UNIT - Uniti Group: A Potential Value Trap

2023-10-10 03:32:13 ET

Summary

- Skepticism about buying Uniti Group Inc. due to weak financial footing and lack of growth prospects.

- High debt risk and potential financial distress pose significant concerns for the company.

- Ownership structure could be a potential catalyst for volatility, leading to fluctuations in stock price and performance.

- Based on the weak fundamentals, I believe the current valuation is a potential value trap, and as a result, it calls for patience for the company to turn around things and improve its financial footing.

Investment Thesis

Despite being relatively undervalued and trading in the support zone, which offers a good entry point, I am skeptical about buying Uniti Group Inc. (UNIT) at the moment. My skepticism stems from the company’s weak financial footing and growth prospects . Further, on evaluating the company’s current ownership structure , I find it a potential cause of volatility, which also calls for my patience before investing in this company.

Although some investors may be carried away by the current valuation and invest here, I tend to believe this current valuation is a potential value trap. In my view, we need patience to wait for the company’s fundamentals to improve before leveraging on the current valuation. Otherwise, if the company’s fundamental doesn’t improve, the shares may experience further downward pressure, forcing the prices down. Given this background, I rate UNIT a hold as we wait for the company’s fundamentals to improve.

Financial Footing: High Debt Risk And Potential Financial Distress

The financial strength metrics for UNIT give me considerable cause for concern about the state of the company’s balance sheet. With an interest coverage ratio of 1.32 , the company fares lower than 84.34% of the 664 firms in the REITs sector. This ratio illustrates potential problems the corporation may encounter while dealing with interest expenses on existing debt relative to its peers. Furthermore, given the importance of free cash flows in debt repayment, I am concerned about UNIT’s negative levered free cash flows. Furthermore, its cash flow from operations of $425.34 million is minuscule compared to its total debt of $5.49 billion, translating to coverage of 7.7%. In my opinion, this indicates a significant debt risk.

Furthermore, the company’s low cash-to-debt ratio of 0.01 shows a problem with existing debt levels. Again, its debt-to-Ebitda ratio is 8.99, which is above the maximum acceptable zone of 3- 4 and worse than 62.64% of the 530 REITs firms. In summary, I believe UNIT is in a very poor financial position, with a substantial debt risk. Furthermore, the company’s detrimental financial standing is confirmed by its Altman Z-Score of negative 0.84, which is below the distress zone of 1.81. This implies that the company may suffer financial distress in the coming years, providing a significant risk of investing here.

Growth: Not Promising

Another area where Uniti appears to stumble is a lack of considerable growth, as indicated by the company’s low growth grades. Over the last three years, the company’s revenue has decreased by about 5.3% per year. To summarize the company’s poor growth grades are the figures below.

Seeking Alpha Seeking Alpha

In my opinion, the company’s financial woes can be attributed to the COVID-19 challenges, which caused supply chain disruptions. Further, the declining profitability could result from increased costs due to an inflationary macroeconomic environment. Above all, I believe a legal dispute with Windstream Holdings , one of its largest customers, has played a significant part in the company’s financial woes. Windstream filed for bankruptcy in 2019 after losing a legal dispute with Aurelius Capital Management, a hedge fund that accused it of violating its bond covenants. This, I believe, affected UNIT substantially. Considering these contributing factors, I still believe the company’s financial outlook is bleak since the current macroeconomic environment is very tough, putting pressure on its weak financial footing discussed earlier.

Ownership Structure: Potential Volatility Catalyst

On evaluating UNITI’s current ownership structure, I find it a potential cause for volatility. To validate this, I will cover some of its major shareholders and how they may cause volatility. To begin with, the biggest owner is Vanguard Group, an investment management company that owns about 16% of the company’s shares. The company is known for its passive investing strategy , which means that it does not actively engage with the management or influence the company’s direction. Vanguard may also change its allocation or rebalance its portfolio at any time, depending on its market conditions and objectives. In my view, this poses a major volatility risk for UNIT, especially considering its weakening fundamentals, which can trigger Vanguard to reevaluate its stake in the company.

The company’s other significant shareholders include various institutional investors, hedge funds, and retail investors, who own about 24% of the company’s shares. In my view, these shareholders may have different interests, expectations, and time horizons for the company. They may also react differently to the news and events related to the company or the industry, creating more volatility in the stock price.

In conclusion, these factors make the company’s ownership a potential catalyst for volatility, as any changes or uncertainties in its shareholder structure could cause significant fluctuations in its stock price and performance. The company’s stock price has been highly volatile in the past year, ranging from $2.94 to $8.04 per share. Given the current weak financial footing and weak growth prospects, these investors may react by slashing their stake in the company, which I believe will be detrimental to its share prices. The company’s implied volatility, which measures the expected price movement of the stock based on the options market, is also high at 68.8%, compared to the industry average of 38.28%

It’s Not All Bleak Here

Despite my skepticism about this company, it appears to have some qualities that could perhaps turn things around. Some of these factors are addressed in this section. To begin with, the company is expanding its portfolio. UNIT is expanding its fiber network and data center portfolio, both organically and through Uniti Group Mergers and Acquisitions Summary , to increase its customer base, revenue, and market share in the fixed-income trading space. The company has a large and diverse network of over 135,000 route miles of fiber and 37 data centers across the US.

