UTHR - United Therapeutics: Eyeing A Re-Rating To 12-13x P/E Growth More Than Justified

2023-08-03 17:41:54 ET

Summary

- United Therapeutics Corporation (NASDAQ: UTHR) reported strong quarterly results, adding strength to its economic characteristics.

- The company's financial performance and cash flows indicate the potential for sustained high returns on operating capital employed.

- I am eyeing $273/share, or 12.6x forward P/E by FY'23 yearend.

- Net-net, reiterate buy.

Investment briefing

United Therapeutics Corporation (NASDAQ: UTHR ) pulled in with a strong set of quarterly results before the open yesterday. Following my May profiling of UTHR the company's equity stock has caught a reasonable bid, and the latest set of numbers adds to an already impressive set of economic characteristics in my opinion.

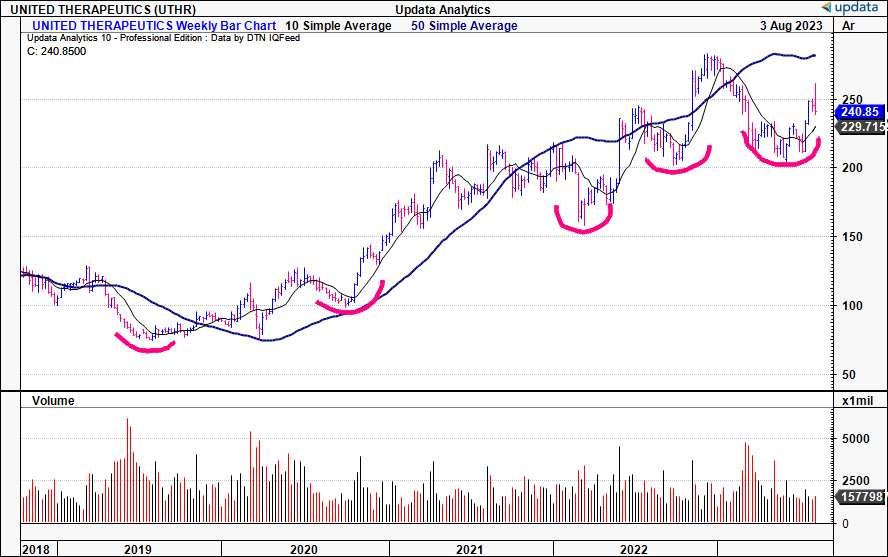

Buying UTHR on sharp corrections has proven to be a bold but profitable move for those with the intestinal fortitude to ride through the volatility [Figure 1]. I'm eyeing UTHR to drive out of this most recent correction and potentially rally back to former highs, after a difficult few months on the charts.

Figure 1. UTHR long-term price evolution

{kind=link}

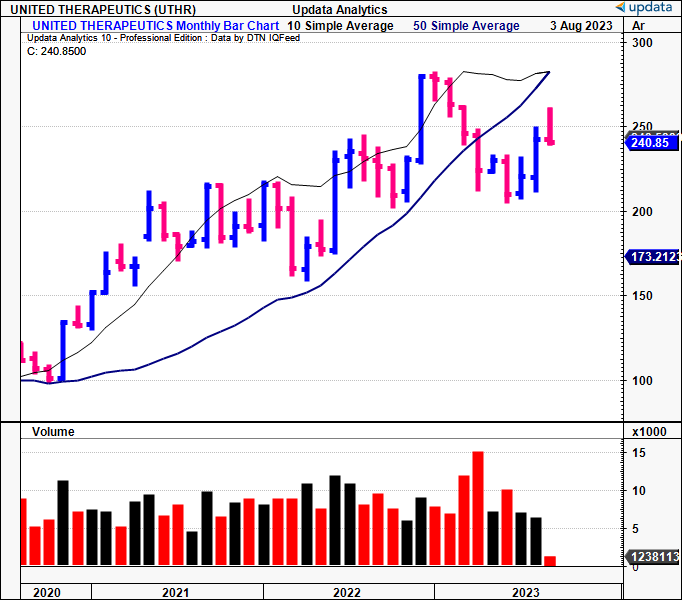

Below you have 3-years of price action shown in monthly bars. You can see through the FY'22 bear market UTHR caught a heavy bid, in line with its resiliency premium, and economic drivers of shareholder value. The last 3-months have been incredibly important in this regard, having bounced from the key support of $200. It found buyers at this range back in FY'22, then rallied some $70/share at the peak. This analysis will run through why I believe UTHR can push to that level again.

