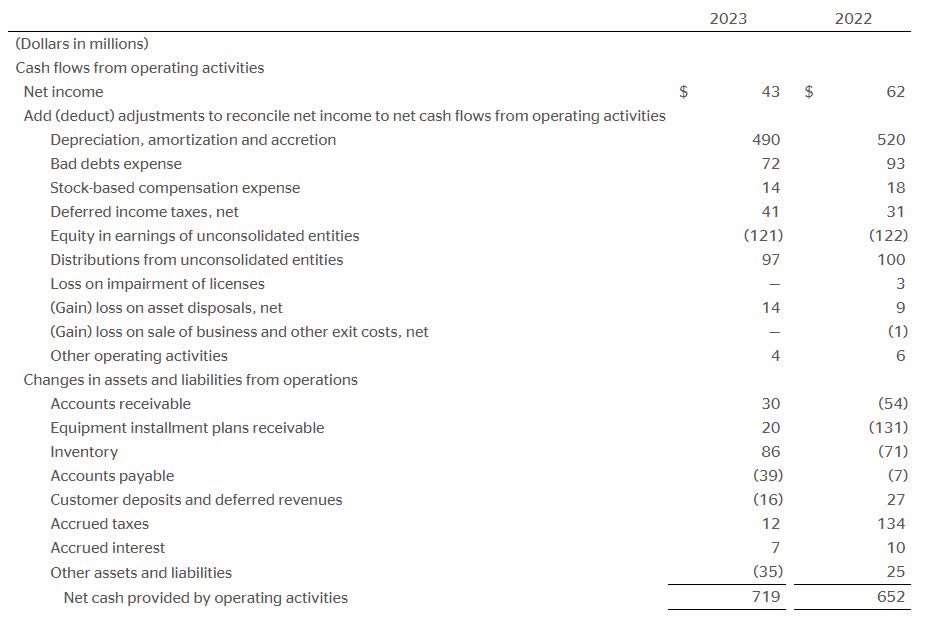

In addition, free cash flow improvement was largely on the back of a change in receivables, not an operating improvement. Operations were largely a drag on FCF.

Cash Flow From Ops (USM Investor Relations)

{kind=link}

US Cellular is not growing, and is not setting themselves up for the future.

Market Cap Exceeds Potential Sale Price

As shown above, US Cellular currently has a market cap of $3.4 billion. With that in mind, I wanted to figure out a potential sale price.

Starting on the balance sheet , tangible book value is negative so nothing to go from there. The book value of intangibles (spectrum) is $4.7 billion, less $3.7 billion of long-term debt and leases, which would yield a $1.0 billion value floor for acquisition.

Comparable small teleco's is the best to look at for a purchase premium. Using Verizon as an example of a possible acquirer due to their recent, public deals.

Verizon bought Bluegrass for ~$400 million (not disclosed but looked at payout from Q1 2021 10-Q). Bluegrass had an estimated revenue of $91 million, 210,000 customers, and at least 30 spectrum licenses.

Verizon bought Tracfone for slightly north of $6 billion dollars. Tracfone had over 8 billion in revenue and 20 million customers, but no spectrum.

Given the spread between revenue multiples, the spectrum is the value driver. So how does Verizon value spectrum? In 2021 Verizon paid $45 billion at a C-band auction for 3,500 licenses or $13 million per license.

Between revenue, customer, and spectrum valuation, USM is worth $2.8-3.0 billion.

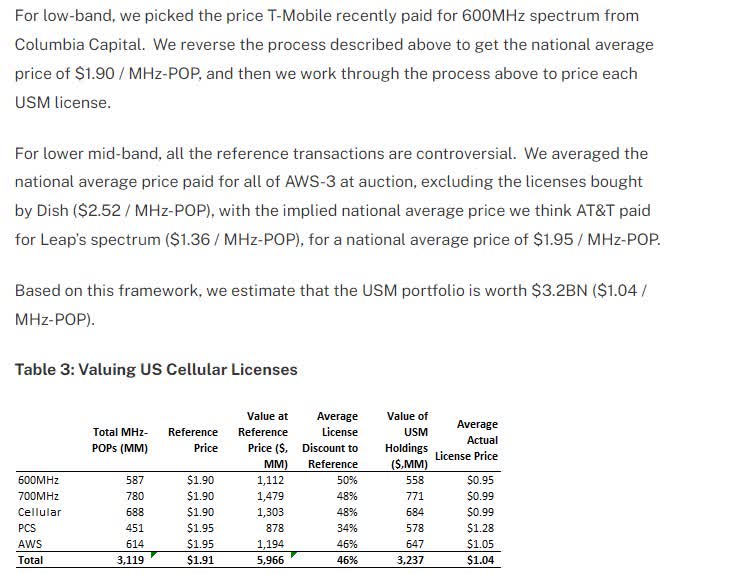

New Street Research did a valuation based on Millihertz per Population and came to a similar value of $3.2 billion.

Spectrum Valuation (New Street Research)

{kind=link}

Merging the two analyses, I believe US Cellular has a target price of $35 or 12% downside from today's pricing.

Upside Potential

Similar to my Q1 analysis, the best-case scenario is a buyout where more than one telecom is interested in US Cellular's spectrum. Then, a bidding war could result in a premium being paid on the current valuation. With no dividend in the interim, shareholder return is entirely dependent on

Verdict

In conclusion, I believe that US Cellular's value, underpinned by the value of its spectrum licenses, customer base, and revenue, is estimated between $2.8 and $3.2 billion. This valuation, corroborated by independent research from New Street, points towards a target price of $35, marking a potential 12% downside from current rates.

The only potential upside is based on a speculative bidding war scenario. Moreover, without a dividend distribution, any shareholder return hinges solely on price appreciation. Given the overvaluation and lack of dividend yield, I recommend investors exit their positions, especially if they purchased prior to August 2023.

For further details see:

United States Cellular Is Priced Above Likely Sale Value