Another positive aspect is its revenue generation diversification. The company is diversifying its revenue streams and reducing customer concentration risk by entering new markets and segments , such as wireless backhaul, cable, enterprise, and government. The company also plans to expand its international presence in Latin America and Europe.

Relative Valuation And Technical Analysis

Based on relative valuation metrics, UNIT appears to be undervalued. With nearly all its relative valuation metrics below the industry median, it appears that the company is trading at a discount.

Seeking Alpha

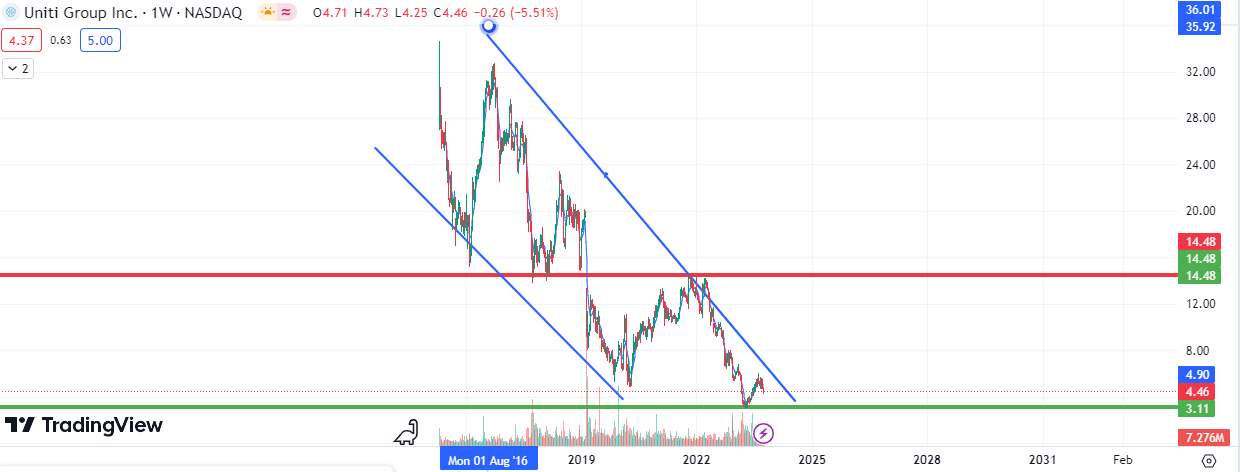

I believe the current undervaluation may be due to the weakening fundamentals, specifically its weak growth prospects and financial footing. Further, from a technical perspective, the stock seems to have dropped to its support zone, which marks a good entry point.

{kind=link}

Based on the above figure, the stock has bounced off the support zone at about $3.11 per share; however, the price seems to return for a retest, which could break the support zone and continue with the downward trend marked by the blue lines. The possibility of a breakout is high, given the stock’s weak fundamentals.

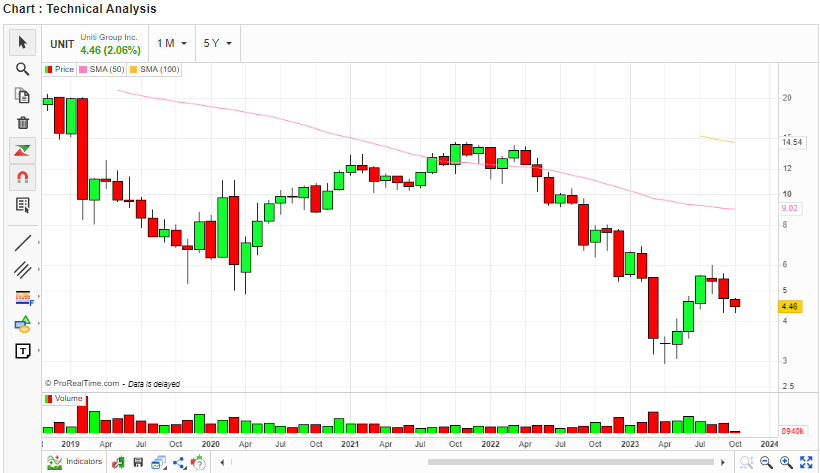

Further, using another indicator to judge the situation, I have focused on the 50 and 100-day moving averages. UNIT is trading way below its MAs, a sign that the company is in a strong bearish momentum, and therefore, this nullifies the current support zone as a potential entry point.

{kind=link}

In my view, I expect the stock to break this zone during the retest and continue with its downward trend to form a new support zone, perhaps when its fundamentals improve.

In conclusion, given the company’s weak fundamentals, the current undervaluation, as evidenced by the technical analysis, isn’t a good entry point but a potential value trap. Investors should wait for a better entry point, perhaps when its financial strength and growth prospects improve.

Conclusion

In conclusion, the bearish trend verified by the price trading below its MAs suggests that the current price is a potential value trap for investors in UNIT. Unless the company’s fundamentals strengthen, I anticipate the current trend will continue to decline. The company’s development of its product line and diversification of its sources of income are encouraging indicators, though. Nonetheless, I believe that these turnaround initiatives are long-term in scope, and as a result, I see a grim short- and medium-term picture for the company. Investors should be patient in light of this history as we closely monitor the company to identify and address the causes of its problems, most notably its tenuous financial footing.

For further details see:

Uniti Group: A Potential Value Trap