Figure 2. UTHR Price evolution—monthly bars

{kind=link}

Critical facts adding to buy thesis

UTHR is one for those aiming to collect long-term capital gains without the major worries of holding a stock that long through various market cycles. For one, on a forward looking basis, my numbers have UTHR performing well, financially, and economically. Second, once you sift through the company's numbers and extrapolate the kind cash flows it is throwing off to shareholders, it is abundantly clear that UTHR has propensity to sustain a high return on operating capital employed. Added to this, should UTHR maintain these levels of profitability, it has stockpiles of cash [and equivalents] to commit and put to work in growing the business.

1. Q2 financials evidence the kind of fundamental momentum to position against

Picking apart its latest numbers, UTHR clearly outshone in the 2nd quarter. It posted record Tyvaso sales, and came in with $596mm at the top line, up 28% YoY. It pulled this down to $313mm in operating income and $259mm in earnings. Given it employs no leverage, you've got high FCF conversion and $5.68Bn of equity holding up $6.68Bn in total assets—very attractive claim on the firm's capital from equity holders in my view. It also helps with rates sensitivity going forward.

As a reminder, the company is looking to being doing $4Bn of business by FY'25-'26, calling for a 24—38% compounding growth in sales over this time. The 28% revenue growth from Q2 last year remains within this performance band.

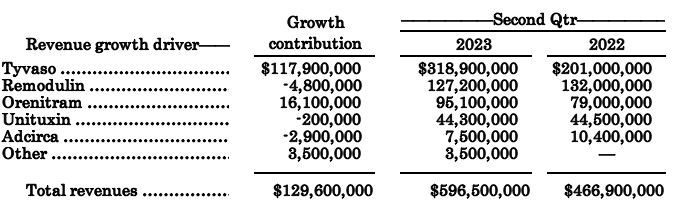

Further breakdown on the top-line saw the following revenue growth drivers in action:

- Treprostinil-based products, including:

- Tyvaso;

- Remodulin; and

- Orenitram;

- ;were up 31% YoY and contributed another ~$129mm to the top line.

- Critically, the bulk of Tyvaso's numbers were demand (volume) driven. More than $117mm of Tyvaso sales were booked through UTHR's distributors, but ~87% of this was specifically tied to patient uptake.

- Hence, only ~13% of this upside was inventory (supply) and/or pricing.

Figure 3.

{kind=link}

There are further bullish points to consider with the Tyvaso DPI segment as well. For one, on the supply side, the company has partnered with MannKind. Critically, management reported that MannKind has completed a production expansion and "process improvement" overhaul.

Management expect these moves will increase Tyvaso's production capacity by around 250% going forward. That says a lot for the kind of sales growth to expect from UTHR into the next few years. It is aiming for $4Bn in sales, and a 250% increase in Tyvaso revenues from Q2 FY'23 gets you to c.$1,116.9Bn in quarterly sales alone (318.9x(1+2.5) = $1,116.9).

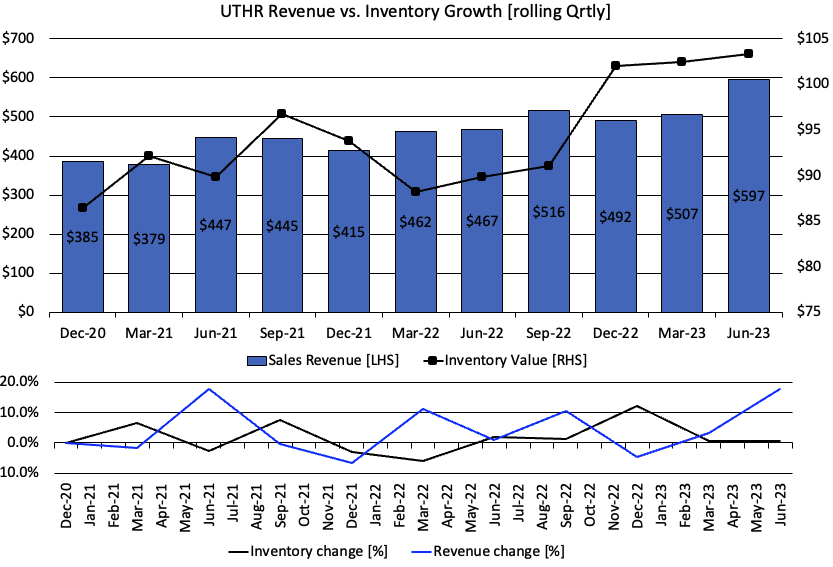

An important point to consider here is that UTHR will need inventory to fulfil this capacity and expected demand-pull. To date you can see the pace of inventory matching sales growth, suggesting it isn't pulling sales forward and booking these too far in advance. From September last year, you can see the strategic inventory purchases of ~$30mm of its Tyvaso DPI inventory through its deep network of specialty pharmacies.

Figure 4.

{kind=link}

2. Capital deployment, high returns on capital deployed supported by heavy reinvestment

The company has 3 focus areas for capital deployment in the coming periods, each with opportunistic outcomes.

One, it hopes to pile back cash into current operations for all the right reasons—efficiencies, increasing capacity, and all other internal projects. In Q1 it mentioned commitments of ~$500mm towards its Tyvaso DPI production facility in North Carolina, which looks to have been reflected throughout the P&L last period.

Two, it looks to build out further production capacity for its xenokidneys and xenohearts segments. You'd expect UTHR to build or acquire a pathogen-free facility to adhere to the FDA's standards here as well, so this would appear to be a necessary step to really get these segments off the ground and running. There hasn't been much talk of acquisition activity, and I for one am all for that. I don't believe it's the right environment and this is supported by how UTHR is moving ahead by recycling its own profits back into capital growth. It also didn't rule out the possibility for buybacks either.

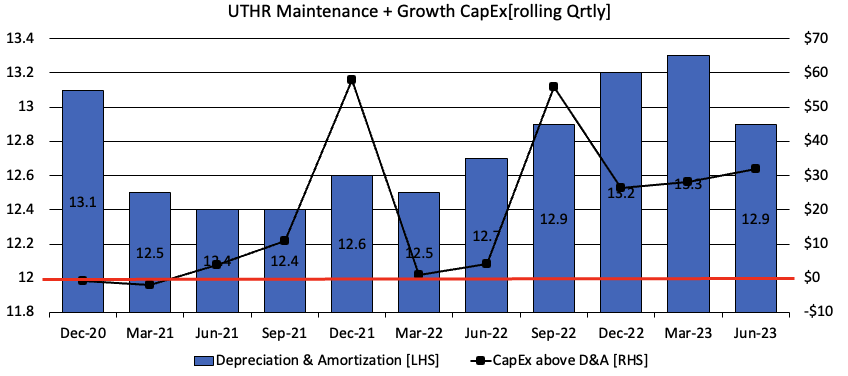

Back to the company's growth investments, you can see the approximation of growth CapEx to maintenance CapEx below [Figure 5]. I've used quarterly depreciation and amortization numbers as the capital charge on maintenance CapEx, and subtracted this from the firm's incremental spend on tangible/intangible assets. Notably, this is trending higher over time, with an additional $32mm last quarter ($128mm annualized) in growth CapEx deployed to expand the business. Given the kinds of returns it sees on its capital budgeting (discussed below), this is a bullish sign in my view.

Figure 5.

{kind=link}

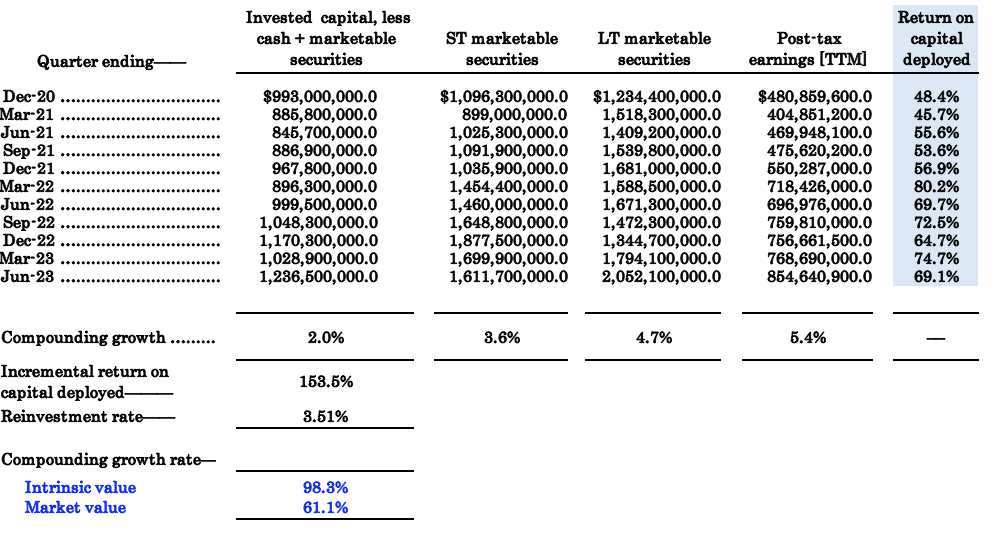

In my view you've got to perform several adjustments to get a feel of the UTHR's ability to compound its intrinsic valuation going forward. I've gone back to Q4 FY'20 to do this [Figure 6] and looked at rolling TTM periods, for a 12-period look-back window. It had ~$4.9Bn in capital commitments by the end of last quarter.

You'll note that UTHR is asset-heavy on marketable securities, both available-for-sale and held-to-maturity. These are a mixture of ST/LT treasuries, with some corporate debt in there as well, ~$660mm on fair value. Liquidity is therefore not even a considered issue in this case. It had ~$3.66Bn [recorded at fair value] of marketable securities on the balance sheet last quarter. You can see the rotation of cash into its money market assets during FY'22 as a liquidity grab on the repricing of rates. Good move in my view. Net-net, it's made a time-weighted gain of ~7% on these assets from 2020, notwithstanding the yields earned.

Hence, I've stripped these out as non-operating assets and looked at the capital actually deployed into generating economic profits. This looks to be ~$1.24Bn at present. You'll note it generated 69% trailing return on capital deployed last period—this comes from $854mm in post-tax earnings produced on this $1.24Bn of operating capital. Looking back across the testing window, you can see similar growth, and, ~21 points of additional return on capital (69.1% - 48.4% = 20.7%).

Figure 6.

{kind=link}

These are tremendously attractive business economics in my opinion. It is averaging 20% returns on capital deployed per quarter as well, indication of the sustainable growth rate looking forward.

The benefits to shareholders on this—plenty. For one, you're looking at 57% spread over the market's long-term return on capital of ~12%. Then, you've got to consider that UTHR has piles of cash flow on hand ready to deploy back into the business.

One of the issues to this point is that it hasn't really been utilizing this tool to its full advantage, in my view. I've got mixed opinions here. On the one hand, you can clearly see the rush to cash (via the marketable securities column below) during FY'22 in Figure 6. That was prudent capital budgeting in my view, as mentioned previously. It also reduced capital density and clipped ~$71mm of operating assets in Q1 last year.

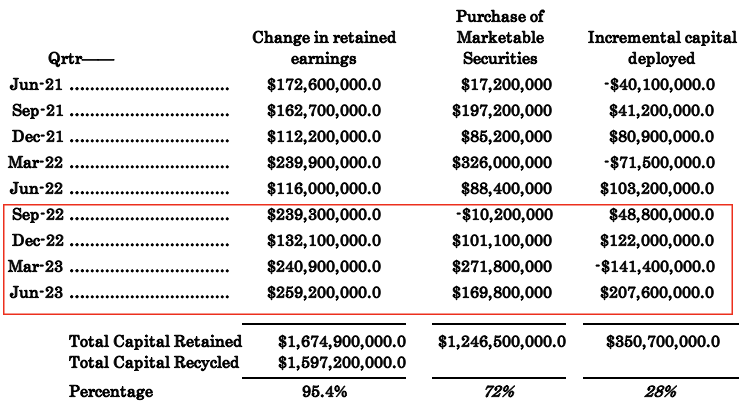

You can also see UTHR has been withholding ~$150—$200mm from investors in retained earnings, on average, since FY'21. It has withheld more than this average since Q3 last year.

Specifically, it has pulled in an additional $871mm in retained capital over this time, reinvested $532.5mm in the purchase of more marketable securities, and put $237mm to work as operating capital [I would also state that the securities calculations are rough given the change in fair value with yield spreads this year. We still get a reasonable approximation] . Over the look-back window, it has recycled ~95% of the $1.67Bn in shareholder capital (retained earnings) back into 1) liquid investments or 2) business growth [Figure 7]. Of this, it looks as if ~72% of the full retained capital has been put towards non-operating assets, whereas just ~28% has been deployed back into the business.

There is where I am on the fence. I would have expected more emphasis on growing operations than growing liquidity over this period. Especially with such tremendous returns on capital deployed.

But in the same breath, It is producing such tremendous rates of return off such a relatively small capital base. The capital intensity on this is superb, up from 1.5x turnover to 1.7x turnover on TTM numbers, on post-tax margin growth of 32% to 40% in this time.

The point being I would prefer to see UTHR recycling more of its profits directly back into the business, but am content noting the tremendous returns on capital deployed produced each quarter.

By all measures, I believe these trends can continue going forward. This is significant, because UTHR in my eyes is undervalued given the market pays just 61% higher market value than 3-years ago, but I've got the firm having compounded its intrinsic value by ~98% over this time [Note: Compounding growth rates, Figure 6, above].

Figure 7.

{kind=link}

Valuation

Investors are parting with their UTHR stock at 10.8x forward earnings and that's a steal in my eyes. With ~35% projected earnings growth next year you get to a PEG ratio of 0.4x when paying this multiple, reducing the payback period immensely. I've got the company pushing ~70% returns on existing capital and ~50% on new capital commitments over the coming 6 to 12-months [Figure 8]. It wouldn't be unreasonable to see ~30% growth in owner earnings to ~$750—$790mm on these projections in my view. I get to this from projections of $1.042Bn in NOPAT less ~$250mm additional investment for growth.

Figure 8.

Data: Author Estimates

Should this be an accurate set of projections, it would call for:

- UTHR to reinvest ~24% of forecast post-tax earnings for H2 FY'22;

- To produce total post-tax income of ~$1.042Bn this year, as mentioned, off $1.485Bn in capital deployed, getting to 70% ROIC;

- An additional $187.6mm in earnings off ~$250mm investment;

- Therefore, as a function of the company's ROIC multiplied by the reinvestment rate, for UTHR to compound its intrinsic value at 17% into FY'23 yearend (0.24x0.7=16.8%).

This would get me to $273 per share in equity value if entering at today's market price at the time of writing. This equates to a fair forward P/E of 12.6x, and thus supports a buy rating in my view, suggesting UTHR is undervalued trading at just ~10x earnings, a 26% value gap to the upside.

Conclusion

Based on UTHR's robust economic characteristics, I am retaining a buy on the company's equity stock. It continues to demonstrate defensible business economics via superb returns on capital deployed and spinning mountains of free cash flow off to its shareholders. I would like to see it allocate more heavily towards operational growth, but am also cognizant that it is producing these cash flows off a relatively light capital base. This is the kind of business that interests me immensely. For one, capital doesn't necessarily produce the profits. Meaning UTHR can grow earnings with small increments of investment to do so. This is also sustainable and gives visibility for growth down the line.

In that vein I've got UTHR at $273/share as the next objective, getting me to 12.6x forward earnings, roughly 26% upside from the market's current pricing of 10x. Net-net, reiterate buy.

For further details see:

United Therapeutics: Eyeing A Re-Rating To 12-13x P/E, Growth More Than Justified